Pony AI (PONY) reported a strong Q4 2025, delivering results that exceeded analyst expectations. The company posted adjusted earnings per share of $0.12 alongside revenue of $29.1 million, reflecting continued progress in its autonomous driving and robotaxi initiatives.

A key highlight from the quarter was the announcement of a strategic agreement to launch what it describes as the first commercial robotaxi service in Europe, with initial operations set to begin in Zagreb. This marks an important step in expanding its global footprint.

Shares initially rose 2.81% in pre-market trading following the earnings beat and strong growth in robotaxi-related revenue, as well as the newly announced partnership with Uber Technologies.

However, those gains were later given back after the full release.

This overview focuses strictly on the key developments from the current quarter.

Pony AI moved well following our initial re-entry, but the stock has since pulled back and begun to flatten out alongside broader global market volatility.

With the recent escalation surrounding the Iran conflict and the potential ripple effects on global growth particularly for export-driven economies like China we are actively assessing whether trimming exposure is the more prudent move.

This is not a straightforward decision. On one side, the long-term thesis remains intact. Pony AI continues to position itself as a leader in autonomous mobility and robotaxi infrastructure, steadily scaling its platform within a rapidly evolving transportation market.

On the other side, geopolitical risk and macro uncertainty tend to weigh disproportionately on China-linked technology names, often regardless of underlying fundamentals.

For now, we are taking a tape-first approach. If momentum continues to deteriorate, trimming exposure becomes more likely. If the stock stabilizes and buyers return, maintaining the position still makes sense given the long-term growth narrative.

At this stage, the trade is balanced and could move in either direction, so we are closely monitoring price action before making a final call.

Our longer-term outlook remains a $28 target for PONY, but near-term direction will ultimately be dictated by macro conditions and market sentiment.

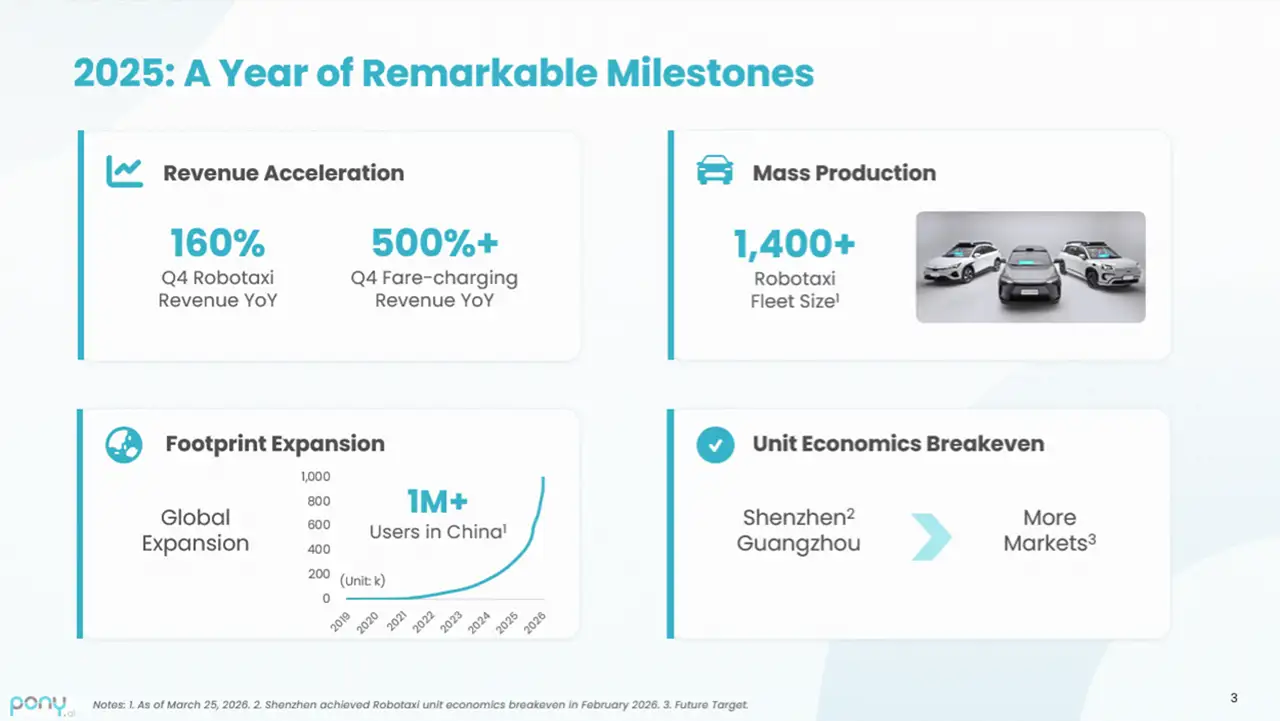

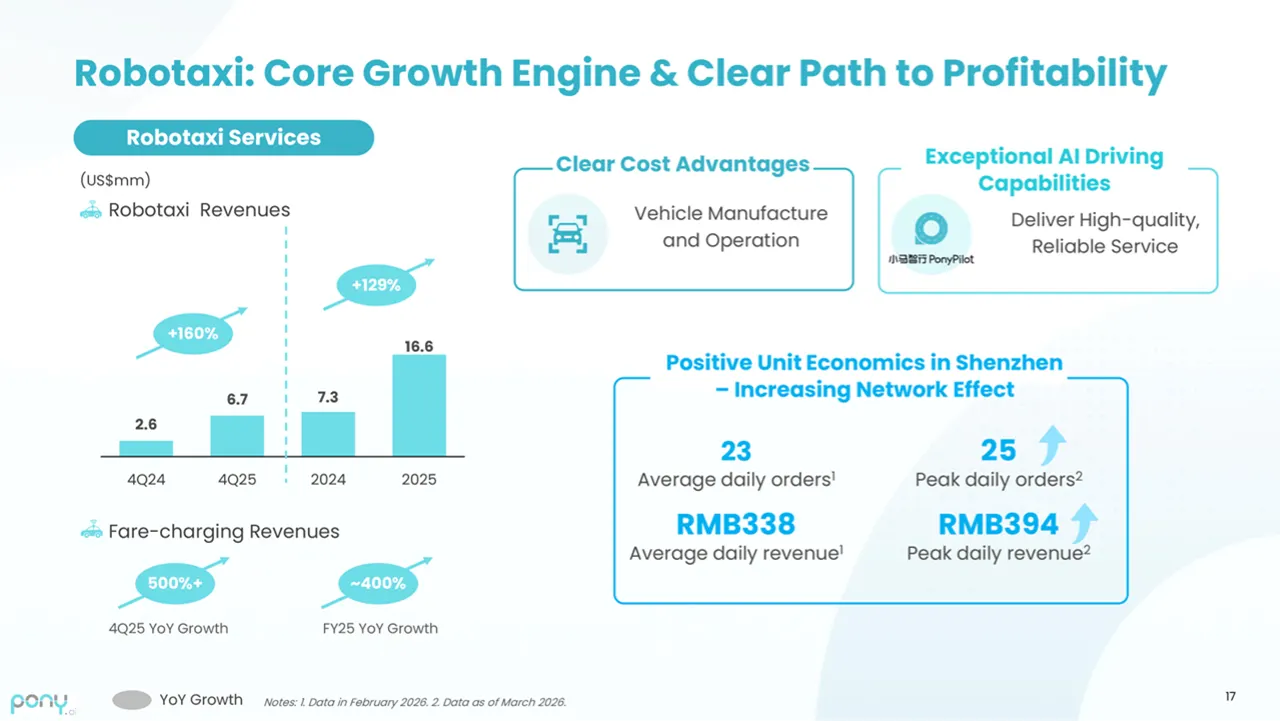

Robotaxi remains the standout growth driver for Pony AI, with revenue from the segment surging 160% year-over-year to $6.7 million in the quarter.

Even more notably, fare-based revenue increased by over 500% compared to the same period last year, highlighting accelerating real-world adoption of its autonomous ride-hailing services.

Despite this strength, total revenue declined 18% to $29.1 million from $35.5 million in the prior-year quarter.

The primary driver of this drop was the licensing and applications segment, where revenue fell 53% to $9.4 million due to timing-related project recognition.

Meanwhile, robotruck services showed modest growth, with revenue edging up 1.2% to $13.1 million, reflecting steady but less explosive momentum compared to the robotaxi segment.

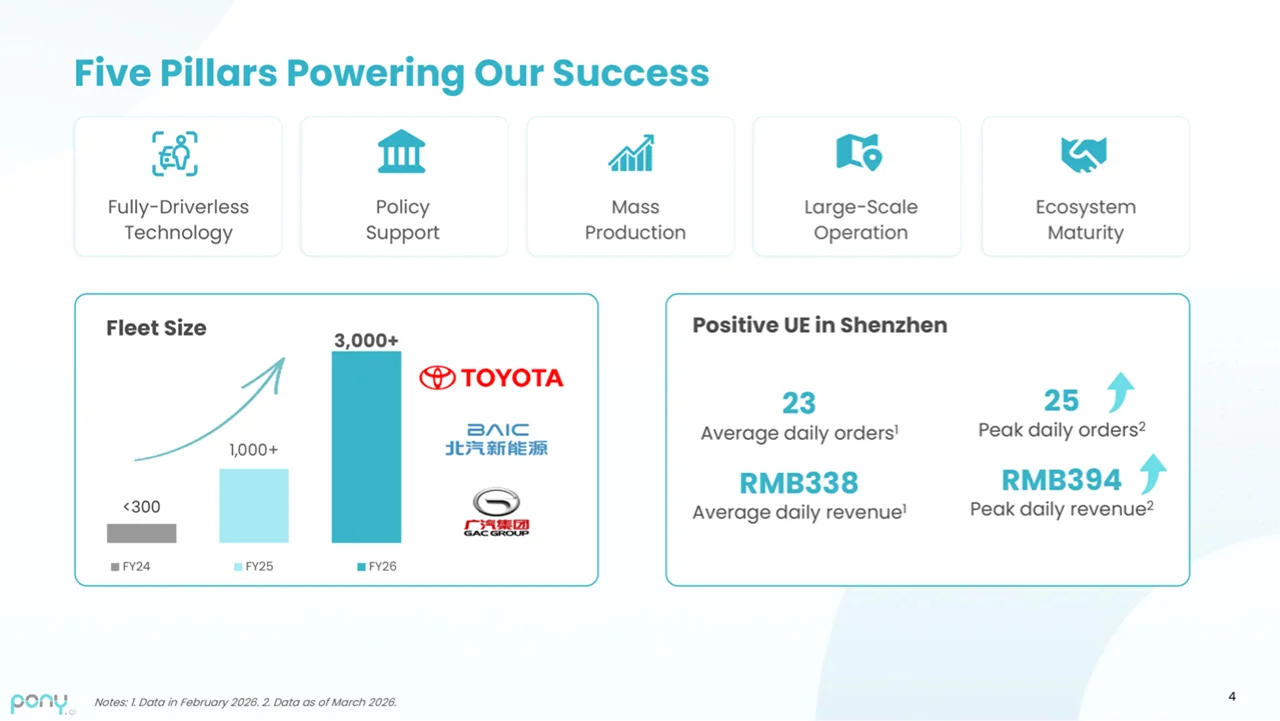

Pony AI continues to show strong operational progress, achieving consecutive unit economics breakeven in both Guangzhou and Shenzhen within just four months of launching its Gen-7 robotaxi.

On March 22, 2026, daily net revenue per Gen-7 vehicle hit a record RMB 394, supported by an average of 25 orders per vehicle in Shenzhen—an important signal of improving utilization and demand.

The company’s fleet has now scaled past 1,400 vehicles as of March 25, 2026, with plans to more than double that number to over 3,000 units by the end of the year.

Expansion is also accelerating geographically, with new operations in Croatia, Hangzhou, and Changsha, while management targets a presence in more than 20 cities globally by year-end 2026. Pony AI significantly strengthened its balance sheet, with cash and cash equivalents, short-term investments, restricted cash, and long-term wealth management instruments totaling $1.51 billion as of December 31, 2025 up sharply from $587.7 million at the end of the previous quarter. (Money raised from the Hong Kong IPO)

Fourth-quarter robotaxi revenue surged 160% year-over-year to $6.7 million, with fare-based revenue jumping more than 500%. Despite this strength, total revenue declined 18% year-over-year to $29.1 million, mainly due to timingrelated recognition in the licensing and applications segment, which fell 53% to $9.4 million.

Robotruck services remained steady, growing 1.2% to $13.1 million.

On profitability, Pony AI reported net income of $75.5 million in Q4, a significant turnaround from a net loss of $181.1 million in the same period last year.

This marked the company’s first profitable quarter, largely driven by gains in the fair value of trading securities rather than core operations.

For the full year 2025, revenue increased 20% to $90.0 million, supported by strong growth in both robotaxi and licensing segments.

Net loss narrowed substantially by 72% to $76.8 million, showing improving operating leverage.

Beyond robotaxis, other segments also contributed meaningfully. Robotruck revenue reached $40.6 million for the year, supported by deeper collaboration with Sinotrans to scale fleet operations.

Meanwhile, licensing and applications revenue grew 19.7%, driven by rising demand for Pony AI’s autonomous domain controller across use cases including low-speed delivery, robotic sweepers, logistics, and humanoid robotics.

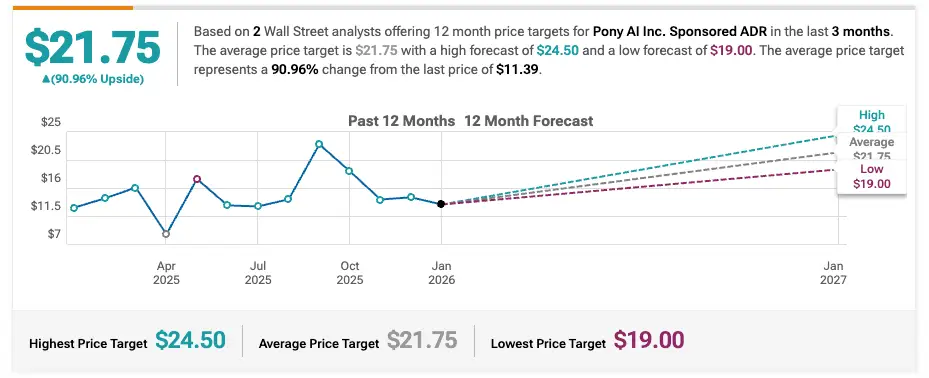

Citigroup Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $29

UBS Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

Deutsche Bank Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

B of A Securities Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $18