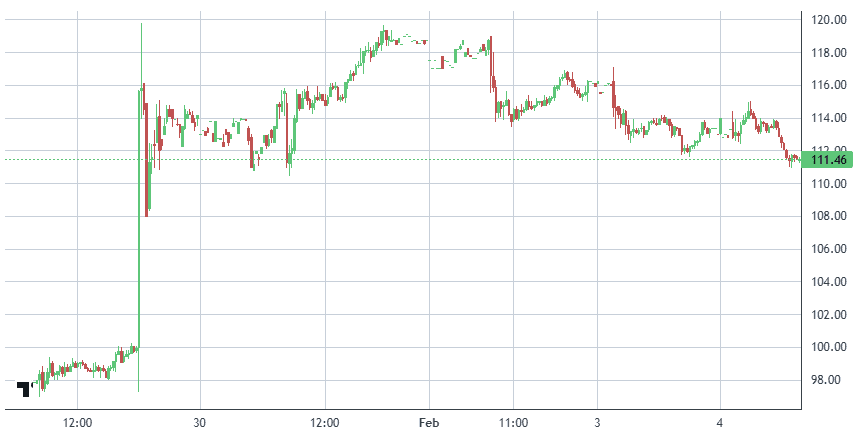

Deckers (DECK) surged 19% on Friday after decisively beating

Wall Street estimates, once again highlighting how consistently analysts have underestimated the company’s growth.

Despite four straight quarters of upside surprises, the stock still trades at a reasonable 17x earnings, which we view as attractive given the brand strength and execution.

In a challenging consumer environment, Deckers delivered Q3 revenue growth of 7.1% to $1.96B, well ahead of the $1.87B consensus.

This overview breaks down the earnings report and reiterates why we remain constructive on the long-term thesis.

We took a position in Deckers (DECK) ahead of earnings, driven by strong buy-side activity on the tape that suggested a beat was likely.

Longer term, we remain constructive.

UGG and HOKA’s brand strength, clear product differentiation, a fortress balance sheet, and a growing direct-to-consumer mix position Deckers well to navigate near-term volatility.

Valuation remains compelling.

The stock trades at roughly 17x earnings, a sharp discount to the S&P 500’s ~28x, despite Deckers’ consistent growth profile.

The setup continues to echo early Nike:

Strong execution, loyal customers, and a durable brand trading at a discount. Even after the post-earnings move, the stock is still down ~33% year-to-date.

The selloff appears driven more by macro concerns than fundamentals, including tariff exposure to China and Vietnam and broader consumer sentiment fears.

Looking ahead to fiscal 2027, Q3 results support a solid outlook with potential for accelerating growth.

The company also benefits from a $110M tariff headwind rolling off and momentum from new product launches like Quill, which should contribute into next year.

Overall, Deckers is executing well in a difficult environment while trading at a meaningful discount to the broader market.

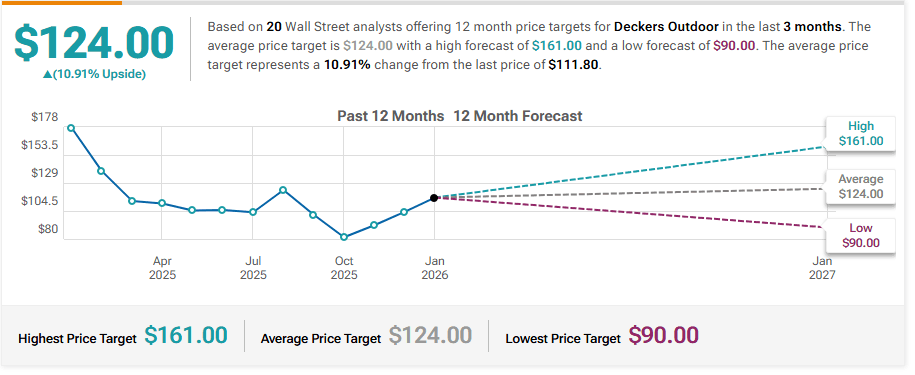

For these reasons, we are maintaining our $150 target and continuing to hold DECK as a long-term position.

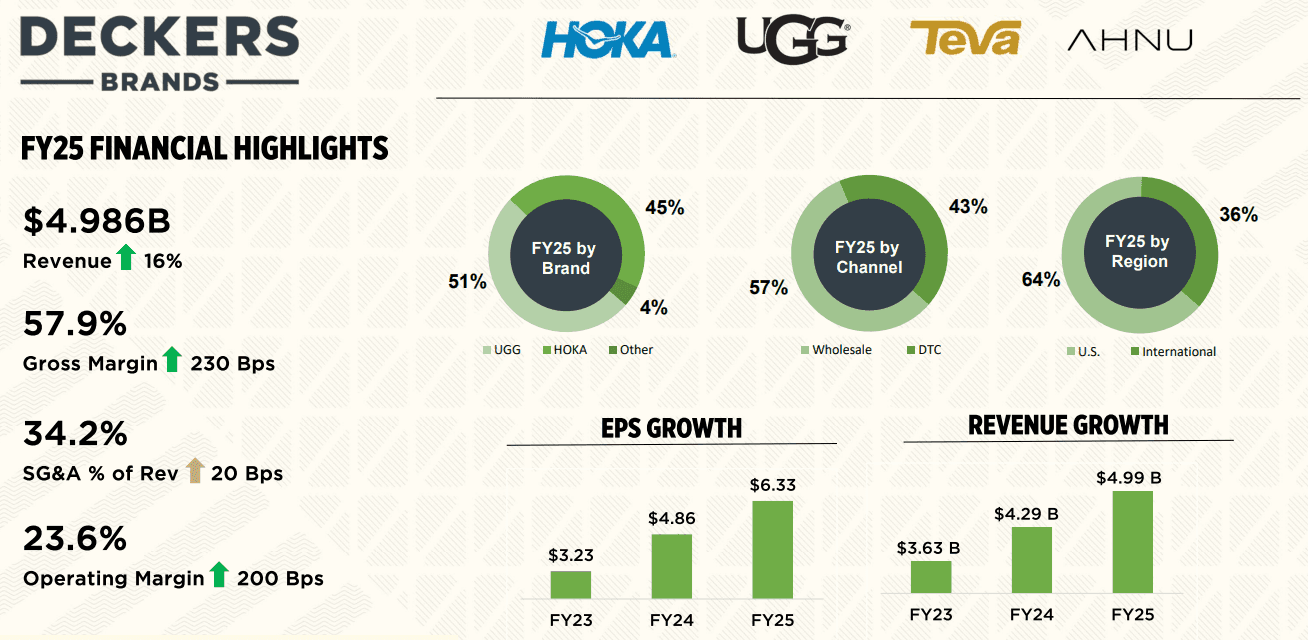

Deckers Brands delivered a strong fiscal Q3 (ended Dec. 31), with revenue up 7.1% year over year to $1.96B.

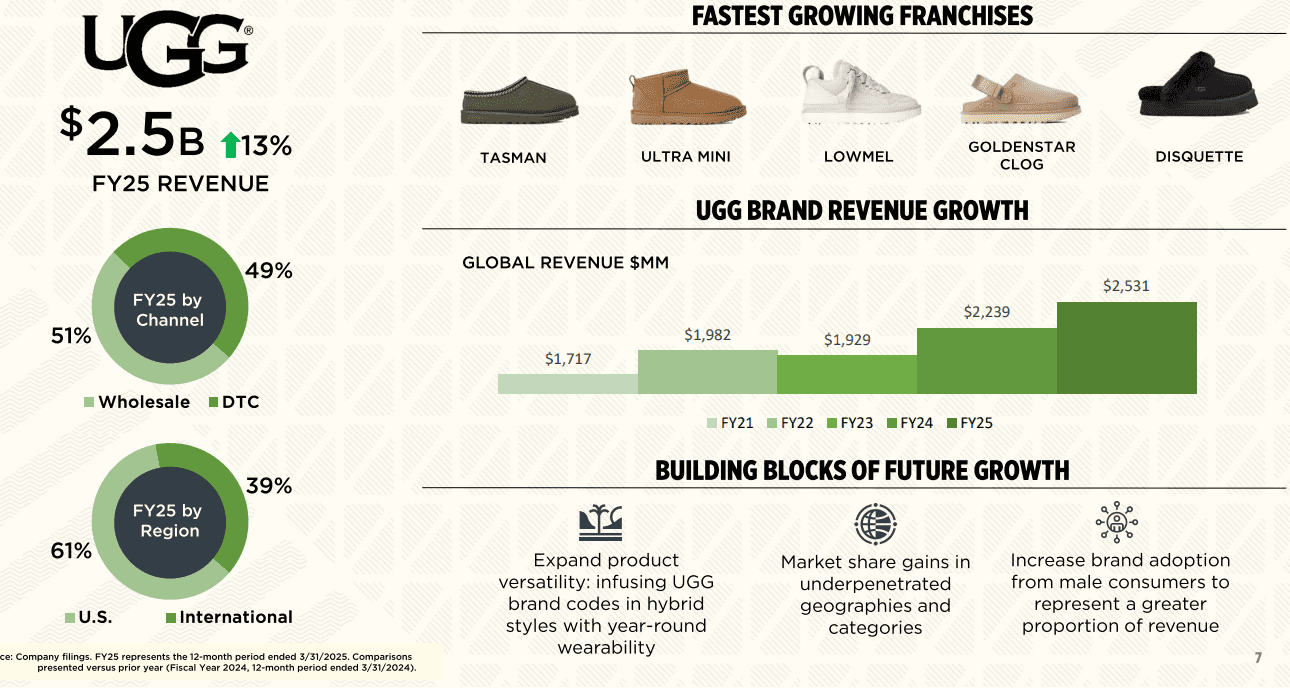

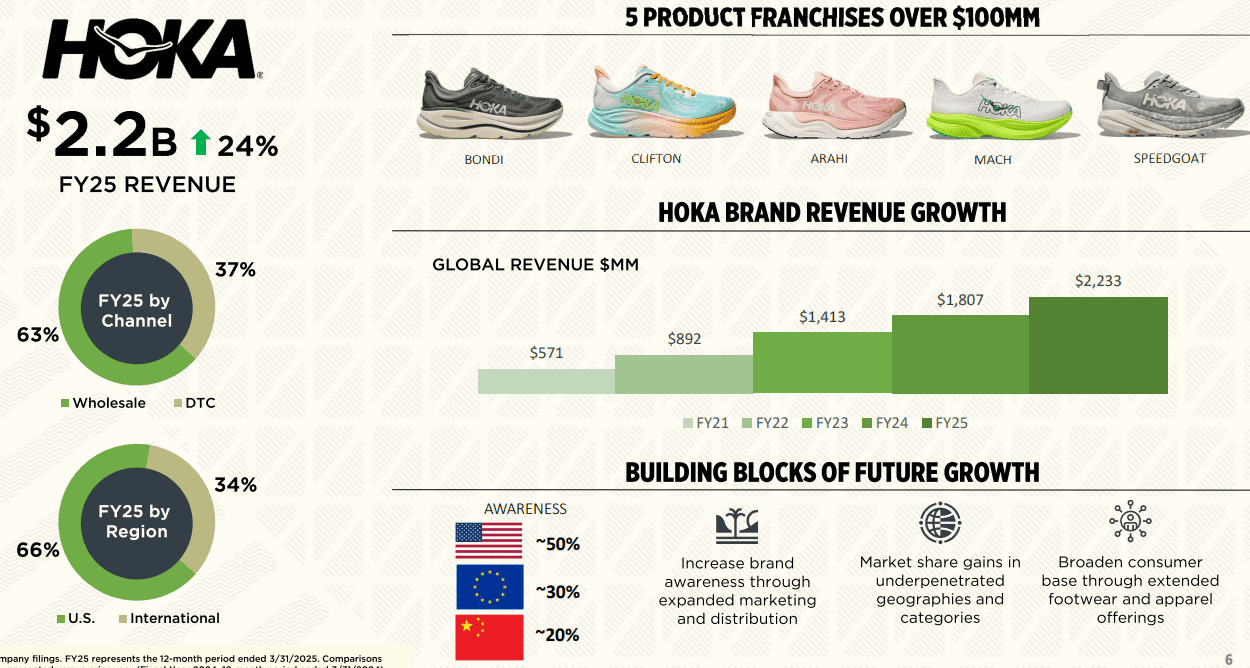

Growth was led by HOKA, with sales up 18.5% to $628.9M, while UGG grew 4.9% to $1.31B.

Wholesale revenue increased 6% to $864.6M, and direct-to-consumer sales rose 8.1% to $1.09B, signaling improving e-commerce momentum.

Regionally, domestic sales returned to growth (+2.7%), while international sales surged 15%.

Importantly, this growth did not come from heavy discounting. Both UGG and HOKA saw high levels of full-price selling, supporting strong margins.

Operating income rose 8.3% to $614.4M, with an operating margin of 31%, while EPS climbed 11% to $3.33, well ahead of expectations.

With momentum improving across previously weaker areas of the business, management raised full-year guidance.

Deckers now expects $5.4B–$5.425B in revenue and EPS of $6.80–$6.85, with HOKA growing mid-teens and UGG up mid-single digits.

Overall, balanced channel growth, stronger international demand, and successful new product launches like Quill reinforce the view that Deckers is executing well and exiting the year with accelerating fundamentals.

Deckers reported solid third-quarter fiscal 2026 results, with net sales up 7.1% year over year to $1.96B, or 6.8% on a constant-currency basis.

Growth was once again driven by its two core franchises, HOKA and UGG, which continue to do the heavy lifting across the portfolio.

By brand, HOKA sales surged 18.5% to $628.9M, reinforcing its position as the company’s primary growth engine.

UGG grew 4.9% to $1.31B, delivering steady performance in a tougher consumer backdrop.

Smaller brands declined, highlighting just how concentrated value creation is within HOKA and UGG.

Across channels, momentum remained balanced.

Wholesale revenue rose 6% to $864.6M, while direct-to-consumer sales increased 8.1% to $1.09B, with comparable DTC sales up 7.3%, signaling improving engagement and execution online.

Geographically, international markets stood out, with sales jumping 15% to $756.7M, while domestic sales returned to growth at +2.7%, an encouraging reversal from prior quarters.

Profitability remained strong despite modest margin pressure.

Gross margin came in at 59.8%, while operating income increased to $614.4M from $567.3M. Diluted EPS rose to $3.33, up from $3.00 last year.

While Deckers owns several smaller brands like Teva, this quarter reinforced the long-standing thesis: management’s early acquisition and disciplined scaling of HOKA and UGG through smart design, marketing, and distribution has created two global footwear powerhouses and driven outsized long-term shareholder returns.

Barclays Maintains Overweight on Deckers Outdoor, Raises Price Target to $143

Goldman Sachs Maintains Sell on Deckers Outdoor, Raises Price Target to $92

Piper Sandler Maintains Underweight on Deckers Outdoor, Raises Price Target to $95

Wells Fargo Maintains Equal-Weight on Deckers Outdoor, Raises Price Target to $110

Stifel Maintains Buy on Deckers Outdoor, Raises Price Target to $140

Telsey Advisory Group Maintains Market Perform on Deckers Outdoor, Raises Price Target to $120