This is a list of stocks that members asked us to do extra research on none of these are alerts/buy/sell recommendations.

Company: Zeta Global Holdings

Quote: $ZETA

Bull Case:

Zeta Global Holdings Corp has increased its 2026 total revenue growth outlook to 34%, up from the prior 21% estimate, signaling strong momentum and deeper customer spend. The company is seeing meaningful expansion from existing clients, highlighted by a 115% net revenue retention rate and an estimated $100 million incremental revenue opportunity from ZetaLive. In addition, improving adjusted EBITDA targets suggest operating leverage is beginning to materialize, pointing toward stronger profitability trends alongside revenue growth.

Bear Case:

Zeta faces notable headwinds. A significant portion of revenue is usage-based, which can introduce quarterly volatility and reduce visibility. The company operates in a highly competitive marketing technology landscape, putting pressure on margins and market share. Zeta is not yet profitable on a GAAP basis, and concerns remain around its ability to scale efficiently while free cash flow margins are projected to decline. Ongoing technological shifts and regulatory uncertainty add another layer of risk.

Sharks Opinion: Zeta appears promising if management can successfully transition from growth-at-all-costs to sustainable profitability. The revenue growth profile is strong, but the market is crowded with similar high-growth companies, and investors are increasingly rewarding those that demonstrate consistent earnings power. If Zeta can establish a clear path to profitability and generate compounding cash flow, a return to all-time highs is possible. For now, however, we view the stock as fairly valued and remain neutral until upcoming earnings confirm meaningful progress on margins and execution.

Description:

Zeta Global Holdings Corp is an omnichannel data-driven cloud platform that provides enterprises with consumer intelligence and marketing automation software. It serves enterprise customers across multiple industries, including financial services, insurance, telecommunications, automotive, travel and hospitality, and retail. Its Zeta Marketing Platform, or ZMP, is an omnichannel marketing platform with identity data at its core.

Founded in 2007 by David Steinberg and former Apple CEO John Sculley, Zeta Global was built with the mission of simplifying sophisticated marketing to accelerate brand growth.

At its core, Zeta is a marketing technology company that leverages a proprietary data cloud and artificial intelligence to deliver highly personalized marketing solutions.

Its platform helps brands acquire, grow, and retain customers across multiple channels, including email, mobile, web, video, and other digital touchpoints.

The company’s flagship offering, the Zeta Marketing Platform (ZMP), is an allin-one solution built around three core pillars: data management, marketing automation, and omnichannel engagement. This integrated approach allows marketers to unify customer data, automate campaigns, and execute across channels within a single ecosystem.

Zeta’s primary differentiation lies in its massive proprietary data asset. The company claims access to over 245 million individuals in the U.S. and more than 535 million globally, with over 2,500 real-time signals per individual.

This equates to more than one trillion consumer data signals processed per month. Marketers use this data to build detailed customer profiles, predict intent, and deploy highly targeted campaigns across paid and owned channels.

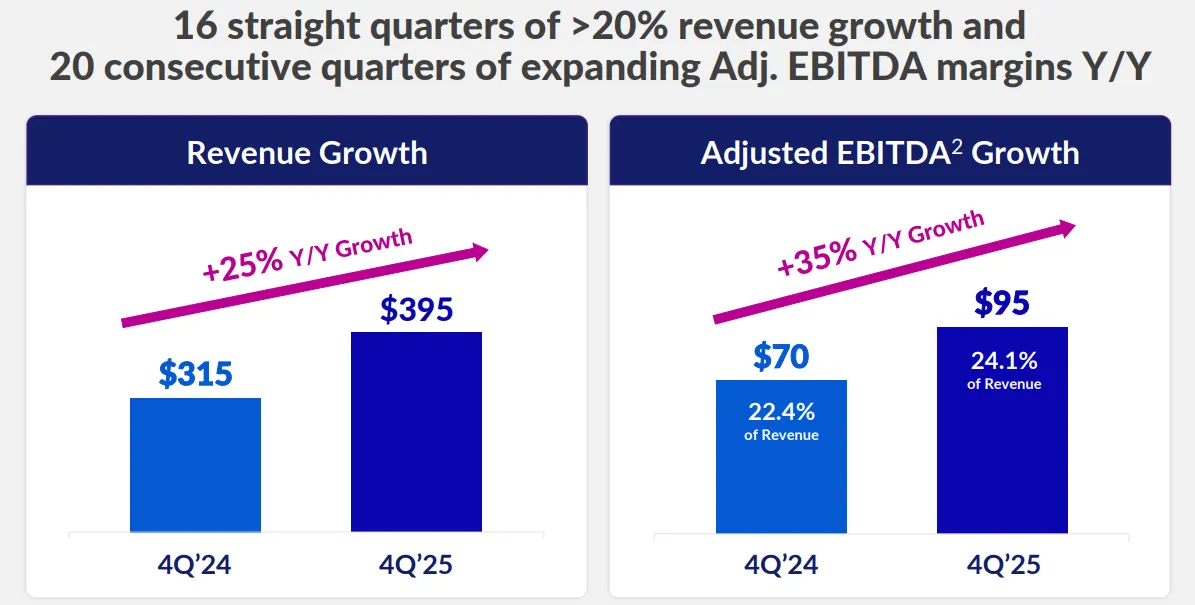

In Q1, Zeta reported revenue of $264 million, up 36% year over year, beating both management’s midpoint guidance and analyst expectations by roughly $10 million.

The contribution from LiveIntent the people-based email marketing platform acquired in October accounted for $19 million of that total.

It’s important to recognize that growth accelerated throughout 2024, largely driven by elevated political advertising during the presidential election cycle and the addition of LiveIntent in Q4.

Excluding both LiveIntent and political-related revenue, Q1 revenue would have grown 26% year over year still a healthy pace, but more reflective of the company’s organic trajectory.

A meaningful portion of Zeta’s revenue is volume-based rather than subscription-based, which introduces variability and reduces predictability quarter to quarter.

Revenue naturally fluctuates with seasonal marketing budgets, and the company typically sees a sequential decline from Q4 to Q1 as brands scale back spending after the holiday season.

Even accounting for political tailwinds and seasonal swings, the broader trend remains constructive. If customer growth continues and existing client spend expands, revenue should continue trending upward over the medium to long term.

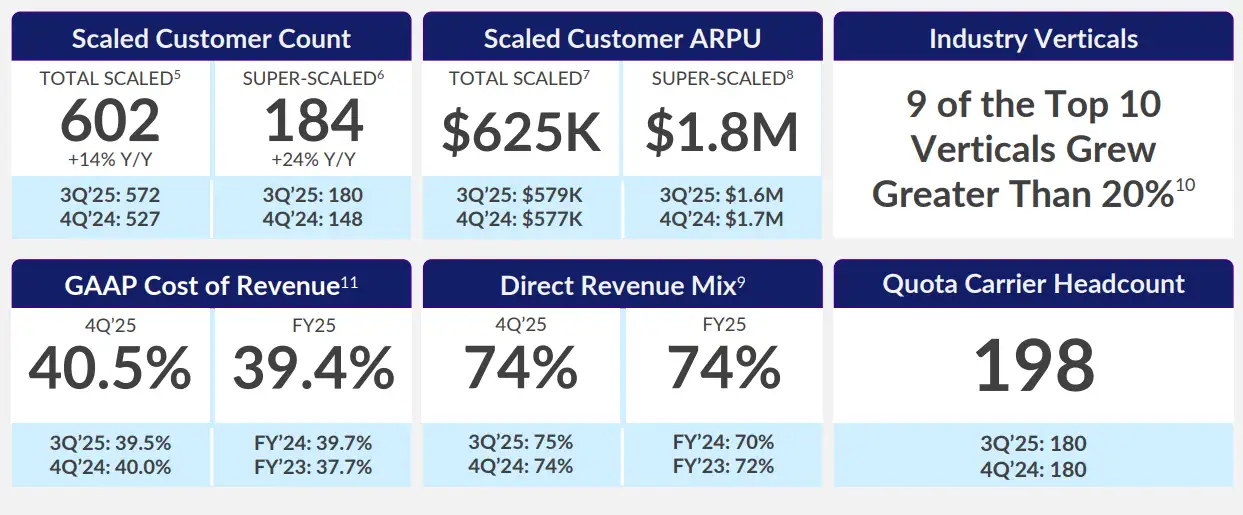

The spike in Scaled Customer growth during Q4 and Q1 was largely driven by the LiveIntent acquisition. For context, LiveIntent added 34 Scaled Customers in Q4 alone.

Excluding that contribution, Scaled Customer growth would have been approximately 9% in Q4, signaling a clear deceleration in organic expansion something that may concern investors focused on underlying growth trends.

While LiveIntent boosted customer count, it had the opposite effect on Average Revenue Per User (ARPU). Because LiveIntent’s customers are smaller on average compared to Zeta’s core ZMP clients, Scaled ARPU growth slowed meaningfully following the acquisition. This dynamic reflects a tradeoff: broader customer reach, but at a lower average spend per account.

Encouragingly, more than 50% of Zeta’s customer base has remained on the platform for over three years, demonstrating strong retention, loyalty, and platform stickiness. This suggests significant embedded monetization potential. In fact, one of the clearest growth opportunities lies not just in acquiring new customers, but in cross-selling, upselling, and deepening wallet share within the existing base.

Despite the current growth momentum, management expects a deceleration throughout 2025 due to difficult year-over-year comparisons following elevated political ad spending in 2024. Notably, while Q2 and full-year 2025 revenue guidance were raised modestly by $2 million each, Q3 and Q4 guidance were lowered. Historically, management has trended toward raising guidance across the board, but this time they opted for a more conservative stance amid macro uncertainty tied to tariff-related pressures.

Current revenue guidance implies:

• Q2 revenue of $297 million, up 30% year over year

• Q3 revenue of $323 million, up 21% year over year

• Q4 revenue of $358 million, up 14% year over year

• Full-year 2025 revenue of $1.242 billion, up 23% year over year

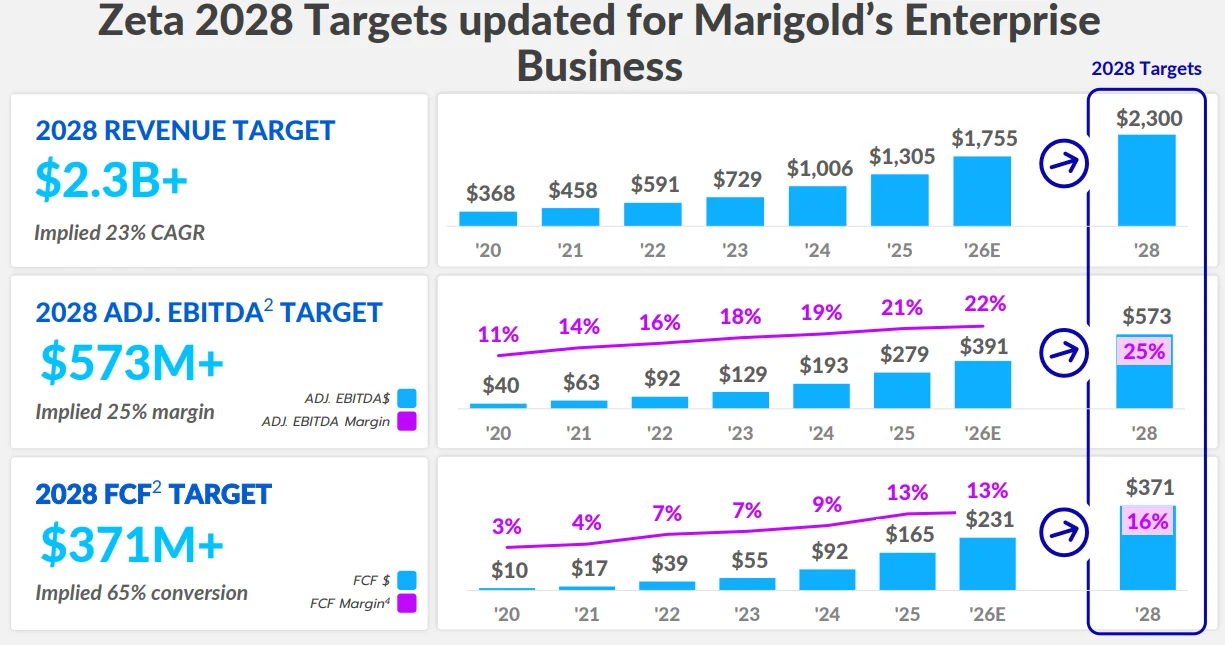

Looking further out, management is targeting at least $2.1 billion in revenue by 2028 more than double 2024 levels — implying an organic revenue CAGR of 20%+ over the next four years.

To achieve this, management aims to expand market share within its existing customer base by just 100 basis points. Scaled Customers collectively spent over $100 billion on marketing and advertising last year, while Zeta generated roughly $1 billion in revenue, representing only about 1% penetration. Simply increasing that share to 2% by 2028 primarily through deeper usage and expanded adoption would materially accelerate revenue growth without requiring dramatic customer acquisition expansion.

DA Davidson Maintains Buy on Zeta Global Holdings, Raises Price Target to $30

Goldman Sachs Maintains Neutral on Zeta Global Holdings, Raises Price Target to $26

Morgan Stanley Maintains Equal-Weight on Zeta Global Holdings, Raises Price Target to $27

Company: Parsons Corporation

Quote: PSN

Bull Case:

Parsons Corp is positioned for meaningful growth, supported by expected margin expansion of 100– 150 basis points over the next three years. Improved hiring trends and strong demand for Critical Infrastructure bookings provide additional tailwinds. The Federal Solutions segment remains well aligned with key U.S. defense and intelligence priorities, creating opportunities for incremental contract wins, including large-scale awards such as the $800 million Joint Cyber Threat Hunt Kit program. Internationally, urban development activity in the Middle East is projected to grow at a mid-teens rate this year, supporting a solid outlook for Parsons’ regional revenue streams.

Bear Case: Financial expectations have moderated, reflected in a reduction of the FY26E target EBITDA multiple from 17.6x to 15.8x. The Federal Solutions segment is exposed to potential federal budget cuts and evolving government procurement practices, both of which could pressure future awards and backlog visibility. Additionally, ongoing challenges in hiring and retaining skilled labor, geopolitical tensions in the Middle East, and broader macroeconomic uncertainty create operational and execution risks that could weigh on performance.

Sharks Opinion:

Parsons is an interesting name because it operates as a behind-the-scenes architect across critical industries from cybersecurity innovation to water treatment and infrastructure modernization serving both government and private sector clients.

The competitive landscape, however, is intense. In Federal Solutions, Parsons competes with established players such as Booz Allen Hamilton, Leidos, CACI, SAIC, Lockheed Martin, and Northrop Grumman firms with deep resources and longstanding government relationships. To differentiate itself, Parsons has strategically pivoted toward higher-margin, technology-driven solutions, accelerating revenue growth to 29%, supported by a three-year CAGR of 37% in Federal Solutions and a shift away from lowermargin legacy infrastructure work.

That said, being diversified across many verticals rather than dominating a single niche makes it difficult to justify a premium valuation multiple, especially with revenue growth moderating since the last report. While strong earnings execution could push the stock back toward the $78 level, we are not viewing this as a breakout or “moonshot” name within the sector based on current fundamentals.

Description: Parsons Corp is a provider of technology-driven solutions in the defense, intelligence, and critical infrastructure markets. The business activities of the group are carried out through Federal Solutions and Critical Infrastructure segments. The Federal Solutions segment is a high-end service and technology provider to the U.S. government, delivering timely, cost-effective solutions for mission-critical projects, whereas the Critical Infrastructure segment provides integrated design and engineering services for complex physical and digital infrastructure around the globe.

Under the leadership of Carey Smith, who became Chair, President, and CEO in 2021, Parsons began its transformation from a traditional industrial engineering contractor into a more technology-focused solutions provider.

Historically rooted in industrial project management and physical infrastructure, Parsons has long relied on securing government contracts a space defined by intense competition and tight margins.

Recognizing the growing role of technology in modern defense and infrastructure, the company strategically pivoted toward higher-margin, tech-enabled solutions to better differentiate itself and capture specialized market share.

Several acquisitions have accelerated this evolution. The 2022 acquisition of Xator Corporation expanded Parsons’ capabilities in cybersecurity, intelligence, and biometrics.

In 2024, the purchase of BlackSignal Technologies added expertise in digital signal processing and electronic warfare, further strengthening its position in defense technology.

Today, Parsons operates through two primary segments. Federal Solutions delivers cybersecurity, missile defense, and advanced engineering services to U.S. government agencies, particularly the Department of Defense. Within this segment, Defense & Intelligence focuses on command, control, and surveillance systems, while Engineered Systems provides infrastructure and environmental monitoring solutions.

The Critical Infrastructure segment addresses complex civil and urban development needs. Mobility Solutions manages large-scale projects such as roads, bridges, and water systems, while Connected Communities integrates smart city technologies to modernize urban infrastructure through digital innovation.

Q4 2025 Financial Highlights

Parsons reported Q4 revenue of $1.6 billion, representing an 8% year-overyear decline and a 10% decrease on an organic basis. Excluding the impact of a confidential contract, total revenue would have increased 11%, or 8% organically.

Net income reached $56 million, up 3% year over year and marking a fourthquarter record. Adjusted EBITDA came in at a record $153 million, up 5%, with an adjusted EBITDA margin of 9.6%.

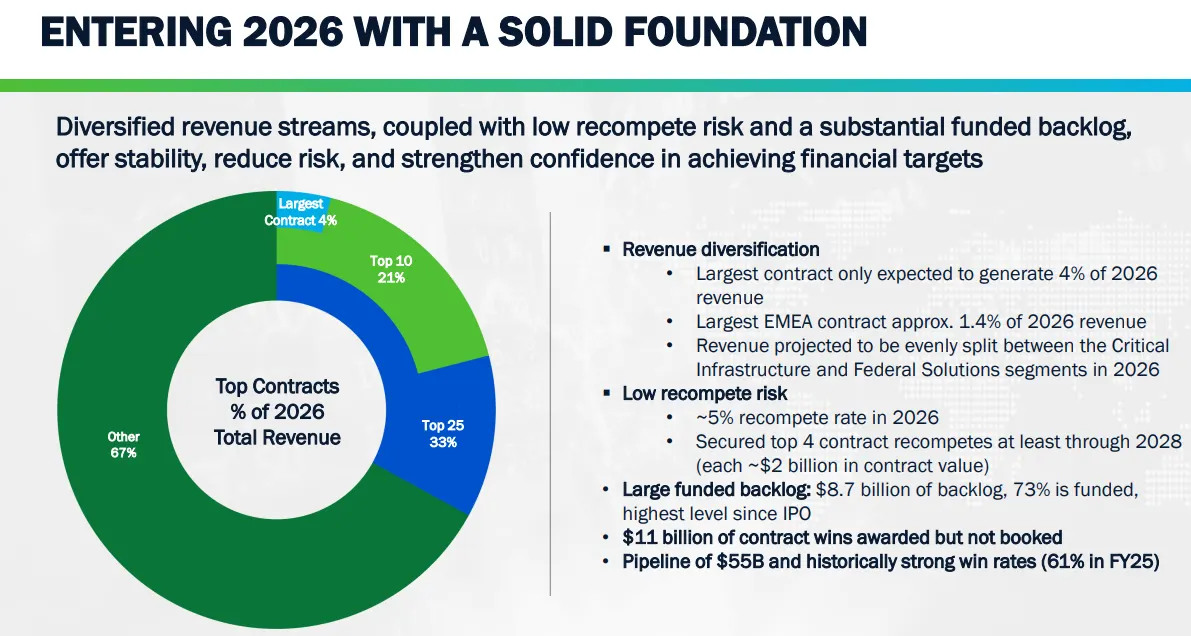

Cash flow from operations increased 32% to $168 million, demonstrating solid cash generation despite top-line pressure. The book-to-bill ratio was 0.9x for the quarter, while the company maintained its streak of trailing twelve-month book-to-bill of 1.0x or greater in every quarter since its IPO.

Fiscal Year 2025 Highlights

For the full year, revenue totaled $6.4 billion, down 6% year over year and 9% on an organic basis. Excluding the confidential contract, total revenue would have grown 12%, or 8% organically.

Net income reached a record $241 million, up 3% year over year. Adjusted EBITDA totaled $609 million, increasing 1%, with a full-year adjusted EBITDA margin of 9.6% both record levels for the company.

Cash flow from operations declined 9% to $478 million, though the company achieved 100% free cash flow conversion. Parsons also secured 15 contracts valued at $100 million or more, matching last year’s record performance.

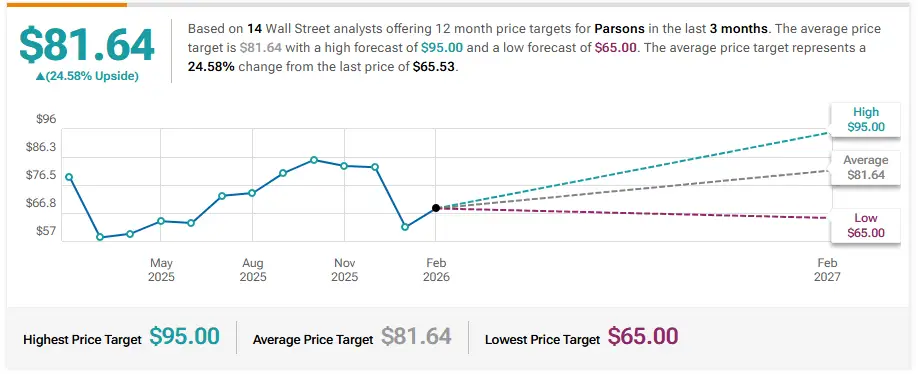

UBS Maintains Buy on Parsons, Lowers Price Target to $95

Keybanc Maintains Overweight on Parsons, Lowers Price Target to $73

Truist Securities Reiterates Buy on Parsons, Lowers Price Target to $85

Company: Archer Aviation

Quote: $ACHR

Bull Case:

Archer Aviation is well positioned within the emerging sustainable air mobility sector. Its proprietary electric powertrain technology is now being utilized by partners such as Anduril for the Omen VTOL drone project, signaling a strategic move toward diversified revenue streams beyond passenger aircraft.

The company maintains a strong balance sheet with roughly $2 billion in liquidity, reducing nearterm financial risk and strengthening its competitive positioning in the growing eVTOL market.

Additionally, Archer’s planned ramp-up in flight testing and operational milestones ahead of highvisibility events like the 2028 Olympics could improve credibility, attract partnerships, and reinforce long-term growth expectations.

Bear Case:

Archer faces material execution risks. Regulatory hurdles and certification delays continue to weigh on its flight test program, pushing out timelines for commercialization and near-term production.

The company has also experienced aircraft order cancellations, adding uncertainty to its demand pipeline relative to competitors.

Inflationary pressures and supply chain constraints particularly around critical components such as batteries are increasing costs and creating additional strain on financial performance.

Sharks Opinion:

Archer is an easy company to get excited about given the technology and the long-term vision of urban air mobility.

However, the reality today is far less compelling.

The company has faced repeated delays, generates no revenue, and at its current cash burn rate is only a few quarters away from needing additional capital which likely means further dilution for shareholders.

While that doesn’t guarantee an immediate financing event, the probability is high in prerevenue aerospace ventures of this scale.

Until Archer can clearly demonstrate a credible path to generating revenue not even profitability, just sustainable top-line traction we believe the stock faces continued downside risk.

The vision is compelling, but execution and funding remain the defining variables.

Description: Archer Aviation Inc advances the benefits of sustainable air mobility. The company is engaged in designing and developing a fully electric vertical takeoff and landing eVTOL aircraft for use in UAM networks. It is creating an electric airline that moves people throughout cities in a quick, safe, sustainable, and cost-effective manner.

Archer remains firmly in the pre-revenue development stage, continuing to invest aggressively in certification, manufacturing scale-up, and technology development ahead of Midnight’s commercialization.

As of Q3 2025, the company reported no meaningful operating revenue, as aircraft deliveries have not yet begun. Net losses remain substantial, though Q3 showed some improvement sequentially.

Archer reported a net loss of $130 million in Q3 2025, narrower than the $206 million loss in the prior quarter, largely due to a non-cash gain tied to warrant liabilities. However, the loss was wider than the $115 million reported in Q3 2024, reflecting increased R&D and manufacturing investment.

Operating expenses reached $174.8 million in Q3, up 43% year over year, driven by expanded engineering headcount, intensified flight testing, and facility build-outs. Approximately $53 million of quarterly expenses were noncash stock-based compensation, highlighting continued investment in talent.

Cash burn remains elevated, with roughly $126 million used in operating cash flow and capital expenditures during the quarter, relatively flat sequentially. Year-to-date 2025 operating cash outflows have exceeded $300 million, underscoring the capital-intensive nature of scaling an aerospace platform.

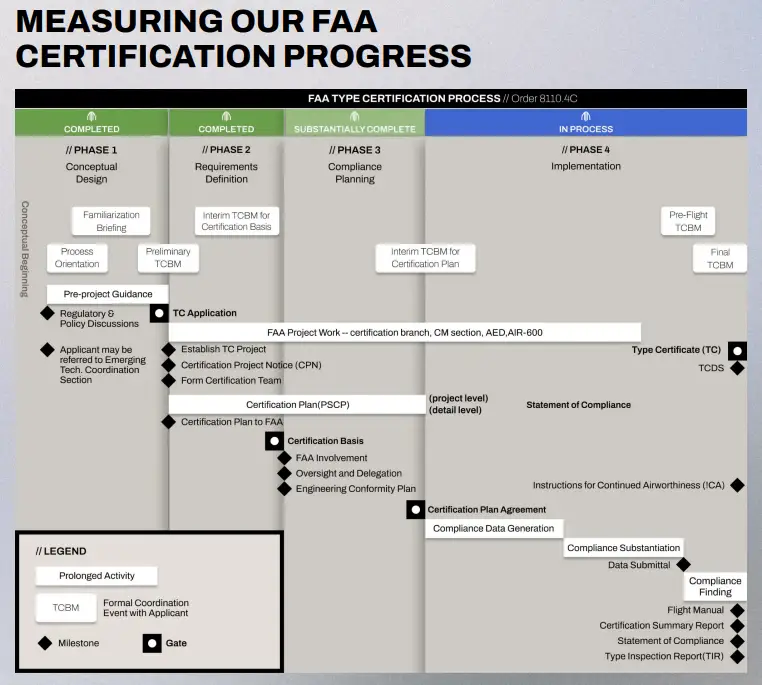

FAA type certification for the Midnight eVTOL remains the critical milestone for commercial launch. Throughout 2025, Archer made meaningful progress via an expanded flight test program using multiple Midnight prototypes.

Recent milestones include flights exceeding 55 miles, durations over 30 minutes, and speeds above 150 mph at 10,000 feet metrics that validate performance capabilities and strengthen the certification case.

The company is nearing completion of conventional takeoff and landing test points, while prior campaigns have already demonstrated vertical takeoff, hover, and transition maneuvers. This testing not only advances safety validation but also builds the extensive data required for regulatory approval.

From a regulatory standpoint, Archer is now in the final stages of FAA certification preparation. After securing its Part 135 Air Carrier Certificate in 2023 allowing it to operate commercial air taxi services under FAA rules the company continues to work closely with regulators toward full aircraft type certification.

While temporary government disruptions posed risks to timelines, certification progress remains the single most important catalyst for unlocking revenue generation.

Needham Reiterates Buy on Archer Aviation, Maintains $10 Price Target

Goldman Sachs Initiates Coverage On Archer Aviation with Neutral Rating, Announces Price Target of $11

Canaccord Genuity Maintains Buy on Archer Aviation, Raises Price Target to $13

JP Morgan Maintains Neutral on Archer Aviation, Lowers Price Target to $8

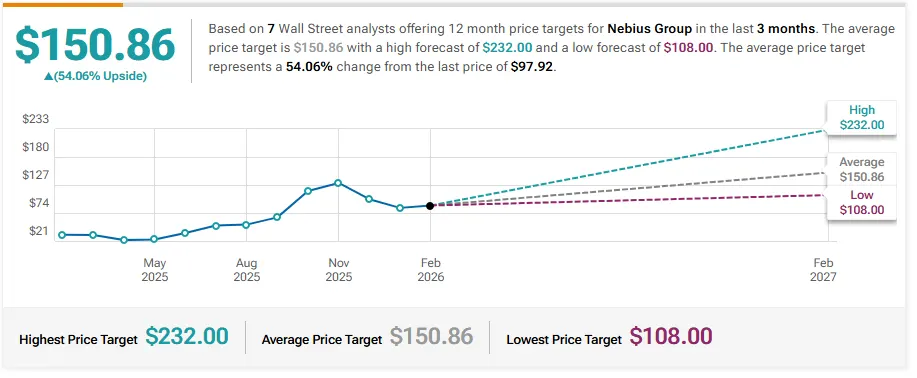

Company: Nebius Group N.V.

Quote: $NBIS

Bull Case:

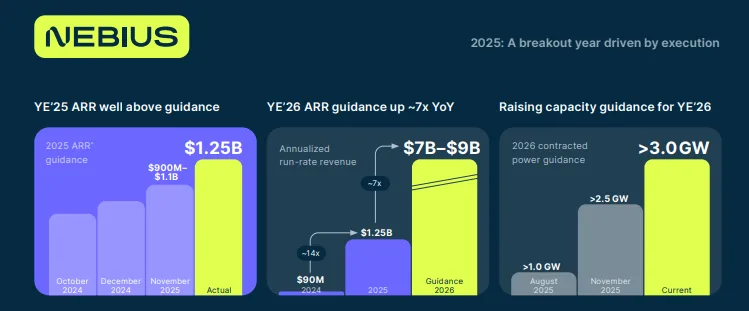

Nebius Group delivered total revenue of $146.1 million, representing a striking 237% year-overyear increase, driven by strong performance in its core AI cloud infrastructure business.

A newly announced multiyear agreement with Microsoft, reportedly valued at $17 billion, significantly strengthens backlog visibility and positions the company for sustained growth.

Management projects an annualized revenue runrate of $7–9 billion by the end of calendar year 2026, supported by improving operational efficiencies that could drive double-digit returns on capital a notable differentiator versus many capital-intensive AI infrastructure peers.

Bear Case:

Despite strong growth, Nebius lowered its 2025 revenue guidance to approximately $525 million, citing an inability to fully meet demand a sign that scaling capacity efficiently remains a challenge. While the company reports a backlog exceeding $20 billion,

converting that into sustained enterprise relationships is critical, particularly given competitive pressure from established hyperscalers. Additionally, Nebius’ historical ties to Yandex and its origins in Russia may continue to attract geopolitical and regulatory scrutiny, potentially complicating partnerships and customer acquisition efforts.

Sharks Opinion:

When first analyzing the company, the story felt familiar and for good reason. Nebius is essentially the rebranded and restructured international arm of Yandex, now relocated to Amsterdam and operating as a standalone AI-focused cloud infrastructure provider trading on NASDAQ under NBIS. The company specializes in highperformance GPU clusters designed specifically for AI model training and inference, positioning itself squarely within the AI infrastructure arms race.

The stock has already surged roughly 184% year to date, and chasing momentum at these levels carries risk. That said, if management executes on its aggressive 2026 projections, the upside case becomes compelling.

For long-term believers in the AI infrastructure buildout, pullbacks may offer more disciplined entry points through dollar-cost averaging. If the projected growth trajectory materializes, a move back toward the $150 level is not unrealistic but execution will need to match the ambition.

Description: Nebius is a vertically integrated cloud provider focusing on AI and highperformance computing. It is a carve-out of the previous Russian tech firm Yandex, following the Russian sanctions since the Ukraine-Russia war. Nebius designs and operates its own data centers and servers across Europe and the US, with a total capacity of several hundred megawatts. In September 2025, Microsoft became a major Nebius client under a multiyear $17 billion revenue agreement to provide computing capacity.

For full-year 2025, Nebius generated approximately $520 million in revenue, reflecting roughly 140% year-over-year growth, driven by ramped capacity and large enterprise AI workload contracts.

Headquartered in Amsterdam, the company competes primarily with hyperscale and AI-native infrastructure providers, including Amazon Web Services, Microsoft Azure, and CoreWeave, though Nebius is more narrowly focused on dedicated AI compute rather than broad enterprise cloud services.

Demand remained extremely strong, with the company completely sold out every quarter in 2025, including Q4, and management confirmed that Q1 2026 is already sold out.

The revenue timing impact is straightforward: the bulk of new capacity came online in late November, meaning it only contributed to December’s revenue, while quarterly revenue is averaged across all three months. Annualized recurring revenue (ARR) projections are based on this exit rate.

Management reaffirmed its 2026 year-end ARR guidance of $7–9 billion, signaling strong confidence in the target either a bold reflection of operational execution or an aggressive projection.

The company ended 2025 with $3.7 billion in cash and $1.57 billion in deferred revenue from customer prepayments, effectively having Microsoft and Meta cofinance the AI infrastructure buildout via interest-free advance payments.

This arrangement not only provides favorable financing but also represents a significant vote of confidence from two of the most sophisticated technology firms globally.

BWS Financial Maintains Buy on Nebius Group, Maintains $130 Price Target

Morgan Stanley Initiates Coverage On Nebius Group with Equal-Weight Rating, Announces Price Target of $126

Citizens Initiates Coverage On Nebius Group with Market Outperform Rating, Announces Price Target of $175

Company: Micron Technology

Quote: $MU

Bull Case: Micron Technology’s outlook is bolstered by strong sequential growth in average selling prices (ASPs) for DRAM and NAND chips, exceeding initial expectations. Bit shipments rose in the mid-to-high single-digit percentages, reflecting healthy demand, particularly from AI applications that are increasing memory content in flagship smartphones.

The company’s elevated capital expenditure plan of $20 billion signals confidence in long-term growth, especially in the high-bandwidth memory (HBM) market, which is projected to reach a $100 billion total addressable market by 2028.

Bear Case: Micron faces risks from potential oversupply and softness in DRAM and NAND demand, which could pressure revenue and margins.

The memory industry’s cyclical nature exposes the company to macroeconomic headwinds, global slowdowns, and volatile pricing. Bit demand growth may decelerate, and competitive pressures could drive further ASP declines. Limited PC exposure also makes Micron more reliant on mobile and AI-driven segments, increasing sensitivity to market fluctuations.

Sharks Opinion: Micron is a household name in semiconductors and one of the largest memory chip manufacturers globally. The stock has already surged roughly 349%, raising the question of whether fundamentals can support further gains. Micron has benefited enormously from prior memory shortages and remains highly profitable with strong cash generation.

That said, the memory sector is extremely cyclical second only to chemicals in volatility meaning slowdowns inevitably occur, which can quickly impact the stock. At a current P/E of 39, the stock’s valuation already reflects much of the growth story.

While Micron can certainly continue higher, any slowdown could trigger a pullback. For investors looking to add exposure at these levels, a dollarcost averaging approach is prudent. The company’s strength and profitability support a long-term case, but the cyclical risks make disciplined entry and risk management essential.

Description: Micron is one of the largest semiconductor companies in the world, specializing in memory and storage chips. Its primary revenue stream comes from dynamic random access memory, or DRAM, and it also has minority exposure to not-and or NAND, flash chips. Micron serves a global customer base, selling chips into data centers, mobile phones, consumer electronics, and industrial and automotive applications. The firm is vertically integrated.

Micron delivered another exceptional quarter, with results that rival some of the most impressive beats we’ve seen in the semiconductor space, second only to Nvidia historically. Sequential and year-over-year revenue and EPS growth were outstanding, with the sequential Non-GAAP gross margin jumping from 45.7% to 56.8%, signaling an unprecedented spike in memory demand.

The majority of this growth was driven by higher average selling prices (ASPs), which also expanded margins. But the story isn’t over: Q2 guidance projects $18.7B in revenue, a 37% sequential increase, and a gross margin of 68%, up over 11 percentage points pointing to continued demand strength.

For CY2025, management now expects server unit growth in the high teens, above the prior forecast of 10%, and PC unit growth in the high single digits, exceeding previous mid-single-digit expectations. While encouraging, a key consideration is whether some of this demand reflects customers front-running DRAM price increases, which could soften Q1 CY2026.

Micron’s guidance assumes sustained server and PC demand alongside ongoing memory supply constraints, particularly in PCs, supporting higher unit sales. If these dynamics persist, the company is positioned to continue benefiting from elevated memory pricing and tight supply conditions.

Needham Maintains Buy on Micron Technology, Raises Price Target to $450

Morgan Stanley Maintains Overweight on Micron Technology, Raises Price Target to $450

Mizuho Maintains Outperform on Micron Technology, Raises Price Target to $480

TD Cowen Maintains Buy on Micron Technology, Raises Price Target to $450