ACM Research reported Q4 and full-year 2025 results, reaffirming its 2026 revenue guidance.

Management highlighted progress in new product platforms and growth in customer engagement outside mainland China.

Despite solid fundamentals, Q4 earnings missed expectations. Shares dropped 16.7%, closing at $57.04.

The selloff reflects market sensitivity to earnings misses, even when long-term guidance remains intact.

While the earnings miss wasn’t fundamentally alarming, the sharp decline raises caution for short-term traders. ACMR’s expansion outside China and new product initiatives remain key drivers for 2026 growth.

ACM Research, Inc. (ACMR) has surged 57.3% since our entry, and while that’s already a strong move, the stock still shows meaningful upside.

The core of the thesis lies in its ownership of 74.6% of ACM Shanghai (STAR Market: 688082), valued at roughly $14.65 billion, while the U.S.-listed parent trades at only $3.3 billion.

This creates a clear “China discount,” where investors are effectively buying the Shanghai business at a bargain while getting the U.S. parent, its cash, and intellectual property essentially for free.

ACM Shanghai trades like a high-growth Chinese tech company with P/E multiples in the 40–50x range, and at times over the past year, the market value of ACMR’s stake in Shanghai exceeded the entire market cap of the U.S. parent.

Even after a 170% rally over the last year, this valuation disconnect remains significant, making ACMR a compelling opportunity relative to its China-listed subsidiary.

The stock recently accelerated above $70 before pulling back, highlighting expected volatility, especially if the broader AI trade cools.

The updated price objective is $84, with a stretch scenario of $134; however, the market’s limited awareness of ACMR compared with names like NVIDIA or AMD makes the higher scenario less immediate.

The approaching semiconductor capex cycle provides a potential catalyst to further unlock this value.

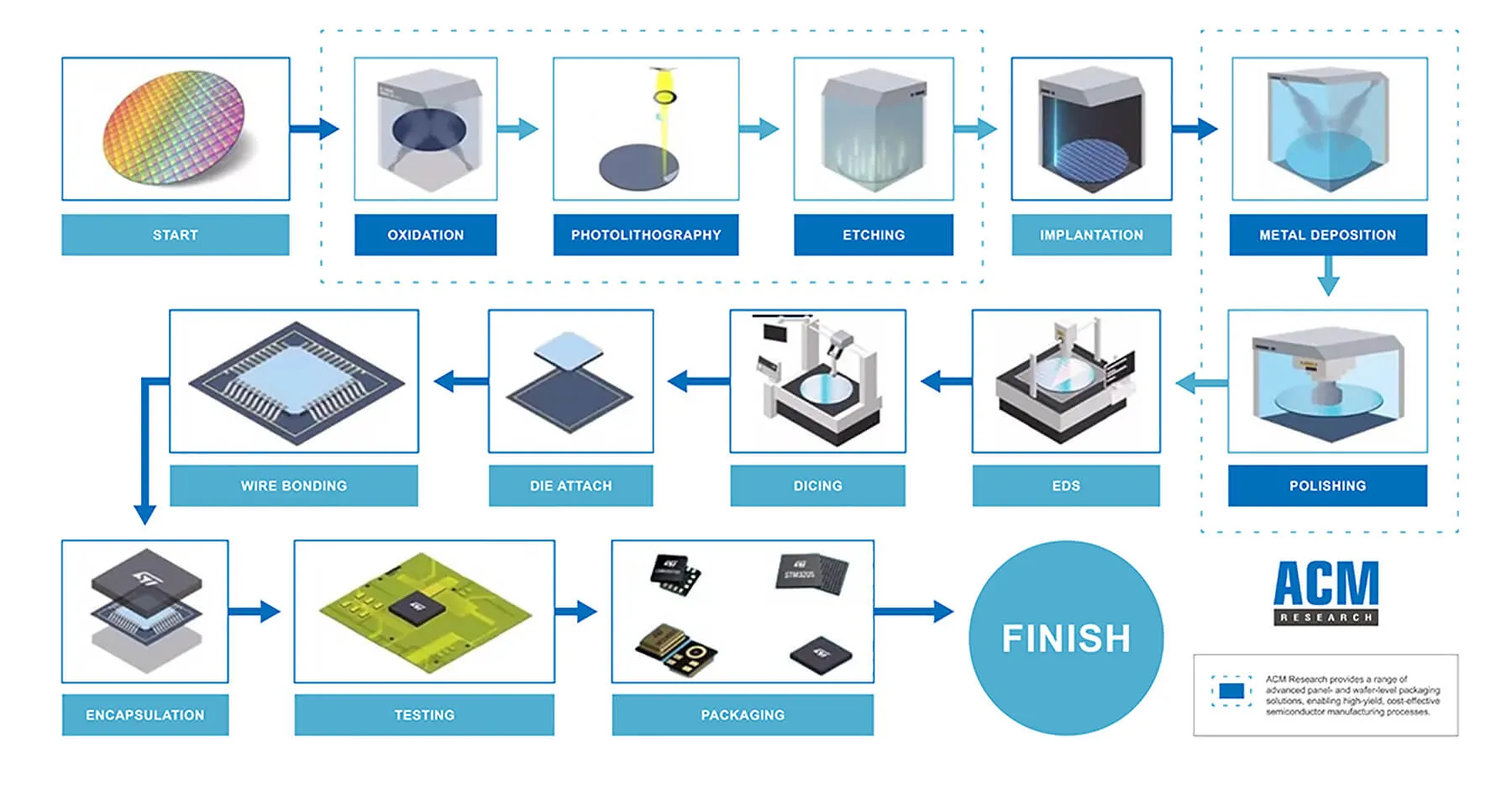

So what exactly does ACM Research (ACMR) do? At first glance, it might sound mundane they build the machines that clean semiconductor chips. But in the microscopic world of semiconductors, “cleaning” is far from boring.

A wafer with even the tiniest particle of contamination can be worth millions or nothing at all. ACMR specializes in single-wafer wet cleaning equipment, and as chips get smaller and AI processors more complex, cleaning becomes exponentially more challenging and critical for yield.

Founded in 2003, ACM Research designs, develops, and markets wet processing equipment that addresses contamination-control requirements for logic, memory, and advanced packaging applications.

Its modular platform tools can be configured for a range of spin, scrub, and batch cleaning processes, making them highly adaptable for semiconductor fabs.

The company’s product portfolio includes single-wafer spin cleaning systems with high-purity megasonic capabilities, dynamic chemical scrubbing modules for post-CMP residue removal, and batch-process equipment for highthroughput production.

At the heart of ACMR’s technology are two proprietary innovations: SAPS (Space Alternated Phase Shift) and TEBO (Timely Energized Bubble Oscillation).

SAPS uses alternating-phase megasonic waves to clean wafers thoroughly without damaging the delicate circuit patterns, much like cleaning a skyscraper with a pressure washer without collapsing the building.

TEBO prevents bubbles created by these sound waves from imploding violently, which could otherwise destroy the chip.

This matters more than ever as chips evolve into 3D NAND and advanced DRAM for AI workloads. The extreme aspect ratios of these architectures make traditional cleaning methods ineffective, but ACMR’s technology succeeds.

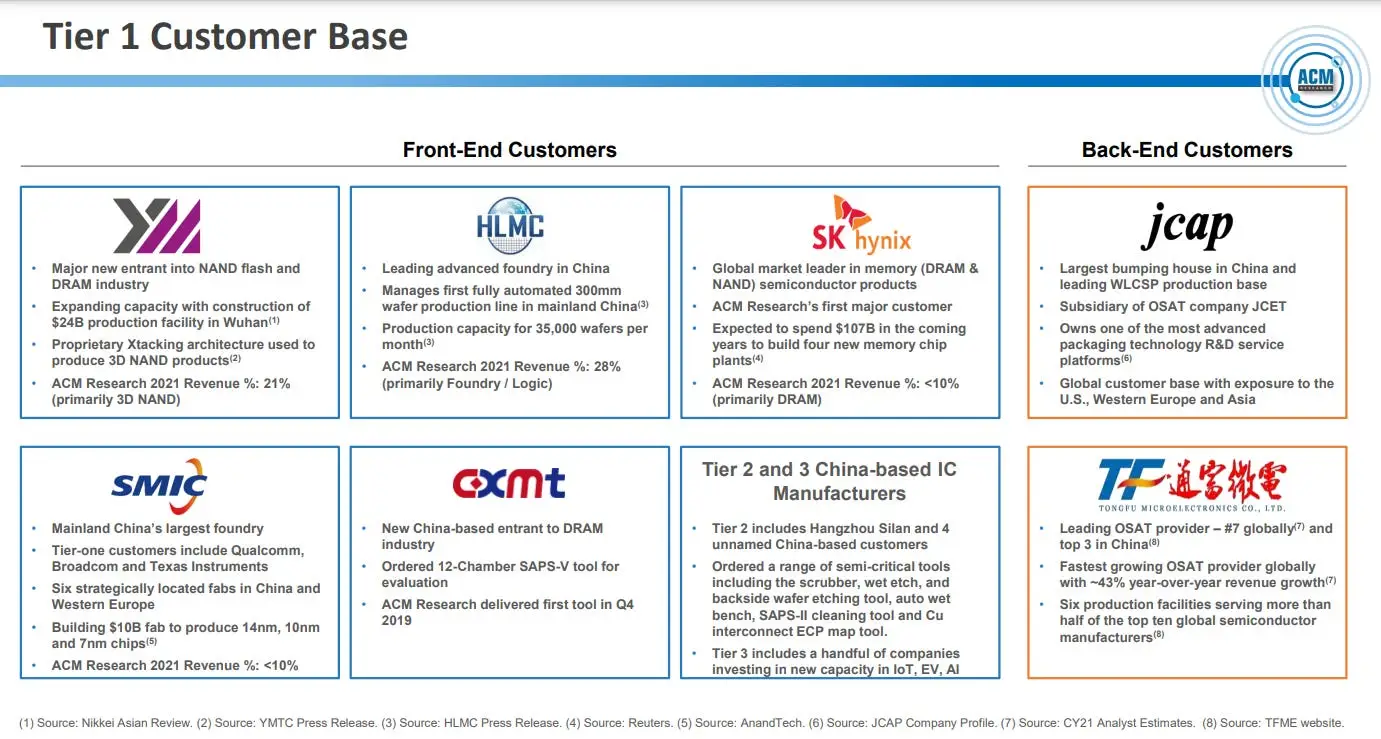

That’s why major industry players like SK Hynix and YMTC rely on ACMR for their most advanced memory production.

In short, ACMR isn’t just cleaning chips it’s enabling the next generation of AI hardware.

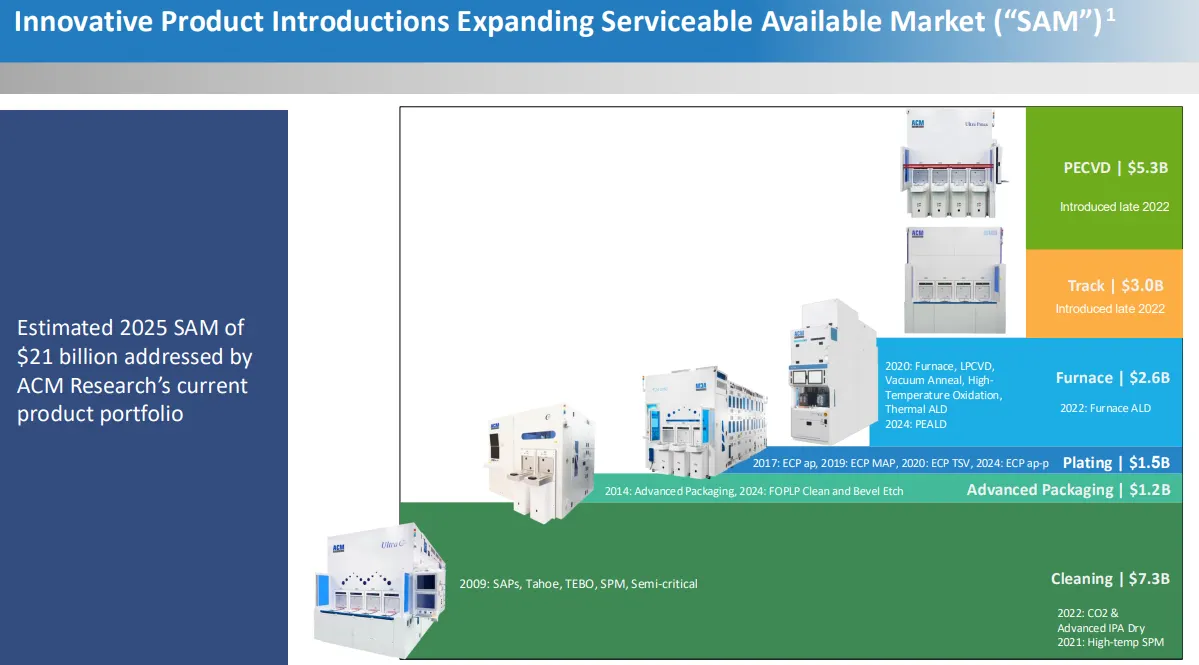

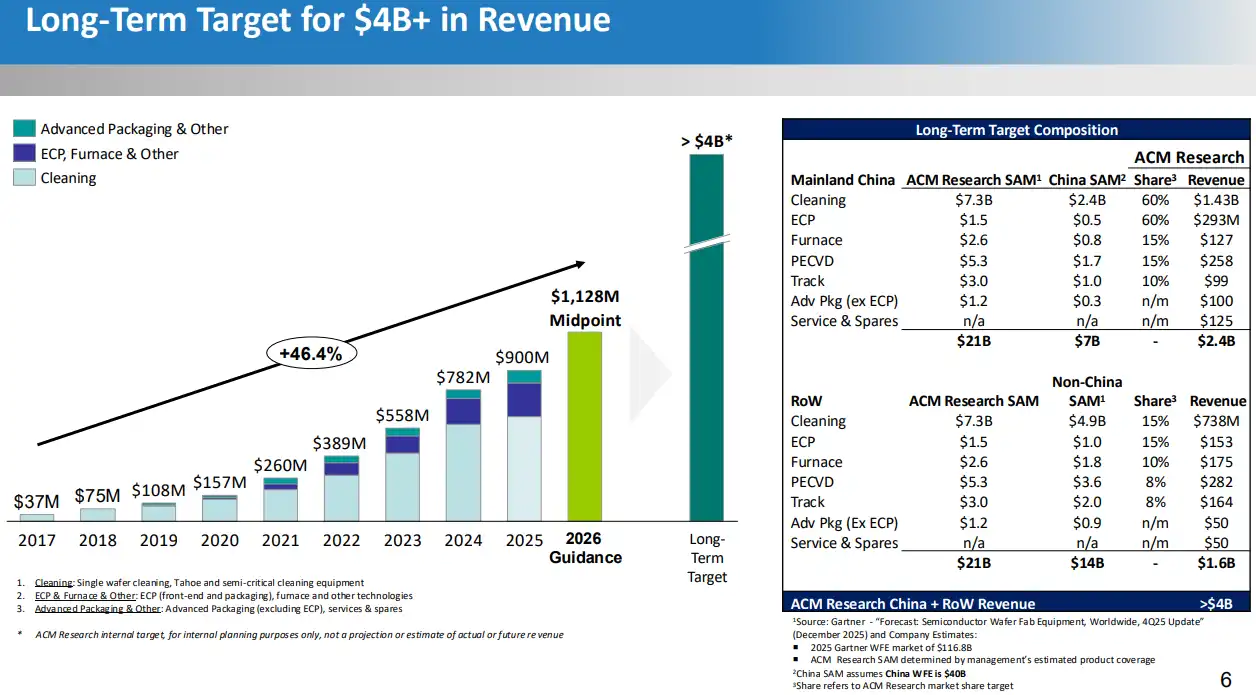

ACM Research continued to advance its product portfolio and expand its presence across the semiconductor equipment market, targeting a $21 billion serviceable available market across multiple equipment categories.

CEO Dr. David Wang highlighted that the company delivered strong execution in 2025, outperforming estimates for China’s wafer fab equipment (WFE) market.

Wang emphasized that ACM has strengthened its long-term growth foundation by advancing new products, expanding global production capacity, and enhancing funding initiatives.

The company continues to tackle increasingly complex semiconductor processes through its cleaning portfolio, high-temperature furnace platform, and horizontal panel-level plating solutions, while deepening relationships with leading global customers.

In early 2026, ACM shipped multiple cleaning tools to Singapore and secured several wafer-level and panel-level packaging tool orders from three major global customers, reinforcing its position as a critical partner for advanced semiconductor manufacturing.

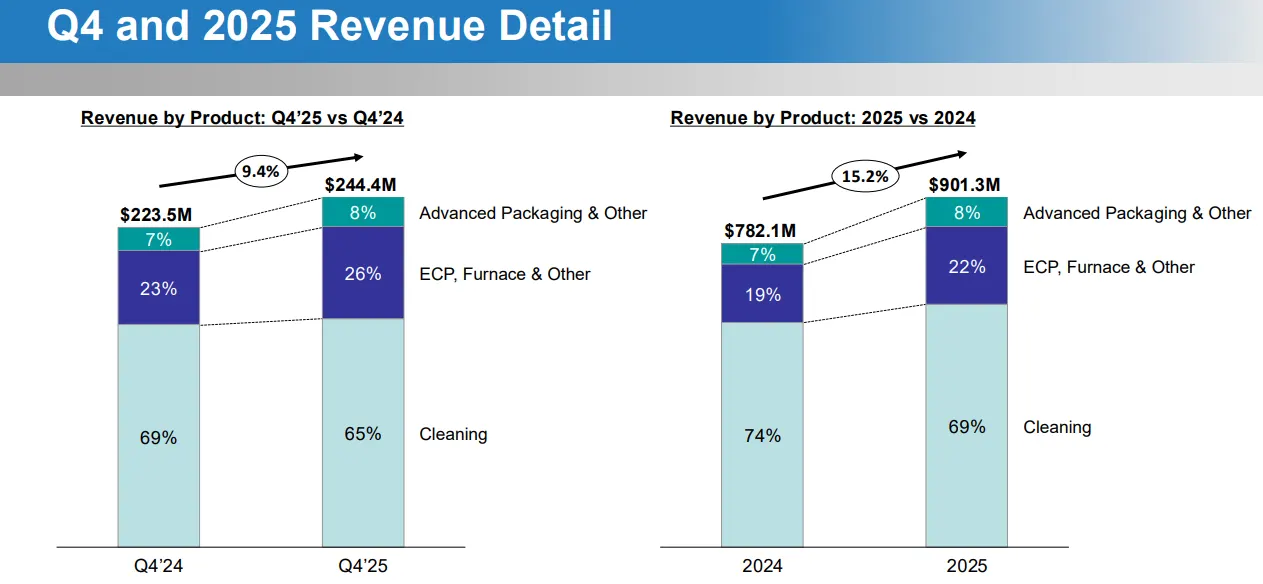

ACM Research’s fourth-quarter results highlighted a notable divergence between top-line growth and bottom-line performance.

Revenue increased 9.4% year-over-year to $244.4 million, yet shipments declined 13.5% to $228 million, suggesting that revenue timing or shifts in product mix played a role.

Despite the revenue increase, non-GAAP gross margin contracted sharply to 41.0% from 49.8% in Q4 2024, falling below the company’s target range of 42%-48%.

Non-GAAP operating income fell 44.2% year-over-year to $29.5 million, representing just 12.1% of revenue.

This compression was driven by higher costs, competitive pressures, and an evolving product mix as ACM continues expanding into new market segments.

Revenue composition shifted meaningfully during the quarter.

Cleaning equipment remained the largest contributor at 65% of Q4 revenue, down from 69% a year earlier.

Meanwhile, the ECP, Furnace & Other category grew to 26% from 23%, and Advanced Packaging & Other held steady at 8%.

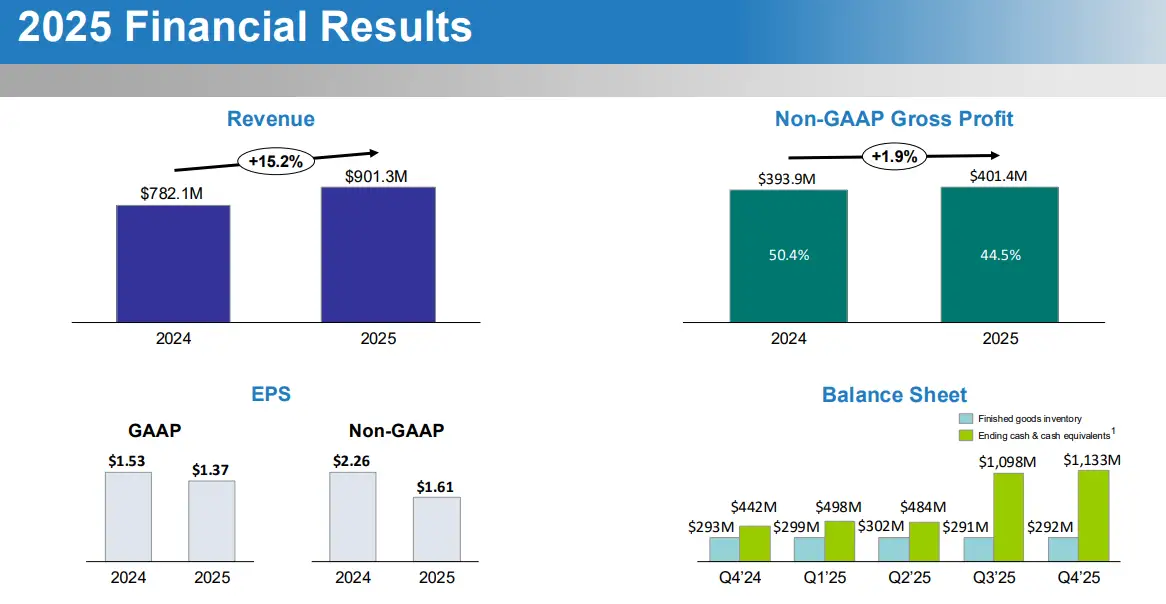

For the full year 2025, ACM Research reported revenue of $901.3 million, up 15.2% from $782.1 million in 2024. Profitability, however, deteriorated.

Non-GAAP gross margin compressed to 44.5% from 50.4%, non-GAAP operating income fell 28.7% to $143.0 million, and diluted non-GAAP EPS declined to $1.61 from $2.26 in 2024.

The results underscore the balance between strong revenue growth and margin pressures as ACM scales into new markets and invests in expanded product offerings.

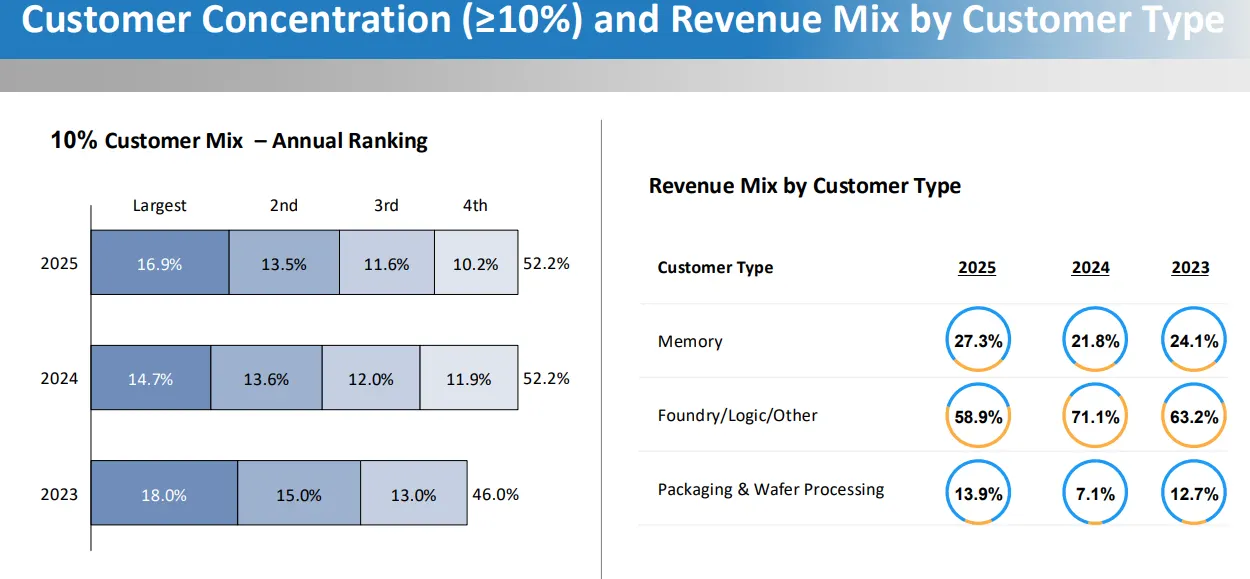

ACM Research’s customer concentration remained high in 2025, with the top four customers accounting for 52.2% of total revenue, consistent with 2024 levels.

However, the company’s revenue mix by end market is showing meaningful diversification.

The Foundry/Logic/Other segment declined to 58.9% of revenue from 71.1% the prior year, while Memory grew to 27.3% from 21.8%, and Packaging & Wafer Processing nearly doubled to 13.9% from 7.1%.

This shift reflects ACM’s strategic focus on advanced packaging and expansion into new market segments.

During its earnings call, ACMR announced several advanced packaging equipment orders from leading global semiconductor and technology customers. These include:

Multiple wafer-level advanced packaging systems for a top global OSAT customer in Singapore, with deliveries slated for Q1 2026.

A panel-level advanced packaging vacuum cleaning tool for a leading semiconductor packaging manufacturer outside mainland China, also scheduled for Q1 2026.

Additional wafer-level advanced packaging systems for a major North Americabased technology customer, with deliveries planned later in 2026.

These orders represent a significant step forward for ACM’s advanced packaging platform, reinforcing the company’s global reach and growing industry recognition.

They also highlight the strength of ACM’s differentiated technology portfolio, spanning both wafer-level and panel-level applications, positioning the company well for continued expansion in higher-value segments of the semiconductor market.

ACM Research is aiming for over $4 billion in long-term revenue, with roughly $2.4 billion expected from Mainland China and $1.6 billion from international markets.

These projections assume continued market share gains across ACM’s product portfolio, including a 60% share in cleaning and ECP in China and a 15% share in cleaning outside of China.

Looking ahead, the company reaffirmed its 2026 revenue guidance of $1,080 million to $1,175 million, implying 20% to 30% growth at the midpoint. Notably, ACM anticipates that shipment growth will exceed revenue growth in 2026, fueled by contributions from its new product platforms and expanding presence in advanced packaging and wafer-level processing markets.

Roth Capital Maintains Buy on ACM Research, Raises Price Target to $50

JP Morgan Initiates Coverage On ACM Research with Overweight Rating, Announces Price Target of $36

Craig-Hallum Downgrades ACM Research to Hold, Lowers Price Target to $18

Needham Downgrades ACM Research to Hold, Maintains Price Target to $25