ATS Corporation delivered a strong earnings report, highlighted by solid top-line growth and improving profitability.

The company posted revenue of $761M, representing a 16.7% year-over-year increase, alongside adjusted EPS of $0.48, underscoring continued execution across its automation platform.

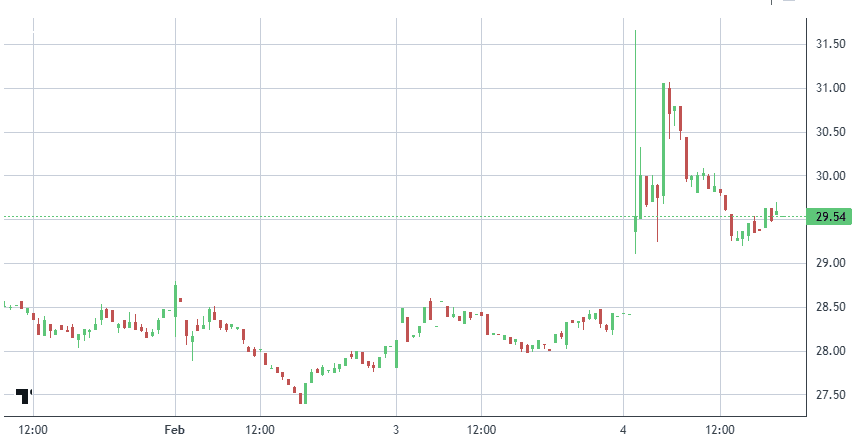

The market reacted favorably to the results.

Shares jumped 6.5% following the report, closing at $30.25, as investors responded to the combination of accelerating revenue growth and confidence in ATS’s long-term strategy.

With the stock now trading just below its 52-week high, the move signals strengthening sentiment and growing belief in ATS’s positioning within industrial automation and advanced manufacturing, particularly as demand for complex, high-value systems continues to expand.

ATS’s latest earnings call reinforced its strong positioning within industrial automation, with continued emphasis on innovation, operational efficiency, and disciplined execution. While the company finished the year slightly below expectations, our long-term bullish view remains intact.

We continue to view ATS as a strategic compounder, not a single business but a diversified automation conglomerate spanning multiple end markets.

To date, ATS has completed 23+ acquisitions, deploying roughly $1.8B to build a broad, AI-enabled automation platform.

That embedded M&A optionality remains a core part of our 2026 outlook.

Near term, we’re staying disciplined.

While we’re inclined to add early in the year, we want to see buy-side volume confirm renewed institutional participation before increasing exposure.

We also note recent leadership changes at both the CEO and CFO levels, which could support a more strategic outcome over time.

This remains a developing thesis, but it’s a signal worth monitoring.

Key Tailwinds Supporting the Thesis

• M&A valuation reset: Recent deals, including SoftBank’s acquisition of ABB’s robotics business at 2.4× sales and 17.2× EBITDA, have established a higher valuation floor for AI-driven automation assets.

• Structural demand: ATS customers have committed more than $350B toward U.S. manufacturing investments, reinforcing a multi-year automation and reshoring cycle.

Why We Stay Overweight ATS

• Direct exposure to AI-enabled industrial automation

• Multi-year demand driven by reshoring and supply-chain localization

• Potential re-rating through M&A and strategic interest in robotics

The market has yet to fully price in ATS’s positioning. The company is quietly building operational, strategic, and balance-sheet optionality that compounds over time.

As AI and robotics shift from narrative to necessity, ATS has the potential to evolve from an overlooked operator into a core holding for capital rotating into AI-linked manufacturing.

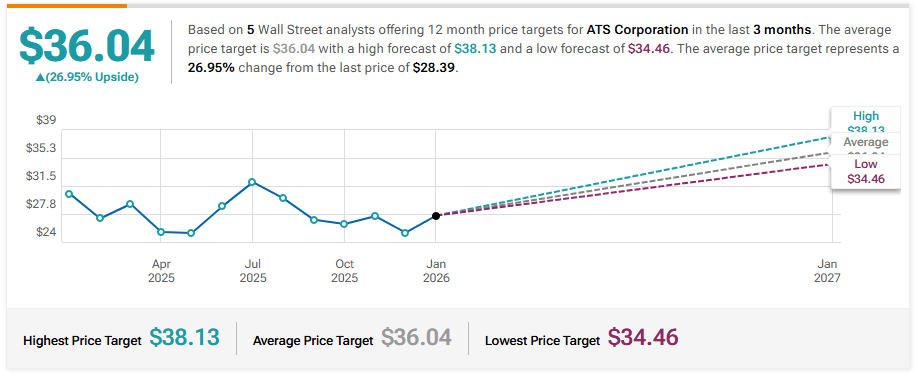

For these reasons, we’re maintaining our $48 target for 2026.

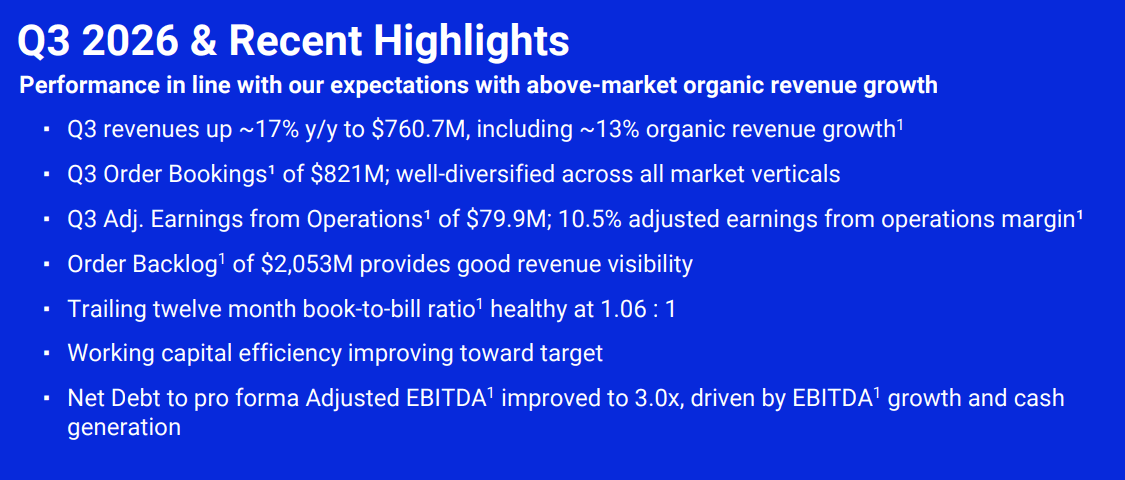

ATS delivered a strong Q3, with revenue up 16.7% year over year to $760.7 million, driven by solid organic growth and favorable FX.

Adjusted EPS came in at $0.48, while net income jumped to $30.0 million, up sharply from $6.5 million a year ago.

The market reacted favorably, with the stock rising 7.5% post-earnings.

Operationally, ATS continues to show strength.

Adjusted EBITDA rose to $105.2 million, up from $87.5 million last year, reflecting improved scale and execution.

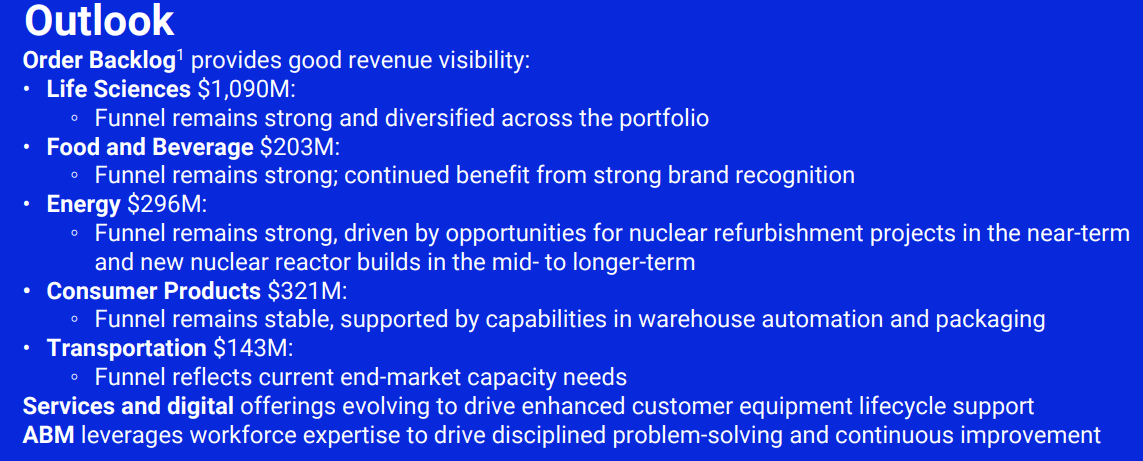

While order bookings moderated to $821 million, the company maintained a healthy order backlog of ~$2.1 billion, underscoring durable demand and solid visibility.

Year-to-Date Momentum

Through the first three quarters, ATS has generated $2.23 billion in revenue, up from $1.96 billion last year.

Net income more than doubled to $87.9 million, with adjusted EPS climbing to $1.33. Adjusted EBITDA reached $310.5 million, reinforcing the company’s ability to translate top-line growth into earnings leverage.

What Stands Out

• Consistent double-digit revenue growth

• Strong profitability expansion year over year

• $2.1B backlog supporting forward visibility

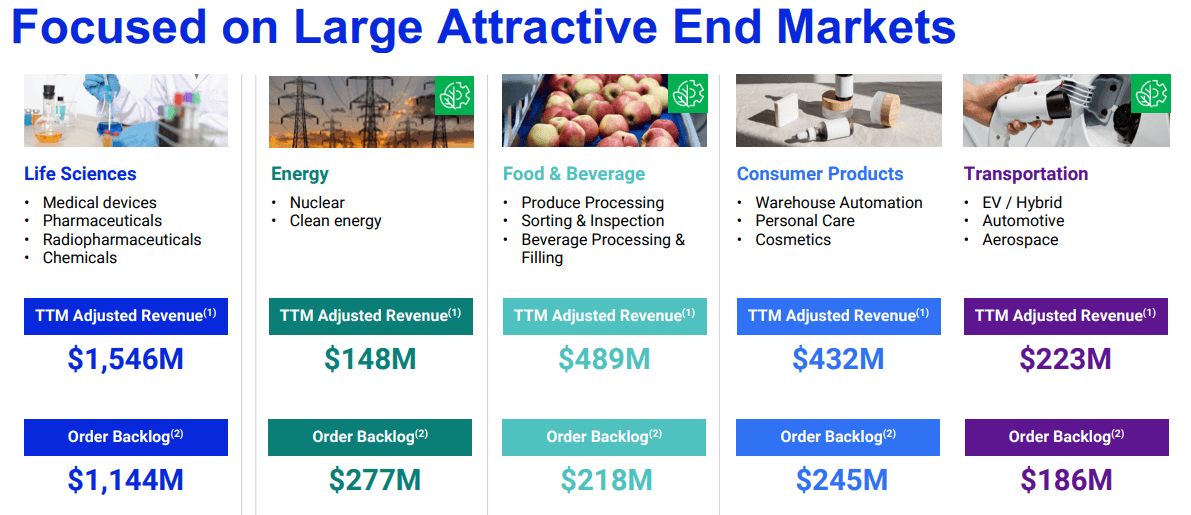

• Expanding exposure to life sciences, energy, and nuclear end markets

Despite a modest dip in gross margin, ATS’s focus on operational efficiency, automation complexity, and high-value end markets continues to strengthen its competitive position.

Overall, the quarter reinforces ATS’s role as a high-quality industrial automation compounder with multi-year growth tailwinds.

Third-quarter fiscal 2026 Order Bookings totaled $821 million, down 7.0% year over year, driven by a 10.4% decline in organic bookings, partially offset by a 3.4% benefit from foreign exchange.

The softer headline figure largely reflects timing effects rather than a deterioration in underlying demand.

Within life sciences, bookings declined versus the prior year due to tough comparisons from several large enterprise orders last year and the normal cadence of customer capital investment cycles.

Importantly, bookings this quarter remained well diversified, including radiopharmaceutical projects and medical device equipment outside of autoinjector (GLP-1) assembly.

Consumer products bookings increased sequentially, supported by timing of customer orders, including demand for warehouse packaging automation.

Food & beverage bookings declined year over year, primarily due to delayed capital spending decisions in Europe for tomato processing, though FX provided a partial offset.

Energy was a clear bright spot, with bookings rising on the back of nuclear-related programs, including reactor refurbishment and fuel fabrication.

Transportation bookings declined as expected, reflecting capacity adjustments in end markets, particularly within electric vehicles.

Looking Ahead

ATS expects Q4 revenue of $710–$750 million and continues to target high single-digit organic growth for the full year.

Strategic priorities remain focused on expanding the aftermarket mix, optimizing R&D deployment, and leveraging advanced business management tools to support long-term margin expansion.

Overall, while bookings were mixed this quarter, the composition reinforces ATS’s exposure to structurally attractive end markets and supports confidence in the company’s multi-year growth trajectory.

ATS’s business model is built around multiple high-growth end markets, helping offset weakness in slower segments like Transportation, where EV-related demand remains under pressure.

Growth momentum is increasingly driven by Life Sciences, Energy, and Food & Beverage, which now anchor the company’s long-term outlook.

Life Sciences remains a core driver, supported by a $1.2B backlog and strong organic bookings.

Demand for auto-injectors, radiopharma solutions, and wearable glucose monitors continues to accelerate, backed by demographic tailwinds and rising chronic disease prevalence.

Acquisitions such as BioDot and Heidolph have expanded ATS’s lab automation capabilities, strengthening its position within the global biopharma market.

Energy is emerging as a meaningful multi-year opportunity.

ATS’s exposure to nuclear, including reactor refurbishment and decommissioning technologies, aligns with the global push toward clean and reliable power. As small modular reactors gain traction, ATS is well positioned to participate in long-duration nuclear investment cycles.

Food & Beverage has also strengthened, with backlog up 30%, reflecting increased demand for automated and sustainable processing solutions.

The Paxium acquisition further enhances ATS’s reach across primary and secondary processing.

While Transportation remains a headwind, ATS’s diversification and disciplined M&A strategy are shifting the growth mix toward structurally attractive markets, supporting a more durable and balanced expansion path.

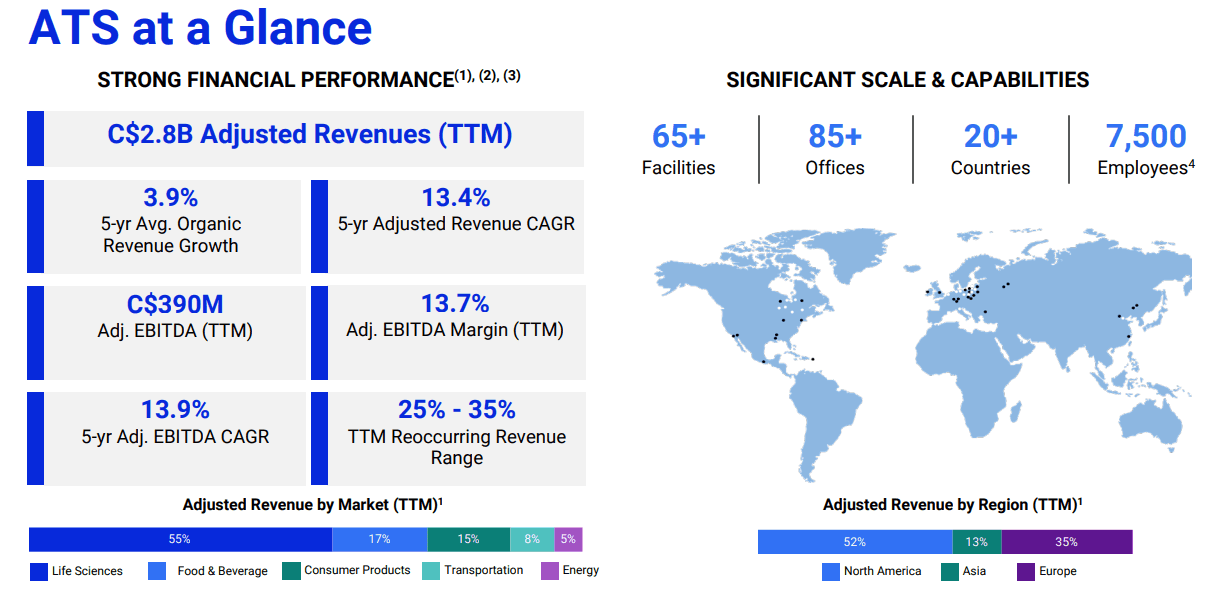

ATS is a leading systems integrator and OEM, delivering end-to-end automation solutions to some of the world’s largest enterprises.

Its capabilities span software, services, and hardware, enabling automated manufacturing across a wide range of industries, from pharmaceuticals to nuclear energy.

At the front end, ATS partners with customers on discovery and analysis, concept development, simulation, and total cost-of-ownership modeling to evaluate feasibility and ROI.

During implementation, ATS provides specialized automation equipment including proprietary OEM products alongside third-party components, supported by integration, engineering design, prototyping, and full system build-out.

Post-deployment, ATS offers ongoing lifecycle support, including training, process optimization, preventive maintenance, retrofits, retooling, and equipment relocation, creating long-term customer relationships and recurring service revenue.

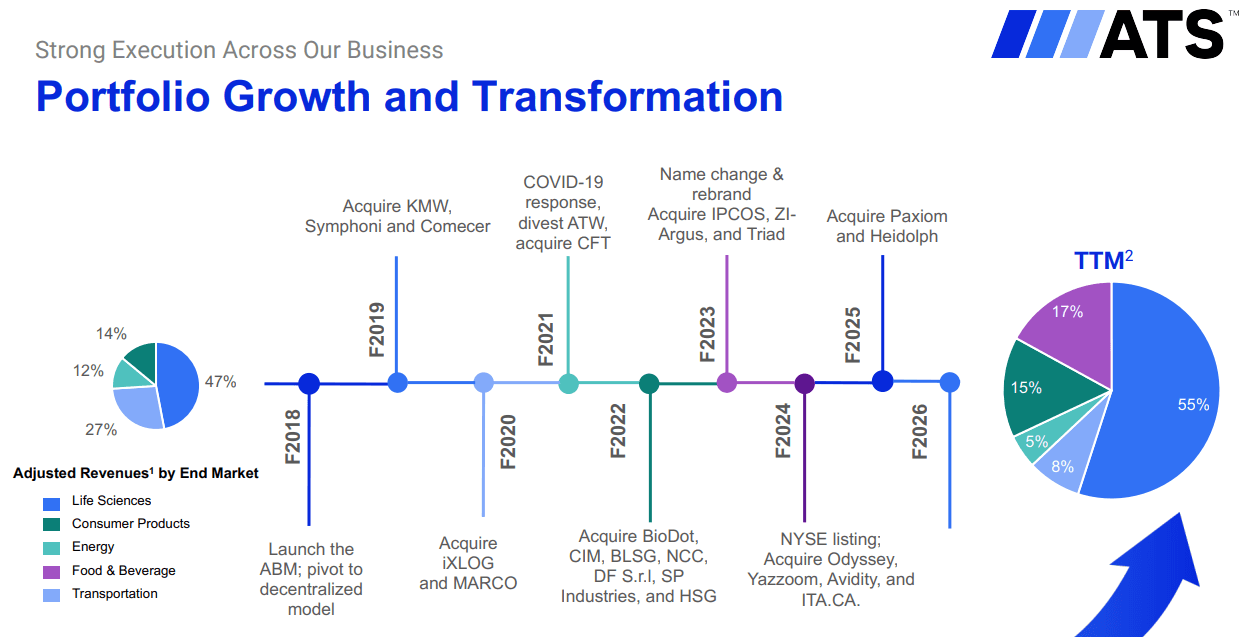

Strategically, ATS has evolved its market mix over time.

In fiscal 2009, automotive represented 32% of revenue.

That shifted meaningfully after the Sortimat acquisition in 2010, which accelerated ATS’s expansion into Life Sciences, now one of its most important growth verticals.

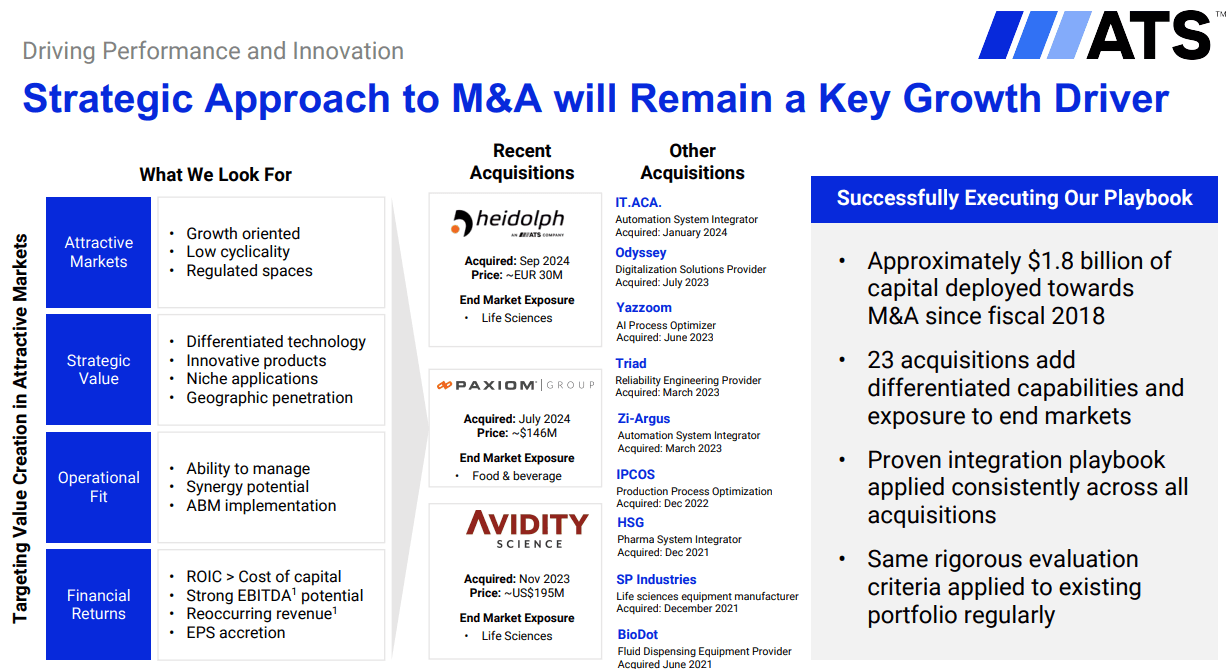

Since fiscal 2018, ATS has invested roughly $1.8 billion in M&A, completing 23 acquisitions that have expanded its capabilities and market presence.

Notable deals include:

Paxiom – May 15, 2024

Avidity Science – Sep 22, 2023 ($195M)

Yazzoom – Jul 05, 2023

Odyssey VC – Jul 01, 2023

Triad Unlimited – Apr 10, 2023

IPCOS – Nov 29, 2022

ZI-ARGUS – Oct 03, 2022

In automation, M&A is a key growth lever.

Strong customer loyalty makes it challenging for new entrants to displace incumbents, so acquisitions are an efficient way for ATS to enter new markets, gain specialized capabilities, and strengthen long-term customer relationships.

JP Morgan Maintains Neutral on ATS, Raises Price Target to $35

RBC Capital Maintains Outperform on ATS, Lowers Price Target to C$48

Goldman Sachs Maintains Sell on ATS, Lowers Price Target to $30