A Message from Sheraz Ali

Market participants may differ on the exact timing and magnitude of the next leg higher, but there is broad consensus on one point: the long-term outlook for semiconductors remains structurally bullish.

Estimates place the global semiconductor market at roughly $630–$680 billion in 2024, with projections reaching $1.0–$1.1 trillion by 2030, driven primarily by the proliferation of AI, data centers, and advanced computing workloads.

The industry is in the midst of a profound transformation.

AI is no longer a marginal growth driver it is reshaping demand across logic, memory, advanced packaging, and equipment.

At the same time, geopolitics and national security considerations are redefining supply chains, with governments accelerating investments in domestic manufacturing capacity to reduce reliance on foreign production.

This combination of secular demand growth and structural realignment is creating both opportunity and dispersion. Not all semiconductor companies will benefit equally.

Winners in the next cycle will be those positioned at critical choke points of the value chain, with exposure to high-performance computing, AI-driven workloads, and regions benefiting from policy-backed capital investment.

As semiconductors become increasingly central to global innovation and economic security, the need for a forward-looking, selective approach has never been greater.

Through this report, we aim to cut through the noise and provide a clear framework for understanding where the next cycle is likely to emerge, which segments stand to benefit most, and how investors and industry participants can position accordingly in this rapidly evolving landscape.

Semiconductors often referred to as microchips or simply chips are the foundational components of modern electronics.

A microchip consists of a network of electronic circuits etched onto a thin wafer of semiconductor material, most commonly silicon.

At the heart of each chip are transistors, which function as microscopic electrical switches that control the flow of current by turning it on or off.

The power of a semiconductor is largely determined by transistor density.

The more transistors integrated onto a single chip, the greater its processing capability and efficiency.

Today’s manufacturing advances allow a microchip roughly the size of a human fingernail to house billions of transistors, enabling levels of computational performance that were unimaginable just decades ago.

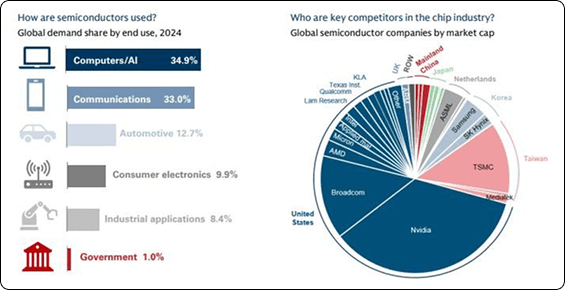

These chips serve as the fundamental building blocks of the digital economy. Semiconductors are embedded across a vast range of end markets, powering everything from computers and smartphones to automobiles, industrial machinery, and medical devices.

As technology becomes more complex and interconnected, semiconductors are no longer just components they are strategic inputs that underpin innovation, productivity, and economic growth across nearly every sector.

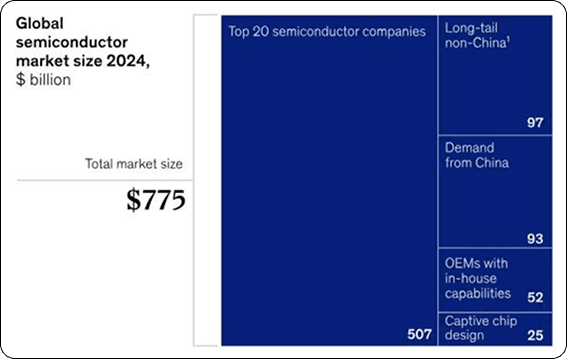

Historically, analysts have measured the size of the semiconductor market by tracking chip sales to electronics manufacturers from fabless designers, foundries, and integrated device manufacturers (IDMs) that both design and fabricate chips.

Where direct data was unavailable particularly for private or non-listed companies market size was estimated using modeled assumptions.

For many years, this sales-based framework was an effective proxy for overall industry value. It accurately reflected the economics of a market dominated by IDMs, fully integrated players, and large fabless firms.

Today, however, the structure of the industry has shifted. A growing share of innovation and value creation now comes from captive chip designers, OEMs with in-house silicon programs, and specialized fabless operators.

As a result, traditional sales-based metrics increasingly understate the true economic value of semiconductors embedded across end products and platforms.

Semiconductors are now indispensable to the global economy, underpinning everything from cloud infrastructure and artificial intelligence to autonomous vehicles, smartphones, and emerging technologies. Demand continues to evolve rapidly as performance requirements rise and new use cases proliferate.

With demand frequently outpacing supply, a deeper understanding of these dynamics is critical to identifying where the most compelling opportunities will emerge.

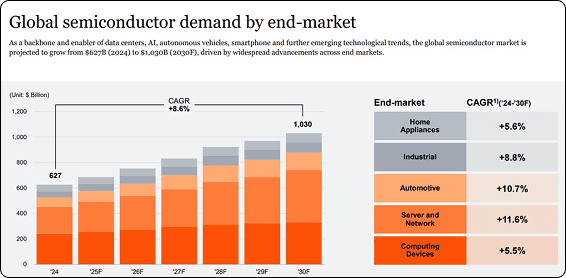

Looking ahead, the global semiconductor market is projected to expand from approximately $627 billion in 2024 to over $1.0 trillion by 2030, driven by broad-based adoption across end markets and accelerating technological complexity. Leading-edge chips particularly those designed for AI workloads are expected to account for roughly 62% of total industry growth.

This expansion is fueled by surging compute requirements, increased silicon content per device, and continued migration to smaller, more advanced process nodes.

Given the capital intensity and technical barriers at the frontier, a winner-take most dynamic is likely to persist, with a small number of companies capturing a disproportionate share of industry profits in the leading-edge segment.

Much of the semiconductor industry’s growth over the past several decades has been concentrated among a handful of leading companies in each segment, highlighting the importance of strategic execution at the top of the market.

Analysis shows that these top performers consistently enhanced their economic profit by executing five key strategic moves.

Three of these relate to portfolio management:

M&A: Acquiring or merging with complementary businesses in a structured, repeatable manner to build scale and expand capabilities.

Dynamic Resource Reallocation: Shifting capital, talent, and R&D investment toward the highest-return projects and away from underperforming areas.

Out-Investing Competitors: Consistently allocating more resources to innovation, advanced processes, and cutting-edge technologies than rivals.

The remaining two moves are operational levers aimed at performance and market positioning:

Improving Productivity: Streamlining operations, automating processes, and enhancing efficiency to maximize output per unit of input.

Differentiation for Higher Margins: Delivering products and technologies that stand out in the market, allowing the company to capture premium pricing and defend profitability.

Collectively, these five strategic pillars enabled leading semiconductor firms to not only drive growth but also maintain resilience and profitability in an intensely competitive and capital-intensive industry

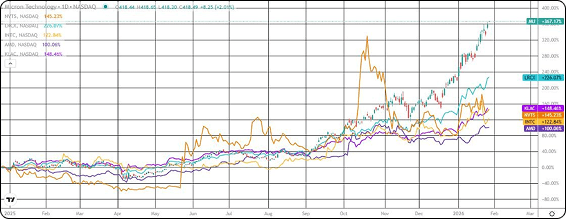

The following semiconductor stocks delivered the strongest 12-month performance as of January 21–23, 2026:

Micron Technology (MU): +264%

Navitas Semiconductor (NVTS): +235%

Lam Research (LRCX): +177%

Intel (INTC): 148%

Advanced Micro Devices (AMD): +105%

KLA Corporation (KLAC):+94%

These gains reflect a combination of strong demand for memory, advanced process technology, and AI-driven chip adoption

Nvidia (NVDA) +59%: Continues to serve as the dominant “anchor” for AI training and inference. Analysts see substantial upside in 2026 driven by strong demand and backlog for its Blackwell and Rubin GPU architectures.

Taiwan Semiconductor (TSM) +75%: Functions as the “center of gravity” for semiconductor manufacturing, holding a near-monopoly on 3nm production and preparing for 2nm nodes.

Broadcom (AVGO) +64%: A leader in networking semiconductors and AI focused custom chip design, benefiting from structural demand in data centers and communications infrastructure.

Top-performing semiconductor ETFs

First Trust Nasdaq Semiconductor ETF (FTXL): +59.88%

VanEck Semiconductor ETF (SMH): +57.53%

Strive U.S. Semiconductor ETF (SHOC): +55.74%

iShares Semiconductor ETF (SOXX): +48.74%

Market Takeaways:

The semiconductor sector is both larger and more dynamic than traditional sales-based estimates suggest.

Growth is concentrated in leading-edge chips and high-bandwidth memory (HBM), which are capturing the majority of new value. Other segments will largely compete on cost and scale.

Companies that can innovate rapidly or achieve meaningful operational efficiencies will be best positioned to dominate in this evolving landscape.

The leading segments in 2030 will be the 5 that now dominate the market, but their growth trajectories and demand drivers will differ:

Leading Semiconductor Segments in 2030

1. Home Appliances: While the market is mature, AI and IoT are making appliances smarter, creating new consumer experiences. Emerging devices AR/VR systems and wearables depend heavily on semiconductors, driving innovation in the “smart home” space.

2. Industrial: Semiconductors are transforming industrial sectors, enabling faster diagnostics, efficient surgeries, and preventive healthcare through advanced CPUs, GPUs, biosensors, and MEMS. Renewable energy adoption fuels demand for SiC power semiconductors, while smart production expands needs for sensors, connectivity ICs, and AI chips.

3. Automotive: EV growth will drive demand for high-voltage power semiconductors like silicon carbide (SiC). Autonomous driving advancements level 2 adoption widespread, level 3 increasing also rely on advanced chips for sensor fusion, AI, and safety systems.

4. Server & Network: The surge of generative AI has exponentially increased data processing needs. By 2030, CPUs, GPUs, AI accelerators, and HBM memory will be critical to supporting massive computational demand.

5. Computing Devices: PCs and smartphones remain central to the semiconductor market. AI applications, high-resolution displays, powerful compute, and storage demands will continue to drive growth in high-performance devices.

While all five segments are critical, growth will be uneven, with AI, EV, industrial automation, and advanced memory driving most of the new semiconductor value.

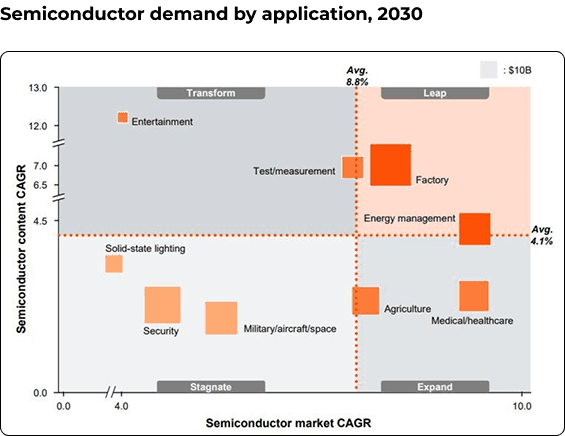

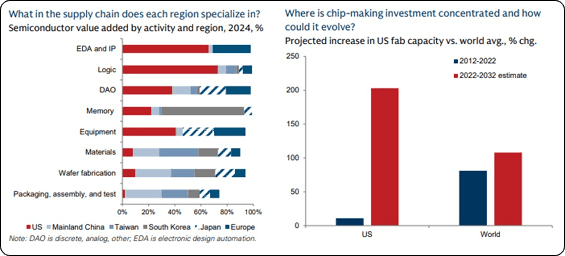

The semiconductor sector remains central to the global race for technological leadership, with major regions investing heavily to strengthen their domestic ecosystems. Design capabilities are increasingly critical, especially in high-end markets such as AI, data centers, and autonomous vehicles, where differentiation drives product value

Key Growth Drivers:

Smart Factories & Automation: Expansion of smart factories is boosting demand for production machinery, control systems, and microcontroller units (MCUs). Integration of robotics into manufacturing processes increases the need for semiconductors in testing, measurement, and automation.

Renewable Energy: The growth of solar, wind, and other renewable sectors is driving demand for high-voltage power semiconductors.

Healthcare & AI Applications: AI integration in medical devices and healthcare systems is increasing semiconductor content per unit, supporting sector growth

Fragmented or Mature Areas:

Military & Security: Customized semiconductors are required, resulting in fragmented, specialized demand.

Solid-State Lighting: LED penetration has saturated the market, leading to slower growth relative to emerging sectors

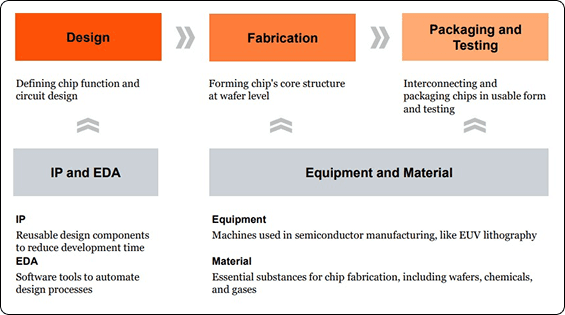

The semiconductor industry is rarely a linear supply chain it’s a highly interconnected ecosystem where a single chip can traverse the globe multiple times before reaching a final product.

Calling it a “supply chain” oversimplifies the reality

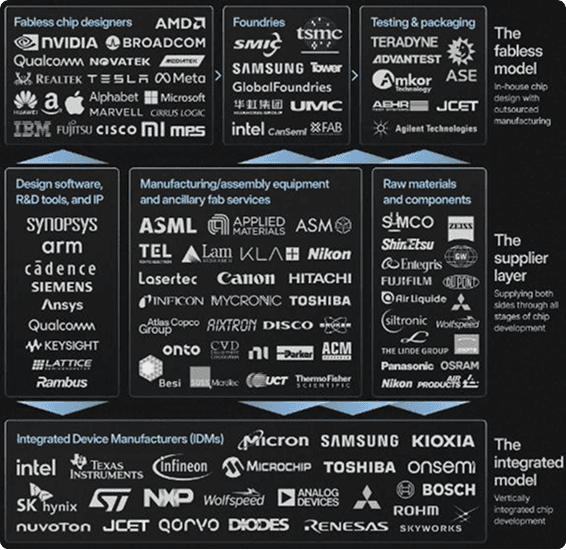

Key Segments in the Semiconductor Industry

Fabless Semiconductor Companies

Fabless companies focus on designing and developing semiconductor chips but do not operate their own manufacturing facilities. Instead, they outsource production to specialized foundries, allowing them to concentrate on innovation and design.

Foundry Companies

Foundries are the “factories” of the semiconductor world. They manufacture chips based on designs provided by fabless companies, turning conceptual blueprints into physical semiconductor devices.

Outsourced Semiconductor Assembly and Test (OSAT) Companies

OSAT firms provide third-party packaging and testing services. After chips are manufactured, they must be packaged for integration into devices and tested for functionality, ensuring reliability and performance.

Electronic Design Automation (EDA) Companies

EDA companies offer software tools and methodologies for designing electronic systems, from integrated circuits to printed circuit boards. Their tools allow engineers to visualize, simulate, and validate circuit performance before manufacturing.

Semiconductor Equipment Manufacturers

These companies design and produce the specialized machinery required for semiconductor fabrication and testing. Their tools are critical for creating transistors, capacitors, and integrated circuits at scale

Semiconductor Stocks Within The Supply Chain With Upside

Here are our favorite names in the semiconductor supply chain with meaningful upside. You’ll notice a few of the major players are missing as is typical with us, we focus on undervalued gems that most investors aren’t paying attention to.

Company: ACM Research, Inc

Quote: $ACMR

To see how Sheraz and JR are trading ACM Research, become a Stock Sharks member today.

Sharks Opinon:

ACM Research remains a core idea for us in the semiconductor space.

The company specializes in semiconductor production equipment, with a focus on single wafer wet cleaning tools that boost wafer yields.

Since our entry, ACMR is up 57.3%, yet we still see meaningful upside.

The U.S.-listed parent trades at $3.3B, while ACMR owns 74.6% of its China subsidiary, valued at roughly $14.65B a valuation gap that continues to highlight upside potential.

The stock recently cleared $50, and while volatility is expected if the AI trade cools, ACMR still looks undervalued relative to its China listing.

Why we like it:

Swing trade: Capture near-term momentum as sentiment remains positive.

Long-term hold: Structural exposure to wafer cleaning technology and the global semiconductor capex cycle.

With the next semiconductor capex cycle on the horizon, we see strong risk/reward and are raising our sell target from $48 to $64. At current levels, fundamentals are intact, and ACMR remains positioned for upside in the coming quarters.

Description: ACM Research Inc supplies advanced, innovative capital equipment developed for the world-wide semiconductor industry. Fabricators of advanced integrated circuits, or chips, can use its wet-cleaning and other front-end processing tools in numerous steps to improve product yield, even at increasingly advanced process nodes. It has designed these tools for use in fabricating foundry, logic and memory chips, including dynamic random-access memory, or DRAM, and 3D NAND-flash memory chips. The company also develops, manufactures and sells advanced packaging tools to wafer assembly and packaging customers

Roth Capital Maintains Buy on ACM Research, Raises Price Target to $50

JP Morgan Initiates Coverage On ACM Research with Overweight Rating, Announces Price Target of $36

Needham Reiterates Hold on ACM Research to Hold

Company: American Superconductor

Quote: $AMSC

Want to know how Sheraz and JR are buying and selling American Superconductor? Become a premium member today.

Sharks Opinon:

American Superconductor (AMSC) doesn’t make chips, but its advanced power electronics and superconductor systems are critical for semiconductor fabs. While not a chipmaker, the semiconductor industry is a fast-growing customer segment placing AMSC squarely in the supply-chain theme.

We traded AMSC successfully last year but exited too early; the stock rallied another 100% afterward.

Following a peak near $70, shares have retraced sharply and now trade around $30, resetting expectations and creating a more attractive entry point.

Why we like it: Supply-chain exposure: AMSC benefits directly from semiconductor capex and fab expansion. Risk/reward: The pullback presents a more compelling opportunity for investors willing to look past short-term volatility.

At current levels, AMSC offers a solid blend of thematic exposure and potential upside as semiconductor demand continues to grow.

Description: American Superconductor Corp generates the ideas, technologies, and solutions that meet the world's demand for smarter, cleaner, and energy. Through its Windtec Solutions, the company enables manufacturers to launch wind turbines quickly, effectively, and profitably. Through its Gridtec Solutions, the company provides engineering planning services and grid systems that optimize network reliability, efficiency, and performance. The company's segment includes Grid and Wind. It generates maximum revenue from the Grid segment.

Clear Street Reiterates Buy on American Superconductor, Maintains $52 Price Target

Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Roth MKM Reiterates Buy on American Superconductor, Maintains $29 Price Target

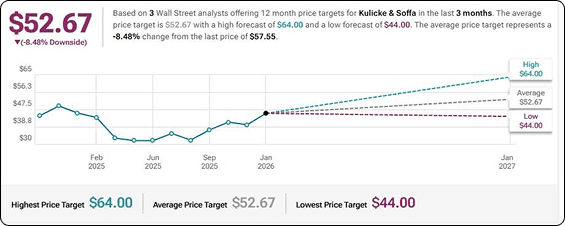

Company: Kulicke and Soffa Industries

Quote: $KLIC

Sharks Opinon:

Kulicke & Soffa is a core supply‑chain semiconductor stock, providing essential assembly and packaging equipment that turns bare silicon wafers into usable chips.

Its tools like wire bonding, flip‑chip assembly, and IC packaging are critical for AI, data centers, EVs, 5G, and advanced consumer electronics.

Unlike wafer fabs or chip designers, KLIC benefits from broad, structural demand: advanced packaging is increasingly needed as chips get more complex, OSAT activity rises, and heterogeneous integration becomes standard. Its high-precision equipment and long-standing customer relationships create a sticky, high barrier-to-entry moat.

KLIC’s growth isn’t tied to one segment it’s tied to the expansion of the semiconductor supply chain itself.

This makes it an attractive thematic play for investors looking for exposure to the semiconductor ecosystem beyond traditional chipmakers.

Description: Kulicke & Soffa Industries Inc. is a United States-based company that is principally engaged in designing, manufacturing, and selling capital equipment and expendable tools that are used for assembling semiconductor devices. The company has four reportable segments, which include Ball Bonding Equipment, Wedge Bonding Equipment, Advanced Solutions, and Aftermarket Products and Services. Its Ball Bonding Equipment segment which generates the majority of the revenue for the company includes results of the company from the design, development, manufacture and sale of ball bonding equipment and wafer level bonding equipment. The majority of its customers are located in the Asia-pacific region.

Needham Maintains Buy on Kulicke & Soffa Indus, Raises Price Target to $64

DA Davidson Maintains Buy on Kulicke & Soffa Indus, Maintains $55 Price Target

B. Riley Securities Reiterates Neutral on Kulicke & Soffa Indus, Raises Price Target to $39

Company: Ambiq Micro

Quote: $AMBQ

Get access to Sheraz and JR’s buys and sells in Ambiq Micro—join Stock Sharks today.

Sharks Opinon:

Ambiq Micro is a specialized semiconductor player focused on ultra-low-power microcontrollers and custom chip solutions. Its technology enables longer battery life for wearables, IoT devices, and edge AI applications, making it a critical enabler across multiple end markets.

AMBQ isn’t a mass-market chipmaker it’s a supply-chain enabler, providing essential IP and silicon that powers the next generation of connected devices.

As demand for energy-efficient, always-on devices grows, Ambiq stands to benefit from structural tailwinds in IoT, AI edge computing, and low-power consumer electronics, making it a thematic way to play the broader semiconductor ecosystem.

Description: Ambiq Micro Inc is a fabless semiconductor company that has developed technology based on a patented Sub-threshold Power Optimized Technology (SPOT) platform that significantly reduces the amount of power consumed by integrated circuits. It is a pioneer and provider of ultra-low power semiconductor solutions designed to address the significant power consumption challenges of general purpose and AI compute - especially at the edge.

UBS Maintains Neutral on Ambiq Micro, Lowers Price Target to $32

Stifel Initiates Coverage On Ambiq Micro with Buy Rating, Announces Price Target of $45

B of A Securities Initiates Coverage On Ambiq Micro with Neutral Rating, Announces Price Target of $42

Needham Initiates Coverage On Ambiq Micro with Buy Rating, Announces Price Target of $48

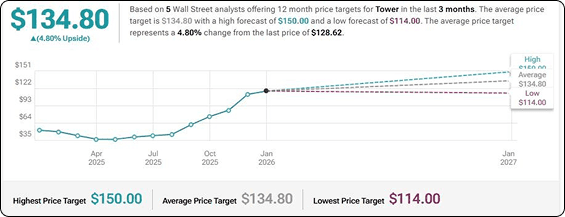

Company: Tower Semiconductor

Quote: $TSEM

Sharks Opinon:

Tower Semiconductor is a pure-play foundry providing specialized manufacturing services for analog, power, and RF chips. Its fabs produce critical components for automotive, industrial, IoT, and consumer electronics, making it a key link in the semiconductor supply chain.

As demand grows for custom and specialty chips, TSEM benefits from structural tailwinds in AI, EVs, and connected devices, positioning it as a thematic way to access the broader semiconductor ecosystem.

Description: Tower Semiconductor Ltd is a pure play specialty foundry that manufactures semiconductors. As a pure-play foundry, it focuses on producing integrated circuits (ICs), based on the design specifications of customers. The company's line of integrated circuits is incorporated into a range of products and markets, including consumer electronics, personal computers, communications, automotive, and industrial and medical device products. It produces ICs alongside wholly-owned subsidiaries through fabrication facilities located in Japan. The company has a geographical presence in the USA, Japan, Asia (other than Japan), and Europe

Benchmark Reiterates Buy on Tower Semiconductor, Raises Price Target to $150

Wedbush Downgrades Tower Semiconductor to Neutral, Maintains Price Target to $125

Barclays Maintains Equal-Weight on Tower Semiconductor, Raises Price Target to $97

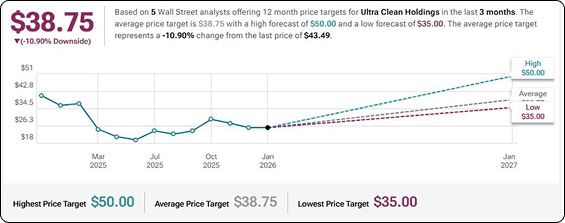

Company: Ultra Clean Holdings

Quote: $UCTT

Sharks Opinon:

Ultra Clean Holdings provides critical manufacturing and assembly services for semiconductor and advanced electronics companies, including precision cleaning, chemical delivery, and fluid management systems. Its solutions are essential for fabs producing semiconductors for AI, EVs, and data centers, making UCTT a key enabler in the semiconductor supply chain.

With growing global demand for advanced chips, UCTT benefits from structural tailwinds in AI, automotive, and industrial electronics, positioning it as a supply-chain theme stock in the semiconductor ecosystem.

Description: Ultra Clean Holdings Inc, through its subsidiaries, manufactures and supplies production tools, modules, and subsystems for the semiconductor capital equipment industry. The product includes precision robotic solutions, gas delivery systems, and a variety of industrial and automation production equipment products; subsystems include wafer cleaning subsystems, chemical delivery modules, top-plate assemblies, frame assemblies, and process modules. Its customer base includes firms in the semiconductor capital equipment industry, medical, energy, industrial, flat panel, and research equipment industries. It has two segments Products and Services. Its principal markets are Americas, Asia Pacific and EMEA.

Needham Maintains Buy on Ultra Clean Hldgs, Raises Price Target to $50

Oppenheimer Maintains Outperform on Ultra Clean Hldgs, Lowers Price Target to $30

TD Cowen Maintains Buy on Ultra Clean Hldgs, Lowers Price Target to $57

Company: Wolfspeed, Inc

Quote: $WOLF

Sharks Opinon:

Wolfspeed is a leading player in silicon carbide (SiC) semiconductors, controlling its supply chain from raw materials to finished devices—a strategic advantage for U.S. semiconductor independence. The company secured $1.5B in CHIPS Act funding and, after emerging from Chapter 11, the stock initially surged over 2,000%.

However, the restructuring came at a heavy cost to equity holders, with legacy shares almost entirely wiped out and control shifted to creditors. While the balance sheet is cleaner, the business remains capital-intensive, consistently unprofitable, and operationally challenged. In short, Wolfspeed has a strong technology platform and political tailwinds, but past execution failures, shareholder destruction, and ongoing cash flow uncertainty make it more a speculative restructuring story than a reliable semiconductor supply-chain play

Description: Wolfspeed Inc is involved in the manufacturing of wide bandgap semiconductors. It is focused on silicon carbide and gallium nitride materials and devices for power and radio frequency (RF) applications. The company serves applications such as transportation, power supplies, inverters, and wireless systems. Geographically, it derives a majority of its revenue from Europe and the rest from the United States, China, Hong Kong, Asia Pacific, and other regions.

Susquehanna Maintains Neutral on Wolfspeed, Lowers Price Target to $20

Piper Sandler Maintains Overweight on Wolfspeed, Lowers Price Target to $6

JP Morgan Downgrades Wolfspeed to Underweight

Goldman Sachs Maintains Buy on Wolfspeed, Lowers Price Target to $8