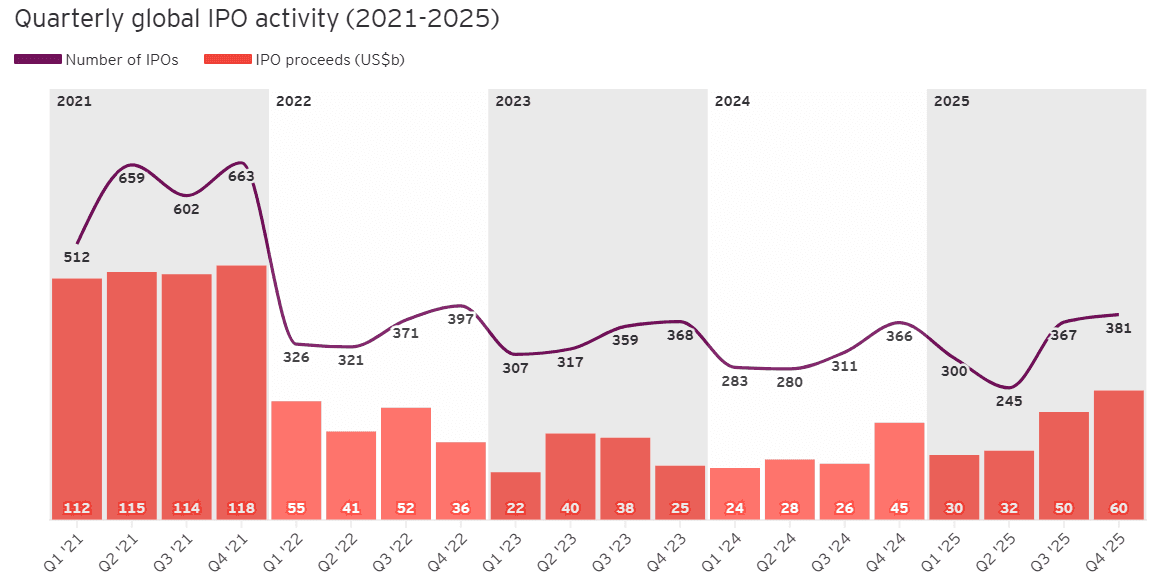

After a muted issuance environment from 2022 through 2024, improving risk appetite, lower interest-rate volatility, and a more stable macro backdrop have reopened the window for what could be the strongest IPO year since 2021.

A growing cohort of large, late-stage private companies particularly across AI, fintech, and space infrastructure are increasingly positioning themselves for potential 2026 listings.

Below, we highlight the most likely and closely watched candidates, based on recent media reports, advisor mandates, secondary market activity, and regulatory filings.

That said, IPO momentum slowed into the final quarter of the year as a record-length U.S. government shutdown effectively paused new offerings. October saw just 22 listings, followed by an even lighter November, underscoring how sensitive issuance remains to policy and macro disruptions.

Looking ahead, a sustained pickup in IPO activity during 2026 will depend on several interconnected forces. A clearer and more predictable monetary policy path remains critical, alongside contained market volatility.

Reduced geopolitical tension would further support investor confidence, while resilient consumer demand and a stable labor market provide the economic foundation needed for new issuance.

Equity market stability will also be key. Importantly, continued progress in AI adoption particularly as the application layer matures should help replenish the deal pipeline and support valuation confidence.

Taken together, these conditions point toward 2026 as a potential inflection point in the global IPO recovery. Companies that enter the year well-prepared, strategically focused, and operationally agile will be best positioned to move quickly when market windows open.

After several years defined by macroeconomic and geopolitical headwinds, 2025 marked a period of stabilization and recalibration for the global IPO market.

In total, 1,293 IPOs raised approximately $171.8 billion worldwide, representing a 39% increase in proceeds year over year despite a relatively flat number of deals compared with 2024. The rebound points to renewed investor confidence and a clear shift toward fewer, higher-quality offerings commanding larger checks.

Looking ahead, a temporary buildup of filings at the SEC, the clearing of holiday-related issuance delays, elevated private-market valuations, and a relatively low-volatility environment set the stage for a potential surge in IPO activity in 2026. If market conditions remain supportive, pent-up supply could move quickly once issuance windows reopen.

That said, risks remain. Sky-high valuations for private AI leaders such as OpenAI and Anthropic raise a critical question for markets: are these prices signaling the formation of a speculative peak, or do they reflect sustained and growing investor appetite as the AI investment cycle enters its early innings?

How that tension resolves will play a major role in shaping the tone and durability of the next IPO wave.

Across the Americas, the U.S. IPO market continued its recovery following the sharp downturn in 2022. The year opened with strong optimism, supported by resilient equity markets, heavy investment in AI-related infrastructure, and a deep pipeline of companies preparing to go public.

That momentum, however, was interrupted by two major shocks: the announcement of new U.S. tariffs in early April and the longest government shutdown in U.S. history later in the year. Together, these disruptions pushed many issuers to delay listings into 2026.

Even so, the U.S. IPO market emerged stronger. Deal count and total proceeds rose 27% and 38%, respectively, compared with 2024, with activity increasingly concentrated in larger, higher-quality transactions.

Eleven IPOs raised more than $1 billion up from seven the prior year and those deals alone accounted for over 40% of total proceeds.

In total, 70 offerings exceeded $100 million. AI remained a dominant driver of issuance, while crypto and digital assets, along with aerospace and defense technologies, also contributed meaningfully to market activity.

SPAC issuance rebounded sharply, with 2025 SPAC IPOs exceeding the combined total of 2023 and 2024. However, merger activity has lagged formation, reflecting ongoing performance and capital constraints. As a result, more than 100 active SPACs remain without announced targets, though many still have over six months to complete a transaction.

Elsewhere in the Americas, momentum was also evident. Canada’s TSX hosted two offerings exceeding $500 million, while Mexico recorded two large IPOs totaling more than $1 billion.

Overall, the pipeline for future offerings across the Americas remains robust. If recent IPOs continue to perform well in the aftermarket and macroeconomic conditions stay supportive, issuance activity is likely to accelerate further into 2026.

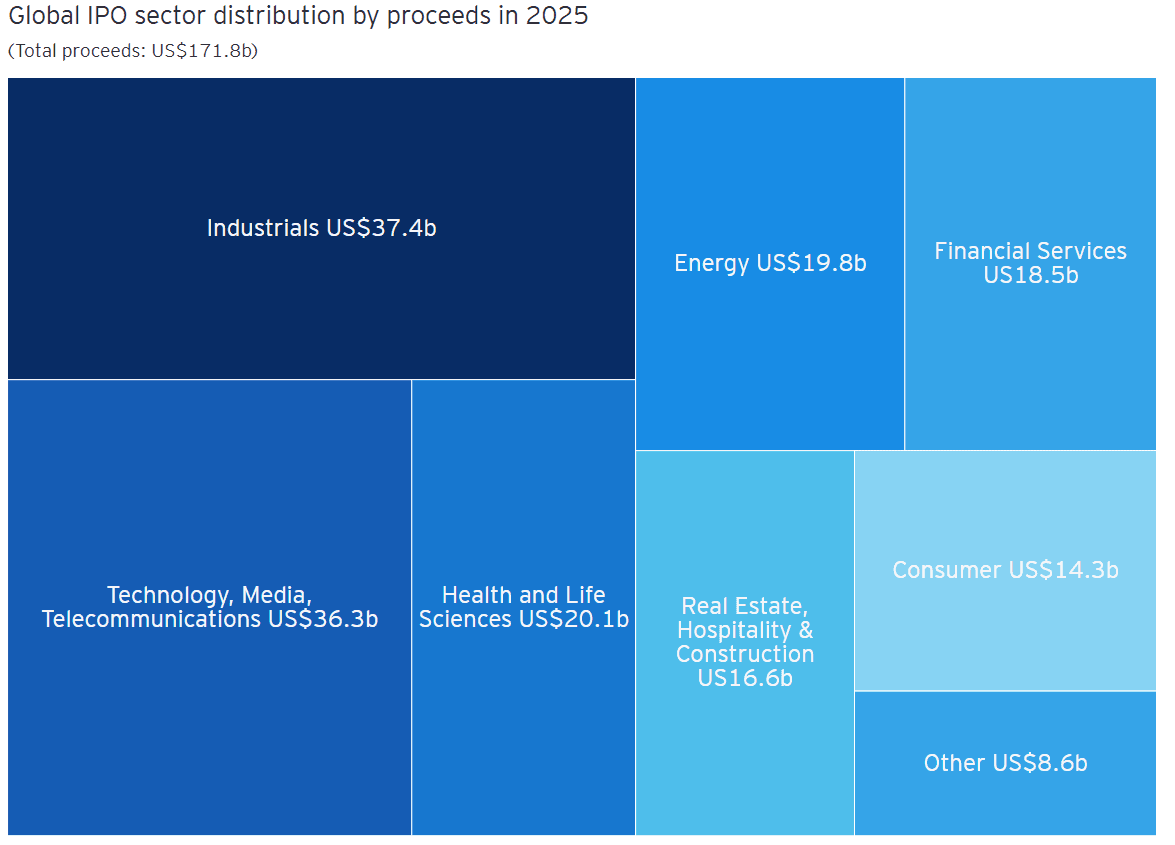

The sector composition of IPO activity highlights how capital is reallocating across the global economy. In 2025, industrials (22%) and technology, media, and telecommunications (TMT) (21%) accounted for the largest share of global IPO proceeds, though regional dynamics differed meaningfully.

In the U.S., TMT dominated, representing nearly 40% of total proceeds, driven largely by companies tied to AI infrastructure and data-intensive platforms. Europe, by contrast, showed a far more balanced mix, with activity spread across industrials, financial services, real estate and hospitality, and consumer sectors. In Asia-Pacific, issuance skewed toward large-scale players in AI-enabled robotics, mobility, and industrial systems, reflecting the region’s emphasis on applied automation and manufacturing leadership.

The transformative promise of artificial intelligence is undeniable, but current valuations have increasingly sparked debate over whether parts of the market are drifting into bubble territory. That question now sits at the center of investor sentiment.

In the U.S., Big Tech stocks accounted for roughly half of the S&P 500’s gains in 2025, with a small group of mega-cap AI leaders responsible for nearly one-third of the index’s advance.

This level of concentration highlights both AI’s outsized influence and its risk profile: even modest valuation resets among a handful of companies have the potential to ripple across broader equity markets and asset classes.

Most Anticipated IPOs of 2026

An overview of the most talked-about companies preparing for public market debuts, including firms that have already filed or are widely expected to list in 2026.

Company: SpaceX

Projected Ticker: SPCX ?

Valuation: $800B (proposed valuation for IPO $1.5 Trillion)

Key Investors: Elon Musk, Founders Fund, 7percent Ventures, Ace Capital, Aeon Family Of Funds, Craft Ventures, Fidelity

Sharks Opinion:

SpaceX will likely be the most anticipated and widely discussed IPO in market history. As a long-term portfolio holding, we believe it could make sense. From a short-term P/L perspective, however, the picture is far less clear.

That leads to the uncomfortable but necessary question: is SpaceX really worth a $1.5 trillion valuation?

On the surface, the case looks compelling. SpaceX operates more than 66% of all satellites currently in orbit through Starlink. It accounts for over 90% of U.S. space launches and is expected to generate roughly $15 billion in revenue this year. By most operational metrics, it is the undisputed leader in commercial space.

But scale does not automatically justify valuation.

The global space launch market itself is still relatively small less than $10 billion annually and has remained largely stagnant for decades when Starlink is excluded.

There is little evidence that Starship will meaningfully expand this market in the near term. The vehicle remains far from achieving its ambitious performance targets, and outside of a limited set of NASA missions and SpaceX’s internal needs, demand appears thin.

More importantly, over 80% of SpaceX launches are tied to Starlink, and Starlink’s long-term profitability remains uncertain at best. Capital intensity is extreme, replacement costs are ongoing, and pricing power is not yet proven at scale. In other words, much of SpaceX’s valuation rests on a single business line whose economics are still evolving.

SpaceX is a generational company. Whether it is a generational investment at IPO pricing is a very different question.

Description: Space Exploration Technologies (“SpaceX”) was founded with a mission to design, manufacture, and launch rockets and spacecrafts with the ultimate goal of enabling people to live on other planets. Headquartered in Hawthorne, CA, the company was founded by Elon Musk in 2002.

Company: OpenAI

Projected Ticker: OPAI?

Valuation: $499.92B

(Proposed IPO valuation $1 trillion)

Key Investors: Microsoft, Andreessen Horowitz, Founders Fund, K2 Global, Sequoia Capital, Thrive, Softbank

Sharks Opinion:

The investment case for OpenAI has rarely looked as fragile as it does in late 2025. What once appeared to be a company destined to dominate the artificial intelligence revolution increasingly resembles a structurally disadvantaged challenger, fighting a defensive battle on multiple fronts.

OpenAI is expected to burn roughly $9 billion this year on about $13 billion in revenue a cash burn rate near 70%. That is not the financial profile of a firm on the cusp of capturing durable, monopolistic profits. Instead, it looks more like a capital-intensive utility, spending enormous sums to deliver an increasingly commoditized product in a market where competitors are rapidly driving prices toward zero.

More concerning is the erosion of OpenAI’s technological moat. In 2023, GPT-4 represented a step-change in capability that felt untouchable. Today, that advantage has largely disappeared. Frontier-level performance is no longer exclusive, and the rapid rise of open-source models is accelerating innovation across the ecosystem at a pace that undermines proprietary dominance.

If this trend continues, the AI landscape may evolve less like a winner-takes-all platform market and more like an infrastructure layer highly valuable to the economy, but structurally hostile to sustained excess returns. For OpenAI, the challenge is no longer about building the best model. It is about proving that owning one still translates into lasting economic power.

Description: OpenAI is an AI research company which offers advanced AI models to organizations and individuals. OpenAI’s models are designed for tasks like language processing, coding, and problem-solving, with the goal of making AI tools accessible and effective for a wide range of users. The company aims to help users improve efficiency and build smarter systems while advancing AI research. This company was founded by Sam Altman, Greg Brockman, Ilya Sutskever, John Schulman, Wojciech Zaremba, Elon Musk, Andrej Karpathy, Trevor Blackwell, Durk Kingma, and Pamela Vagata in 2015 and is headquartered in San Francisco, CA.

Company: Anthropic

Projected Ticker: N/A

Valuation: $183B

(Proposed IPO Valuation $300 B)

Key Investors: Google, Menlo Ventures, Nls Ventures, Raison, Salesforce Ventures, Blackrock, Blackstone, Coatue Management, D1 Capital Partners, Amazon

Sharks Opinion:

Anthropic is in early talks to launch one of the largest initial public offerings as early as next year, while simultaneously weighing fresh private funding that could push its valuation over the $300 billion mark. Both Anthropic and OpenAI are now preparing for what could be monumental IPOs, and their investors are demanding a decisive first-mover advantage. With pervasive chatter about an “AI bubble” swirling and increasing scrutiny over scalable revenue growth, the company that lists first will serve as the crucial litmus test. They will determine whether the public market views these astounding valuations as the foundation for future growth or an inflated ceiling poised for a correction.

Description: Anthropic is an AI research company which offers AI models focused on alignment and safety to organizations and developers. Anthropic's models are designed to prioritize safety and interpretability, supporting AI applications that align with human values. The company strives to promote responsible AI development through its research and tools, helping organizations deploy AI in a way that adheres to ethical standards. This company was founded by Dario Amodei, Daniela Amodei, Jack Clark, and Jared Kaplan in 2021 and is headquartered in San Francisco, CA

Company: Stripe

Projected Ticker: STRP ?

Valuation: $92.37B

Key Investors: Andreessen Horowitz (a16z), Sequoia Capital, Founders Fund, General Catalyst, Thrive Capital, Redpoint, DST Global, Kholsla Ventures, Kleiner Perkins,, Temasek, Baillie Gifford, BDT & MSD Partners, NTMA, Ireland Strategic Investment Fund, AXA, Fidelity Investments.

Sharks Opinion:

Stripe, once considered the crown jewel of fintech, would face meaningful challenges if it attempted to go public in the near term.

While the company still commands a dominant position in global payments and carries a private valuation in the $50–60 billion range, the broader macro backdrop, ongoing pressure across fintech multiples, and internal strategic priorities suggest an IPO is not imminent.

That said, Stripe remains structurally differentiated. Unlike peers such as Square, Plaid, and Adyen, Stripe’s end-to-end payments and banking infrastructure positions it less as a single product company and more as core financial plumbing for the digital economy.

Its ambition to power the full financial stack from payments to banking-as-a-service supports a higher-quality, longer-duration revenue profile.

For now, management appears content staying private, prioritizing internal growth while providing employee liquidity through secondary transactions and private funding rounds. From an investor standpoint, Stripe still screens as one of the strongest long-term IPO candidates in fintech, with a high-margin, recurring-revenue model that could be well received once market conditions and sector sentiment turn more constructive.

Description: Stripe is a fintech company focused on building the economic infrastructure for the internet, offering software that allows enterprises to accept online payments and run technically sophisticated financial operations in more than 100 countries. The company was founded by John Collison and Patrick Collison in 2010 and is headquartered in San Francisco, CA.

Company: Databricks

Projected Ticker: DATAB?

Valuation: $139.36B

Key Investors: Andreessen Horowitz, Blackrock, Blackstone, Coatue Management, Fidelity, Baillie Gifford, Blackrock, Canada Pension Plan Investment Board

Sharks Opinion:

Databricks recently crossed the $100 billion valuation mark following its latest funding round, placing it alongside elite private names such as SpaceX, ByteDance, and OpenAI.

With an estimated $4 billion annualized revenue run rate, the company is effectively valued at roughly 25× forward revenue.

That premium stands out when compared to public-market peer Snowflake.

Snowflake is expected to generate about $4.4 billion in revenue for its fiscal year ending January 2026, representing roughly 27% year-over-year growth, and trades closer to 18× forward revenue with a market cap near $80 billion.

Databricks’ faster growth profile roughly 50% versus Snowflake’s high-20s helps justify the valuation gap, at least on paper.

If Databricks can sustain even a more conservative 40% growth rate next year, a 25× multiple would imply a market capitalization approaching $140 billion.

However, that outcome assumes public markets remain willing to reward high-growth software names with elevated multiples an assumption that has proven inconsistent in recent cycles.

There’s no question Databricks has many of the right ingredients: rapid top-line expansion, deep customer lock-in, and a platform well-positioned for the AI and data infrastructure era.

Still, history urges caution. Several marquee tech IPOs entered the market with similar momentum, only to face valuation compression once growth normalized and expectations reset.

Databricks may ultimately justify its price, but the transition from private-market enthusiasm to public-market discipline is rarely seamless.

Description: Databricks is a data and AI company which offers a unified analytics platform for processing and analyzing large-scale data to enterprises. Databricks’ platform is built on Apache Spark and is designed to simplify data engineering, data science, and machine learning workflows. The platform seeks to accelerate innovation by enabling teams to process, analyze, and collaborate on big data efficiently. This company was founded by Ali Ghodsi, Ion Stoica, Matei Zaharia, Patrick Wendell, Reynold Xin, Andy Konwinski, and Arsalan Tavakoli-Shiraji in 2013 and is headquartered in San Francisco, CA.

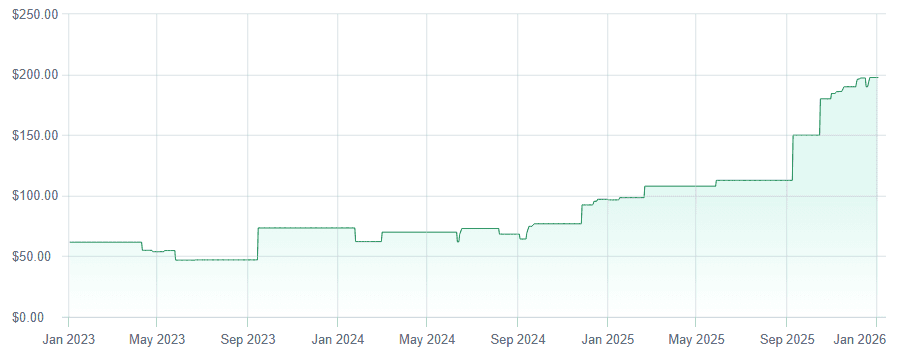

Company: Canva

Projected Ticker: CANV ?

Valuation: $42 Billion

Key Investors: Blackbird Ventures, Felicis Ventures, Matrix Partners, Owen Wilson, Bessemer Venture Partners, Blackbird Ventures, General Catalyst

Sharks Opinion:

Canva is accelerating its push into AI-driven design as it positions itself for the next phase of growth and, eventually, a potential IPO. In April, the company rolled out a conversational AI photo editor, a clear signal of its intent to move upmarket and capture enterprise customers traditionally dominated by Adobe.

That competitive pressure is intensifying. Adobe continues to invest heavily in its Firefly AI platform, while Figma’s public debut in July at a $34 billion valuation has reset expectations for design-centric software companies in the public markets.

Together, these developments have raised the bar for scale, differentiation, and monetization across the sector.

Founded in 2013 by Melanie Perkins, Canva has quietly built one of the world’s most widely adopted design platforms, now boasting more than 240 million monthly active users and annualized revenue exceeding $3.3 billion.

Its freemium model, combined with expanding enterprise offerings, gives Canva a rare blend of mass-market reach and corporate relevance.

While the company has not formally disclosed IPO plans, recent secondary share sales have provided liquidity for employees while allowing Canva to remain private.

This approach suggests management is in no rush to test public markets, instead choosing to deepen its product moat and AI capabilities before subjecting the business to public-market scrutiny.

Description: Canva is the developer of a design tool that includes an integrated marketplace that has both free and paid stock photography, fonts, illustrations, and thousands of templates; a paid subscription that offers the ability to set up a brand kit, and ensure consistency across their designs; and a print service that gives users the ability to produce professional prints. The company was founded by Cameron Adams, Cliff Obrecht, and Melanie Perkins in 2012 and is headquartered in Sydney, Australia.

Company: Once Upon A Farm

Projected Ticker: OFRM

Valuation: $1B

Key Investors: CAVU Consumer Partners, S2G Investments, and Cambridge Companies SPG.

Sharks Opinion:

When news broke that Once Upon a Farm had filed for an IPO, the initial reaction was excitement it’s always encouraging to see a consumer brand reach for the public markets.

However, a closer look suggests that this offering may not yet be market-ready.

There’s certainly a lot to admire about OFRM strong branding, a growing presence in the organic foods space, and a loyal customer base. But the fundamentals and scale required for a smooth public debut appear limited compared with larger, more established peers.

The company’s potential performance will inevitably invite comparisons to the Honest Company, the consumer packaged-goods brand co-founded by Jessica Alba. Honest went public in 2021 at a $1.44 billion valuation, but its stock has struggled since, underscoring the challenges young consumer brands face in sustaining investor confidence once they enter the public arena. OFRM IPO could generate buzz, but investors should approach with measured expectations.

Description: Producer of cold-pressed organic baby food intended to serve tasty, crave-worthy, refrigerated snacks for children of all ages. The company's food is made using high-pressure processing technology to retain product flavor, aroma, color, texture and nutrients to optimize nutrition absorption and palate development in infants, enabling parents to serve their kids fresh, organic and healthy food.

Company: Cerebras

Projected Ticker: $CBRS ?

Valuation: $8.73B

Key Investors: 1789 Capital, Alpha Wave Ventures, Altimeter Capital, Atreides Management

Sharks Opinion:

Cerebras attracted attention when rumors of an IPO surfaced last year, but a deeper look raises concerns.

The company’s IPO structure and promotional approach suggest that management may be more focused on accessing public-market liquidity than on addressing core technology challenges or positioning themselves as a true competitor to Nvidia.

At present, the product is far from competitive. While the IPO could generate an initial surge in share prices fueled by hype and media buzz, the long-term performance on public markets is likely to disappoint. This scenario carries a deeper risk: critical intellectual property could fall into the wrong hands, potentially undermining the emergence of what could have been the next great American chip company.

A more prudent path would be for Cerebras to stay private, consider a down round if necessary, and focus on developing a compelling, competitive product before seeking public investors.

Description: Cerebras is a semiconductor technology company which offers AI compute systems for machine learning and high-performance computing applications to enterprises. Cerebras’ systems are powered by its Wafer-Scale Engine, one of the world’s largest AI processors, designed to accelerate AI model training and inference. The company aims to provide transformative computing power, supporting breakthroughs in industries such as healthcare, energy, and scientific research. This company was founded by Andrew Feldman, Gary Lauterbach, Michael James, Sean Lie, and Jean-Philippe Fricker in 2016 and is headquartered in Sunnyvale, CA.

Company: Kraken

Projected Ticker: N/A

Valuation: $12.55B

Key Investors: Hummingbird Ventures, Blockchain Capital, Tribe Capital, SkyBridge Capital, SBI Holdings and Digital Currency Group.

Sharks Opinion:

Kraken’s anticipated IPO, targeted for early 2026, will invite public investors to assess the company’s future cash flows within a maturing cryptocurrency exchange market.

Below, we outline the investment thesis, expected timeline and use of proceeds, and valuation considerations.

Kraken has consistently ranked among the top crypto exchanges by volume, though its global share remains modest.

As of April 2025, Kraken accounted for roughly 2% of worldwide spot trading, trailing Binance (~38%), Coinbase (~6.9%), and several Asian exchanges (~5–9% each).

Despite this, Kraken maintains a strong position in fiat-centric trading and benefits from a reputation for security, regulatory compliance, and reliability.

The company differentiates itself through a focus on quality, compliance, and trust factors increasingly valued as regulatory scrutiny intensifies. Kraken also has potential avenues for growth through strategic acquisitions of smaller compliant exchanges, which could further expand its market presence and operational scale.

Description: Kraken is a crypto exchange based on euro volume and liquidity. Globally, Kraken’s client base trades more than 100 digital assets and 8 different fiat currencies. Kraken was the first U.S. crypto firm to receive a state-chartered banking license, as well as one of the first exchanges to offer spot trading with margin, regulated derivatives, and index services. Kraken is based in San Francisco, CA and was founded in 2011 by Jesse Powell.

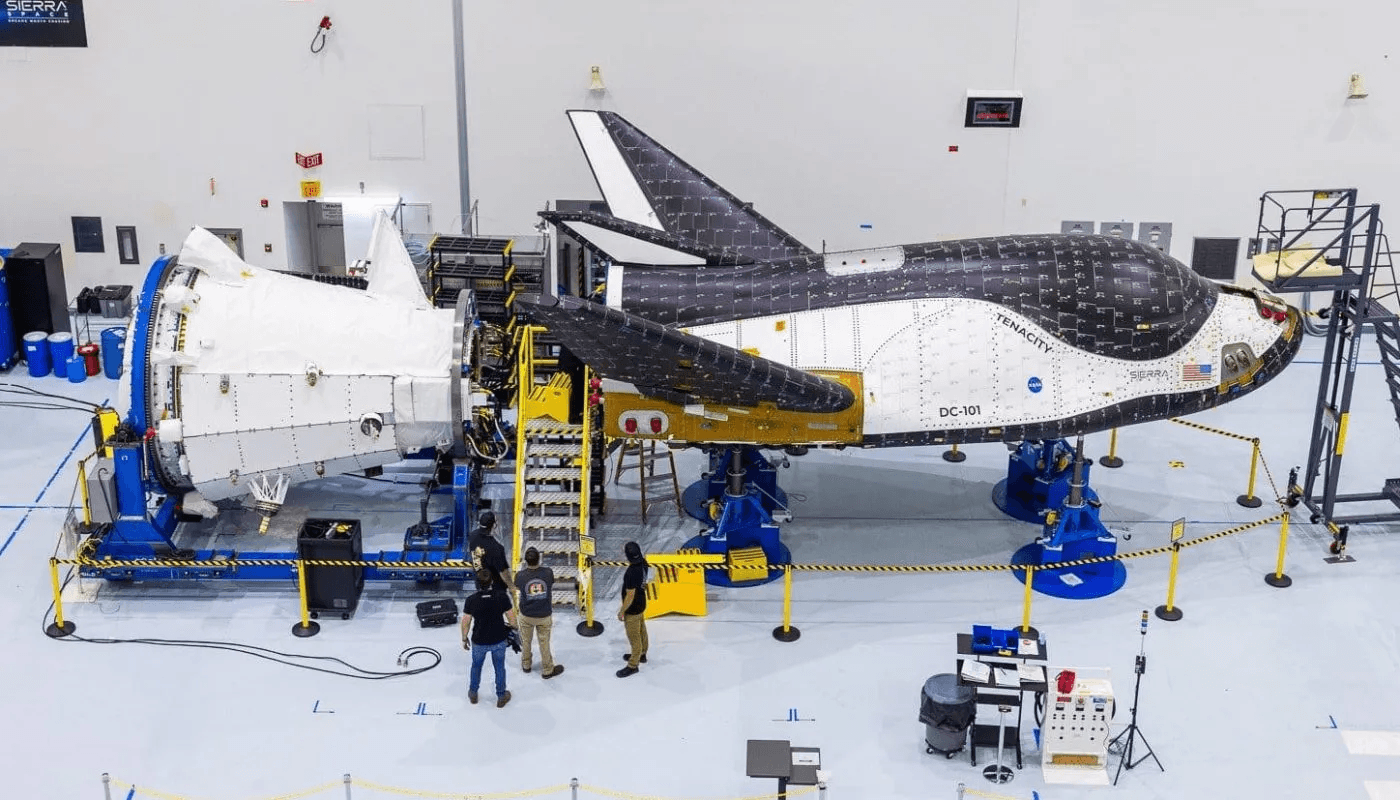

Company: Sierra Space

Projected Ticker: N/A

Valuation: $5.3 B

Key Investors: General Atlantic, Coatue, BlackRock Private Equity Partners, MUFG, Kanematsu, Tokio Marine

Sharks Opinion:

Sierra Space is the only company operating a commercial winged spaceplane, Dream Chaser, capable of landing on standard airport runways. Its gentle reentry is uniquely suited for returning sensitive scientific experiments and biological cargo that could be damaged by capsule splashdowns, such as SpaceX’s Dragon.

Defense Pivot: Sierra Space has strategically shifted toward national security, securing over $1 billion in defense contracts.

This pivot provides a stable revenue base, reducing dependence on purely commercial or scientific missions, especially amid the U.S. Space Force’s expanding budget.

Market Tailwinds: Looking ahead, a potential 2026 SpaceX IPO could broadly “re-rate” the space sector, boosting valuations for competitors like Sierra Space as generalist investors increase exposure to aerospace and space technology stocks.

Description: Known for its Dream Chaser vehicle, Sierra Space, founded in 2021, is a developer of commercial infrastructure and transportation for outer space. Dream Chaser is a cargo vehicle that hauls supplies to astronauts working in space at the International Space Station. However, Sierra Space also works on other commercial space projects, including commercial space station projects and astronaut training programs. Sierra Space is headquartered in Louisville, Colorado.

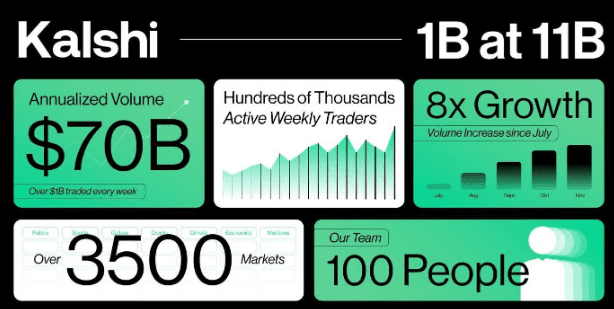

Company: Kalshi

Projected Ticker:

Valuation: $11B

Key Investors: Andreessen Horowitz, Capitalg, Coinbase Ventures, General Catalyst

Sharks Opinion:

While it’s a long shot that either Kalshi or Polymarket will go public in 2026, both are among the hottest companies in the emerging prediction market space.

Kalshi IPO Potential: Going public would cement Kalshi’s position as a leader in federally regulated U.S. prediction markets, offering investors a unique, compliant way to access event-based contracts.

As the first federally regulated exchange for event contracts (Designated Contract Market), Kalshi can operate nationwide under CFTC oversight a major advantage over competitors that must navigate state-by-state licensing.

This allows them to tap the entire U.S. market, including the $30 billion sports betting sector. Revenue growth is strong, with an estimated $600–700 million run rate as of late 2025, though the long-term profitability of its low-fee business model remains unproven.

Competitive Landscape: Kalshi faces intense competition from well-funded rivals, including Polymarket backed by the NYSE’s parent company and traditional sportsbooks such as DraftKings entering the space.

User Retention & Volatility: Trading volumes are highly event-driven, spiking during major moments like elections or March Madness, then potentially declining during quieter periods. This seasonality raises questions about consistent engagement and sustainable growth outside peak cycles.

An IPO would signal industry maturity, but investors should be aware that regulatory uncertainty and profitability questions still make this a high-risk play.

Description: Kalshi is the first CFTC regulated exchange dedicated to trading on a new asset class: event contracts. The contracts cover a wide range of topics from weather to international affairs to media and more. Kalshi makes money by charging a transaction fee on the expected earnings on the contract. The company's mission is to allow people to capitalize on their opinions and hedge against everyday risks. Kalshi was founded in 2018 by Luana Lara and is headquartered in New York, NY.

Company: Polymarket

Projected Ticker: N/A

Valuation: $9B

Key Investors: Intercontinental Exchange,1789 Capital, 1confirmation, Founders Fund, Kevin Hartz, Parafi Capital, Vitalik Buterin

Sharks Opinion:

Like Kalshi, Polymarket is a long shot for a 2026 IPO but momentum is building fast, and when companies scale quickly, going public is often the next step.

IPO Potential: A public listing would likely be a watershed moment for Polymarket and the broader prediction market industry. Success for investors, however, will hinge on how effectively the company navigates significant regulatory hurdles and establishes a sustainable, profitable business model beyond sheer trading volumes.

Regulatory Environment: While Polymarket has CFTC approval for its U.S. platform, the global regulatory landscape for prediction markets remains fragmented and highly scrutinized. Ongoing debates over whether these platforms constitute gambling could result in legal challenges, potentially escalating to the Supreme Court, creating material risk for the business.

Business Model & Profitability: Polymarket currently prioritizes market share over profits and has historically not charged trading fees. While potential revenue streams, such as data services, exist, the long-term viability and profitability of the model remain unproven.

An IPO would mark a milestone for the industry, but investors should approach with caution given regulatory uncertainty and untested monetization strategies.

Description: Polymarket is a decentralized information markets platform which aims to offer event prediction markets to individuals interested in speculating on future events. By connecting to the platform through an Ethereum-compatible wallet, the company's mission is to help people use the USDCstablecoin to place bets on events. Polymarket was founded in 2020 by Shayne Coplan and is headquartered in New York, NY.

Potential IPOs on Our Radar

Here’s a look at the companies that stand out most to us as potential 2026 listings. If any of these firms go public, we would be evaluating them for day-one participation.

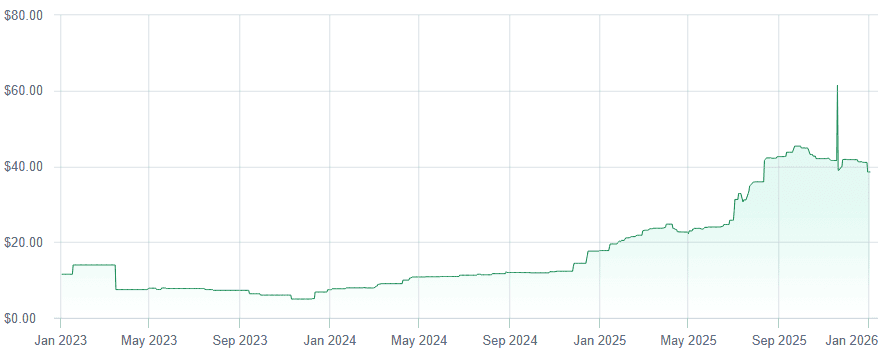

Company: Anduril

Projected Ticker: N/A

Valuation: $30.5B

Key Investors: Altimeter Capital, Baillie Gifford, Counterpoint Global, Fidelity, Founders Fund

Sharks Opinion:

Anduril Industries remains privately held with no official IPO date, though founder Palmer Luckey has hinted at a potential timeframe in 2026 or later.

The company benefits from strong private funding and rapid growth, prioritizing favorable market conditions over rushing to go public. Retail investors should approach pre-IPO shares with caution.

IPO Potential: An Anduril IPO could offer a compelling, though less speculative, investment opportunity compared with Palantir’s public debut. The contrast lies in business models, valuation dynamics, and market timing.

Comparative Insights: Anduril vs. Palantir:

Palantir (PLTR): Went public via direct listing in September 2020, offering high-margin, scalable software platforms (Gotham and Foundry) for government and commercial clients. Benefits include rapid revenue growth, robust contracts, and high profitability. Risks include extremely high valuation (~70x trailing sales) and intense competition.

Anduril: Operates in the physical layer of defense tech, combining hardware manufacturing with software solutions. The model is more capital-intensive and operationally complex but provides tangible products for the defense industry, appealing to investors seeking concrete, high-growth exposure.

In short, Anduril’s IPO would likely deliver a grounded, high-growth defense technology play, contrasting with Palantir’s premium-valued, software-centric offering. Investors can expect growth potential tied to both defense contracts and scalable hardware-software integration.

Description: Anduril is a developer of defense technology focused on delivering consumer hardware and national-security software, leveraging off-the-shelf components with custom engineering to bring products to market faster, cheaper and more effectively. The company was founded by Brian Schimpf, Matthew Grimm, Palmer Luckey, Trae Stephens, and Joseph Chen in 2017 and is headquartered in Costa Mesa, CA

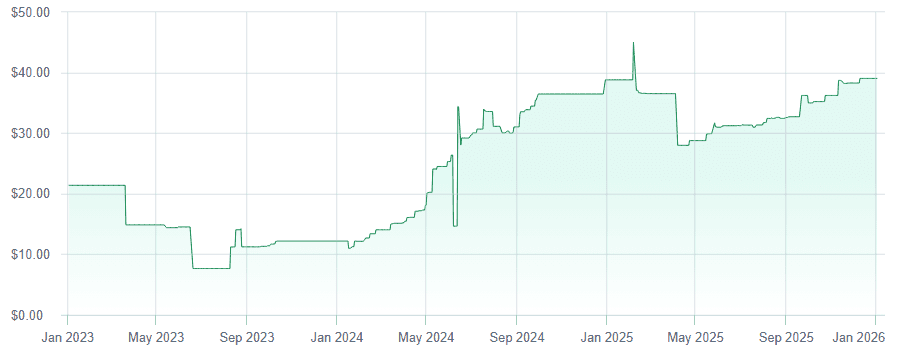

Company: Redwood Materials

Projected Ticker: N/A

Valuation: $5.66B

Key Investors: Amazon, Breakthrough Energy Ventures, Capricorn Investment Group, Toyota

Sharks Opinion:

Redwood Materials remains privately held, with no official IPO date, though some projections suggest a potential offering in 2026 or the near future. Founded by Tesla’s former CTO, the company specializes in battery recycling and building a domestic EV supply chain.

IPO Potential: A 2026 IPO would likely be one of the most significant debuts in the “circular economy” space, positioning Redwood as a vertically integrated leader in sustainable energy materials.

Key Highlights:

Vertical Integration: Unlike pure recyclers, Redwood operates a full-cycle manufacturing model. By 2026, it aims to produce 100 GWh of cathode-active materials (CAM) annuallyenough for approximately 1 million EVs.

Energy Storage Expansion: In late 2025, Redwood launched Redwood Energy, repurposing EV batteries for grid-scale storage, targeting high-demand applications such as AI data centers.

Financial Strength: Backed by a $2 billion DOE loan and consistent private funding, Redwood enters 2026 with a strong balance sheet relative to peers.

Investment Case: An IPO would position Redwood as a profitable, vertically integrated manufacturer, contrasting with prior “pure-play” EV battery recyclers like Li-Cycle. While T1 Energy has pivoted successfully into solar, Redwood retains a dominant position in battery recycling and supply chain leadership, offering investors exposure to both sustainability and scalable manufacturing.

Description: Redwood Materials is a developer of sustainable lithium-ion battery recycling technology designed to optimize circular supply chains to recycle waste into profit. Redwood was founded by JB Straubel (previously Chief Technology Officer and co-founder of Tesla) in 2017 and is headquartered in Carson City, NV. The company's technology processes scrap from battery cell production and consumer electronics, seeking to help clients turn them into electric vehicles and energy products, effectively re-using and processing raw materials into the battery supply chain.

Company: Render

Projected Ticker: RNDR?

Valuation: $1.51B

Key Investors: Addition, Bessemer Venture Partners, General Catalyst, South Park Commons

Sharks Opinion:

Render Network is a decentralized GPU computing platform that connects artists and developers with providers of idle GPU capacity, enabling high-demand workloads such as 3D rendering and AI/ML tasks.

Key Developments:

Token Migration: In November 2023, Render migrated its network from Ethereum to Solana to improve transaction speeds and reduce costs.

Industry Adoption: The network has an advisory board of prominent entertainment and tech industry leaders, signaling a strategic focus on bridging Web3 technologies with traditional creative industries.

Investment Profile: Render (RENDER) remains privately held and has not conducted an IPO. Its value is tied to the RENDER cryptocurrency token, which is used to access decentralized GPU compute power across the network and trades on various exchanges.

Outlook: Render’s decentralized model positions it as a unique infrastructure play at the intersection of blockchain, creative content, and AI/ML computing.

Description: Render, founded in 2018, is a a cloud hosting platform that's designed to enhance the experience of developers. Its platform aims to facilitate the building and running of all applications and websites, with complimentary SSL, a global CDN, and automatic deployment from Git. Their goal is to allow businesses to cut down on both complexity and expenses. Render is headquartered in San Francisco, California.

Company: Inspire Brands

Projected Ticker: N/A

Valuation: $20 billion

Key Investors: Roark Capital

Sharks Opinion:

In February 2024, reports indicated that Roark Capital was exploring a potential IPO for Inspire Brands.

Valuation: Early estimates suggest a valuation of around $20 billion, positioning it as one of the most significant restaurant IPOs in recent years. Inspire leverages shared back-of-house technology and cross-training labor across its portfolio including Dunkin’ and Arby’s to drive operational efficiencies and potentially achieve higher-than-peer returns.

Investment Thesis: A central focus of the IPO will likely be technological synergy. Inspire’s “Alliance Kitchen” concept reportedly reduces labor by 54% and energy use by 50%, showcasing a level of operational integration that competitors like YUM and QSR have yet to replicate at scale.

Bear Case: Integrating 20,000+ domestic locations with diverse customer demographics poses significant data and operational challenges.

Mismanagement could slow decision-making and temper projected returns, making execution risk a key consideration for investors.

Outlook: If executed successfully, Inspire Brands could redefine restaurant-scale efficiency and serve as a bellwether for tech-driven operational models in the QSR sector.

Description: Inspire Brands LLC is an American fast-food restaurant franchise company. Backed by Roark Capital Group, it owns the Arby's, Buffalo Wild Wings, Sonic Drive-In, Jimmy John's, Dunkin' Donuts, and Baskin-Robbins chains, which have a combined 33,000 locations and US$32.6 billion in system sales.

Company: SKIMS

Projected Ticker: N/A

Valuation: $5B

Key Investors: D1 Capital Partners, Greenoaks Capital Partners, Imaginary Ventures, Wellington

Sharks Opinion:

Co-founder Jens Grede has indicated that while Skims may go public in the future to provide “optionality” for institutional investors, no final decision or IPO date has been set. The company continues to focus on growth as a private entity with long-term investors.

Previous Speculation: Early reports suggested a potential IPO as soon as 2024 or the first half of 2025. However, uncertain market conditions and recent successful private funding rounds have delayed any public listing.

Growth Profile: Skims has demonstrated strong, consistent expansion, including a 50% revenue increase from 2022 to 2023, highlighting scalability and robust market demand.

Profit Margins: Healthy gross and net margins reflect operational efficiency and pricing power, setting Skims apart from other DTC brands that struggled in their IPO launches.

Customer Metrics: Skims’ direct-to-consumer model, bolstered by strong brand loyalty and social media engagement, likely produces favorable LTV-to-CAC ratios, a key indicator of sustainable, long-term profitability.

Takeaway: While the timing of a public debut remains uncertain, Skims’ strong fundamentals, growth trajectory, and operational efficiency position it as a compelling potential IPO candidate for the near future.

Description: Skims, founded in 2018, is a solutions-oriented brand striving to create the next generation of underwear, loungewear, and shapewear. The company manufactures and retails undergarments and loungewear designed to enhance the body shape. It offers a wide range of products including bodysuits, shapewear, and underwear that feature styles and color shades for different body types, with the goal of providing women with the right support and coverage. Skims is headquartered in Culver City, California.