This is a list of stocks that members asked us to do extra research on none of these are alerts/buy/sell recommendations.

Company: SoFi Technologies

Quote: $SOFI

Bull Case:

SoFi just printed a monster quarter. Originations hit a record $10.5B, up 46% year over year, powered by strong loan platform activity. GAAP revenue came in at $1.025B, up nearly 40% and ahead of expectations, driven by higher net interest income, platform revenue, and interchange fees. They added one million members in the quarter alone and deposits climbed to a record $37.4B. The growth engine is clearly still running, and the path to their 2026 targets looks intact.

Bear Case:

Despite record numbers, the stock sold off roughly 10% after earnings. The concern isn’t what they just did it’s what happens if the economy rolls over. A prolonged downturn could pressure credit quality, increase loan loss provisions, and weigh on capital ratios. On top of that, demand for personal loans could soften, credit metrics could deteriorate, and newer product adoption might slow. The market is questioning how resilient the model really is in a tougher macro backdrop.

Sharks Opinion:

SoFi Technologies is a name we’ve followed closely for years, and management has executed at a high level growing the business, scaling deposits, and reaching profitability. That matters.

But fintech is crowded. Beyond traditional banks, you’ve got public competitors like Nu Holdings and Chime, plus private players like Revolut and Neo Financial waiting in the wings. It’s not easy to stand out in a space where everyone offers some version of digital banking.

What makes SoFi different is the vertically integrated stack. One app where members can manage loans, deposits, and investments and they hold a bank charter, which lowers funding costs and deepens the moat.

Long term, we believe the company deserves a premium multiple and could work its way toward a $40 target.

But the market may take its time rewarding that. At the end of the day, it’s still viewed as a neobank and those rarely rerate overnight.

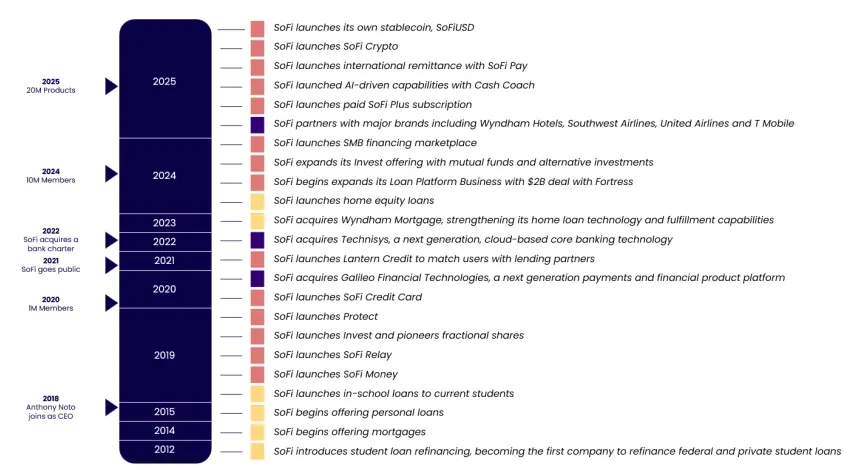

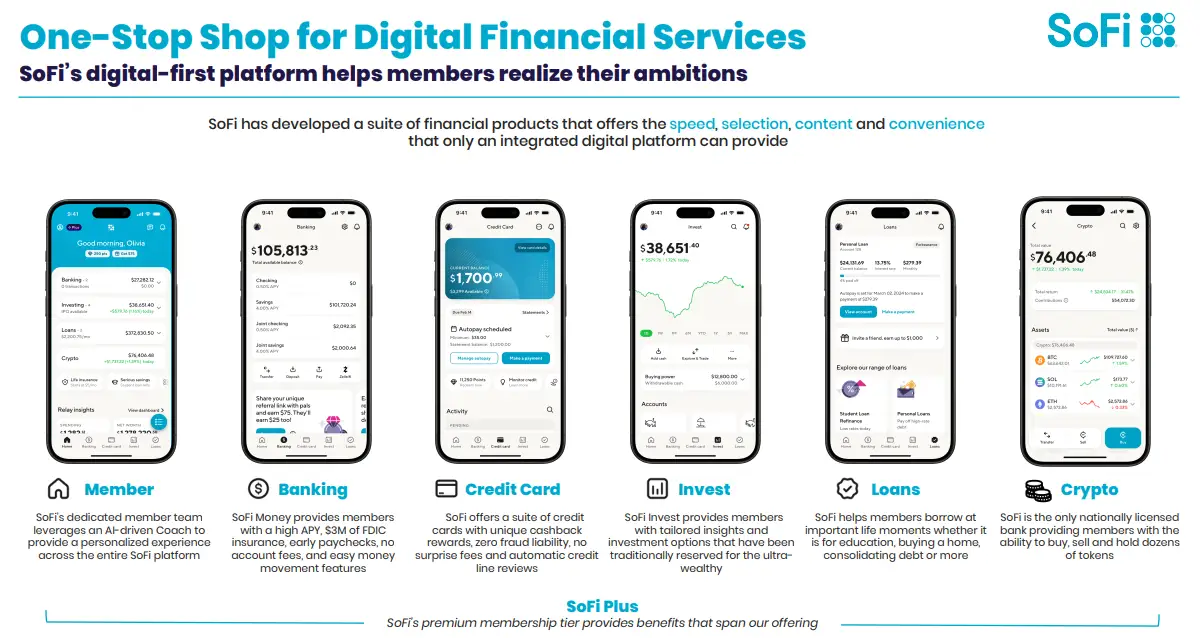

Description: SoFi is a financial-services company that was founded in 2011 and is based in San Francisco. Initially known for its student loan refinancing business, the company has expanded its product offerings to include personal loans, credit cards, mortgages, investment accounts, banking services, and financial planning. The company intends to be a one-stop shop for its clients' finances and operates solely through its mobile app and website. Through its acquisition of Galileo in 2020, the company also offers payment and account services for debit cards and digital banking.

In a nutshell, SoFi Technologies is a fintech platform built to help members get their money right all in one place. Borrow, save, spend, invest, and protect your money through a single digital ecosystem.

At a high level, the company operates across three core segments. First is Lending the flagship engine. SoFi offers personal, student, and home loans, handling everything from application and underwriting to funding and servicing directly in-app. It also operates Lantern, its marketplace that connects borrowers with third-party lenders.

Second is Financial Services. This includes checking and savings, investing (stocks, IPOs, alternatives, and robo-advising, with crypto expected to relaunch), credit cards, budgeting tools, credit score monitoring, and insurance offerings through partnerships. They also monetize engagement through SoFi Plus, a premium membership tier tied to direct deposit and subscription perks.

Third is the Technology Platform. Through acquisitions like Galileo Financial Technologies and Technisys, SoFi provides banking-as-a-service infrastructure to enterprise clients. That includes digital banking, card issuing, payments, and risk management effectively powering other fintechs behind the scenes. Clients include names like Dave, Robinhood, and Toast.

As for competition, neobanks like Block, Chime, and Revolut compete on the consumer side — but they don’t have the same banking-as-a-service layer that Galileo provides. Robinhood is a contender in investing, but it lacks a bank charter and doesn’t originate loans. Meanwhile, PayPal is more focused on checkout and payments, making it less of a direct overlap.

The differentiator remains the vertically integrated model consumer finance on the front end, infrastructure on the back end all under one roof.

Combined with its growing brand presence, SoFi Technologies is positioned to continue attracting new members at scale.

High-profile marketing has played a major role from securing naming rights to SoFi Stadium, to becoming the official banking partner of the National Basketball Association, to sponsoring the tech-driven TGL. These partnerships build credibility and keep the brand in front of a national audience.

The strategy is simple: attract members with brand and product quality, then deepen the relationship over time. The more products a member adopts lending, deposits, investing, credit the stronger the ecosystem becomes and the higher the lifetime value.

From a competitive standpoint, the moat rests on three pillars.

First, the all-in-one fintech stack a vertically integrated platform serving both consumers and enterprise clients. Second, strong resonance with younger demographics, allowing SoFi to acquire customers early and cross-sell products as their financial lives expand.

Third, a structural cost advantage driven by its bank charter, funding model, and integrated technology platform giving it operating leverage many peers simply don’t have.

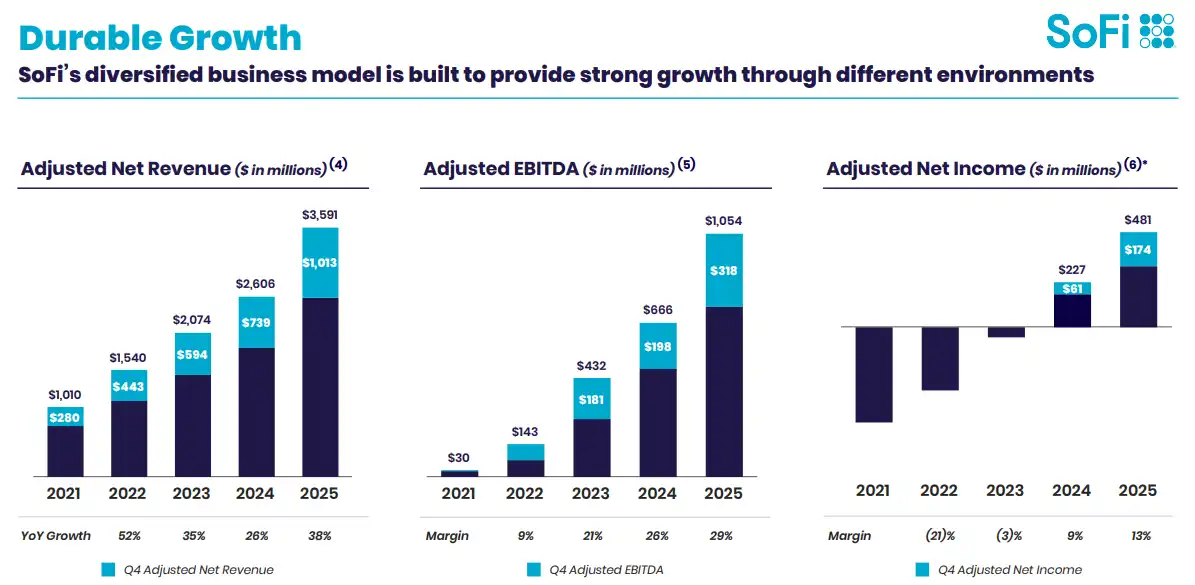

SoFi Technologies just delivered another quarter of record performance across the board.

In Q4 2025, GAAP net revenue hit a record $1.0 billion, up 40% year over year from $734 million. Adjusted net revenue also reached $1.0 billion, growing 37% versus last year. Fee-based revenue came in at a record $443 million, up 53%, driven by strength in the Loan Platform Business, referral fees, interchange, and brokerage revenue. Combined, the Financial Services and Technology Platform segments generated $579 million in net revenue a 61% increase from the prior year.

Net interest income rose 31% year over year to $617 million, supported by a 35% increase in average interest-earning assets and a 50-basis-point decline in cost of funds. Net interest margin came in at 5.72%, down slightly from 5.91% last year due to mix shifts and lower asset yields. Importantly, the average deposit rate was 181 basis points lower than warehouse funding costs, translating to roughly $680 million in annualized interest expense savings as the company optimized its funding base. During the quarter, SoFi also paid down its remaining warehouse lines using proceeds from its public offering.

Profitability continues to scale. Adjusted EBITDA reached a record $318 million, up 60% year over year, representing a 31% margin. This marked the ninth consecutive quarter of GAAP profitability, with net income of $173 million and diluted EPS of $0.13.

On the balance sheet, equity increased by $1.7 billion to $10.5 billion, with tangible book value rising to $8.9 billion. Tangible book value per share climbed to $7.01, up significantly from $4.47 a year ago, supported in part by $1.5 billion of new capital raised.

Operationally, SoFi now serves 12.6 million members and continues positioning itself as a one-stop financial platform. The company has funded more than $73 billion in loans and helped members pay down over $34 billion in debt reinforcing both scale and engagement within its ecosystem.

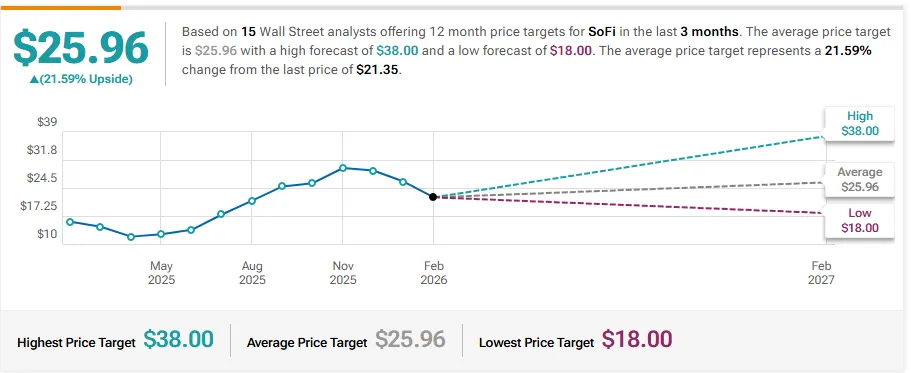

Truist Securities Maintains Hold on SoFi Technologies, Lowers Price Target to $21

Citizens Upgrades SoFi Technologies to Market Outperform, Announces $30 Price Target

JP Morgan Upgrades SoFi Technologies to Overweight, Announces $31 Price Target

Needham Maintains Buy on SoFi Technologies, Lowers Price Target to $33

Company: Richtech Robotics

Quote: $RR

Bull Case:

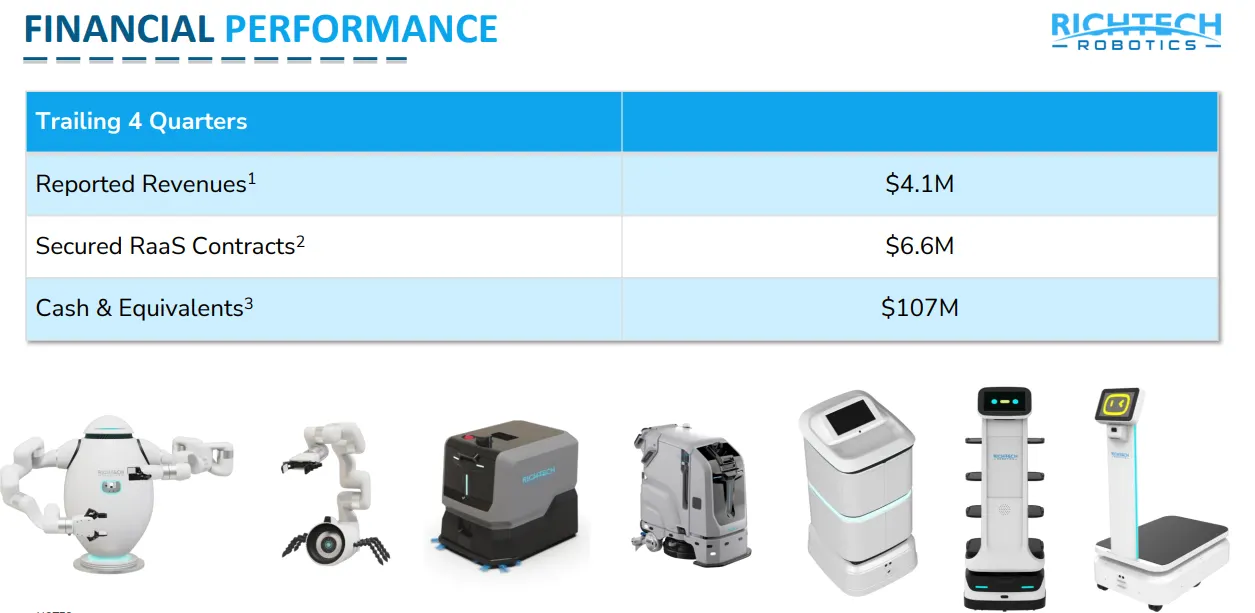

Richtech Robotics Inc. is projected to deliver significant top-line acceleration, with FY27 revenue estimated at $22 million roughly 80% growth from FY26 as robotic system adoption expands across hospitality, healthcare, and service industries. The company exited FY25 with revenue above $5 million, up 19% year over year, including sequential growth of more than 20% in Q4, signaling momentum.

Financially, Richtech strengthened its balance sheet following a $100 million capital raise, ending with approximately $275 million in cash and no debt. On paper, that provides runway and reduces near-term reliance on additional financing.

Bear Case:

Margins are already showing pressure. Gross margin came in at 65.2%, well below the 72.9% forecast, raising questions about cost structure and pricing power. The company reported an EBITDA loss of $5.5 million, with projections suggesting losses could widen to nearly $10 million. Profitability may not be visible until FY28, creating a long and uncertain path forward.

More concerning is promotional behavior. The stock’s largest spikes have followed partnershipstyle press releases rather than material earnings developments.

A recent example: shares surged over 40% after Richtech announced a “collaboration” with Microsoft via its AI Co-Innovation Labs only for the company to announce a $38 million dilutive raise the very next morning. The lab engagement itself appears to be a standard program available broadly to startups exploring Microsoft’s AI tools, rather than a transformative strategic deal.

From IPO through mid-2025, Richtech issued more than 40 press releases an unusually high volume relative to a sub-$20 million revenue base which raises red flags about promotional intensity versus operating scale.

Sharks Opinion:

Richtech is the kind of story that looks thrilling on the surface: cutting-edge robotics, partnerships with major tech players, and rapid growth in revenue. For a casual investor, it feels like a chance to get in early on the “next big thing” in automation. But when you start to dig into the company, the narrative starts to unravel. The repeated use of press releases as a tool to move the stock rather than communicate meaningful progress is concerning. Many of these “partnerships” are low-impact, standard industry programs that any small startup could join, yet they have been used to generate outsized market reactions.

The capital raise after the Microsoft Co-Innovation Lab announcement is a perfect example: the stock pumps on the partnership hype, and the next day the company dilutes investors. This pattern has repeated multiple times, signaling that management may be more focused on financing and market optics than on operational execution.

Operationally, the numbers tell a different story than the headlines. Margins are under pressure, EBITDA is negative, and profitability remains several years away, despite bold top-line targets. The high frequency of press releases relative to the small revenue base suggests that communication strategy is disproportionately aggressive compared to real operational achievements.

At the end of the day, Richtech may have real technology potential, but as an investment, the risk lies heavily on management behavior and promotion-driven volatility.

For anyone seeking a disciplined, fundamentalsdriven growth story, this is a cautionary tale. It’s the kind of setup where retail enthusiasm can keep the stock elevated short-term, but without execution, hype will fade, and losses for uninformed investors could be significant. We see it as a stock that, while technically innovative, functions more as a trading story than a reliable long-term investment.

Description: Richtech Robotics Inc is a robotics and artificial intelligence (AI) technology company focused on developing embodied AI systems that aims to improve the efficiency and productivity of businesses. The company trains proprietary artificial intelligence models on in-house data to operate robotic systems in the real world. It designs, engineers, manufactures, and deploys next generation embodied AI systems to serve a wide range of industries, including food service, retail, industrial manufacturing, automotive, healthcare, and hospitality. The company's offerings include Commercial Robotic Products, Industrial Robotic Products and Data Services.

Richtech Robotics positions itself as a cutting-edge U.S. AI-robotics innovator, but a closer look tells a very different story. Public filings, import records, and third-party product teardowns paint the picture of a company whose operations are largely routed through Shenzhen, China. The firm relies on a distribution and import chain, wrapped in patriotic branding and a compelling narrative, rather than on true in-house technological innovation.

The real engine behind Richtech isn’t product development or manufacturing it’s narrative monetization. The company leverages hype, press releases, and investor attention to fuel liquidity, which in turn sustains more attention.

Marketing claims of “U.S.-designed autonomous service robots built from the ground up” crumble under scrutiny. Public import data and product teardowns reveal that much of the hardware comes from standard Chinese factories, meaning the so-called design advantage is largely a story rather than reality. Functionally, Richtech acts as a marketing-driven reseller rather than a true proprietary manufacturer, repackaging and branding existing hardware to create the appearance of innovation.

Investors should be cautious: while Richtech’s stock moves can be dramatic, they are often fueled by narrative and hype rather than sustainable operational or technological progress. This is a company where market perception is being monetized more than the products themselves, making it a high-risk, attentiondriven play rather than a reliable long-term investment.

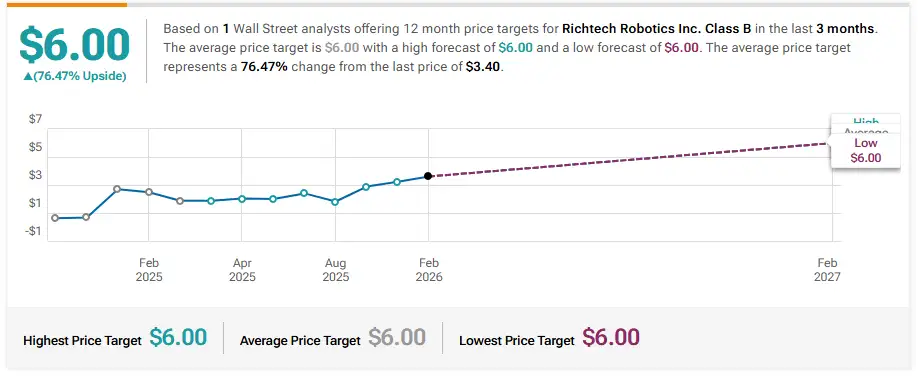

HC Wainwright & Co. Reiterates Buy on Richtech Robotics, Maintains $6 Price Target

Company: Rezolve AI PLC

Quote: $RZLV

Bull Case:

Rezolve AI PLC is positioned for rapid growth, with 2026 revenue projections raised from $165 million to $270 million, reflecting strong adoption of its AIdriven solutions. Annual recurring revenue (ARR) is expected to exit 2025 above $200 million and reach $500 million by the end of 2026. The combination of accelerating revenue, improving visibility, and the potential for operating profitability as early as 2027 supports a bullish outlook. The company’s AI platform and acquisitions could strengthen market position and expand customer reach if executed effectively.

Bear Case:

Rezolve AI has struggled to inspire investor confidence, with shares down 42.4% year-to-date versus a 12.5% gain in the Russell 2000 Index. The company is projecting an adjusted EBITDA loss of $25.3 million and expects revenue to decline by $46.4 million in 2025. Concerns exist around Rezolve’s reliance on acquired revenue versus organic growth, the long timeframe until profitability, and skepticism about the quality of its reported customer base. These factors create material downside risk.

Sharks Opinion:

Rezolve AI’s story is largely about perception versus reality. Prior to rebranding in 2023, the company was Rezolve Instant Saleware, a mobile commerce platform. Their SPAC guidance in 2021 projected $1.05 billion in revenue by 2024 a target they missed by 99.98%, generating under $190,000 instead, all from ticket sales for Spanish football teams. The AI narrative appears to have been layered on top of a history of underperformance.

Acquisitions, such as ViSenze in Singapore and GroupBy, are used to inflate ARR, yet both acquired companies had declining revenue and shrinking margins. Strategic partnerships, including the Microsoft deal, seem largely PRdriven, with the app listed in the Azure store receiving zero reviews and no tangible revenue generation. Insider enrichment is also a concern: the CEO’s Seychelles entity was paid $93.9 million in shares for acquisitions of companies valued at near zero.

Overall, Rezolve AI is selling a growth story that is heavily engineered through PR, acquisitions, and marketing. While headline ARR numbers appear impressive, the underlying fundamentals and balance sheet transparency are questionable, making it extremely difficult to model a credible path to profitability. Investors should approach cautiously.

Description: Rezolve AI PLC is an AI-powered solutions company, specializing in enhancing customer engagement, operational efficiency, and revenue growth for the retail and e-commerce sectors. The company's product, Brain Commerce, powered by its proprietary Large Language Model (LLM) brainpowa, transforms the online shopping experience. By surpassing traditional site search and product discovery tools, Brain Commerce improves conversion rates, increases average order value (AOV), and reduces cart abandonment.

HC Wainwright & Co. Reiterates Buy on Rezolve AI, Maintains $12 Price Target

Cantor Fitzgerald Assumes Rezolve AI at Overweight, Announces Price Target of $8

Northland Capital Markets Maintains Outperform on Rezolve AI, Raises Price Target to $7

Company: TOYO Co

Quote: $TOYO

Sharks Opinion:

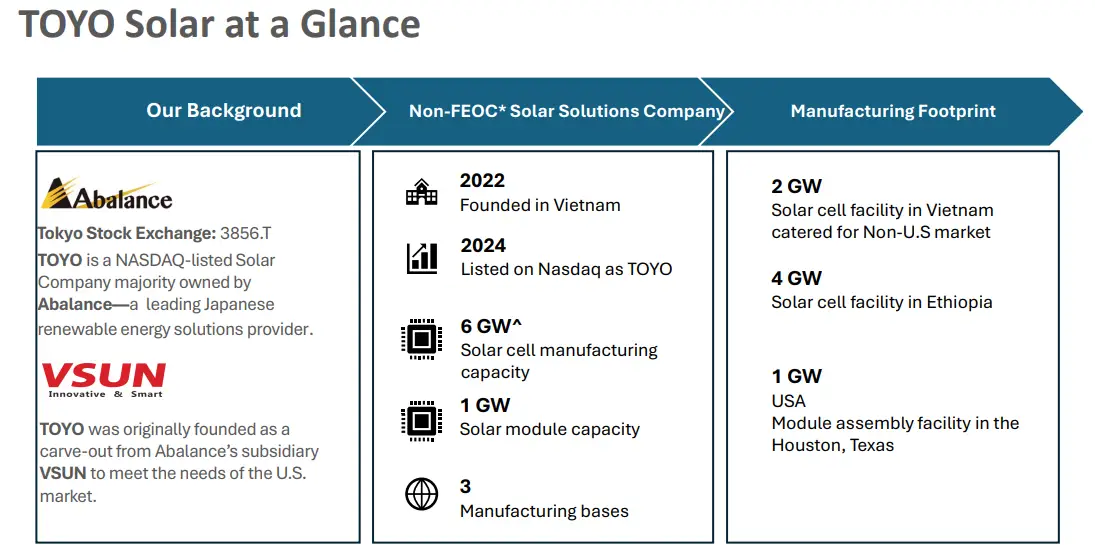

Toyo Co., Ltd. (not to be confused with Toyo Tire) operates across the solar power supply chain, including upstream wafer and silicon production, midstream solar cells, and downstream photovoltaic (PV) modules.

Founded in 2022, the company also manufactures solar PV modules, giving it a vertically integrated footprint in the sector.

We view Toyo as an interesting long-term play. The company maintains a disciplined balance sheet, which is uncommon in the solar space, and at current levels appears undervalued relative to its peers.

That said, the stock is up 164% and earnings are due in 11 days, which introduces near-term uncertainty. Ideally, we would like to see a pullback to create a better entry point, but there is potential for the name to revisit its SPAC listing price of $10 or even move higher. Trading volume is very light, so until liquidity improves, the stock may remain range-bound.

Despite these near-term considerations, Toyo has been added to our solar sector watchlist as a company worth monitoring for long-term exposure.

Description: Toyo Co Ltd along with its subsidiaries, is engaged in research and development, production, and sales of solar cells. Geographically, the company generates revenue from Asia and the USA, out of which the majority of revenue is generated from Asia.

Toyo Co. debuted on the Nasdaq through a SPAC merger with BWAQ in July 2024, initially trading at its $10 SPAC price before dropping to a low of $1.36 that same month a trend common among SPACs over the past two years.

Since then, the stock has rebounded to $5.41 as investors began analyzing the company’s financials and recognizing its valuation and growth potential.

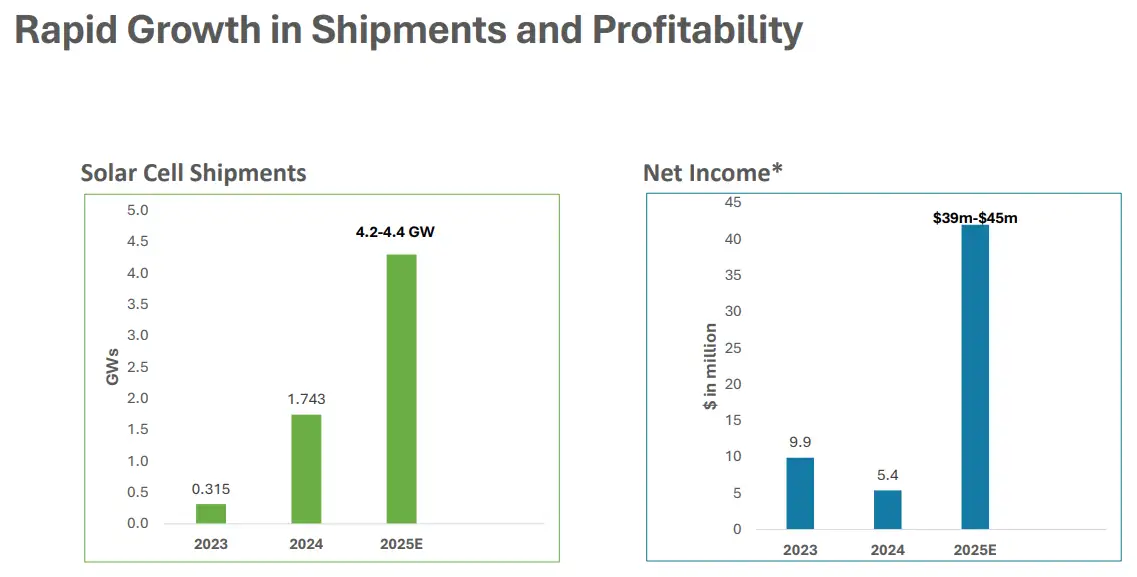

Last year, Toyo secured a $150 million contract to supply solar cells to a manufacturer with operations in India and Texas. This new client and contract is expected to generate additional revenue across 2025 and 2026. The announcement caused the stock to surge 81% on the news.

Looking at 2023 financials, Toyo generated $62.3 million in revenue with net income of $12 million, resulting in a 19% profit margin. The market cap sits around $240 million but may adjust lower following the recent 80% price move. The company’s P/E jumped to 29 from 17 prior to the stock surge. Using a 20% margin assumption, the new $150 million contract could contribute roughly $30 million in additional net income spread over 2025 and 2026.

For 2025, revenues in the first half reached approximately $139 million, up slightly from $138.1 million in the same period of 2024. This increase reflects contributions from the company’s new solar cell facility in Ethiopia, which began operations in April 2025 and serves U.S. customers, offering improved pricing and margin potential.

Costs of revenue for the first half of 2025 were about $116 million, up from $111.4 million in the prior-year period, causing gross margins to dip to 16.6% from 19.3% due to rising raw material costs. Operating expenses also climbed 220% to roughly $13 million from $4.2 million, reflecting the company’s ongoing investment in growth initiatives.

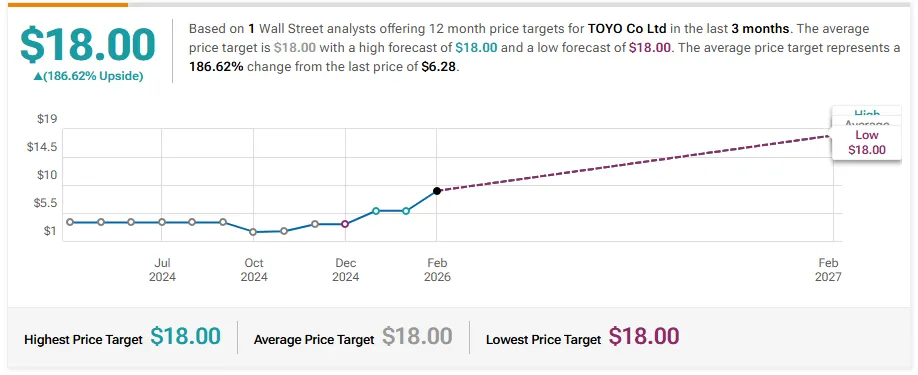

HC Wainwright & Co. Initiates Coverage On Toyo Co with Buy Rating, Announces Price Target of $18

Company: CHEMTRADE LOGSTCS

Quote: $CGIFF

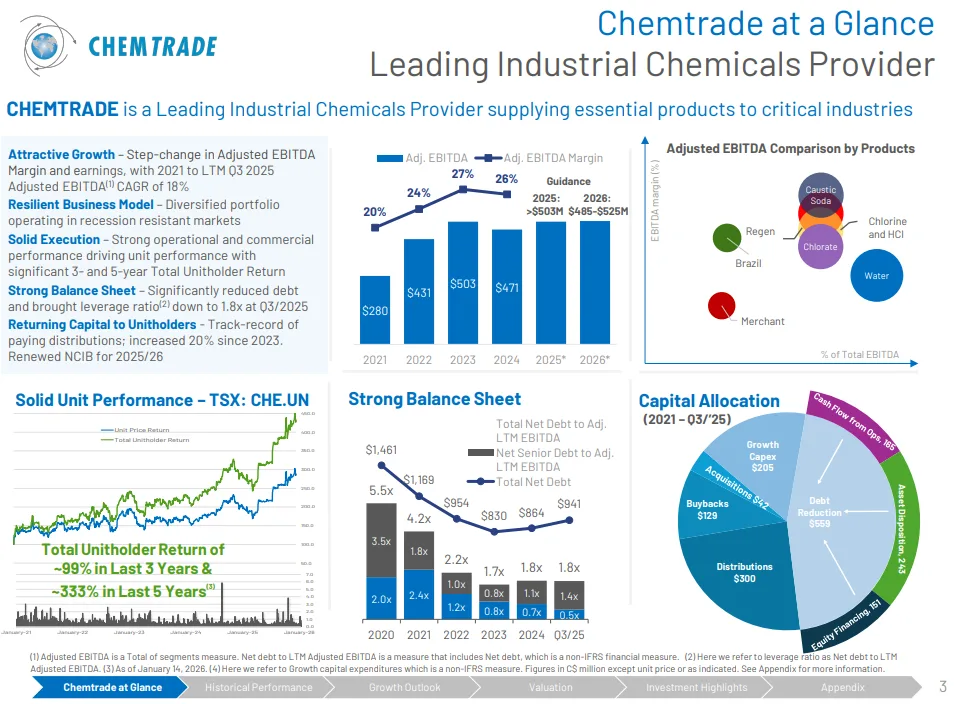

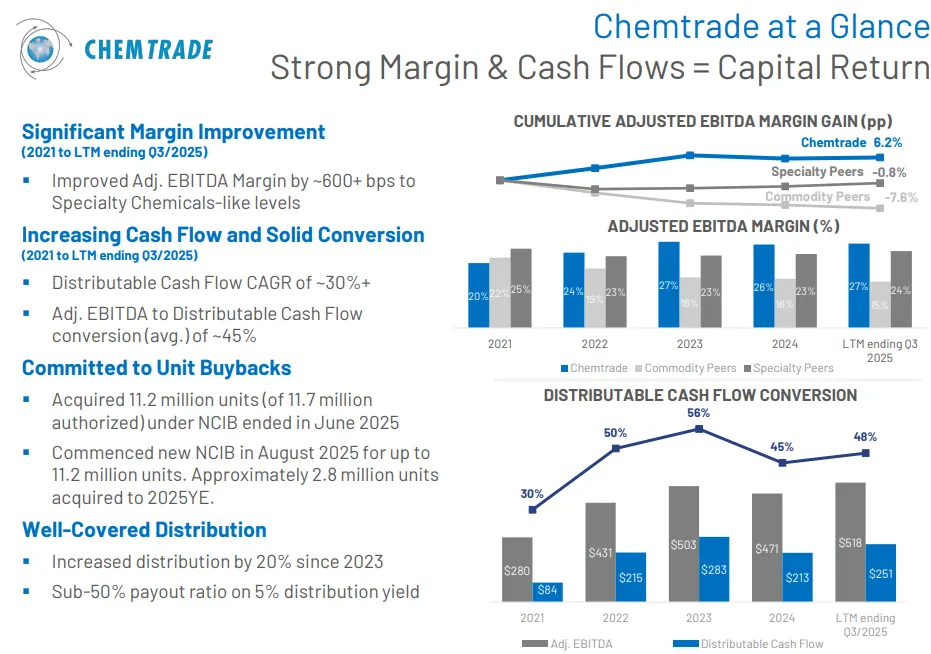

Sharks Opinion: In a volatile market, quieter names can often be overlooked but occasionally one quietly makes a big move. Chemtrade Logistics Income Fund (TSX:CHE.UN) is a perfect example, returning over 65% this past year.

This isn’t a high-growth tech stock, and it won’t appear on any AI top-10 lists, but it provides essential industrial chemicals for water treatment, agriculture, oil refining, and pulp and papercritical sectors that the economy relies on.

Its steady dividends and consistent earnings make it appealing in uncertain markets. For investors seeking a reliable, lower-volatility alternative, Chemtrade is worth a closer look: it may not double overnight, but with a strong yield, rising earnings, and a credible growth plan, sometimes boring is beautiful

Description: Chemtrade Logistics Income Fund provides industrial chemicals and services to customers in North America and around the world. The company is organized into two operating segments: Sulphur and Water Chemicals (SWC) and Electrochemicals. Its geographical segments are Canada, the United States which derives maximum revenue, and South America.

Chemtrade is organized into three main segments: Sulphur Products & Performance Chemicals, Water Solutions & Specialty Chemicals, and Electrochemical Products. Its products serve essential industries such as water treatment, agriculture, pulp & paper, oil refining, and food production.

All of Chemtrade’s North American production takes place in North Vancouver, where its lease—granted by the Vancouver Fraser Port Authority runs through 2032. The lease currently restricts Chemtrade from receiving, manufacturing, storing, or distributing liquid chlorine after June 30, 2030. The company has begun discussions with the Port to renew the lease and is engaging local officials to support its efforts.

A major competitive advantage for Chemtrade is its access to low-cost hydropower, which powers its electricity-intensive chlor-alkali process to produce chlorine and caustic soda. This makes Chemtrade one of the lowestcost producers globally, a benefit amplified by rising energy prices. Its Water Solutions segment also benefits from innovative, higher-value coagulants that smaller competitors cannot replicate, ensuring a stable revenue stream from municipalities.

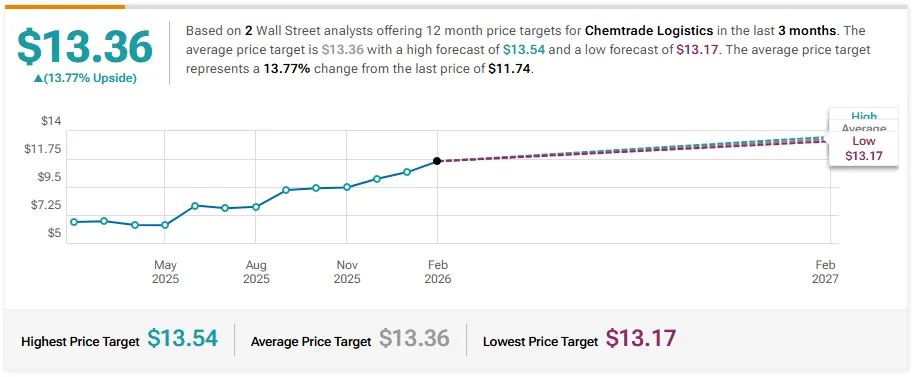

Chemtrade’s disciplined capital allocation featuring a robust 6.2% dividend yield supported by strong cash flow and an active share buyback program makes it attractive to investors. Based on earnings growth alone, the stock could reach $14 in the next two years, with potential upside to $20 if the market re-rates the company in line with industrial chemical peers. In our view, Chemtrade offers a compelling combination of a high dividend, a strong cash-flow engine, and clear pathways for both organic and inorganic growth.

RBC Capital Upgrades Chemtrade Logistics to Outperform, Announces $9 Price Target

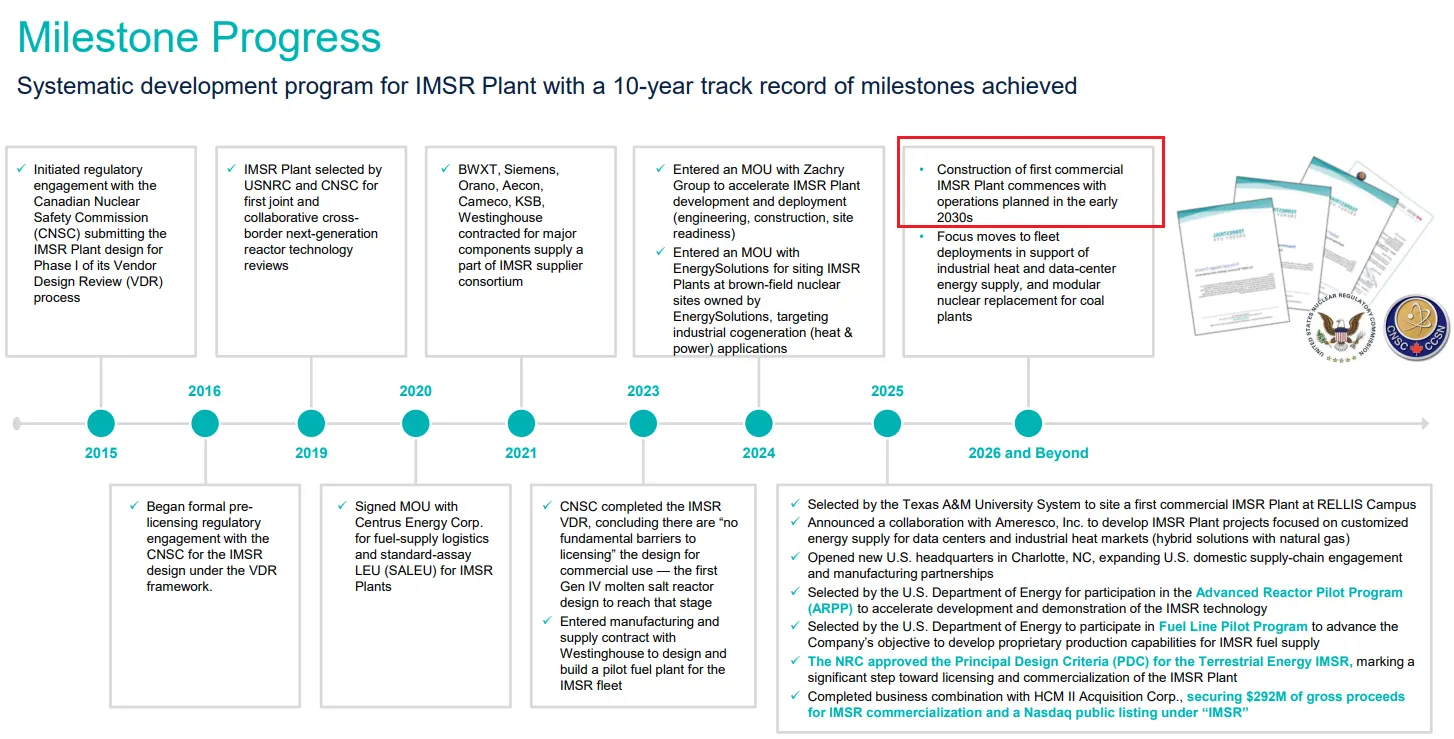

Company: Terrestrial Energy Inc

Quote: $IMSR

Sharks Opinion: I’m not the biggest fan of nuclear, and that view has already been discussed in the group chat. My main concern with IMSR is simple: the company won’t generate meaningful revenue until 2030, as nothing will be online until then. When a business is projecting that far into the future, dilution is almost inevitable. For us, IMSR is a stay-away not because it can’t be traded for a profit, but because trying to analyze or assign realistic targets to a product that doesn’t exist yet is like chasing numbers in the sky.

Description: Terrestrial Energy Inc is an industryleading technology company committed to delivering reliable, emission-free, and costcompetitive nuclear energy with a transformative advanced reactor, the Integral Molten Salt Reactor (IMSR). Its mission is to transform global energy markets by commercializing its IMSR Plant, which will deliver low-carbon electricity and industrial heat with superior economics, speed to deployment, and siting flexibility

The race to develop and deploy small modular reactors (SMRs) is global and highly competitive. Few technologies have captured as much attention as SMRs, and for good reason: if successfully scaled, they could meet soaring global power demand, stabilize electric grids, and unlock the full potential of nuclear energy.

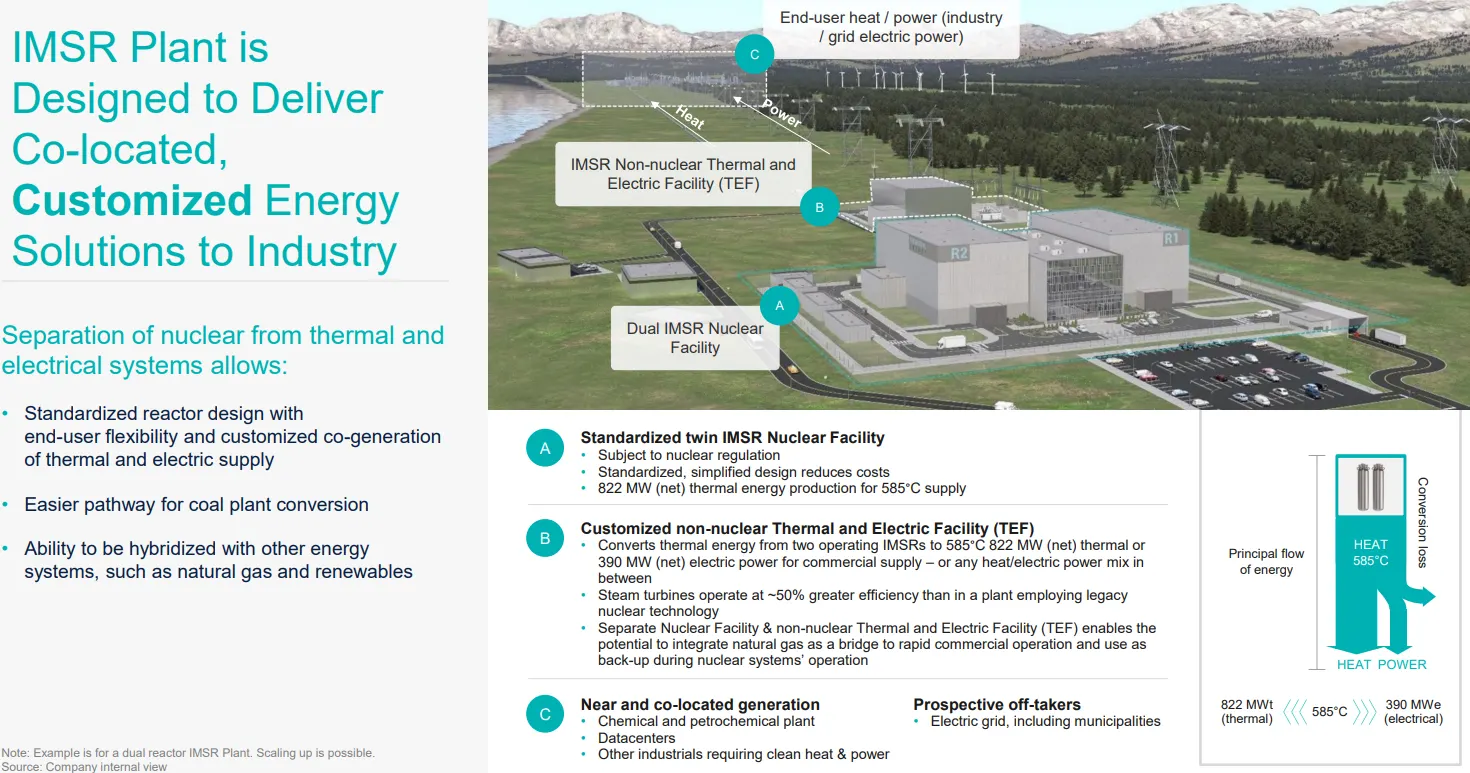

Terrestrial Energy, trading under the Nasdaq ticker IMSR following its merger with HCM II Acquisition Corp, raised over $292 million in gross proceeds to accelerate commercialization of its nuclear reactors. The company’s proprietary Integral Molten Salt Reactor (IMSR) technology features modular plants with two reactors per site, generating a combined 822 MWth of thermal output and 390 MWe of electric power.

The design prioritizes modular deployment, high thermal efficiency, and costeffective scalability.

IMSR plants aim to deliver clean, flexible, and affordable power to both electricity grids and industrial sectors, using Standard-Assay Low Enriched Uranium fuel with less than 5% U-235, ensuring regulatory compliance and compatibility with existing nuclear infrastructure. Key collaborations with Texas A&M University, Siemens, Westinghouse, and Ameresco support supply chain optimization and technical validation, while integration with DOE programs adds momentum toward licensing and commercial deployment.