ACM Research, Inc. (ACMR) updated its full-year 2025 revenue outlook on Thursday.

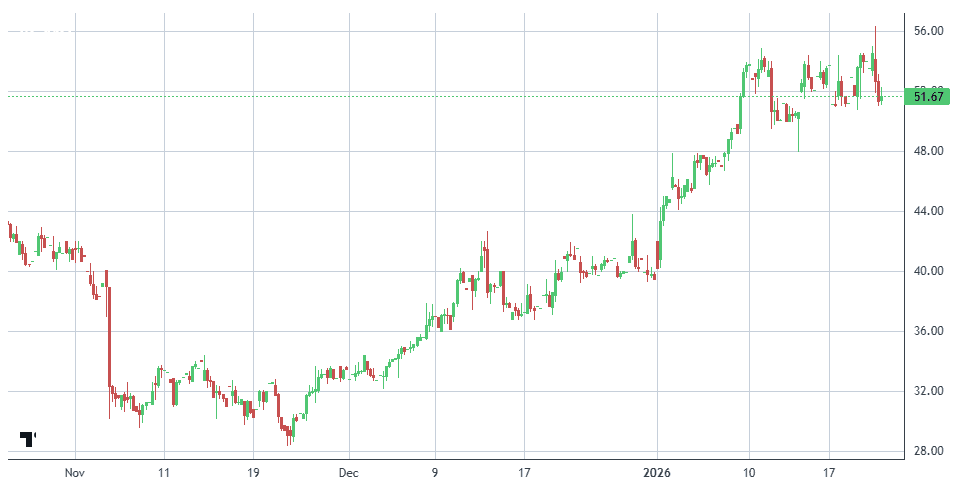

Shares fell 4% in market trading after closing at $53.45 on Wednesday, marking a 4.48% drop.

We’re taking a closer look at the update and why we remain long ACMR, despite the sharp run-up in such a short period.

ACM Research has had a strong run since our entry, up 57.34%, but we still see room ahead.

ACMR owns a 74.6% stake in its China subsidiary, valued at roughly $14.65B, while the U.S. parent trades at just a $3.32B market cap.

That valuation gap remains meaningful, even after the stock’s sharp move higher.

While ACMR shares are up over 170% in the past year, the underlying business strength and exposure to wafer-cleaning technology continue to justify a premium.

The stock has been accelerating quickly and recently crossed $50.

Volatility is a given, especially if the AI trade cools, but we still view ACMR as undervalued relative to its Asia listing.

With the next semiconductor capex cycle approaching, we like the risk/reward here and are upgrading our sell target from $48 to $64.

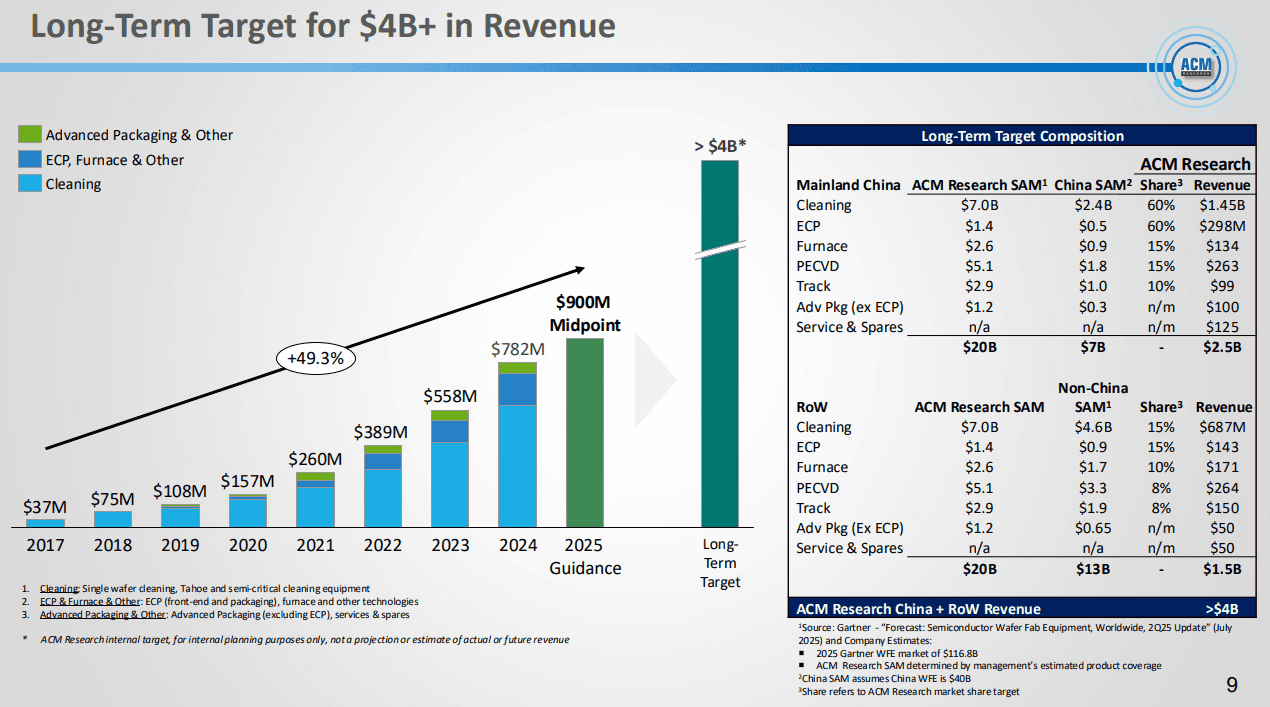

ACM Research updated its full-year 2025 revenue outlook, narrowing guidance to a range of $885–$900 million, compared with the prior range of $875–$925 million provided in the company’s Q3 2025 earnings release on November 5.

While the range was tightened, the midpoint remains largely unchanged, signaling stable underlying demand rather than a deterioration in the business.

More importantly, ACM introduced its initial outlook for 2026, guiding revenue to $1.08–$1.175 billion.

This forward view reflects management’s assessment of international trade policy impacts, customer spending patterns, supply-chain constraints, and the timing of tool acceptances currently in field evaluation.

Taken together, this implies continued top-line growth into 2026 despite a more complex macro and geopolitical backdrop.

The company plans to report fourth-quarter and full-year 2025 results in late February 2026. Management emphasized that the 2025 revenue figures remain preliminary and subject to final audit review, but the updated guidance reinforces our view that ACM’s long-term growth trajectory remains intact.

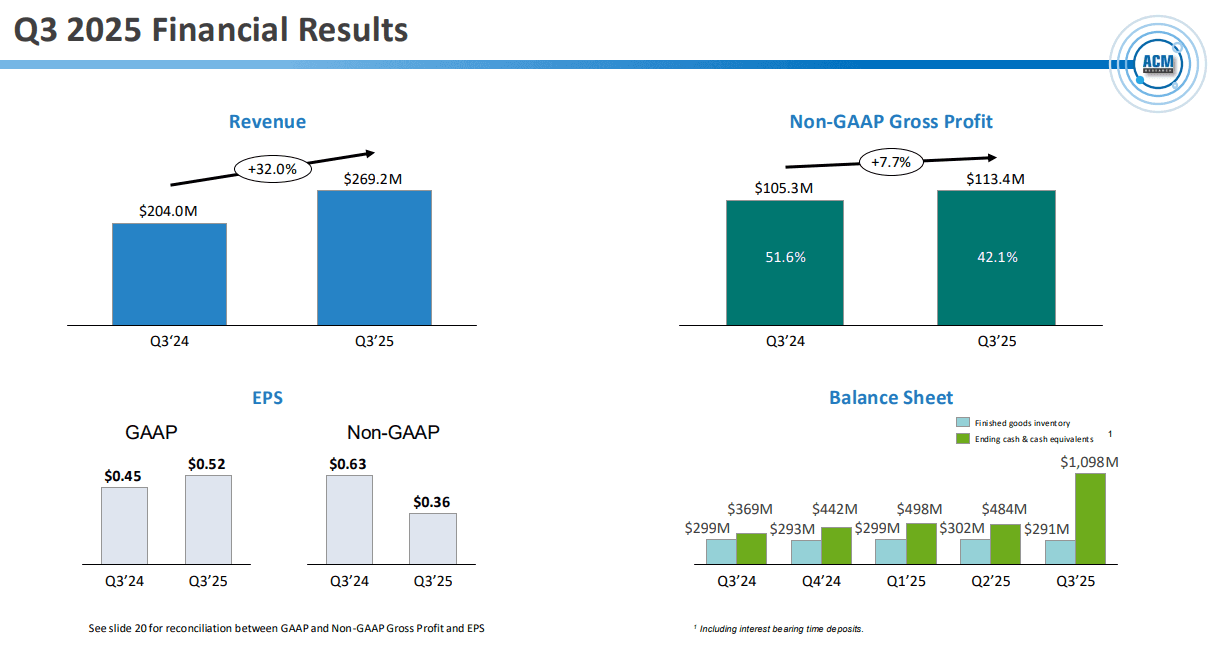

ACM Research reported quarterly revenue of $269.6 million and earnings per share of $0.36, a mixed outcome that highlights the inherent timing volatility in semiconductor equipment sales while still pointing to steady operational execution.

Management narrowed full-year revenue guidance to a range of $875–$925 million, tightening both ends from the prior $850–$950 million outlook.

Although EPS came in below consensus expectations of $0.55, revenue exceeded analyst estimates of $252 million, reinforcing that top-line demand remains intact.

Management was clear in its messaging: the quarterly earnings variance was driven by order and delivery timing rather than any deterioration in end-market demand.

This type of lumpiness is typical for semiconductor capital equipment providers, where customer acceptance schedules can shift revenue recognition between quarters without changing the underlying growth story.

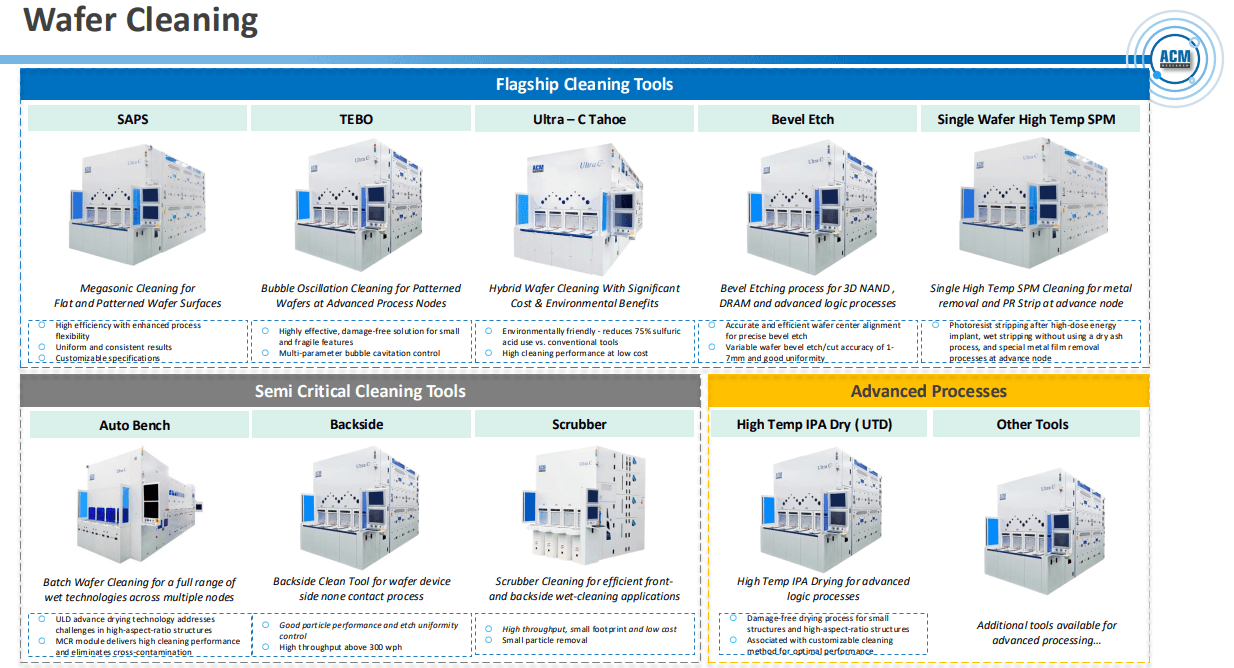

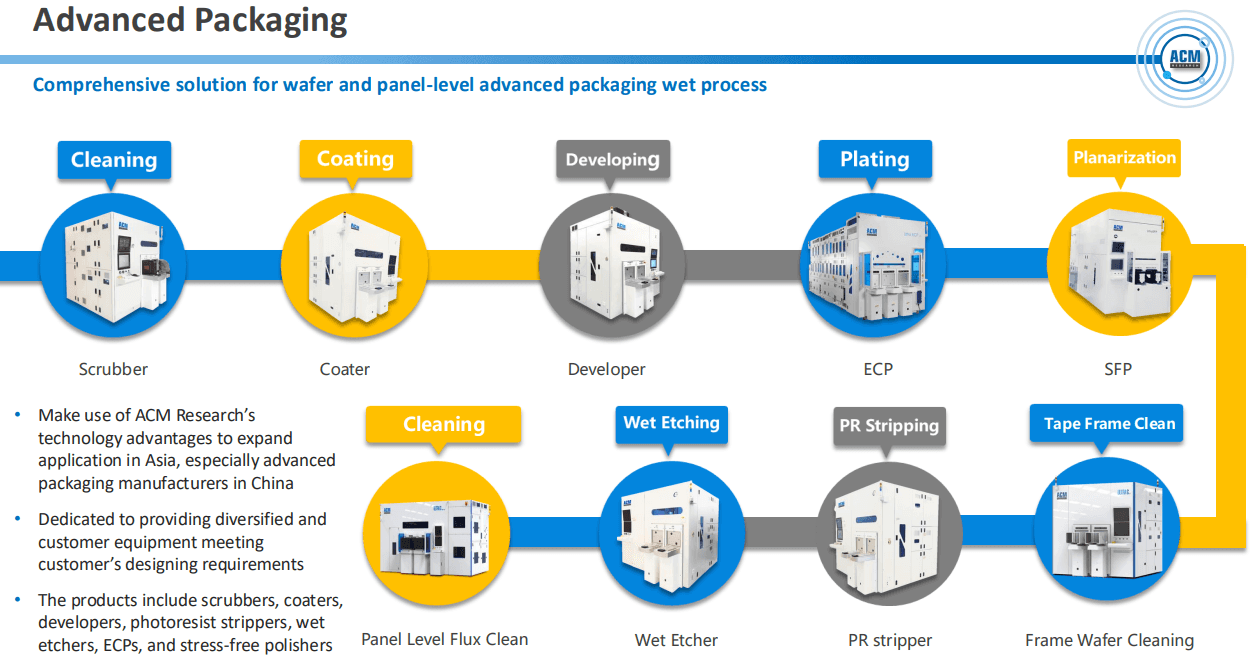

ACM Research sells semiconductor production equipment with a core focus on single-wafer wet cleaning tools that improve wafer yields during chip manufacturing.

While the company is U.S.-based, the center of gravity for its business is China, where demand dynamics are far more favorable than in most global markets today.

Its product portfolio spans several critical categories. Ultra-high critical cleaning tools are essential for advanced-node manufacturing, removing nanoscale contaminants that directly impact yields.

The company also supplies advanced packaging cleaning equipment, electrochemical polishing (ECP) systems used for metal removal and planarization, and thermal processing tools that support multiple stages of the fabrication process.

Management continues to invest aggressively in new cleaning technologies while expanding the product mix and geographic reach.

As China pushes toward semiconductor self-sufficiency, ACM Research is uniquely positioned to benefit. U.S. export controls have restricted competitors such as Lam Research and Screen Holdings from selling advanced cleaning tools into China.

Those constraints have created a vacuum that Chinese fabs must fill, and ACM has been one of the primary beneficiaries.

This is where the story becomes particularly compelling. ACM owns a majority stake in ACM Research (Shanghai), a Chinese operating entity that is not subject to the same export restrictions.

That structure allows ACM to operate as a domestic supplier within China while still being majority American-owned, effectively giving it access to both markets.

As a result, the company has captured significant market share as Chinese fabs seek reliable alternatives to restricted Western suppliers.

Globally, the wafer-fab equipment market is highly concentrated, with a small number of players dominating each step of the manufacturing process. China, however, is far more competitive, with multiple domestic players vying for share within specific niches.

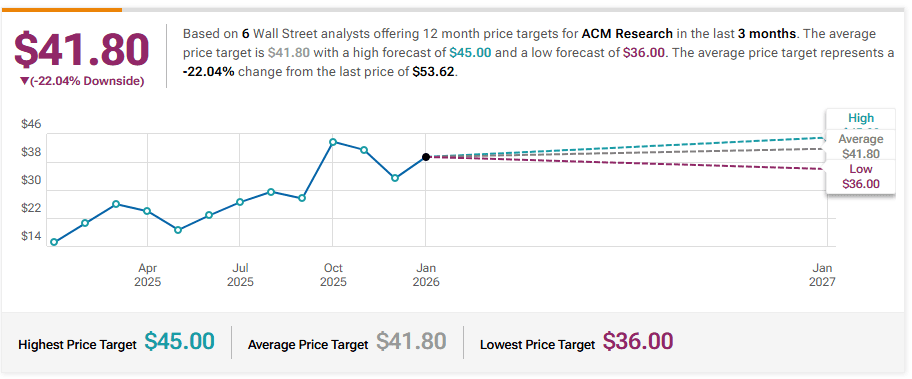

Roth Capital Maintains Buy on ACM Research, Raises Price Target to $50

JP Morgan Initiates Coverage On ACM Research with Overweight Rating, Announces Price Target of $36