Kodiak AI reported fourth-quarter and full-year 2025 results that exceeded management’s guided expectations, while reaffirming its plan to launch longhaul driverless operations by late 2026.

This marked the company’s first full quarter as a public company, with leadership highlighting continued progress in scaling customer-owned autonomous deployments, advancing safety validation, and forming partnerships aimed at reducing autonomous hardware costs all key pieces to making driverless trucking commercially viable.

Despite the operational progress, the market reaction was negative. Shares gapped down pre-market, opening at $8.24 after closing at $8.81, following the release of weaker-than-expected earnings.

This creates a bit of a disconnect: strong execution on long-term milestones, but near-term financials failing to meet expectations something we often see with early-stage autonomous and AI-driven companies still in heavy investment phases.

The key going forward will be whether Kodiak can continue to execute on deployment timelines and partnerships, while gradually improving the financial profile enough to regain investor confidence.

We exited Kodiak (KDK) last month for one primary reason: earnings risk.

In hindsight, the reaction was muted, and our caution proved somewhat overstated, which now shifts our focus toward identifying the right opportunity to re-enter the name.

From a purely fundamental standpoint, trimming ahead of earnings may have seemed overly cautious.

But this is not a purely fundamentals-driven market right now it is reactiondriven, where positioning around events often matters more than the results themselves.

The initial plan was straightforward: step aside into earnings, reassess the reaction, and look to re-enter once volatility cleared.

However, given the lack of meaningful movement in both price action and volume, we are now waiting for a clear catalyst and stronger tape confirmation before stepping back in.

That said, our broader view on the company remains unchanged. We continue to maintain a $14 price target for the year, but for now, we are taking a waitand-see approach until momentum returns.

From a valuation perspective, Kodiak still screens as one of the most undervalued names in the autonomous driving space.

For context, Waymo (Alphabet) carries an estimated valuation of roughly $45 billion, while Aurora Innovation (AUR) has averaged around $11.7 billion over the past six months.

Kodiak, in comparison, trades at a fraction of those valuations, despite already generating revenue, securing government and military contracts, and hitting key operational milestones.

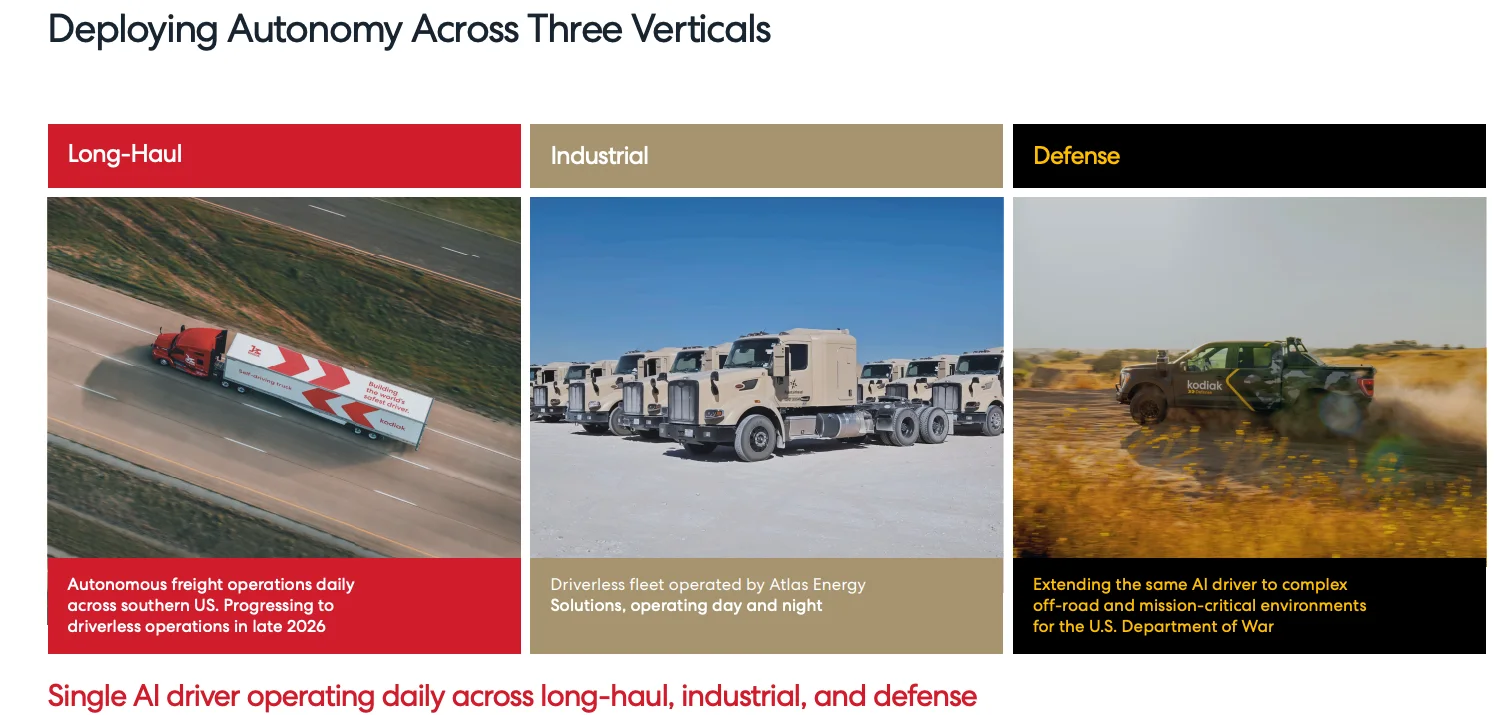

The company is now approved to operate in 24 states, with both commercial and defense partnerships in place, and plans to deploy thousands of autonomous trucks by 2027.

This is no longer a concept-stage story Kodiak is actively executing on its roadmap.

We continue to approach this trade with measured conviction, targeting a short-term swing to $14 (roughly aligned with its initial listing range) and a longer-term upside above $20 as adoption scales and institutional ownership increases

Key Operational Highlights

Fleet Expansion:

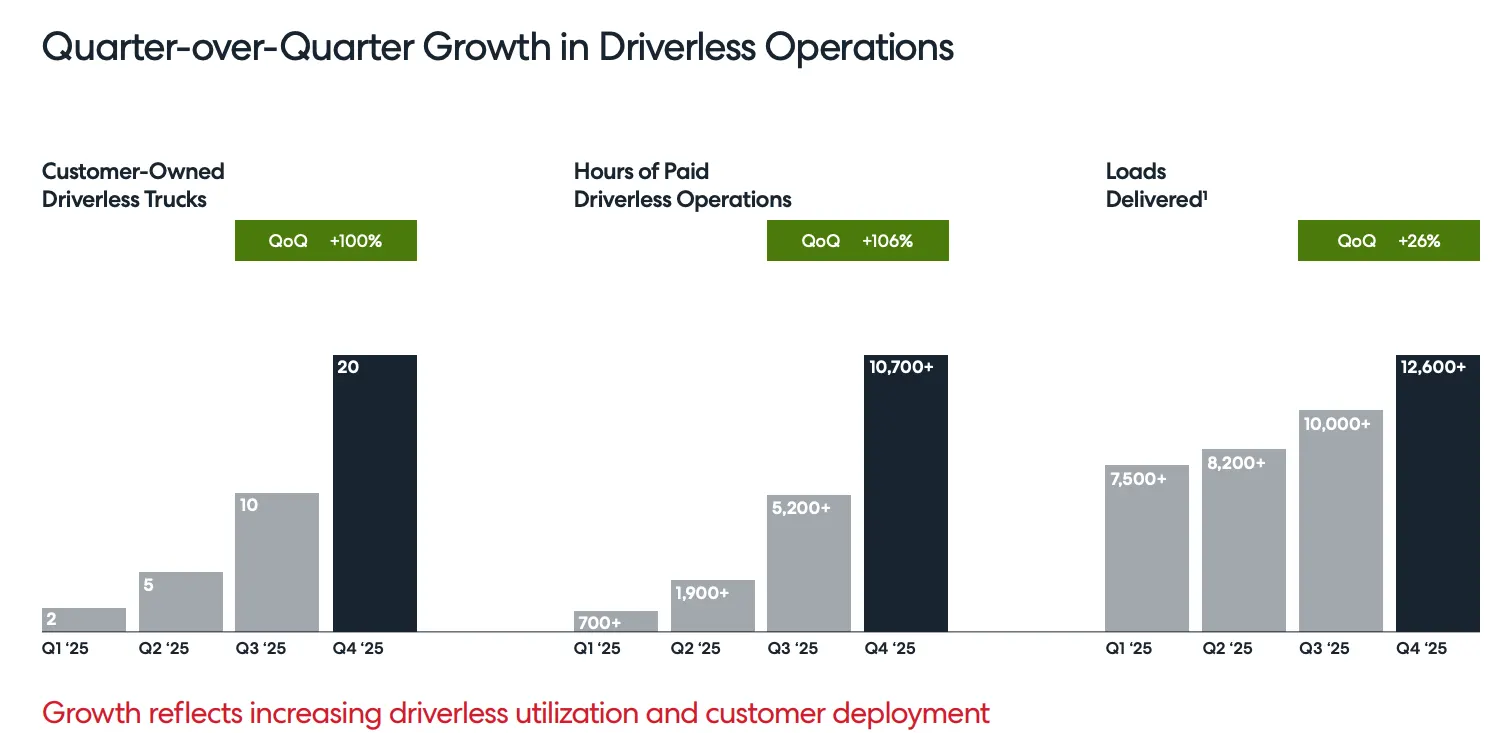

Kodiak deployed 10 additional driverless trucks to Atlas Energy Solutions, bringing the total fleet to 20 fully driverless trucks, a 100% increase from Q3.

Safety Progress:

The company continues to make meaningful strides toward regulatory and operational readiness, with its Kodiak Autonomy Readiness Measure reaching 84% as of February 2026 a key internal benchmark for launch preparedness.

Driverless Operations Growth:

Kodiak has now accumulated over 10,700 cumulative hours of paid driverless operations, representing a 106% increase quarter-over-quarter, and positioning the company as a leader in real-world autonomous trucking deployment.

Kodiak AI continues to show steady operational progress, particularly around its Atlas platform, while also delivering a lower-than-expected fourth-quarter free cash flow burn relative to prior guidance.

The company also highlighted advancements in its AI initiatives and defenserelated business, reinforcing the broader strategic positioning of Kodiak beyond just commercial trucking. However, these positives were partially offset by slightly higher projected free cash flow usage for 2026, indicating continued investment as the company scales.

One notable update is the timeline shift for driverless long-haul commercialization, which is now framed as a late-2026 milestone, rather than earlier expectations of the second half of the year. While not a major delay, it does reflect the complexity of final safety validation and deployment at scale.

Fourth Quarter and Year End Results and Business Highlights:

Kodiak AI delivered a quarter defined by continued innovation, strategic partnerships, and expanding real-world deployments, alongside steady progress on the financial front as it scales toward full commercialization.

Business & Operational Highlights

Industry-First Capability:

Kodiak introduced new functionality enabling the Kodiak Driver to haul three trailers with a single tractor, a first for the autonomous trucking industry, effectively allowing customers to triple hauling capacity.

Strategic Partnership:

The company announced a technology collaboration with Bosch to develop a next-generation autonomous platform, focused on redundant systems and automotive-grade scalability.

Defense Expansion:

Kodiak was awarded a contract with the U.S. Marine Corps to integrate its technology into the ROGUE-Fires carrier vehicle, further strengthening its position in defense applications.

Pentagon Demonstrations:

The company participated in two major defense initiatives: – The U.S. Army’s xTech Overwatch demonstration (Texas) – The Defense Innovation Unit’s Project GI (Hawaii)

Route Expansion:

Kodiak launched operations between Dallas-Fort Worth and El Paso, marking its second long-haul route beyond single hours-of-service limitations.

Enterprise Pilot Program:

A new pilot program was launched with a Fortune 500 private fleet, moving freight between Dallas and Houston, as customers begin preparing for driverless long-haul integration.

Financial Highlights

Revenue:

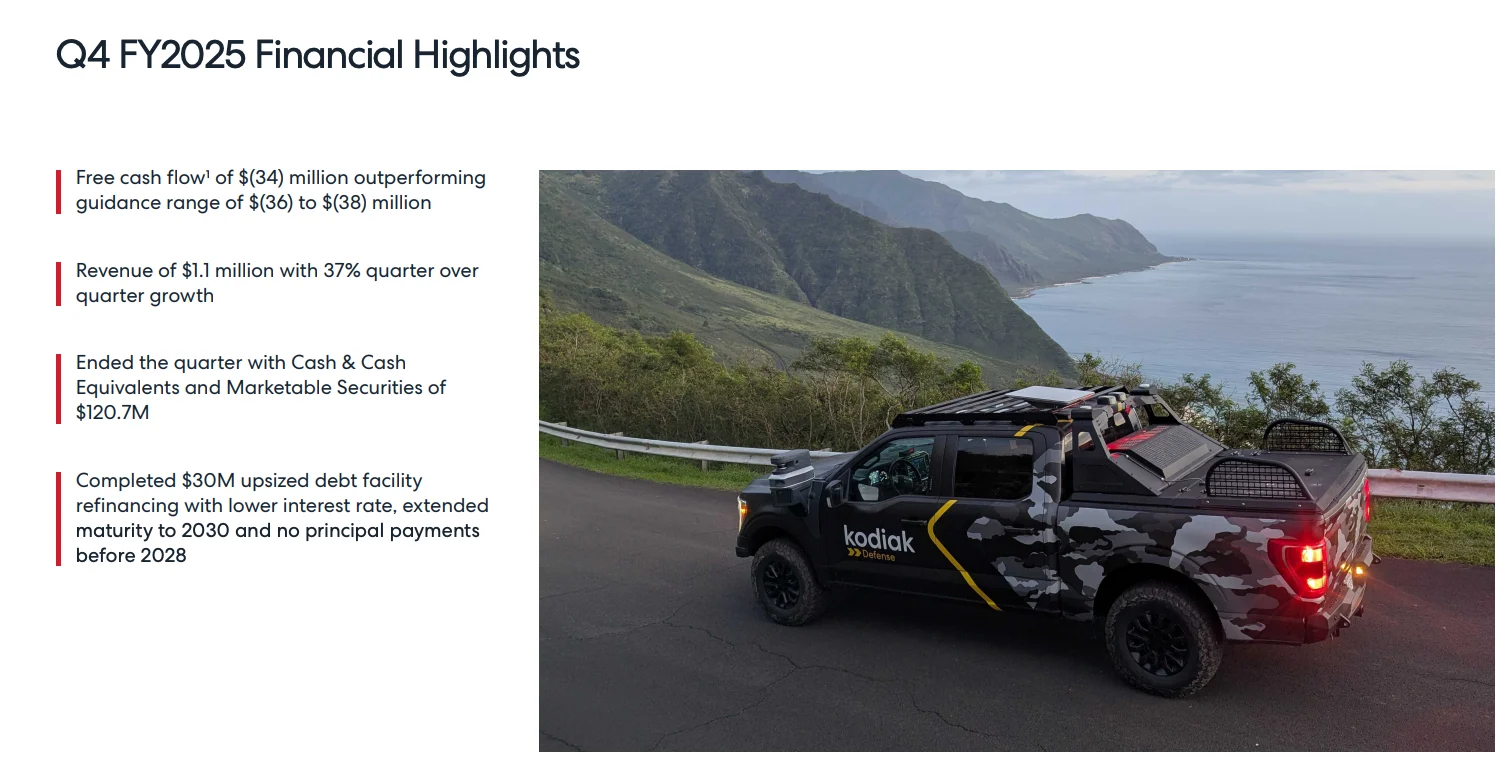

Q4 revenue came in at $1.1 million, representing 37% quarter-over-quarter growth.

Cash Flow:

– Net cash used in operating activities: $24.2 million – Free cash flow (Non-GAAP): -$34 million, outperforming guidance of -$36M to -$38M

Balance Sheet Strength:

Kodiak completed a $30 million debt refinancing, improving its capital structure through lower interest rates, extended maturity, and increased flexibility.

Liquidity:

The company ended Q4 with $120.7 million in cash, equivalents, and marketable securities, including proceeds from the refinancing.

TD Cowen Maintains Buy on Kodiak AI, Lowers Price Target to $13

Chardan Capital Maintains Buy on Kodiak AI, Maintains $22 Price Target

Cantor Fitzgerald Reaffirms Their Buy Rating on Kodiak AI