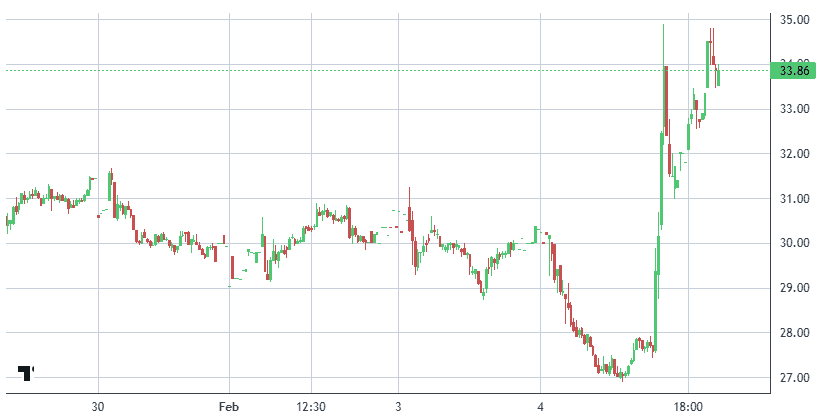

American Superconductor (AMSC) shares jumped 22.2% in after-hours trading Wednesday following a third-quarter earnings report that significantly exceeded analyst expectations.

The upside was fueled by robust revenue growth and a sizable tax benefit.

American Superconductor (AMSC) shares jumped over 22% following yesterday’s earnings report, perfectly validating our entry last week another example of why tape-watching matters.

The underlying business remains strong. Over the past five years, AMSC has delivered solid revenue growth, improving cash profitability, and expanding operating margins, signaling a more efficient and resilient model.

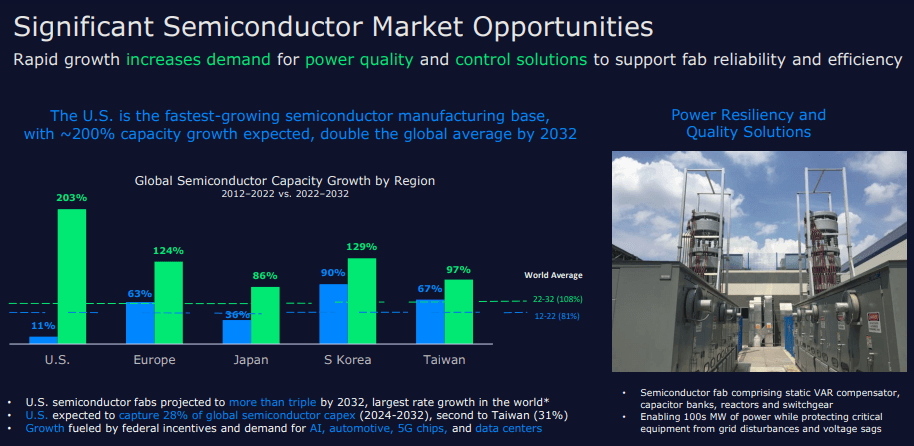

While AMSC doesn’t make semiconductors, its advanced power electronics and superconductor systems are critical for semiconductor fabs, placing it squarely within the supply-chain theme.

We traded AMSC successfully last year but exited too early, missing the subsequent 100% rally. After peaking near $70, shares have retraced to around $30, resetting expectations and creating an attractive entry point.

Why we like it:

Supply-chain exposure: Directly benefits from semiconductor capex and fab expansion.

Risk/reward: The pullback presents a compelling opportunity for investors willing to look past short-term volatility.

After strong earnings and the recent move, we’re affirming our $64 target and watching this trade closely as semiconductor demand continues to expand.

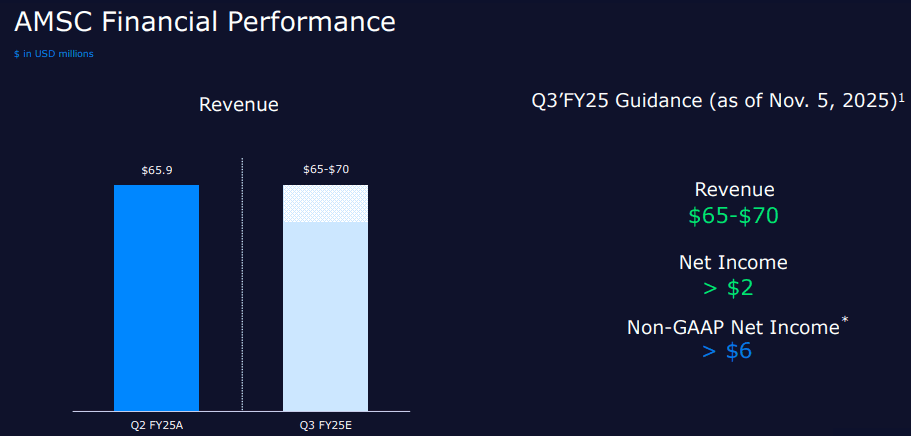

AMSC reported revenues of $74.5 million, up from $61.4 million in the same period last year, driven by organic growth and the acquisition of Comtrafo, which contributed partial results in December 2025.

Net income was $117.8 million, or $2.68 per share, compared to $2.5 million, or $0.07 per share, in Q3 2024, reflecting a $113.1 million discrete tax benefit from the release of a valuation allowance on a deferred tax asset.

Cash and cash equivalents totaled $147.1 million, up from $85.4 million at the end of March 2025, strengthening the balance sheet.

Looking ahead to Q4 ending March 31, 2026, AMSC expects revenues to exceed $80 million, with net income projected above $3 million, or $0.07 per share, and non-GAAP net income above $8 million, or $0.17 per share.

The company’s 12-month backlog surpasses $250 million, with bookings fueled by strong market demand. Revenue through the first nine months nearly matches total revenue for the prior fiscal year, highlighting momentum across diversified end markets, including AI and data center expansion.

With steady backlog and continued market demand, AMSC remains positioned for sustained growth, reinforcing its role as a key supply-chain play in the semiconductor ecosystem.

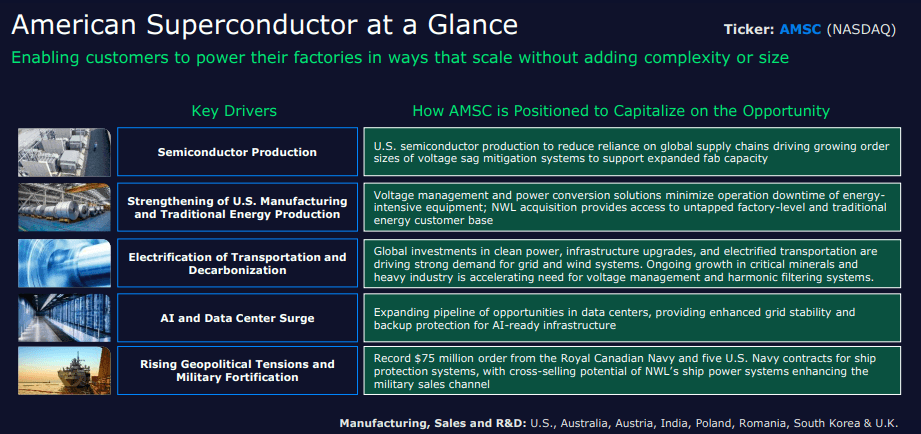

AMSC’s business sits at the intersection of power electronics, grid resiliency, and semiconductor supply-chain demand, with five key growth drivers:

Semiconductors & AI Data Centers: Reliable, stable power is critical for fabs and data centers. The AI boom and semiconductor expansion directly drive demand for AMSC’s solutions.

Renewable Energy Integration: Wind and solar growth fuels demand for AMSC’s power converters and electronic controls, helping manage intermittency and maintain grid stability.

Naval Electrification: The U.S. Navy relies on AMSC’s high-temperature superconductor (HTS) degaussing systems to reduce ship magnetic signatures and enhance operational safety.

Industrial Electrification: Traditional energy sectors and heavy industries from mining to materials processing depend on AMSC for specialized power conversion and grid interconnection.

Grid Modernization & Power Resiliency: AMSC’s Gridtec solutions support utilities in hardening infrastructure against extreme weather and scaling electricity delivery to meet rising demand.

Notable Customers: Commonwealth Edison, Huntington Ingalls Shipbuilding, U.S. Navy, Capital Power, Targa Resources, Micron Technology, SSE plc, Consolidated Power Projects, Fuji Bridex, Ergon Energy.

AMSC’s diversified customer base and exposure to critical power infrastructure position it as a strategic supply-chain partner for the semiconductor and energy industries, offering thematic upside alongside infrastructure modernization trends.

American Superconductor develops the technologies and solutions that enable smarter, cleaner energy while supporting the evolving needs of industrial infrastructure. High-efficiency, compact power delivery is particularly critical for semiconductor manufacturing, where stable, reliable electricity is essential.

Windtec Solutions: AMSC helps manufacturers deploy wind turbines efficiently, maximizing speed, effectiveness, and profitability in renewable energy projects.

Gridtec Solutions: The company provides engineering planning and grid systems designed to optimize network reliability, efficiency, and overall performance.

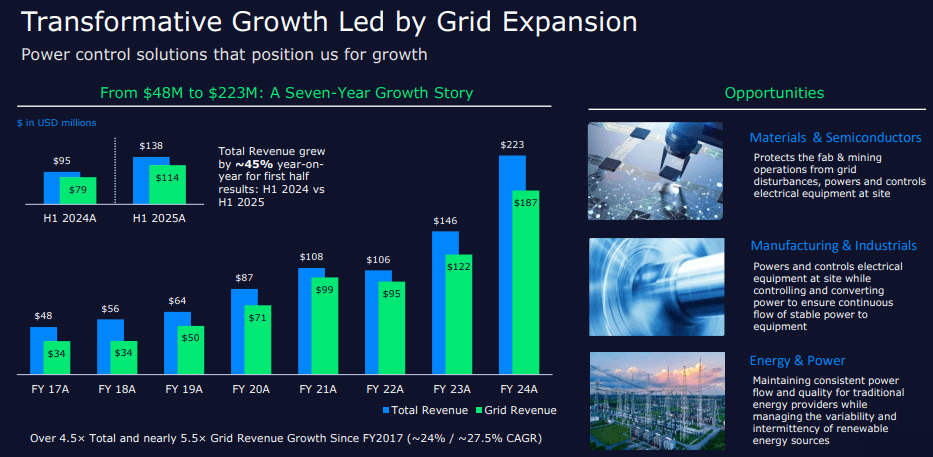

AMSC’s business is organized around two primary segments Grid and Wind with the Grid segment generating the majority of revenue, reflecting strong demand for reliable, high-quality power solutions across industrial and critical infrastructure applications.

Positioning: By combining renewable energy, grid modernization, and industrial electrification, AMSC continues to deliver strategic supply-chain exposure to semiconductor fabs and other high-growth end markets.

Semiconductor manufacturing has become a key growth driver for AMSC, now contributing roughly 25% of total revenue.

The company’s solutions ensure ultra-clean, stable electrical power, protecting sensitive fabrication equipment from costly voltage fluctuations.

Key Semiconductor-Specific Drivers:

Voltage Sag Mitigation: PQ-IVR and D-VAR systems detect and correct power disturbances in milliseconds, preventing downtime and equipment damage.

Reshoring & Fab Expansion: U.S.-based semiconductor production is surging, driving new orders for substation-level power conditioning.

AI & Data Center Growth: Increased chip production for AI infrastructure has made AMSC’s semiconductor-related segment one of its strongest performers.

Higher Project Content: As fabs grow more complex, the size and value of AMSC’s typical orders continue to rise.

AMSC sits squarely in the semiconductor supply chain, providing critical power infrastructure that scales with the industry’s expansion.

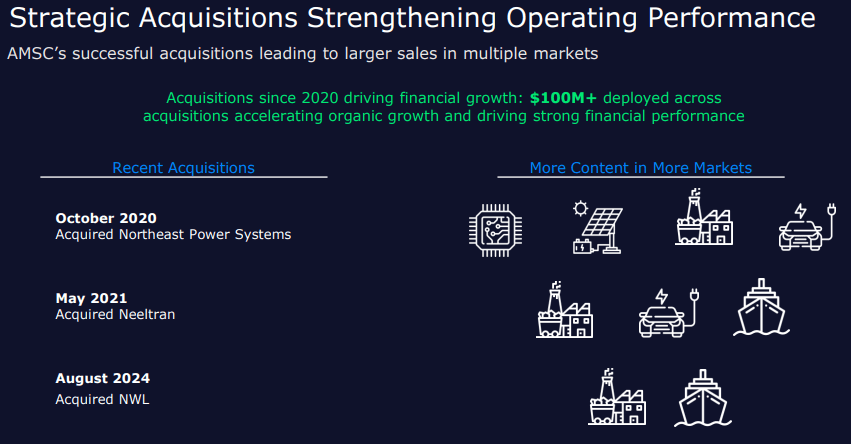

While AMSC hasn’t pursued large-scale M&A aggressively, it has made targeted acquisitions and partnerships to expand its capabilities in grid stabilization and wind energy, often collaborating with utilities and turbine manufacturers.

Key Moves:

Neeltran, Inc. (May 2021, $16.4M): Expanded industrial power offerings.

NWL, Inc. (Aug 2024): Strengthened military and industrial market presence.

NEPSI (Oct 2020): Added leadership in static voltage management for grids.

Power Quality Systems, Inc.: Enhances grid reliability solutions.

Comtrafo (Dec 2025, $162M): Entry into Brazil’s $1.5B transformer market, aligning with a $20B government grid plan, expected to contribute $55M revenue in 2025.

Through these acquisitions and strategic collaborations, AMSC continues to broaden its energy footprint while reinforcing its position as a critical supplier to semiconductor fabs and the broader energy infrastructure ecosystem.

Clear Street Reiterates Buy on American Superconductor, Maintains $52 Price Target

Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Roth MKM Reiterates Buy on American Superconductor, Maintains $29 Price Target