Shares of Chemours (CC) fell 16.8% on Friday following earnings, but the stock has since begun to rebound. Tape action shows strong volume coming in on the bounce a constructive signal after the selloff.

The company reported results and guidance that essentially met consensus expectations. After doubling since late November, the lack of an upside surprise was enough to trigger profit-taking.

While Chemours is often viewed as a low-growth cyclical chemical name, there may be more under the surface.

Its largest segment Opteon low-carbon refrigerants delivered growth last year and remains one of the company’s most promising long-term drivers.

The setup now becomes interesting: a sharp pullback after a big run, stabilization on strong volume, and exposure to a product line with structural demand tailwinds.

Chemours (CC) is currently trading at $18.27 showing a rebound post earnings, shares were down nearly 17% over the past week despite being up 44.5% year-to-date.

The recent selloff has coincided with a decline in Adjusted EBITDA.

Full-year estimates of roughly $750 million are down sharply from the $1.4 billion generated in 2021, reflecting the prolonged downturn in its two cyclical segments.

Chemours’ cyclicality is clear but so is the setup.

The stock has been on our radar since the start of the year and has quietly trended higher on steady, above average volume, suggesting accumulation rather than speculation. That relative strength persisted even while broader markets chopped.

We believe this continues to position CC well as capital rotates from crowded mega-caps into mid- and small-cap cyclicals.

The stock trades at a discount to revenue and normalized earnings potential, while still benefiting from its focused structure as a spin-out of a major conglomerate often an attractive re-rating profile.

Strategy:

With a high probability of fundamental recovery over the next three years and significant upside leverage to normalized EBITDA, CC represents a compelling opportunity for aggressive, long-term investors.

However, investors must understand the volatility inherent in its operating segments and their earnings power across cycles.

For these reasons, we are maintaining our $32 price target for the year.

Since we didn’t previously publish the full long thesis in a standalone watchlist report, we will incorporate the broader thesis framework into the detailed earnings overview below.

Chemours (CC) was formed on July 1, 2015, as a spin-off of DuPont (DD)’s more cyclical performance chemicals businesses.

Today, Chemours operates across three primary segments:

Thermal & Specialized Solutions (TSS)

Titanium Technologies (TT)

Advanced Performance Materials (APM)

In 2024, the company generated $5.8 billion in revenue and $786 million in Adjusted EBITDA. For 2025, EBITDA is tracking closer to ~$750 million, reflecting cyclical softness. The company currently carries an enterprise value of approximately $5.6 billion, positioning it at a compressed multiple relative to historical earnings power.

Separation Background:

Chemours inherited DuPont’s former Performance Chemicals segment, including:

Titanium Technologies (Ti-PureTM)

Fluoroproducts (TeflonTM, FreonTM)

Chemical Solutions

Since the spin-off, DuPont has continued reshaping its portfolio, most recently completing the separation of its electronics business into Qnity Electronics in November 2025 a name that is also on our radar.

The broader context matters: Chemours was intentionally carved out as the more cyclical, commodity-exposed piece of DuPont.

That cyclicality creates volatility but also opportunity when earnings normalize.

Chemours (CC) sits at the intersection of two powerful secular forces: the AI-driven expansion of data center infrastructure and the increasing need for advanced thermal management solutions.

As hyperscalers like Microsoft, Google, and Amazon accelerate AI buildouts, heat density inside modern data centers has become one of the industry’s most urgent engineering constraints. Chemours brings over 90 years of fluorochemical expertise to this problem positioning it as a key enabler rather than a peripheral supplier.

Why F-Gases Matter

Fluorinated gases are not commodity inputs they are high-performance thermal solutions with limited substitutes at scale.

High-density AI chips such as NVIDIA’s H100 and Blackwell GPUs generate extreme localized heat loads that traditional air cooling struggles to manage efficiently. F-gas-based liquid and immersion cooling solutions provide:

The Liquid Cooling Venture

Chemours’ dedicated Liquid Cooling Venture signals that management views this as a structural growth platform, not a niche application. By integrating early into the liquid cooling supply chain and forming industry partnerships, the company positions itself to secure multi-year supply agreements tied directly to hyperscale infrastructure expansion.

Chemours does not need to win the AI race it simply needs to cool whoever does.

AI compute growth, sovereign cloud investment, IoT expansion, and crypto infrastructure cycles are all independently driving global data center construction. As compute scales, so does thermal load. Every incremental megawatt of processing capacity requires proportional heat management.

The opportunity extends beyond data centers.

Semiconductor Supply Chain Leverage Chemours is also embedded upstream in semiconductor fabrication itself.

Advanced chip manufacturing is one of the most chemically intensive industrial processes in existence.

Chemours’ specialty fluoropolymers and electronic chemicals are used in:

Photolithography

Plasma etching

Chemical mechanical planarization

Meanwhile, government-backed expansion through the CHIPS and Science Act, alongside European and Asian subsidy programs, makes semiconductor capacity growth structural rather than purely cyclical.

The Double Leverage Thesis

In the fabrication plants that manufacture advanced chips.

In the data centers that power AI workloads.

That dual exposure combined with cyclical EBITDA compression and a discounted valuation creates a setup where structural growth and cyclical recovery can converge.

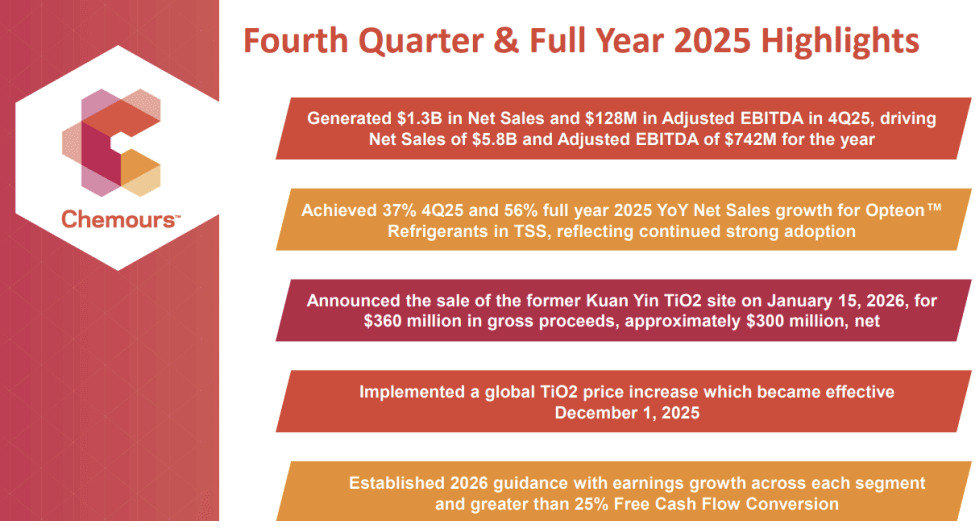

Chemours (CC) reported Q4 2025 earnings that came in below expectations.

EPS was $0.05 versus $0.07 expected, a 28% miss.

Revenue was $1.3 billion versus $1.33 billion expected, a modest top-line shortfall. Overall, it was a mixed quarter, but not one that changes the broader narrative.

The bigger issue is cash flow. Free cash flow conversion has been weak, and with leverage sitting at 4.7x at year-end 2025, the company needs to show real progress toward its 25%+ FCF conversion target in 2026 and a clear ramp beyond that.

Q4 highlights:

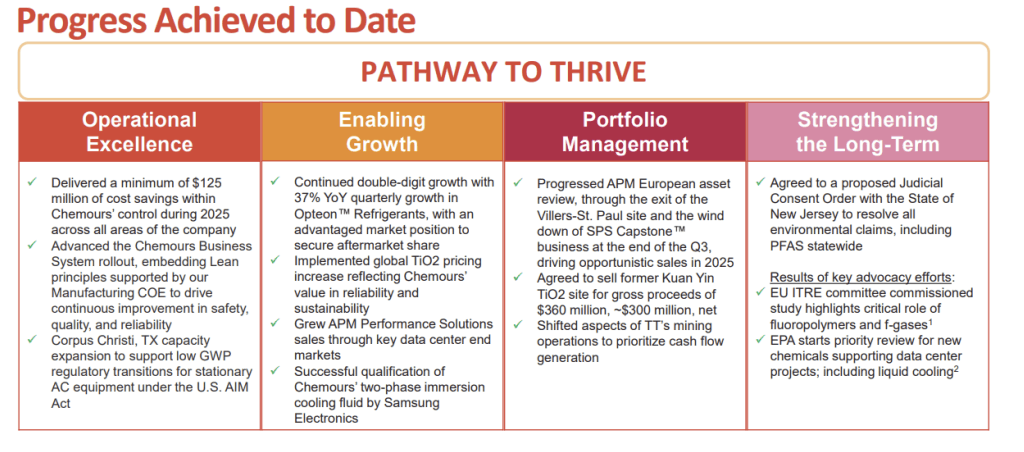

• Net sales of $1.3B, slightly down year over year, though TSS delivered record Q4 performance with 37% Opteon refrigerant growth

• Net loss of $47M vs. $11M loss last year

• Adjusted EBITDA of $128M vs. $168M last year

• Global TiO2 price increase effective December 1, 2025

• Sale of former Kuan Yin TiO2 site for ~$300M in net proceeds

Full-year 2025:

• Revenue flat at $5.8B

• Net loss of $386M vs. $69M net income last year

• Adjusted EBITDA of $742M vs. $768M prior year

Bottom line: solid pockets of strength in TSS, but leverage, weak cash conversion, and soft TiO2 demand continue to weigh on the story.

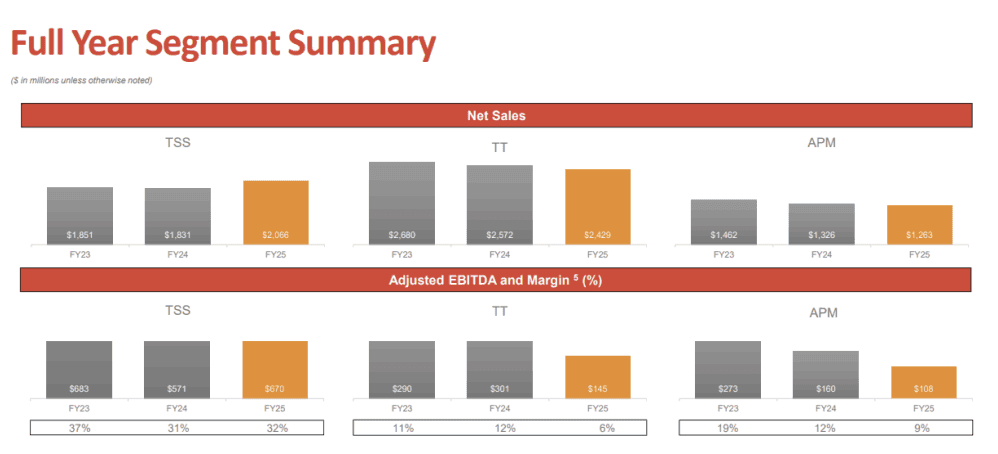

The TSS segment is currently Chemours’ profit engine, with strong margins that appear relatively insulated from cyclical swings and potentially sustainable.

Its Titanium Technologies segment houses the Ti-Pure titanium dioxide business. Titanium dioxide is a key whitening agent used in paints, coatings, plastics, and cosmetics.

Chemours is the second-largest global producer in a market dominated by four major players, but demand remains tied to broader housing and industrial cycles.

Within Advanced Performance Materials, Chemours owns a high-end fluoromaterials portfolio, including Teflon fluoropolymers and coatings, Viton fluoroelastomers, Krytox specialty lubricants, and Nafion ion-exchange membranes.

These products serve semiconductors, advanced electronics, automotive applications, and energy transition markets like hydrogen electrolysis and fuel cells.

In Q4, revenue declined 2.2%, roughly in line with expectations, while adjusted EPS fell 46% to $0.05, missing by $0.02.

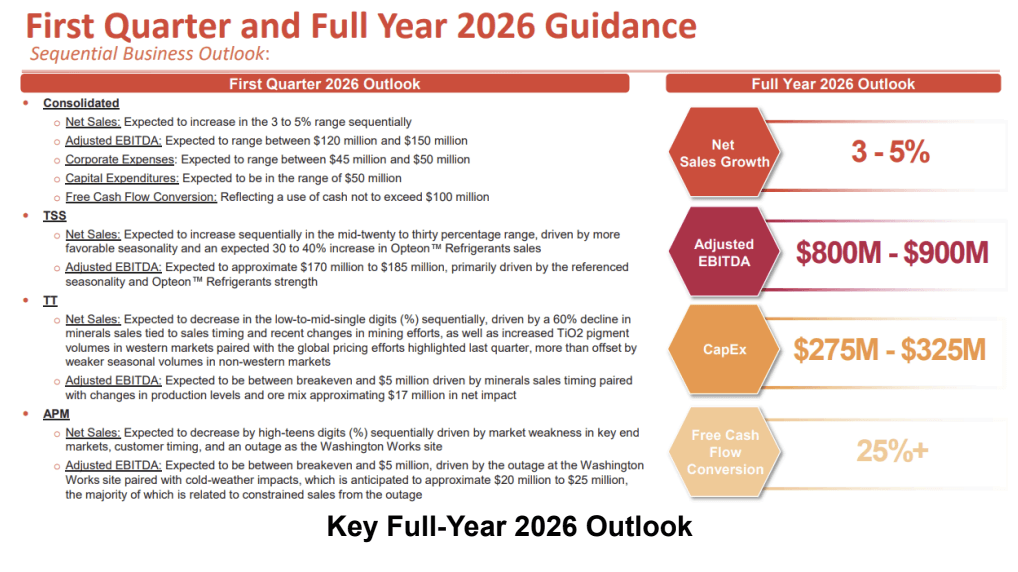

Looking ahead, management is guiding for 3% to 5% revenue growth in 2026, implying roughly $6.0 billion at the midpoint, broadly in line with consensus.

Adjusted EBITDA is projected between $800 million and $900 million, which would represent about 14–15% growth at the midpoint versus 2025’s $742 million.

It’s worth noting that 2025 EBITDA was pressured by a one-time inventory charge in Advanced Performance Materials, a segment currently facing short- term cyclical headwinds.

Key Full-Year 2026 Outlook

• Consolidated net sales growth of 3% to 5%

• Adjusted EBITDA between $800 million and $900 million

• Free cash flow conversion above 25%

A major driver behind that outlook is Opteon, Chemours’ patented low-GWP refrigerant platform within its Thermal & Specialized Solutions segment.

These next-generation refrigerants have been shipping to HVAC manufacturers for several years, and adoption is accelerating as legacy refrigerants are phased out under tightening environmental regulations over the next decade.

Last year, Opteon revenue grew 56%, helping lift the entire Thermal Solutions segment by 13% and driving an 18% increase in segment EBITDA.

Opteon now represents roughly 22% of total company sales. If cyclical businesses like titanium dioxide stabilize while Opteon continues gaining share and mix, earnings quality could improve meaningfully over time.

For value-oriented investors, the recent pullback may warrant a closer look especially if management can deliver on free cash flow improvement and deleveraging alongside Opteon’s growth trajectory.

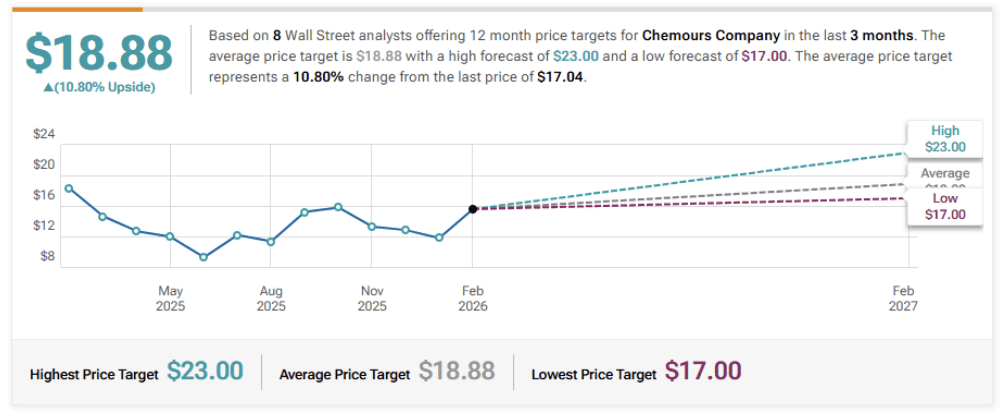

UBS Maintains Buy on Chemours, Raises Price Target to $23

BMO Capital Maintains Outperform on Chemours, Lowers Price Target to $19

JP Morgan Maintains Neutral on Chemours, Raises Price Target to $17

Morgan Stanley Maintains Equal-Weight on Chemours, Raises Price Target to $17