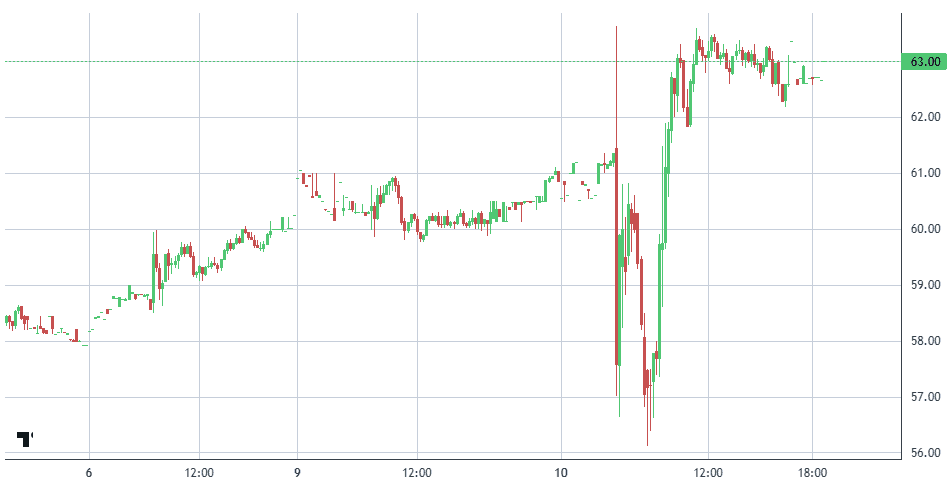

Fiserv (FISV) got off to a shaky start this morning following earnings but managed to gap higher and close the session in the green a constructive sign after last quarter’s volatility.

The payments giant is highlighting progress under its “OneFiserv” modernization strategy, following a rocky period late last year.

Q4 2025 results showed stable, broad-based activity trends, largely in line with the outlook management provided in October, with no major negative surprises.

Revenue trends reflected broader consumer behavior, including a brief slowdown in discretionary spending early in the holiday season.

Still, core business performance remained resilient as the company continues its multi-year effort to streamline platforms and integrate operations.

This quarter follows October’s earnings report, when Fiserv cut its full-year outlook and announced strategic adjustments after facing customer backlash over fees tied to its Clover point-of-sale system.

That update triggered a sharp selloff, wiping out roughly $30 billion in market cap.

One notable signal of confidence: Fiserv repurchased 3.1 million shares for $200 million during the quarter.

After the prior reset, this report feels more like stabilization than acceleration and for now, that may be enough

Fiserv (FISV) has collapsed nearly 75% from its all-time high, transforming what was once a market-favored growth compounder into what now trades more like a discounted value play.

The reset has been significant. At roughly 8–10× earnings and a free-cash-flow yield near 7%, the stock is no longer priced for perfection. It is priced for skepticism.... But at value

Fiserv is no longer a premium multiple compounder it’s a turnaround story.

The thesis now hinges on whether management can stabilize core growth, rebuild margins, and restore investor confidence after a period marked by slowing fundamentals, margin compression, and poorly timed buybacks.

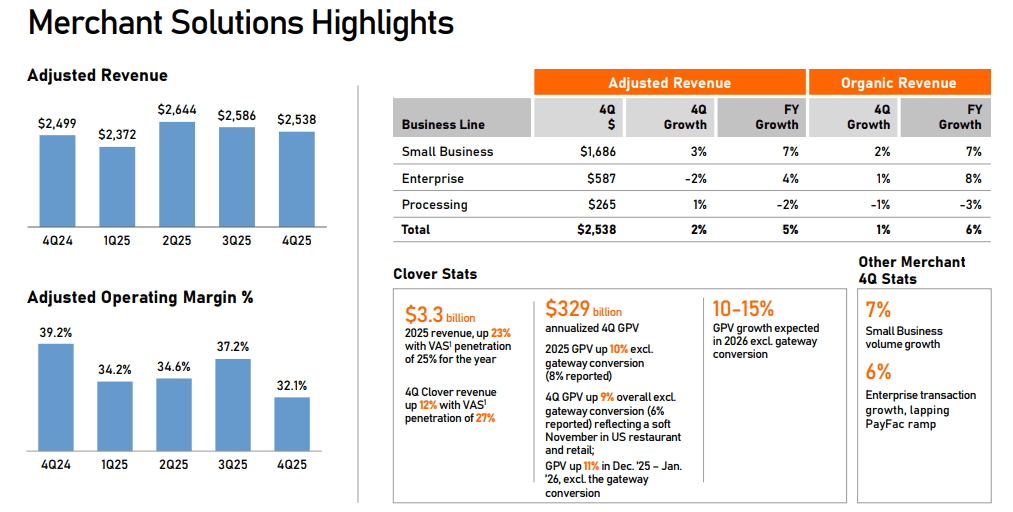

Core growth decelerated sharply as inflation-driven distortions in Argentina faded. However, Clover remains a bright spot, with Q4 revenue up 12% and Clover Capital expanding 30% in North America in 2025.

That operating leverage and embedded ecosystem value remain central to the long-term story.

Management has also pushed forward on strategic initiatives under the One Fiserv plan, emphasizing operational discipline, modernization of core banking and card platforms, and a more client-focused approach.

International expansion efforts including a strong launch in Brazil and a strategic relationship with TD in Canada suggest the company is still capable of executing.

The recent $1.5 million insider purchase adds incremental confidence, signaling internal belief in stabilization. That said, risks remain elevated, and position sizing matters in a turnaround setup.

For those reasons, we are maintaining our $120 price target for the year, recognizing that execution not narrative will determine whether this becomes a successful turnaround or a prolonged value trap.

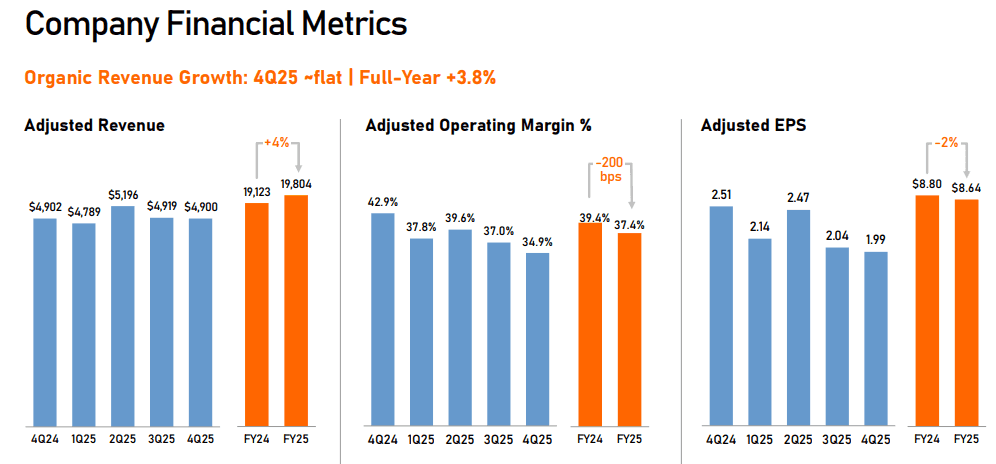

Fiserv delivered a mixed Q4 and full-year 2025 report, with revenue holding steady but earnings under pressure.

Adjusted revenue was essentially flat at $4.9 billion in Q4, and rose 4% to $19.8 billion for the full year.

On a reported basis, revenue totaled $5.28 billion for the quarter (vs. $5.25 billion a year ago) and $21.2 billion for the full year, up 3.6% year over year.

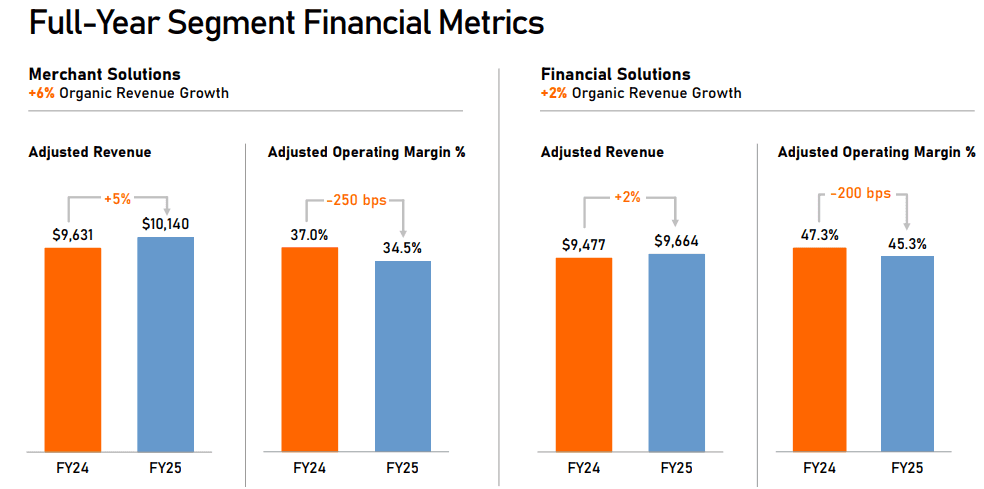

Organic revenue was flat in Q4, reflecting a 1% increase in Merchant Solutions offset by a 2% decline in Financial Solutions.

For the full year, organic growth came in at 4%, driven by 6% growth in Merchant Solutions and 2% growth in Financial Solutions.

Profitability told a softer story. Adjusted EPS declined 21% to $1.99 in Q4 and fell 2% to $8.64 for the full year, highlighting margin pressure and slower operating leverage despite stable top-line performance.

The headline takeaway: revenue stabilized, but earnings compression remains the key issue investors will be watching going forward.

Fiserv delivered a quarter defined by stability at the top line and pressure on earnings.

Adjusted revenue was flat year over year, while GAAP revenue rose 1% to $5.28 billion, reflecting modest reported growth but limited underlying acceleration.

Adjusted EPS came in at $1.99, beating the analyst consensus estimate of $1.90. However, earnings still declined 21% compared to the same quarter last year, underscoring ongoing margin compression.

Segment performance remained mixed.

Merchant Solutions grew 2%, continuing to show relative resilience, while Financial Solutions declined 2%, weighing on overall results.

On an organic basis, revenue was flat, with 1% growth in Merchant Solutions offset by a 2% decline in Financial Solutions.

The quarter suggests Fiserv is stabilizing operationally, but meaningful earnings recovery has yet to materialize.

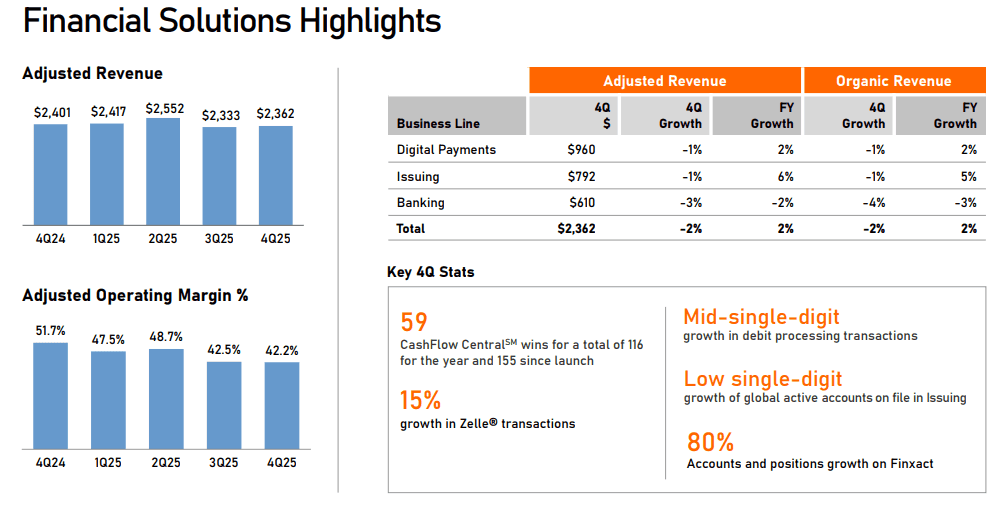

Fiserv faced continued pressure across key segments this quarter, particularly within its banking-related operations.

Banking services revenue declined 4% year over year, while Financial Solutions revenue fell 2%, reflecting slower organic growth and softer demand across parts of its core franchise.

At the same time, the company is in the midst of modernizing its banking services infrastructure an effort that requires meaningful upfront investment and is contributing to near-term margin compression.

Profitability was notably weaker. Adjusted operating margin fell 800 basis points year over year to 34.9% overall. Within segments:

Merchant Solutions margin declined 710 bps to 32.1%

Financial Solutions margin dropped 950 bps to 42.2%

The margin erosion reflects slowing growth in both Merchant and Financial Solutions, combined with increased spending on technology upgrades and strategic restructuring initiatives.

Legal overhang remains as well. At least two lawsuits have alleged that Fiserv forced merchant customers onto its Clover point-of-sale system allegations the company has denied.

Despite operating headwinds, cash generation remains solid. Fiserv produced $1.94 billion in operating cash flow and $1.56 billion in free cash flow during the quarter, providing flexibility as it works through its transition period.

The broader picture: revenue softness and margin compression are real, but the company retains strong cash flow giving it time to execute on modernization and stabilize the business.

Cantor Fitzgerald Initiates Coverage On Fiserv with Neutral Rating, Announces Price Target of $70

Tigress Financial Maintains Buy on Fiserv, Lowers Price Target to $95

Mizuho Maintains Outperform on Fiserv, Lowers Price Target to $100