This is a list of stocks that members asked us to do extra research on none of these are alerts/buy/sell recommendations.

Company: Qualys, Inc.

Quote: $QLYS

BT: $120- $130

ST: $150 without M&A, $200 With M&A

Qualys to Report Third Quarter 2025 Financial Results on November 4, 2025

Sharks Opinion:

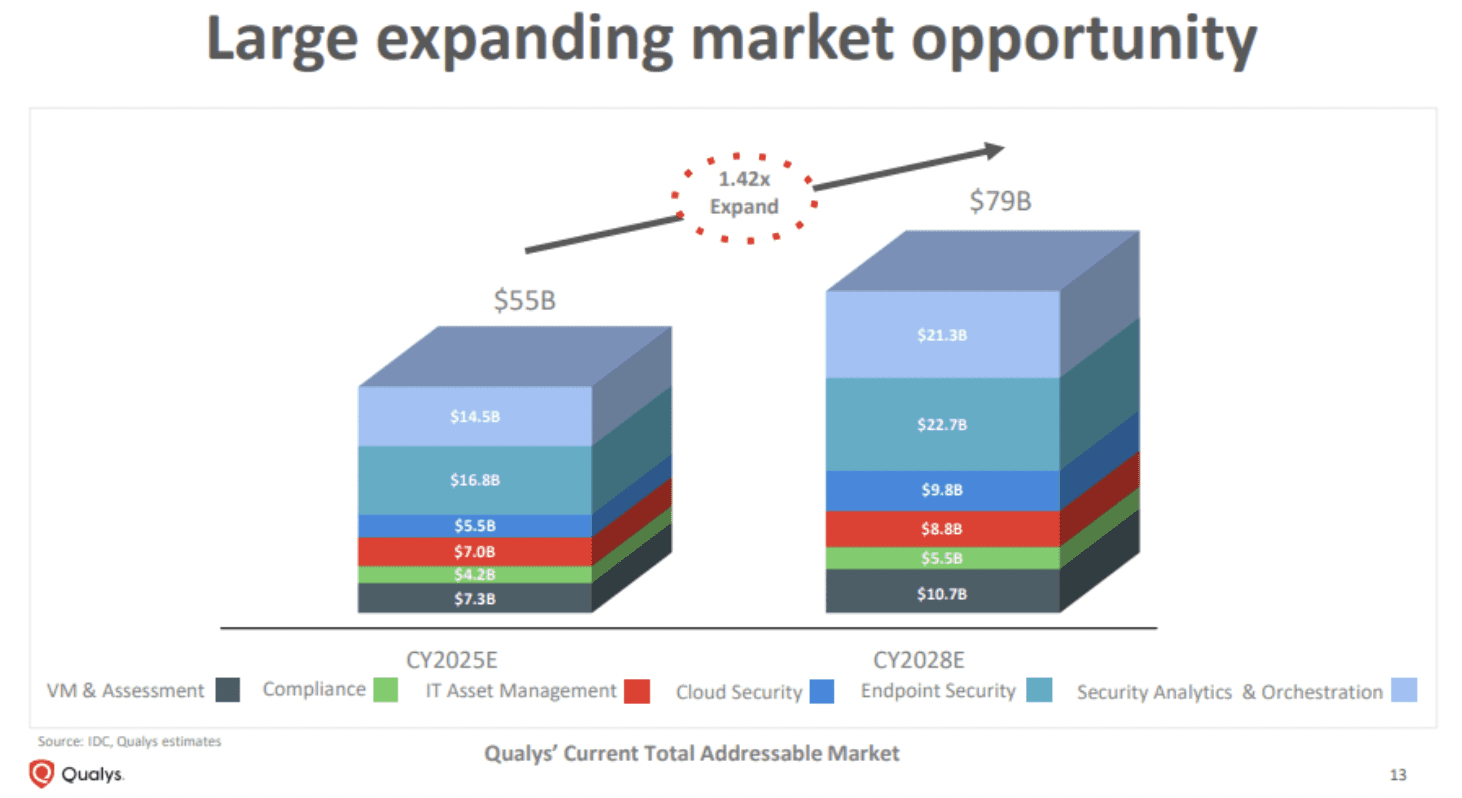

We view Qualys as representative of a broader theme unfolding across mid-tier cybersecurity companies firms that built strong platforms, achieved meaningful market penetration, but are now facing a growth plateau.

While giants like CrowdStrike and Palo Alto Networks continue to consolidate market share, companies like Qualys sit in a difficult middle ground profitable, efficient, and technologically sound, yet struggling to accelerate growth at the same clip as the leaders. When that happens, the next major catalyst often comes through M&A activity, as larger players seek bolt-on acquisitions to enhance platform breadth or integrate niche capabilities.

That’s the current risk-reward profile for Qualys.

The fundamentals remain sound: the company’s cloud-native platform and integrated suite of security solutions deliver customers a unified, scalable approach to compliance and vulnerability management.

Its high gross margins and robust cash flow generation underscore an efficient operating model that can withstand cyclical slowdowns.

But the headwinds are real. Competition is intensifying, with larger, better-capitalized peers aggressively expanding into overlapping product areas. This could pressure pricing and slow net new customer growth.

Moreover, the rapid evolution of the cybersecurity threat landscape demands continual reinvestment in R&D a costly requirement that can weigh on near-term profitability.

In short, Qualys stands at an inflection point: a steady, cash-generative operator whose next leg higher may depend less on organic momentum and more on strategic consolidation. If the M&A narrative plays out, upside could be significant. If not, investors could be in for a longer, more patient hold.

Description: Qualys, Inc. provides cloud-based platform delivering information technology (IT), security, and compliance solutions in the United States and internationally. It offers Qualys Cloud Apps, which include Cybersecurity Asset Management and External Attack Surface Management; Vulnerability Management, Detection and Response; Web Application Scanning; Patch Management; Custom Assessment and Remediation; Multi-Vector Endpoint Detection and Response; Policy Compliance; File Integrity Monitoring; and Qualys TotalCloud, as well as Cloud Workload Protection, Cloud Detection and Response, Cloud Security Posture Management, Infrastructure as Code, SaaS Security Posture Management, Kubernetes, and Container Security.

Qualys, Inc. has long been a pillar in the cybersecurity ecosystem, known for its cloud-based IT, security, and compliance solutions. Its foundation lies in vulnerability management (VM) — an area where it built both credibility and market leadership over two decades. The company’s Software-as-a-Service (SaaS) model delivers recurring, predictable revenue primarily through annual subscriptions to its Qualys Enterprise TruRisk Platform, which integrates multiple security applications into a single cloud-native framework.

While Qualys remains a recognized leader in VM, the competitive terrain around it has grown increasingly fierce. Direct rivals like Tenable (TENB) and Rapid7 (RPD) are competing aggressively for enterprise contracts, while platform giants such as Palo Alto Networks (PANW) and CrowdStrike (CRWD) have begun expanding into vulnerability and compliance management eroding Qualys’s traditional moat.

Financially, the company benefits from a sticky customer base and high-margin subscription model, with customers typically paying upfront for multi-year terms, creating large deferred revenue balances that are recognized over time.

This structure provides strong visibility and stability in cash flows, though it also highlights the importance of renewal growth and cross-sell momentum to sustain top-line expansion.

In short, Qualys remains a technically strong, cash-generative cybersecurity player, but one that must adapt to a market shifting toward integrated, full-stack security platforms.

Continued product innovation or potential consolidation within the space will determine whether it stays a leader or becomes an acquisition target in the next phase of cybersecurity evolution.

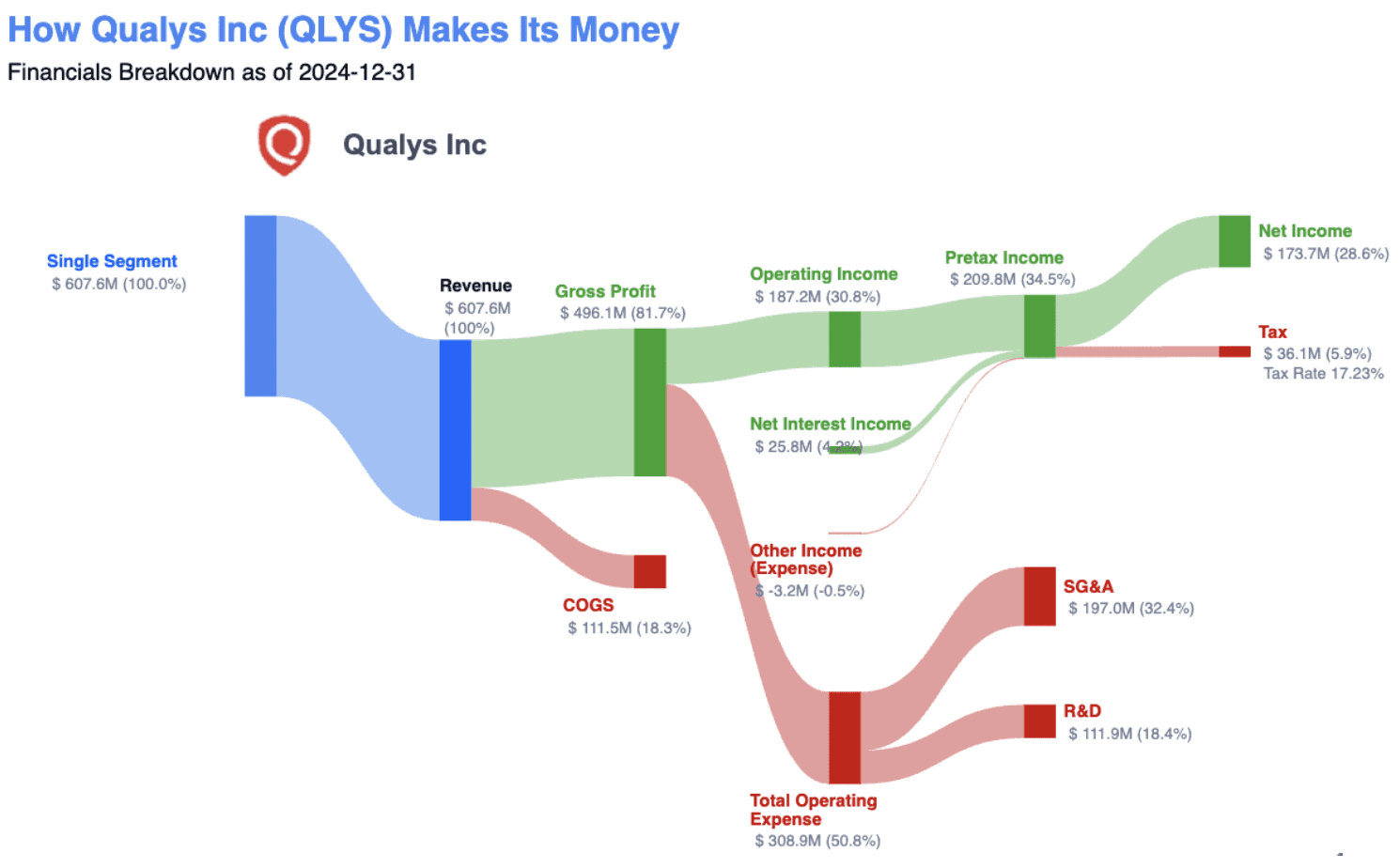

Qualys’ financial profile stands out sharply in a sector often defined by high growth but thin margins. The company’s disciplined execution and efficient SaaS model have made it one of the most profitable mid-cap names in cybersecurity, underscoring the strength and scalability of its platform.

Revenue Growth & Stability:

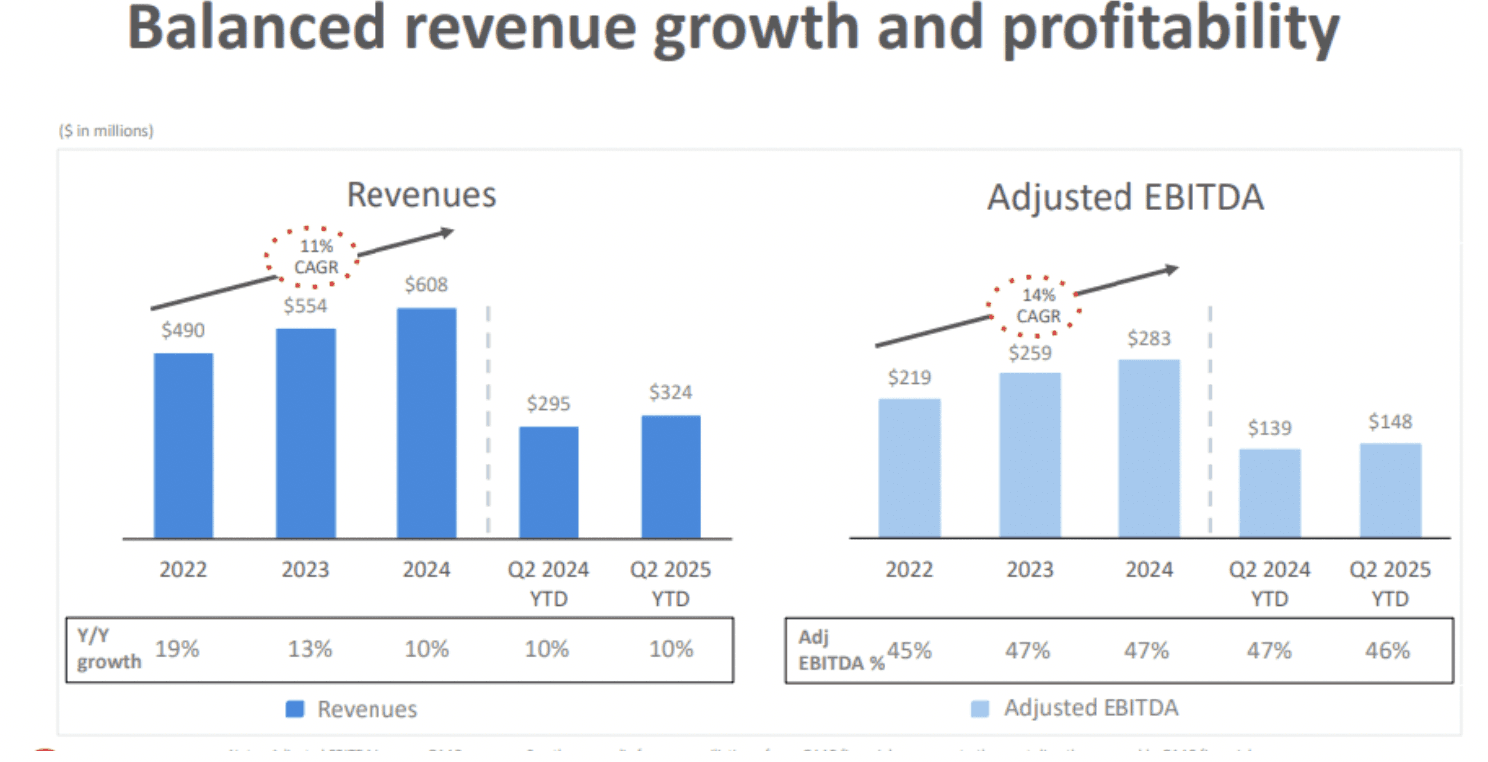

In 2024, Qualys delivered 12% year-over-year revenue growth, bringing total sales to $608 million. While not explosive by tech-sector standards, this steady growth reflects the resilience of its subscription-driven business model. With customers typically signing multi-year cloud platform contracts, Qualys benefits from a recurring, predictable revenue base that provides both stability and visibility into future cash flows.

This consistency highlights the company’s entrenched role in enterprise IT security stacks.

Exceptional Profitability & Operating Efficiency:

Where Qualys truly distinguishes itself is in profitability a rarity among cybersecurity peers still chasing scale.

Gross margin: Above 80%, reflecting the low incremental cost of serving new customers once the core cloud infrastructure is built.

Operating margin: Around 28%, showcasing tight cost control and a lean operational model.

Net income margin: Also near 28%, translating strong top-line performance directly into bottom-line results a mark of exceptional execution and pricing discipline.

In an industry where many competitors trade profitability for growth, Qualys delivers both sustainable expansion and elite margins. The combination of consistent revenue growth, recurring subscription income, and top-tier profitability positions the company as a financial standout and a potential strategic asset in an increasingly consolidated cybersecurity landscape.

Financially, Qualys achieved a 5-year revenue Compound Annual Growth Rate (CAGR) of approximately 12.1% from 2019 to 2024, though year-over-year growth slowed to 9.6% in 2024.

Despite this slowdown, the company maintains strong profitability, with GAAP operating margins consistently above 20% in recent years

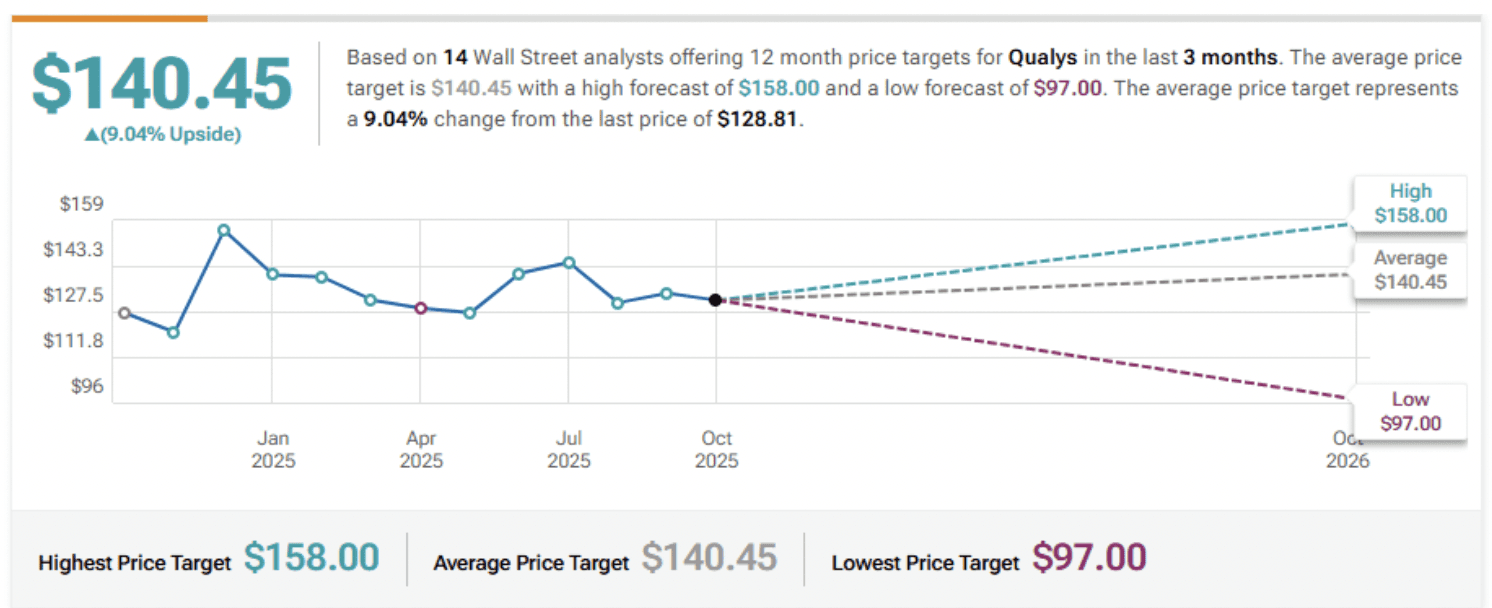

UBS Maintains Neutral on Qualys, Lowers Price Target to $145

Jefferies Maintains Hold on Qualys, Raises Price Target to $150

DA Davidson Maintains Neutral on Qualys, Raises Price Target to $135

Scotiabank Maintains Sector Perform on Qualys, Raises Price Target to $150

Morgan Stanley Maintains Underweight on Qualys, Raises Price Target to $97

Wedbush Maintains Outperform on Qualys, Raises Price Target to $155

Company: Super Micro Computer, Inc

Quote: $SMCI

BT: N/A

ST: $55-$60

Sharks Opinion:

SMCI’s stock has been on a wild ride since the start of the semiconductor supercycle rising sharply alongside Nvidia before diverging as scrutiny around its accounting practices and margin sustainability weighed on investor sentiment. Despite the turbulence, the company has proven remarkably resilient, continuing to deliver growth through its expanding AI server business and deep partnerships across the semiconductor ecosystem.

Valuation Context — Growth vs. Multiples:

SMCI’s current valuation demands a nuanced view — it’s not cheap, but there’s a reason for that premium:

P/E Ratio: Elevated versus historical norms, though arguably justified given strong top-line expansion and consistent earnings momentum.

EV/EBITDA: Remains competitive when measured against peers, supported by its dominant niche in AI-driven infrastructure.

Forward Growth Outlook: Analysts still forecast double-digit revenue and EPS growth over the next 3–5 years, reflecting sustained AI server demand and broader enterprise digital transformation.

Peer Comparison: Versus Dell, HPE, and Lenovo, SMCI trades at a premium multiple, underpinned by superior growth prospects and deeper exposure to AI workloads — but with tighter profit margins that cap near-term breakout potential.

While SMCI’s recent moves into data centers and large-scale AI infrastructure could eventually serve as a meaningful catalyst, execution will take both time and capital. For now, the fundamentals suggest limited near-term upside — we continue to see it as a double-digit stock rather than a renewed momentum play.

Scenario Outlook:

Bull Case: Accelerating AI server demand, stronger pricing power, and operational leverage drive earnings expansion, pushing shares higher.

Bear Case: Valuation compression, margin pressures, or supply chain challenges trigger a re- rating lower.

Base Case: SMCI remains a high-growth infrastructure name with credible long-term potential, but the stock’s steep valuation and cyclical risks temper expectations in the near term.

Description: Super Micro Computer, Inc., together with its subsidiaries, develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Super Micro Computer, Inc. (SMCI) has quickly evolved into one of the most strategically positioned hardware companies in the global computing landscape. Specializing in high-performance servers and storage systems, SMCI sits at the intersection of artificial intelligence (AI), cloud computing, and edge infrastructure three of the most powerful secular growth themes in technology.

The company’s recent growth surge reflects a perfect alignment with the AI- driven demand cycle, as hyperscalers, enterprises, and data centers seek optimized hardware platforms to support increasingly complex workloads.

Key Differentiators Driving SMCI’s Edge:

High Customization & Rapid Innovation: Unlike legacy OEMs such as Dell, HPE, or Lenovo, SMCI employs a modular, building-block architecture that enables rapid configuration and deployment. This agility allows the company to deliver bespoke server designs tuned to specific AI, cloud, and HPC applications.

Strategic Partnerships: SMCI maintains direct integration with leading semiconductor partners — NVIDIA, AMD, and Intel ensuring early access to cutting-edge chipsets and architectures vital to next-gen computing. This gives SMCI a consistent technological lead in GPU and CPU optimization.

Vertical Integration & Cost Efficiency: By controlling much of its design, manufacturing, and assembly in-house, SMCI reduces its dependency on external vendors. This vertical integration drives faster turnaround times, enhanced quality control, and higher operating leverage.

AI & HPC Tailwinds: As global spending on AI infrastructure accelerates, GPU- optimized server demand continues to climb sharply. SMCI’s ability to scale production and customize systems for specialized AI models positions it as a direct beneficiary of this ongoing capital investment wave.

Super Micro Computer (SMCI) continues to post robust financial results, reflecting its integral role in powering the current wave of AI-driven computing infrastructure. The company’s fundamentals paint the picture of a disciplined, growth-oriented operator with strong profitability, efficient capital management, and clear visibility into expanding demand cycles.

Key Financial Highlights:

Revenue Growth: SMCI delivered strong year-over-year revenue growth, propelled by surging global demand for AI-optimized server and storage hardware. Its close alignment with hyperscaler and enterprise data center spending continues to translate into sustained top-line momentum.

Gross Margins: The company has maintained healthy gross margins, signaling solid pricing power and operational efficiency. Its vertically integrated manufacturing model allows tighter cost control and faster adaptation to shifts in component pricing.

Operating Expenses: R&D and SG&A expenses have scaled proportionally with revenue, showing balanced investment discipline — funding innovation and sales expansion while protecting margins.

Net Income: Profitability remains strong, with significant year-over-year increases in net income, underscoring the leverage inherent in SMCI’s high-volume, high-margin business model.

Cash and Liquidity: SMCI maintains a healthy cash position, providing flexibility to fund new capacity expansions and navigate supply chain cycles.

Debt Levels: Leverage remains modest and well-managed, offering headroom for strategic investments or future capacity buildouts.

Inventory Management: Inventory turnover remains steady, highlighting effective supply chain coordination amid rising global demand for AI and HPC systems.

Strategic Positioning and Tailwinds:

SMCI’s core markets are aligned with the fastest-growing segments of global tech infrastructure:

AI & Data Center Expansion: The global AI infrastructure market is projected to grow at a CAGR above 30% through 2030, and SMCI’s GPU-optimized systems are directly at the heart of this buildout.

Cloud & Edge Computing: As workloads migrate to distributed cloud and edge environments, SMCI’s scalable, energy-efficient server platforms cater to hyperscalers, enterprises, and telecoms alike.

Enterprise AI Adoption: Corporations across sectors are integrating AI into core operations, driving demand for high-density GPU servers and custom hardware configurations both areas where SMCI holds clear technical advantages.

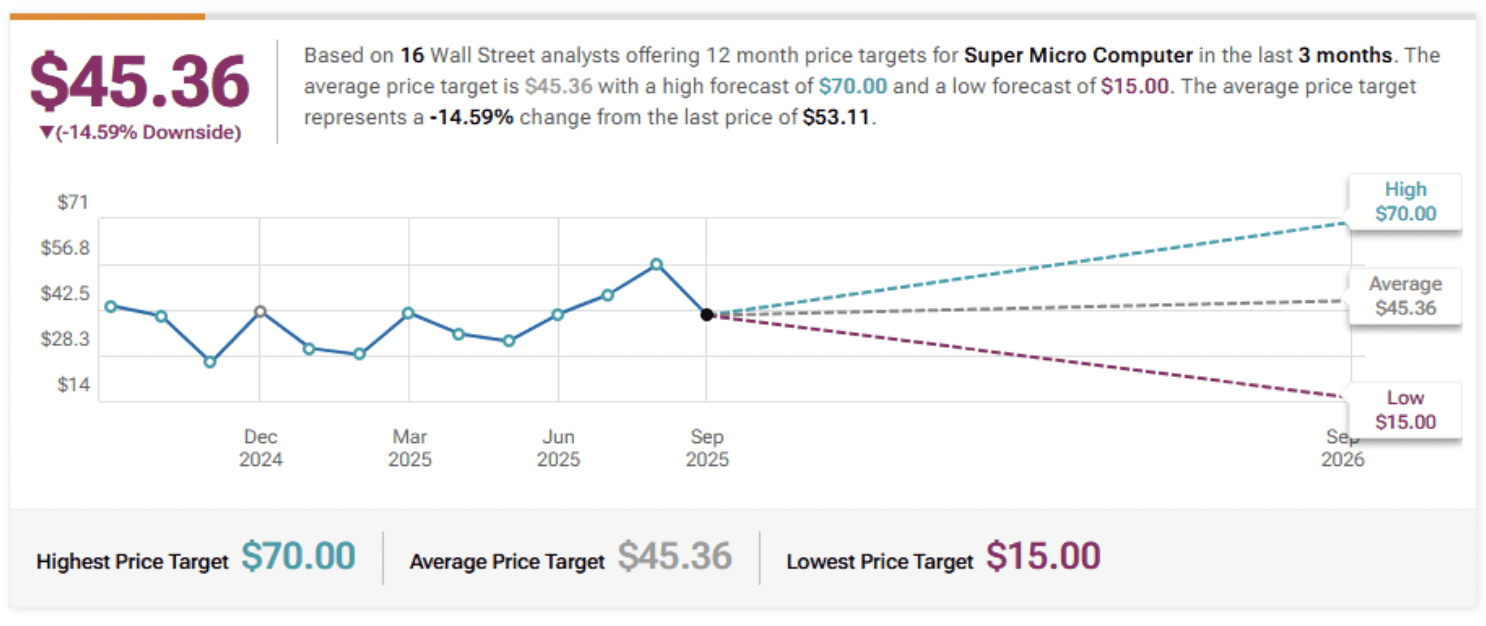

Bernstein Initiates Coverage On Super Micro Computer with Market Perform Rating, Announces Price Target of $46

Barclays Maintains Equal-Weight on Super Micro Computer, Raises Price Target to $45

JP Morgan Maintains Neutral on Super Micro Computer, Lowers Price Target to $45

Wedbush Maintains Neutral on Super Micro Computer, Raises Price Target to $48

Goldman Sachs Maintains Sell on Super Micro Computer, Raises Price Target to $27

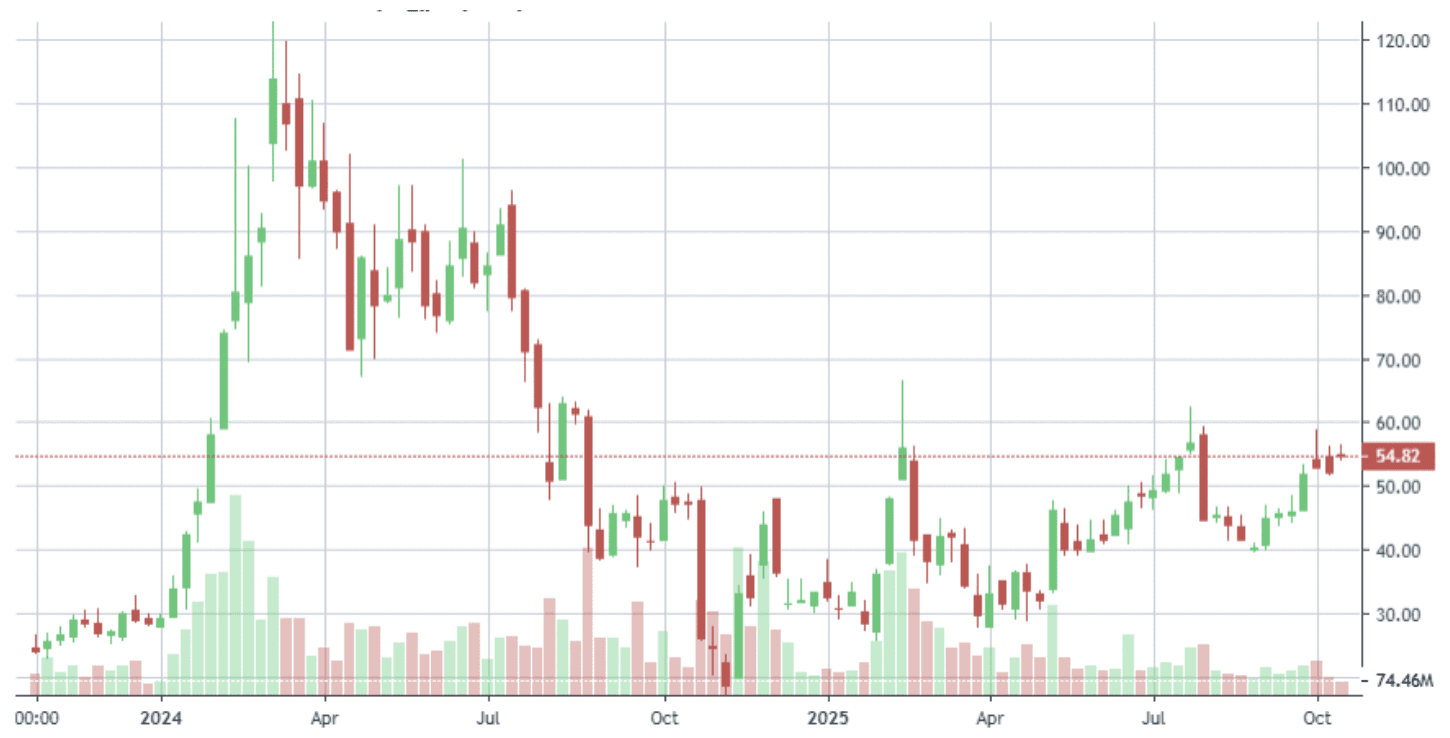

Company: IonQ, Inc.

Quote: $IONQ

BT: N/A (would avoid)

ST: $12- $20

Sharks Opinon:

Quantum computing has become one of the most hyped frontiers in technology investing. Over the past year, the sector has drawn billions in speculative capital, sending valuations for companies with limited commercial traction soaring. Some names have seen share prices multiply by several thousand percent reflecting investor enthusiasm more than business fundamentals.

Among these, IONQ stands out as the emblem of this speculative wave. The company’s meteoric rise has been driven almost entirely by narrative, not numbers. While IONQ positions itself as a leader in trapped-ion quantum computing, its financial reality tells a different story: persistent operating losses, minimal recurring revenue, and a business model still years away from commercial scale.

IONQ’s most successful product to date has arguably been its stock issuance program.

Through repeated share offerings, the company has managed to fortify its balance sheet but at the expense of shareholders, who face constant dilution. The company continues to burn through cash each quarter without a viable path to sustainable revenue or profitability.

In our view, IONQ represents the speculative extreme of the quantum sector a company priced for perfection in a field that remains deeply experimental. Until IONQ can demonstrate tangible progress in monetization and product delivery, we see it as a strong sell, emblematic of the broader irrational exuberance driving the quantum bubble.

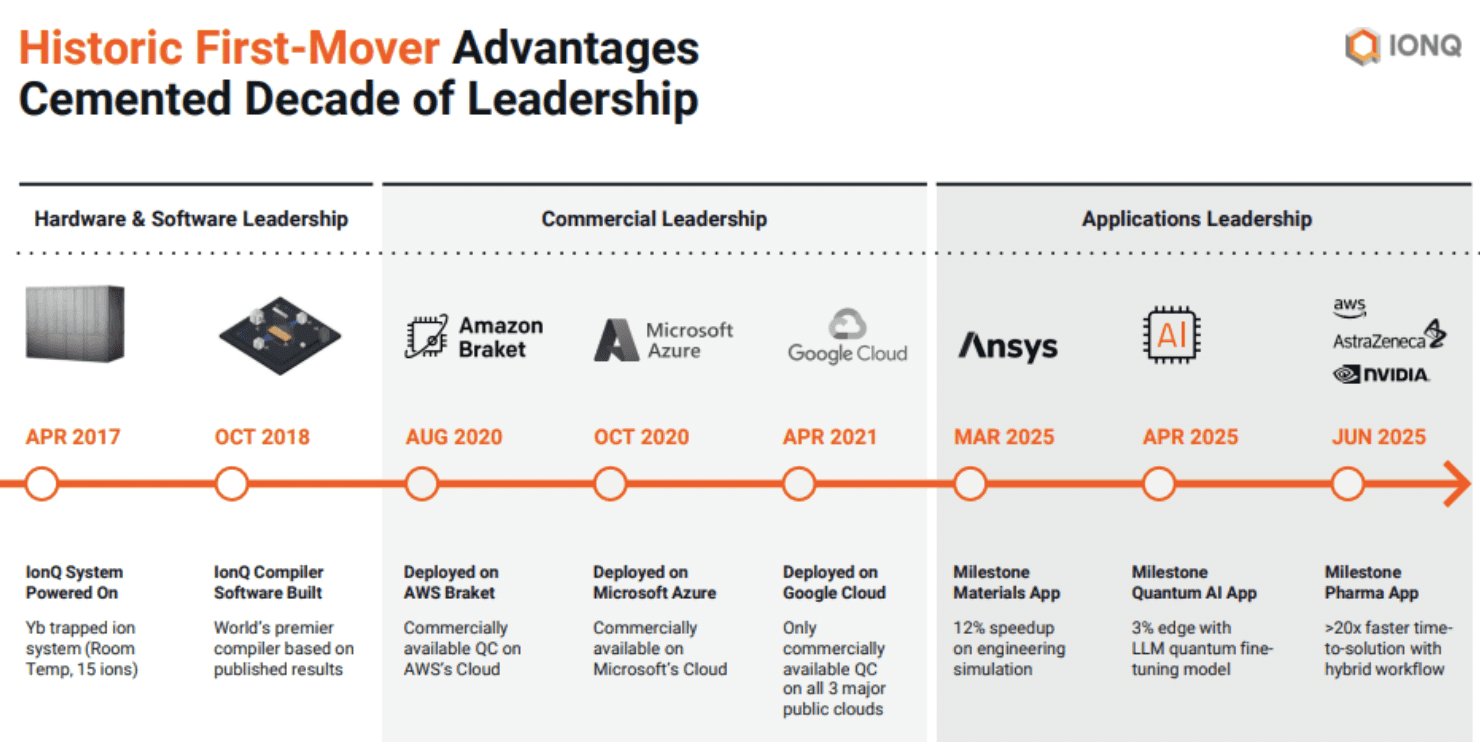

Description: IonQ, Inc. develops quantum computers and networks in the United States. It sells access to quantum computers of various qubit capacities. The company also makes access to its quantum computers through cloud platforms, such as Amazon Web Services (AWS) Amazon Braket, Microsoft's Azure Quantum, and Google's Cloud Marketplace, as well as through its cloud service.

As remarkable as IonQ’s stock performance has been, the company’s breakthroughs are still far from bringing quantum computing into practical, everyday use. Current systems remain confined to controlled lab environments, where engineers continue to battle persistent issues such as qubit coherence and scalability—fundamental obstacles that make large-scale quantum computing years, if not decades, away from mass adoption.

Competition is also intensifying. Tech giants like IBM, Google, and Amazon are investing heavily in proprietary quantum technologies, while dozens of startups crowd the same theoretical frontier. Meanwhile, growing regulatory focus on quantum-safe encryption adds yet another layer of uncertainty, as governments and corporations seek to protect current systems from potential future quantum threats.

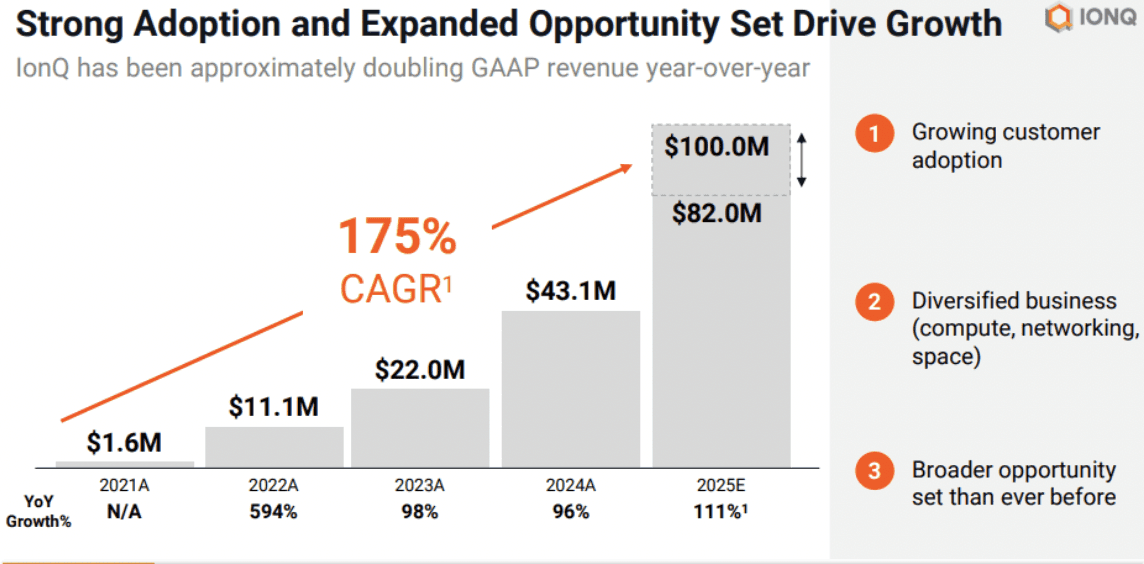

Despite posting triple-digit revenue growth, IonQ’s financial base remains small —revenues measured in mere millions per year, dwarfed by its multi-billion- dollar valuation. The company’s growth narrative is entirely dependent on execution and investor patience, both of which could falter amid technological setbacks or tighter funding conditions in the venture space.

That said, IonQ has built notable technical and strategic momentum. The acquisition of Oxford Ionics expanded its patent portfolio and established a strong foothold in the United Kingdom, enhancing its position as a global quantum player. The company’s roadmap highlighting a 256-qubit demonstration by 2026 and ambitions to scale toward million-qubit systems by 2030 is ambitious, positioning IonQ as a potential backbone of future quantum infrastructure.

IonQ’s business model remains a delicate balance between high-risk R&D investment and modest revenue streams from government contracts, research collaborations, and cloud-based quantum services (QCaaS). For now, its valuation is driven less by what the company earns and more by what it might achieve—a bet on the future of computation itself.

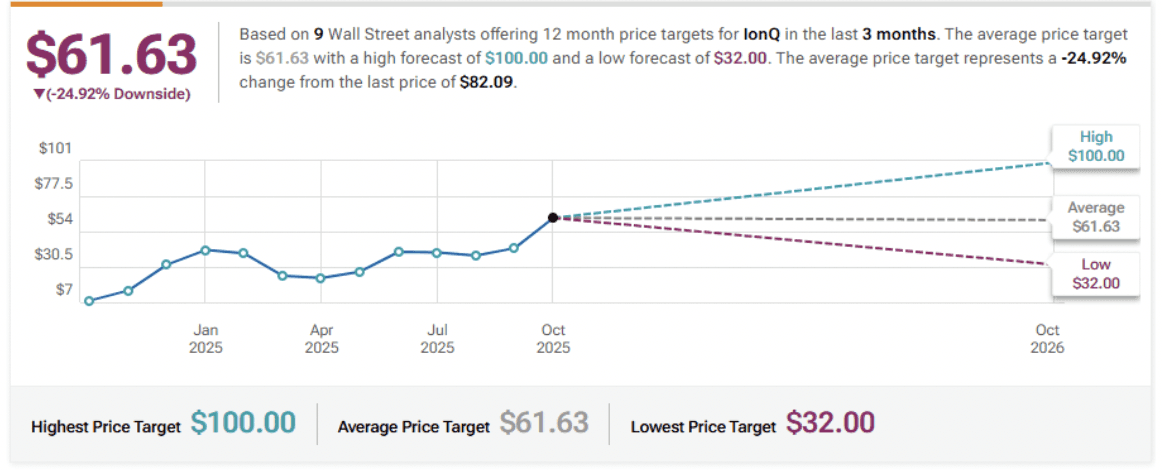

B. Riley Securities Maintains Buy on IonQ, Raises Price Target to $100

Needham Reiterates Buy on IonQ, Maintains $80 Price Target

Cantor Fitzgerald Maintains Overweight on IonQ, Raises Price Target to $60

Rosenblatt Maintains Buy on IonQ, Maintains $70 Price Target

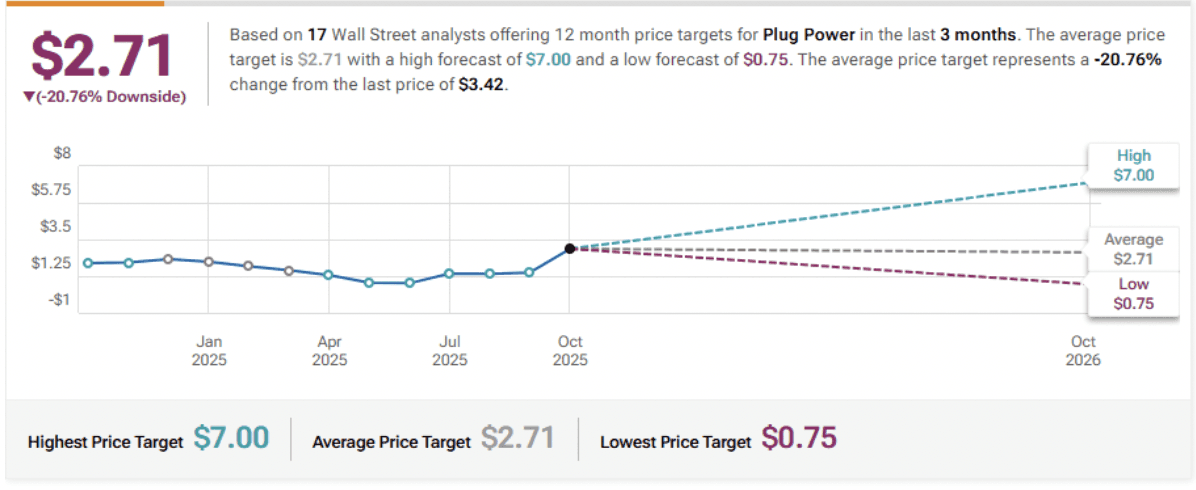

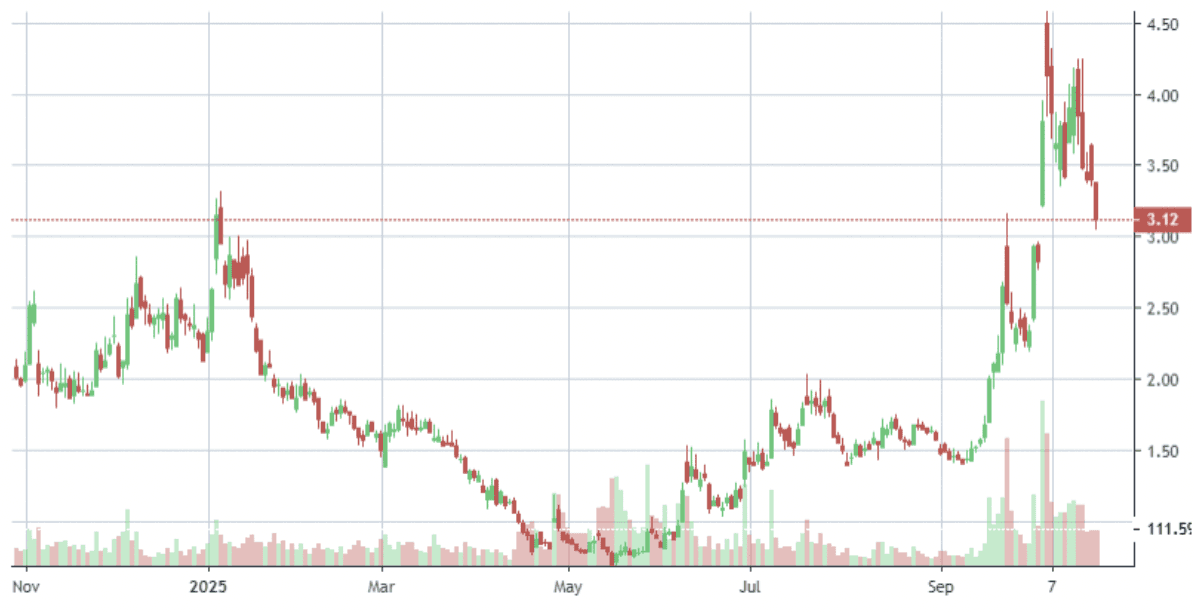

Company: Plug Power Inc.

Quote: $PLUG

BT: N/A (would avoid)

ST: $1.50

Sharks Opinion:

If investors thought IonQ’s dilution was aggressive, Plug Power redefines the term. With a staggering float exceeding 1.15 billion shares, the company has effectively turned shareholder dilution into a business strategy.

Despite being publicly traded since 1997, Plug Power has never posted a profit, and its financial trajectory remains alarming net income losses are now roughly double its total revenue.

For over two decades, the company has pitched the same vision: a clean hydrogen-powered future.

Yet after countless capital raises, government incentives, and strategic pivots, the fundamentals tell a far different story. Operational inefficiency, high cash burn, and ongoing dilution have eroded long-term shareholder value.

With a market valuation disconnected from fundamentals and a track record spanning nearly three decades without sustainable earnings, Plug Power represents one of the clearest examples of speculative excess in the clean energy space. In our view, this is a company to avoid entirely.

Until it can prove operational discipline, show positive cash flow, or at least reduce dependence on dilution to survive, Plug Power remains a cautionary tale not a comeback story.

Description: Plug Power Inc. develops hydrogen fuel cells product solutions in North America, Europe, Asia, and internationally. The company offers GenDrive, a hydrogen fueled proton exchange membrane (PEM) fuel cell system that provides power to material handling electric vehicles; GenSure, a stationary fuel cell solution that offers modular PEM fuel cell power to support the backup and grid-support power requirements of the telecommunications, transportation, and utility sectors; and Progen, a fuel cell stack and engine technology used in mobility and stationary fuel cell systems.

Hydrogen fuel remains far from economically viable, even after decades of development. While costs have dropped since Plug Power’s founding in 1997, alternatives like wind and solar continue to outpace hydrogen in efficiency and adoption. Certain sectors like aviation or steel still face major technological hurdles in switching to low-carbon fuels, but that doesn’t make hydrogen any more investable today.

The second key point: we don’t yet know which hydrogen technology will dominate long-term. Plug Power focuses on proton exchange membrane (PEM) systems, which use electricity and water at low temperatures to generate hydrogen. Competing approaches, like solid oxide electrolysis cells (SOEC), use high heat and electricity, offering different efficiency and application advantages. PEM is more scalable today and better suited for variable loads, but SOEC could outperform in industrial settings with waste heat recovery. Betting on Plug Power isn’t just a bet on hydrogen it’s a bet specifically on PEM technology, with all the uncertainty that entails.

The reality for Plug Power is grim: its markets aren’t expanding fast enough to offset massive cash burn, and shareholder dilution is the only thing keeping it alive. For now, the company is trapped between slow-growing end markets and unsustainable losses, making it a highly risky proposition. For cautious investors, the bigger question isn’t if it can thrive—it’s whether it will survive another 25 years.

Susquehanna Maintains Neutral on Plug Power, Raises Price Target to $3.5

Clear Street Downgrades Plug Power to Hold, Announces $3.5 Price Target

HC Wainwright & Co. Maintains Buy on Plug Power, Raises Price Target to $7

Wells Fargo Maintains Equal-Weight on Plug Power, Raises Price Target to $1.5

BMO Capital Maintains Underperform on Plug Power, Lowers Price Target to $1

Jefferies Maintains Hold on Plug Power, Raises Price Target to $1.6

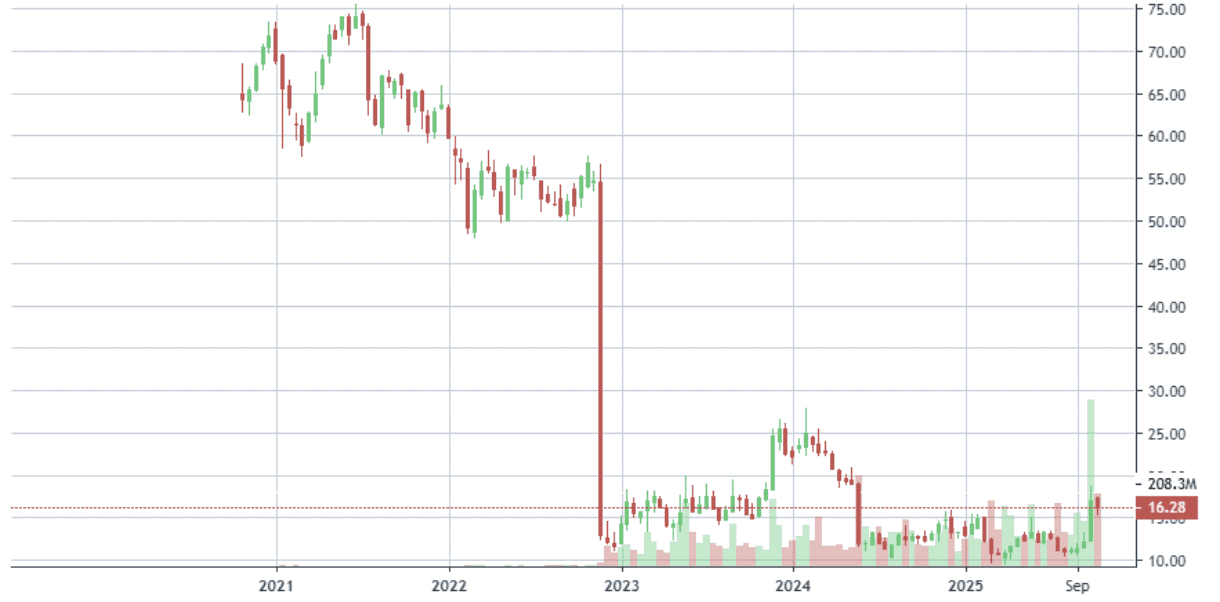

Company: UiPath Inc.

Quote: $PATH

BT: $10-$12

ST: $16-$18

Sharks Opinion: UiPath soared during the pandemic-driven tech boom, but since 2023, the stock has struggled to regain footing and for good reason. The company remains unprofitable, and without a clear path to earnings, upside is limited.

Recent insider selling during minor rebounds underscores caution. While the stock superficially aligns with 2025 tech themes, fundamentals suggest it’s plateaued, offering little reason for us to consider it as an investment at this time.

Description: UiPath Inc. provides an end-to-end automation platform that offers a range of robotic process automation (RPA) solutions primarily in the United States, Romania, the United Kingdom, the Netherlands, and internationally. The company delivers software robots that emulate human actions with precision and speed for organizations to automate repetitive tasks.

UiPath’s core product, the UiPath Platform, enables “agentic automation,” allowing AI, robots, and humans to collaborate for faster, smarter business operations. Originally focused on robotic process automation (RPA) for repetitive tasks, the company has expanded into AI, machine learning, and natural language processing to tackle more complex automation.

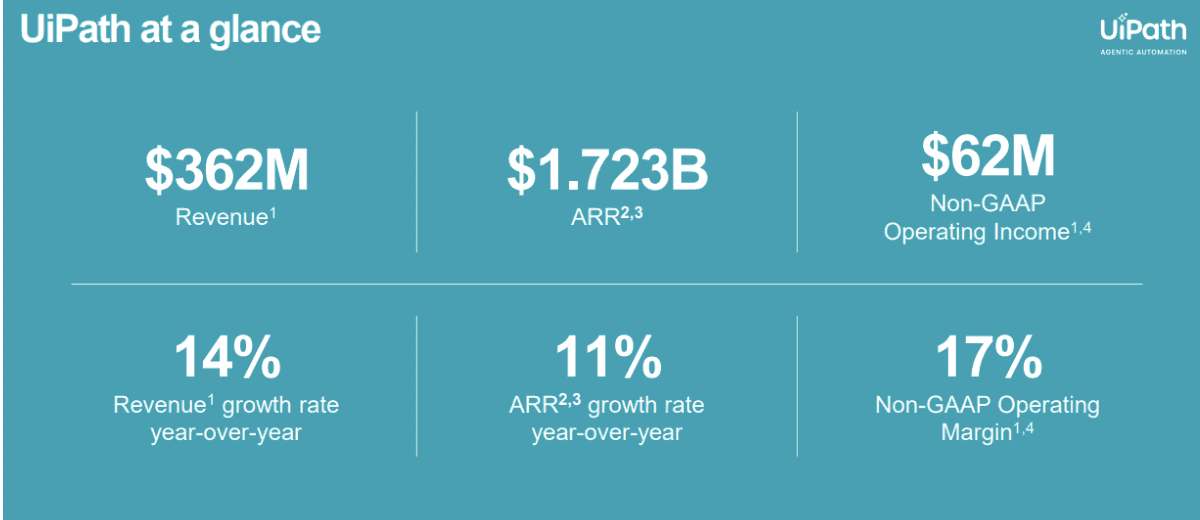

In its most recent quarter, annual recurring revenue (ARR) grew 11% to $1.72 billion, surpassing guidance, while cloud ARR jumped 25%, passing $1 billion.

Net revenue retention stabilized at 108%, signaling that existing customers are increasing spending. The public sector business is rebounding, and adjusted operating margins rose to 17% after prior cost-cutting and restructuring.

Q2 fiscal 2026 results showed total revenue up 14% YoY to $362 million, with ARR increasing 11% YoY, including $31 million in net new ARR. Gross margin remained strong at 84%, and the company broke even this quarter, improving from a $0.15 per share loss last year.

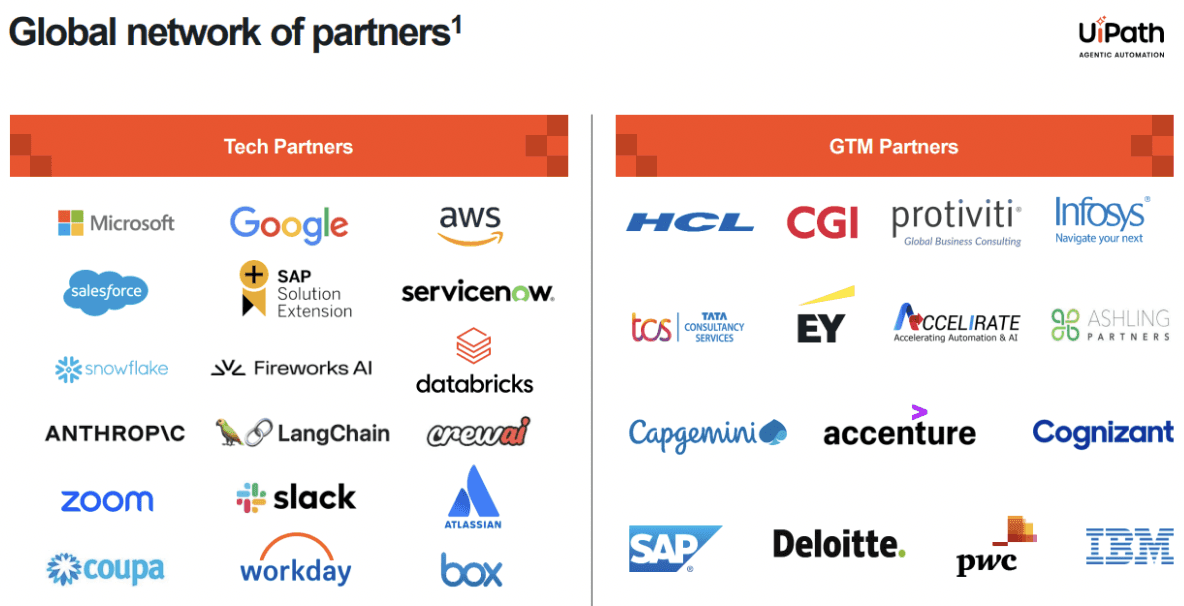

UiPath is leveraging its agentic AI strategy to drive growth, partnering with Deloitte, Cognizant, and Microsoft, which endorses UiPath as its enterprise automation platform. Customer expansion continues, with 10,820 total customers, 2,432 contributing over $100,000 ARR, and 320 contributing over $1 million ARR. The net retention rate remained at 108%, highlighting the stickiness of its enterprise relationships.

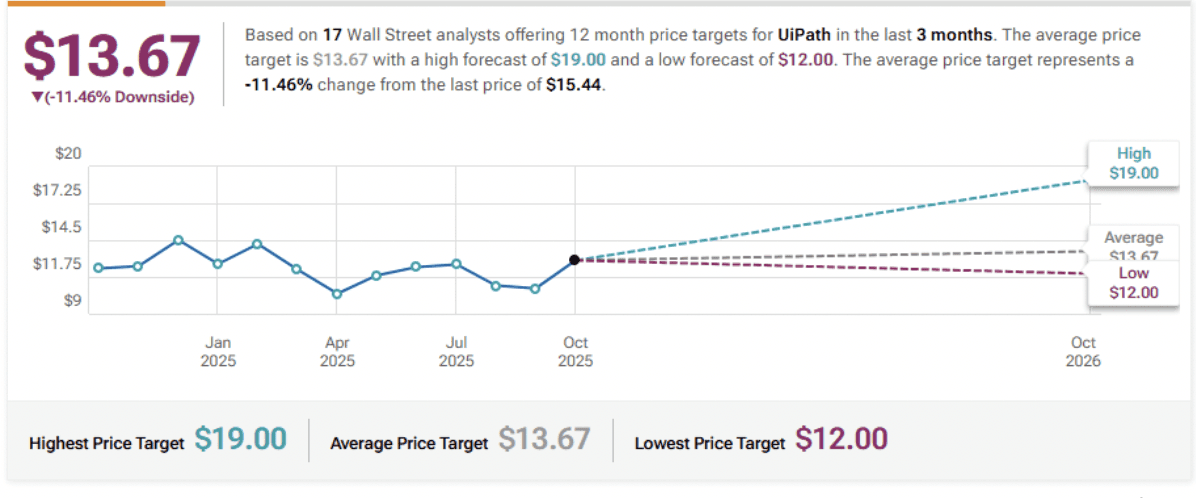

BMO Capital Maintains Market Perform on UiPath, Raises Price Target to $13

Truist Securities Maintains Hold on UiPath, Lowers Price Target to $12

DA Davidson Assumes UiPath at Neutral, Lowers Price Target of $12

Morgan Stanley Maintains Equal-Weight on UiPath, Raises Price Target to $15

Company: TeraWulf Inc.

Quote: $WULF

BT: $8

ST: $16

Sharks Opinion:

Terrawulf (WULF) has seen a big run in 2025, fueled largely by hype around its pivot from bitcoin mining to high-density data centers.

The company now leases liquid-cooled rooms and sells electricity to customers on a monthly basisshifting from mining profits to megawatt rentals. Short-term, this could drive the stock toward $20, but long-term fundamentals look weak.

The pivot feels more like a desperation move than a sustainable strategy. Just recently, WULF announced a $3.2 billion notes offering.

Considering the company trades at a $5 billion valuation on quarterly revenues of $47 million while operating at a loss, the fundamentals are shaky. While hype could push the stock higher temporarily, from an analytical standpoint, we remain bearish.

Description: TeraWulf Inc., together with its subsidiaries, operates as a digital asset technology company in the United States. The company develops, owns, and operates bitcoin mining facilities in New York and Pennsylvania. It is involved in the provision of miner hosting services to third-party entities. The company was founded in 2021 and is headquartered in Easton, Maryland.

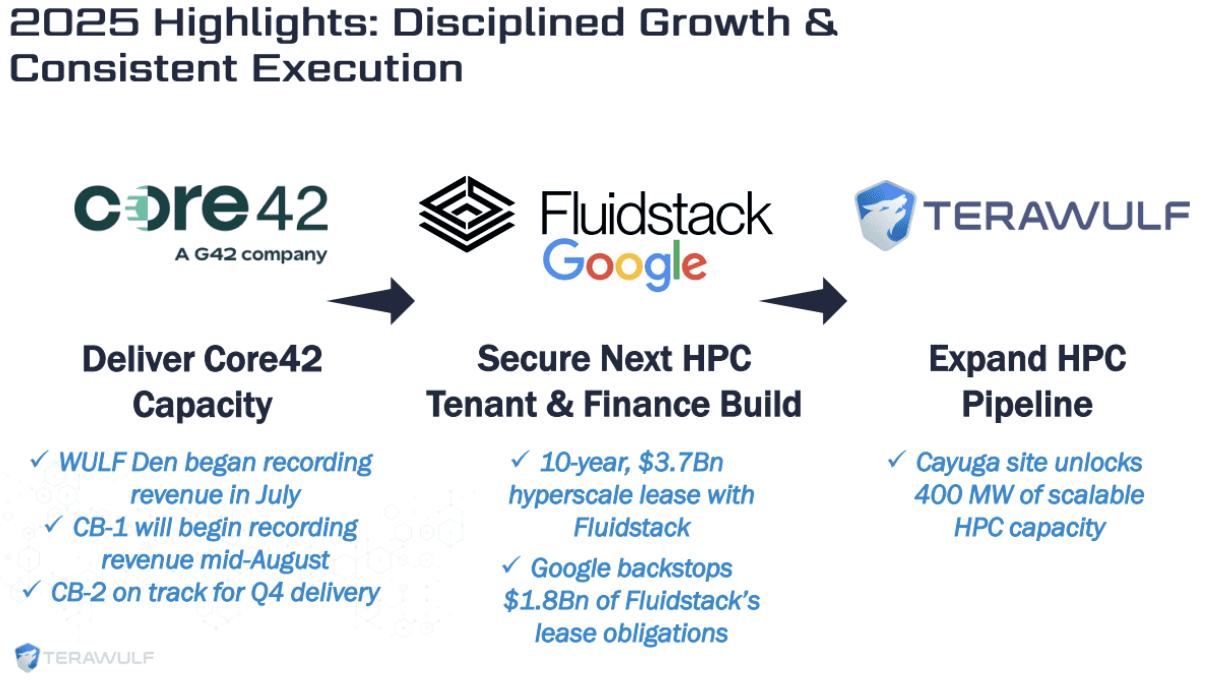

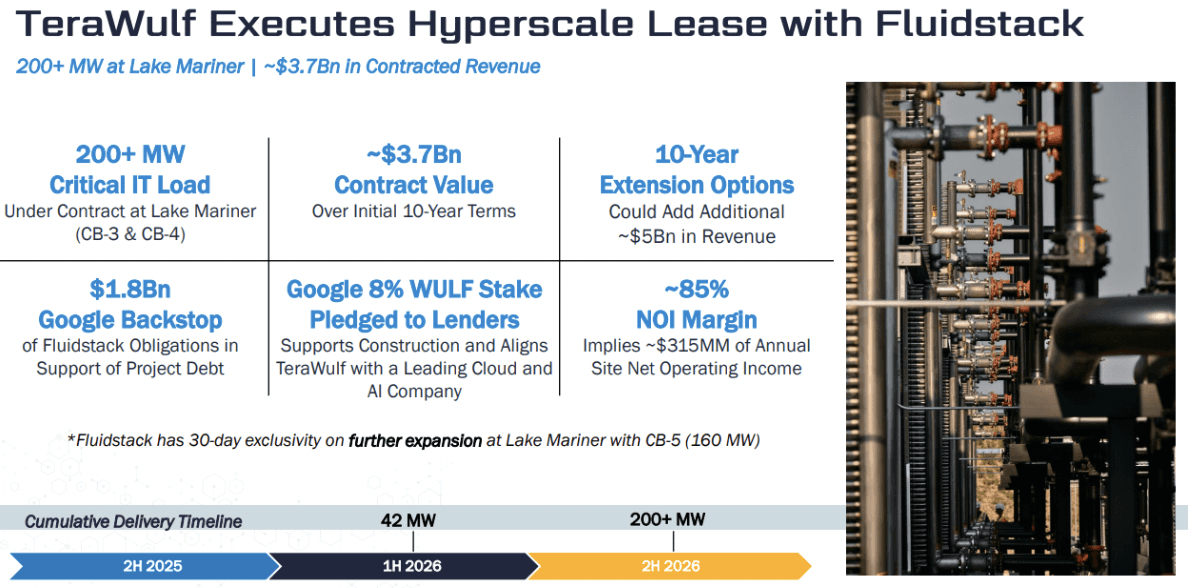

TeraWulf , originally a Bitcoin mining operator, has been aggressively pivoting into high-performance computing (HPC) data centers, signaling a strategic shift from pure cryptocurrency mining to leasing and powering liquid-cooled data center space. The company recently announced a major strategic partnership with Google as part of its co-location agreements with Fluidstack. Under this arrangement, Google will backstop approximately $1.8 billion of Fluidstack’s lease obligations, providing critical support for project-related debt financing.

As part of the deal, Google also holds a warrant to acquire roughly 41 million shares of TeraWulf common stock, which would represent an approximate 8% pro forma equity stake if exercised. This partnership provides both credibility and financial support, positioning TeraWulf as a more formidable player in the high-efficiency data center space.

The company is also pursuing a substantial $3 billion debt financing round, structured by Morgan Stanley, to support its expansion into data center operations. This move aligns with TeraWulf’s broader pivot away from standalone mining operations toward providing fully powered, liquid-cooled rooms for HPC clients, who pay monthly rent for electricity and space. The pivot reflects the company’s recognition that leasing megawatts and offering infrastructure as a service could provide a more sustainable revenue model than cryptocurrency mining alone.

From a financial perspective, TeraWulf reported a 34% increase in revenue for Q2 2025, totaling $47.6 million. The company also holds strong reserves, with $90 million in cash and Bitcoin, giving it flexibility to fund operations and support its ambitious expansion plans. However, despite these topline gains, profitability remains a critical challenge.

The company reported an EBIT margin of -99.1% and an EBITDA margin of -53.5%, underscoring the difficulty of turning revenue growth into meaningful operating profit.

While the Google partnership and debt financing provide significant growth opportunities, the company’s financials highlight the risks inherent in its business model. Investors should weigh the excitement around short-term growth and strategic partnerships against the ongoing challenges of converting revenue into sustainable profits.

In short, TeraWulf presents a high-risk, high-reward proposition: it has potential to capitalize on the growing demand for HPC data center services, but fundamentals indicate that profitability and operational efficiency remain long-term hurdles.

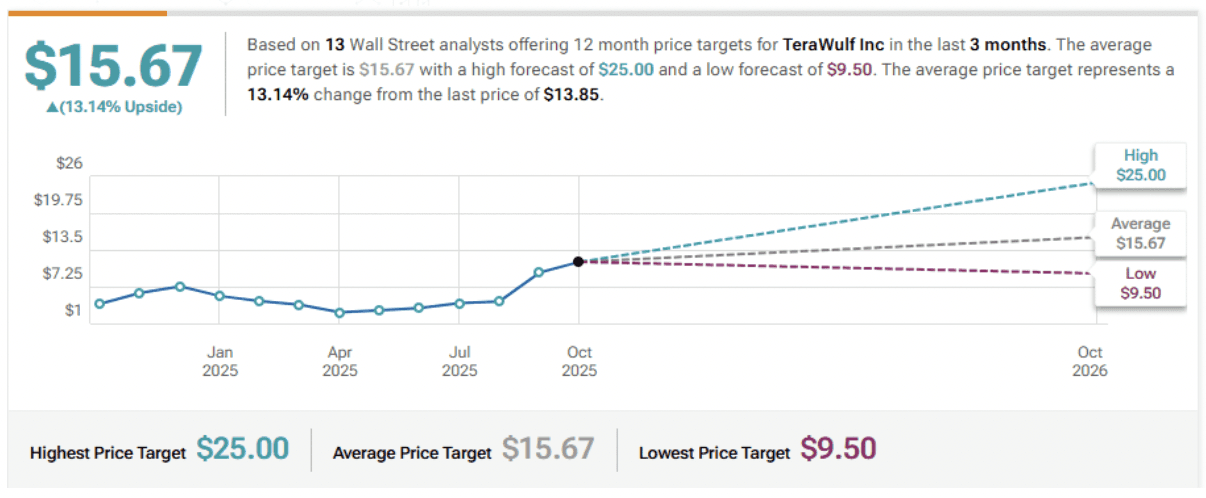

JMP Securities Maintains Market Outperform on TeraWulf, Raises Price Target to $18

Rosenblatt Maintains Buy on TeraWulf, Raises Price Target to $14.5

Roth Capital Maintains Buy on TeraWulf, Raises Price Target to $21.5

Northland Capital Markets Maintains Outperform on TeraWulf, Raises Price Target to $15