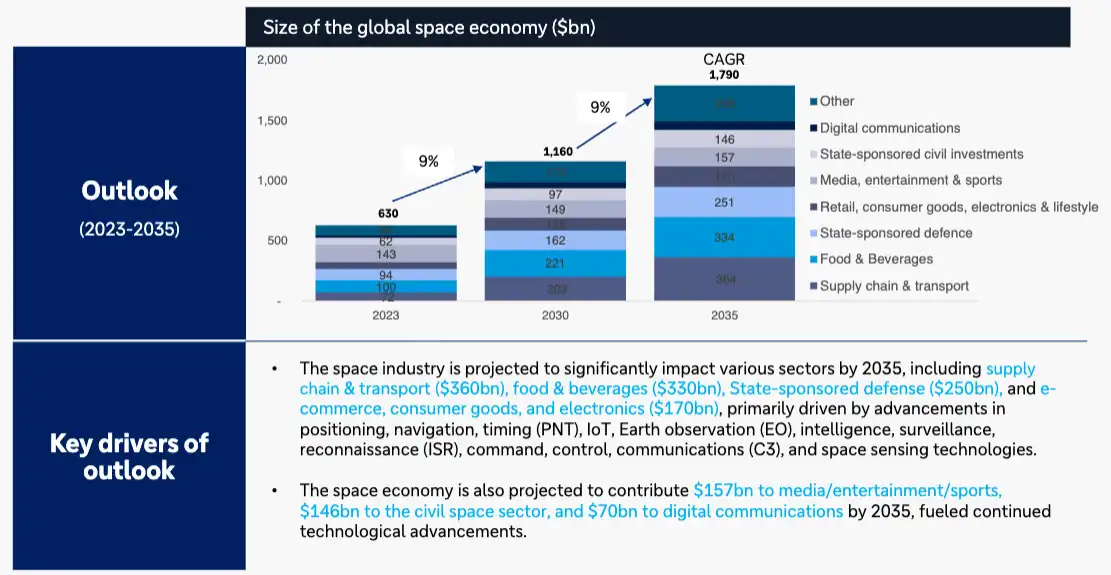

Over the past four decades, the cost of launching payloads into space has declined by nearly 98%, fundamentally reshaping the economics of the industry.

As a result, the space economy has expanded at an accelerating pace and is projected to reach approximately $772 billion by 2027.

What was once a government-dominated frontier has evolved into a commercially driven ecosystem, opening the door to a new wave of investment opportunities that extend far beyond space tourism and into the core infrastructure shaping the future of both technology and global power dynamics.

The United States continues to lead this new space race, not just in activity but in structure.

In 2026 alone, the U.S. conducted 193 launches, outpacing China, Russia, and India by a wide margin.

What differentiates the U.S. is the dominance of its private sector, with commercial launches accounting for roughly 81% of total activity.

This shift toward commercialization has accelerated innovation, reduced costs, and created a competitive environment where companies, not just governments, are driving progress.

As capital continues to flow into the sector from institutions, ultra-high-networth investors, and strategic players, the space economy is becoming increasingly investable.

The opportunity set is no longer limited to speculative concepts but is anchored in tangible business models and revenue-generating infrastructure.

We see these as the core themes and narratives currently driving the Space Race:

Launch Platforms & Defense: Innovations in launch vehicles, medium- and heavy-lift rockets, and national security-focused space technologies are shaping both commercial and government priorities.

Satellite Communications & Imagery: Growth in LEO constellations, SmallSats, and high-resolution Earth observation is transforming global communications, defense intelligence, and commercial applications.

Space Infrastructure & New Listings: Expansion in satellite manufacturing, in-orbit services, space-based data platforms, and the emergence of new publicly listed space companies are providing fresh investment opportunities and fueling sector growth.

The rapid expansion of the space economy is creating a compelling opportunity for investors to gain exposure to the core tools and services that make space activity possible.

At the center of every mission are spacecraft ranging from satellites to launch vehicles which serve as the functional backbone of operations beyond Earth.

However, none of these systems have value without reliable and cost-effective access to orbit, making launch services one of the most critical and investable layers of the entire ecosystem.

Alongside this, space-related manufacturing continues to scale, supporting the production of increasingly sophisticated hardware required to meet rising global demand.

Launch services sit at the foundation of the space economy, enabling virtually every downstream application.

From communications and navigation to Earth observation, the deployment of satellites depends entirely on consistent and efficient launch capabilities.

As demand for satellite constellations and real-time data accelerates, the importance of launch providers continues to grow, positioning them as key enablers of both commercial expansion and national security priorities.

Satellites themselves represent the operational backbone of the space economy, powering global connectivity and data transmission.

Satellite communication networks facilitate everything from internet access in remote regions to live broadcasting and secure military communications, making them indispensable in an increasingly connected world.

The transition from government-led space programs to a commercially driven ecosystem has fundamentally reshaped the economics of the industry.

Private players such as SpaceX, Rocket Lab, and Blue Origin have driven launch costs down dramatically while accelerating deployment timelines, unlocking entirely new business models built around satellite constellations and recurring revenue streams.

This shift has not only increased accessibility to space but has also attracted significant institutional capital, with investment banks and financial intermediaries playing a growing role in facilitating funding, M&A activity, and strategic partnerships as these companies scale.

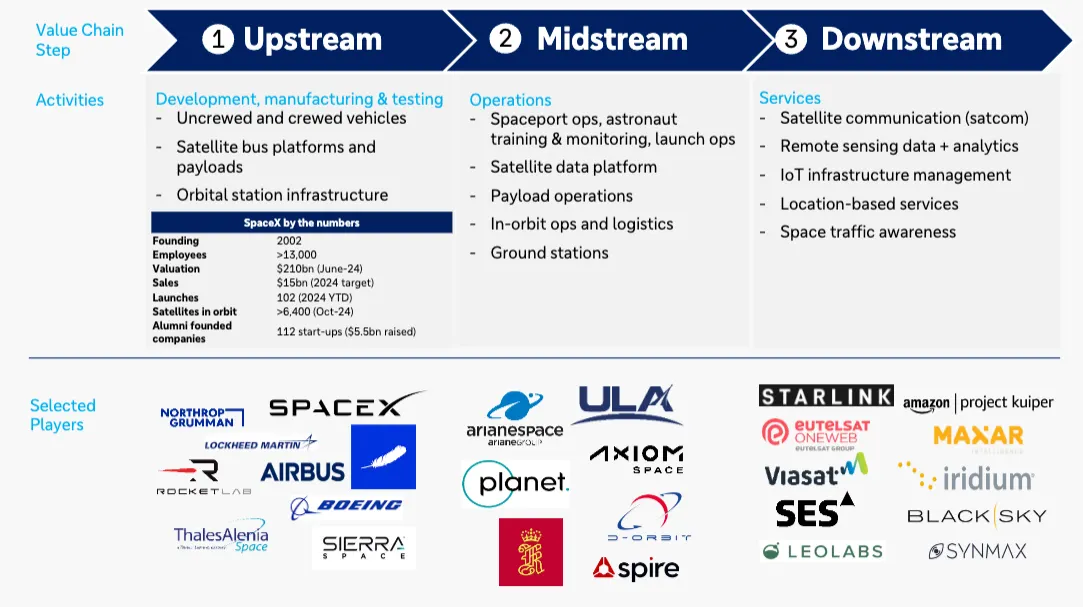

Within the space economy, the market is broadly divided into upstream and downstream segments.

The upstream layer includes spacecraft design, manufacturing, launch infrastructure, and ground operations, essentially everything required to get assets into orbit.

This segment, while critical, continues to face structural challenges including rising input costs, component shortages, and supply chain disruptions tied to both post-COVID dynamics and geopolitical tensions.

A clear example of this fragility was seen in 2022, when OneWeb’s reliance on Russian Soyuz launches collapsed following sanctions, leaving satellites stranded and forcing a rapid restructuring of its launch strategy.

As a result, vertical integration is emerging as a key competitive advantage. Companies are increasingly bringing multiple stages of the value chain inhouse to reduce dependency on external suppliers and improve execution. SpaceX stands as the clearest example, leveraging its launch capabilities to build out Starlink, a global broadband network that allows the company to control both deployment and service delivery.

We constructed a “Space Thematic Basket” composed of companies with meaningful exposure to the broader space economy, spanning launch, satellites, and infrastructure.

As individual sub-themes within the space economy continue to gain traction, we expect this momentum to persist, with capital increasingly rotating into the sector and driving the next phase of exponential growth.

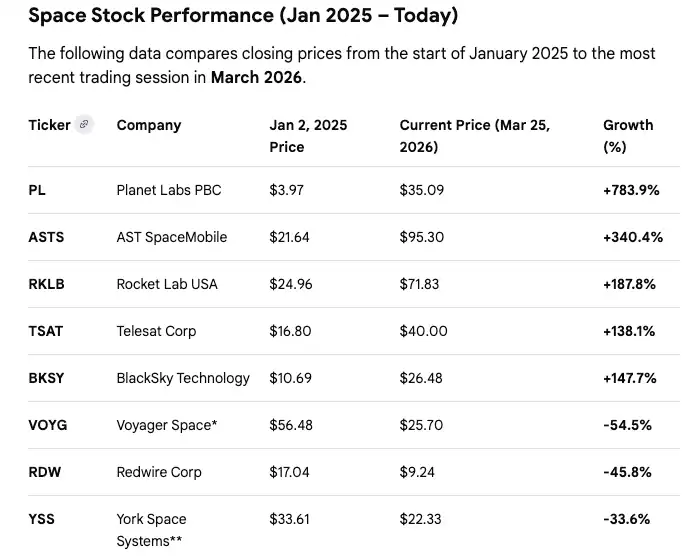

Since the start of 2026, space stocks have seen a significant re-rating, with names like Planet Labs and AST SpaceMobile surging more than threefold by late March.

This broad-based rally has been fueled by increasing investor interest in the sector, but momentum accelerated further following reports of a potential SpaceX IPO.

That development has acted as a major sentiment catalyst, lifting valuations across the space ecosystem as investors position ahead of what could be a defining event for the industry.

Narratives Driving the current trend in Space Stocks

The current momentum in space stocks is being driven by a convergence of powerful narratives that extend well beyond traditional launch economics.

One of the most compelling themes is the emergence of space-based data infrastructure, where companies focused on satellite networks and orbital hardware are attracting increased capital as Low Earth Orbit connectivity scales and the concept of in-space data centers and manufacturing becomes more viable.

At the same time, rising geopolitical tensions have elevated space into a critical defense domain.

Governments are allocating larger budgets toward space-based communication, surveillance, and navigation systems, while traditional defense contractors are increasingly partnering with or acquiring commercial space companies to strengthen their capabilities.

This alignment between defense spending and commercial innovation is creating a strong and durable demand backdrop for the sector.

Adding to the narrative, renewed focus on lunar exploration is reinforcing longterm confidence in space infrastructure buildout.

NASA recently outlined plans to invest roughly $20 billion over the next seven years to develop a moon base near the lunar south pole, complete with habitats, pressurized rovers, and nuclear power systems.

This announcement, paired with the upcoming Artemis II mission, signals that large-scale, government-backed space development is accelerating, further supporting the broader investment case for the sector.

Part 1: The Global Launch Shortage

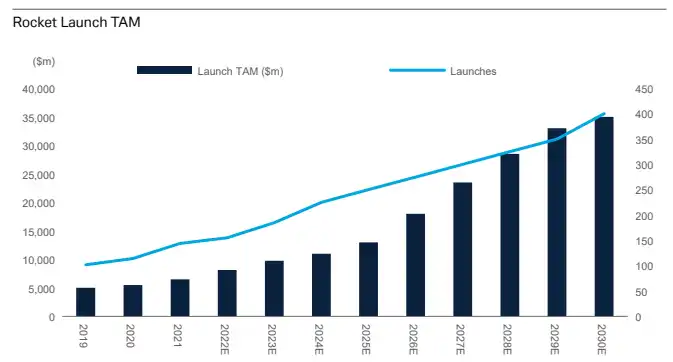

A growing imbalance between supply and demand is creating a structural bottleneck across the global launch market.

Demand for deploying satellite constellations continues to surge, led by largescale projects like Starlink & Light Speed, while available launch capacity struggles to keep pace.

SpaceX has effectively dominated the market, accounting for roughly 90% of U.S. launches in 2026, but the rest of the industry has not scaled at the same rate.

This imbalance is driving higher launch costs and extended scheduling timelines, with many satellite operators facing delays in getting payloads into orbit.

As a result, access to launch has become one of the most constrained and valuable parts of the space economy.

Current projections suggest these bottlenecks could persist through the end of the decade, reinforcing the strategic importance of launch providers and creating a favorable environment for new entrants that can successfully bring capacity online.

Key Aspects of the Launch Shortage:

The launch shortage is being driven by a combination of surging demand and structural constraints across the industry.

The rapid deployment of mega-constellations has overwhelmed existing launch capacity, creating a bottleneck where medium and heavy-lift vehicles are often fully booked well in advance.

SpaceX has emerged as the dominant provider, with Falcon 9 becoming the most reliable and widely available option, while competing platforms such as Neutron, Ariane 6, New Glenn, and Vulcan have faced repeated delays that have limited alternative capacity.

At the same time, physical infrastructure is becoming a limiting factor. Major launch sites in Florida and California are experiencing increasing congestion, effectively creating a traffic jam that leads to scheduling conflicts and delays.

This strain is not just a U.S. issue but a global one, as international players, particularly in Europe, are being forced to either wait longer for access or pay a premium to secure launch windows.

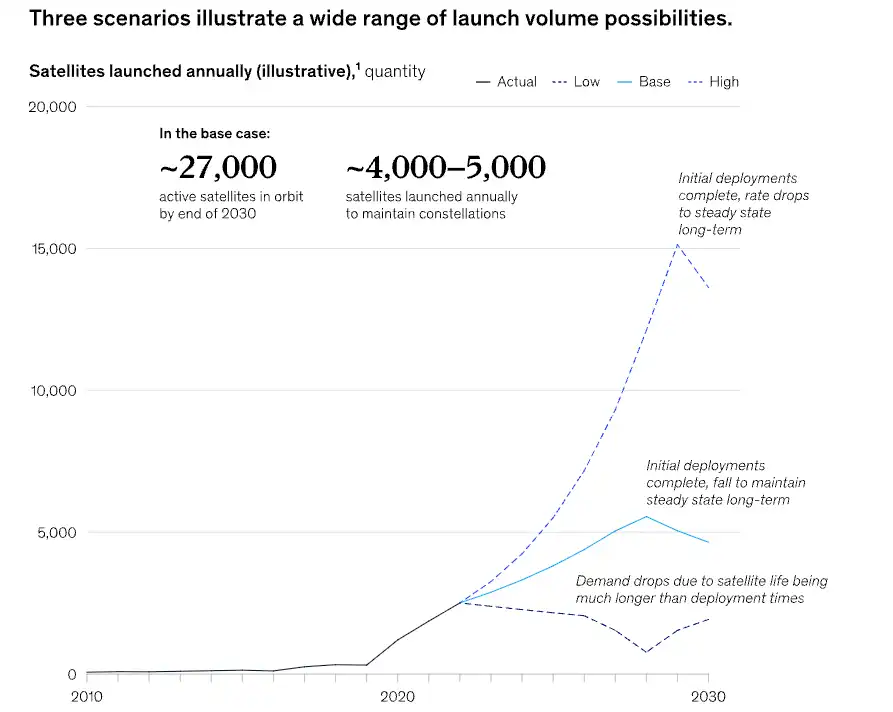

In a base-case environment, the number of active satellites in orbit is expected to reach roughly 27,000 by 2030, nearly a fourfold increase from current levels.

Maintaining that constellation size would require a steady cadence of approximately 4,000 to 5,000 satellite launches per year, creating consistent demand across the entire value chain.

The key variable, however, is how many of the planned constellations actually reach deployment.

In a high-demand scenario, where the majority of proposed projects materialize, the total number of satellites in orbit could exceed 65,000 by 2030, including a higher proportion of larger, more complex payloads.

This would require a dramatic increase in launch capacity, estimated at around 15 kilotons annually.

In contrast, a more conservative base case would require closer to 4.5 kilotons of capacity, while a low-demand scenario, defined by fewer and smaller constellations, would need less than 2 kilotons.

These scenarios also point to very different demand trajectories.

In a high-growth environment, launch demand would accelerate rapidly before stabilizing as constellations reach maturity.

In the base case, demand is expected to peak around 2028 and then level off, while in a lower-demand scenario, activity would remain relatively flat before declining slightly due to reduced replenishment needs.

Across all cases, the evolution of major players remains a central driver of overall demand dynamics.

Company: Rocket Lab Corporation

Quote: $RKLB

Bull case: Rocket Lab Corp has demonstrated significant financial growth, ending the quarter with current cash, cash equivalents, and marketable securities of $977 million, marking a 42% increase from the previous quarter and a 121% rise yearover-year. The company is experiencing strong demand for its solar arrays, resulting in improved gross margins, while also noting substantial revenue growth from its Electron launch services and anticipated expansions with the Neutron launch vehicle set for 2026. Additionally, Rocket Lab's total backlog has reached $1.1 billion, reflecting a 5% year-over-year growth, with a notable 19% increase in the next twelve months (NTM) backlog, positioning the company as a competitive alternative to dominant players in the launch services market.

Bear case: Rocket Lab Corp's Launch Services segment, which represents 26% of total sales, experienced a significant year-over-year growth of 95%; however, it faced a sequential decline of 12% due to a reduction in launches from five in the previous quarter to four, compounded by a customer cancellation. Additionally, the Space Systems backlog saw a concerning decline of 19% year-over-year, which raises concerns about future revenue and operational stability. Although the Launch backlog grew by 58% year-over-year, the overall negative trends in sequential sales and backlog reductions in one segment suggest potential vulnerabilities in Rocket Lab's financial performance and operational outlook.

Sharks Opinion:

Rocket Lab has long been a familiar name in the Sharks community we’ve tracked it through multiple earnings cycles post-exit.

The thesis mirrors what we’ve discussed for MDA and Telesat, but with a key difference: Rocket Lab is a launch provider, not a satellite operator. That makes it a direct play on space infrastructure and launch cadence, which remains critical as commercial and defense demand accelerates.

Next earnings: May 7, 2026

Near-Term Overhang:

The $1B ATM equity offering registered on March 16 caused a -9.1% move on March 18. While some see dilution risk (~1.4% of a $39B market cap), this is actually a healthy entry signal management is opportunistically raising capital at elevated prices, which is a hallmark of disciplined growth companies.

Bull Case / Re-Rating Catalysts: Neutron rocket Q4 2026 first launch a major re-rating event.

Silicon solar arrays for space data centers opening new revenue streams.

$23.9M CHIPS award validating semiconductor/space infrastructure exposure.

SpaceX IPO adjacency sector sentiment tailwind. Geopolitical + AI tailwinds the Iran conflict and defense AI spend amplify demand for launches.

Factoring in Rocket Lab’s outlook for 2026, we present two scenarios.

In the bear case, continued dilution and ongoing delays weigh on the company, setting a target of $40 per share.

The bull case assumes a flawless Neutron launch, strong sector re-rating, and positive investor sentiment ahead of the anticipated SpaceX IPO, yielding a target of $126 per share.

Description: Rocket Lab Corp is engaged in space, building rockets, and spacecraft. It provides end-to-end mission services that provide frequent and reliable access to space for civil, defense, and commercial markets. It designs and manufactures the Electron and Neutron launch vehicles and Photon satellite platform. Rocket Lab's Electron launch vehicle has delivered multiple satellites to orbit for private and public sector organizations, enabling operations in national security, scientific research, space debris mitigation, Earth observation, climate monitoring, and communications. The business operates in two segments Launch Services and Space Systems. Geographically it serves Japan, and rest of the world and earns key revenue from the United States.

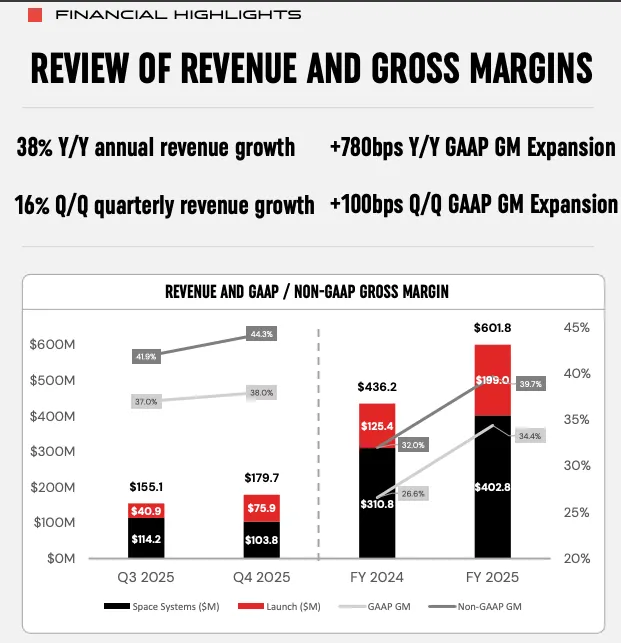

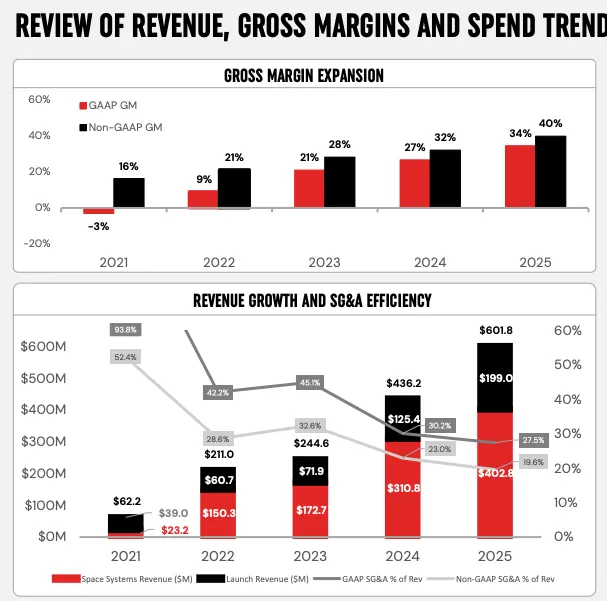

Rocket Lab delivered a strong set of results in 2025, highlighting both accelerating growth and increasing visibility into future revenue.

The company reported full-year revenue of $602 million, representing 38% year-over-year growth, while Q4 revenue reached a record $180 million, up 36% from the prior year.

Despite posting a GAAP loss of $0.09 per share in the quarter, the results reflect continued investment into scaling operations, particularly around its next-generation Neutron rocket program.

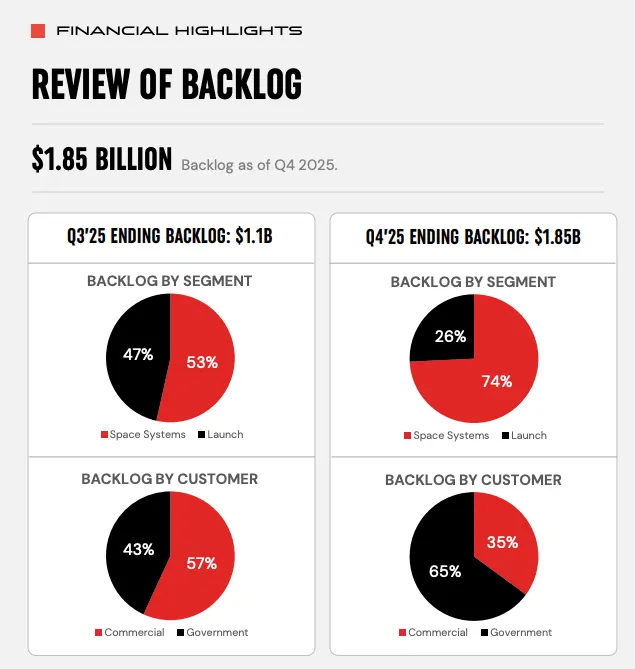

One of the most important takeaways from the report was the company’s backlog, which climbed to a record $1.85 billion. This provides a clear line of sight into future revenue and underscores the strength of demand across Rocket Lab’s space systems segment. Margins also remained solid, with Q4 gross margin coming in at 38%, demonstrating improving operational efficiency even as the company continues to invest heavily in growth initiatives.

Overall, the results reinforce Rocket Lab’s positioning as a key player in the evolving space economy, balancing near-term execution with longer-term upside tied to launch expansion and infrastructure buildout.

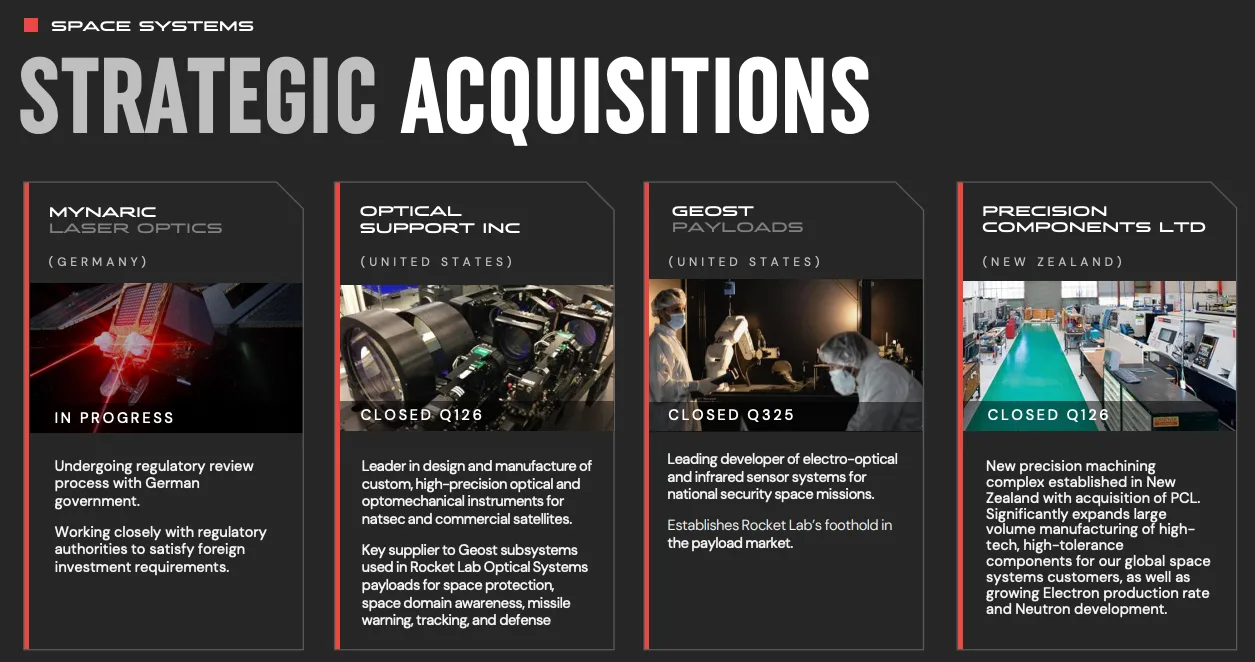

Rocket Lab has been strategically expanding its capabilities through a series of key acquisitions aimed at strengthening both its technology portfolio and geographic presence.

In 2025/2026, the company announced plans to acquire a majority stake in Mynaric, a German laser communication provider, enhancing its space-tospace communication capabilities and establishing a foothold in Europe.

Earlier, in 2025, Rocket Lab acquired GEOST, adding specialized electrooptical and infrared sensor expertise for military and government applications, including missile warning and tracking.

The company’s acquisition strategy extends back several years, including SolAero Technologies in 2022, which brought high-efficiency solar cell manufacturing in-house and bolstered spacecraft power systems.

Other notable acquisitions include Advanced Solutions in 2021, which provided Guidance, Navigation, and Control (GNC) software for spacecraft, and Sinclair Interplanetary in 2020, a specialist in small satellite hardware such as reaction wheels and star trackers.

Rocket Lab significantly strengthened its financial flexibility with a $1 billion equity raise in March 2026, providing capital for future strategic acquisitions and scaling Neutron rocket production.

Rocket Lab entered 2026 with a robust backlog and accelerating contract activity, highlighting both commercial and defense demand.

As of late March 2026, total backlog surpassed $2 billion, fueled by major engagements across multiple segments.

Notable contracts include an $816 million deal with the Space Development Agency (SDA) for 18 satellites and a $190 million, 20-flight HASTE hypersonic test program.

Growth momentum remains strong, with 28 new launches signed in Q1 2026 alone nearly matching the total sold throughout 2025.

The backlog spans Electron launch services and the expanding Space Systems segment, which covers satellite components and manufacturing.

While the Neutron medium-lift rocket has been delayed to Q4 2026, the existing contract portfolio ensures solid financial visibility and positions Rocket Lab for continued expansion.

Rocket Lab is advancing the Neutron medium-lift rocket program, aiming for a maiden flight in late 2026 or early 2027.

The company is actively conducting qualification tests on critical structural components, including the interstage and the “Hungry Hippo” fairings, while scaling production of the 3D-printed Archimedes engines. Launch Complex 3 at Wallops Island is fully prepared to support Neutron operations.

Key developments include ongoing high-power testing of Archimedes engines with a 3–4 hot fire cadence daily, completion of qualification for the “Hungry Hippo” fairings, and continued interstage testing, including a standard test-tofailure tank rupture.

The launchpad itself features a 9-meter mount, water deluge system, and propellant infrastructure. Rocket Lab is also preparing a 400-ft recovery barge, “Return on Investment,” for early splashdown operations, with full return-tolaunch-site capability planned for future missions.

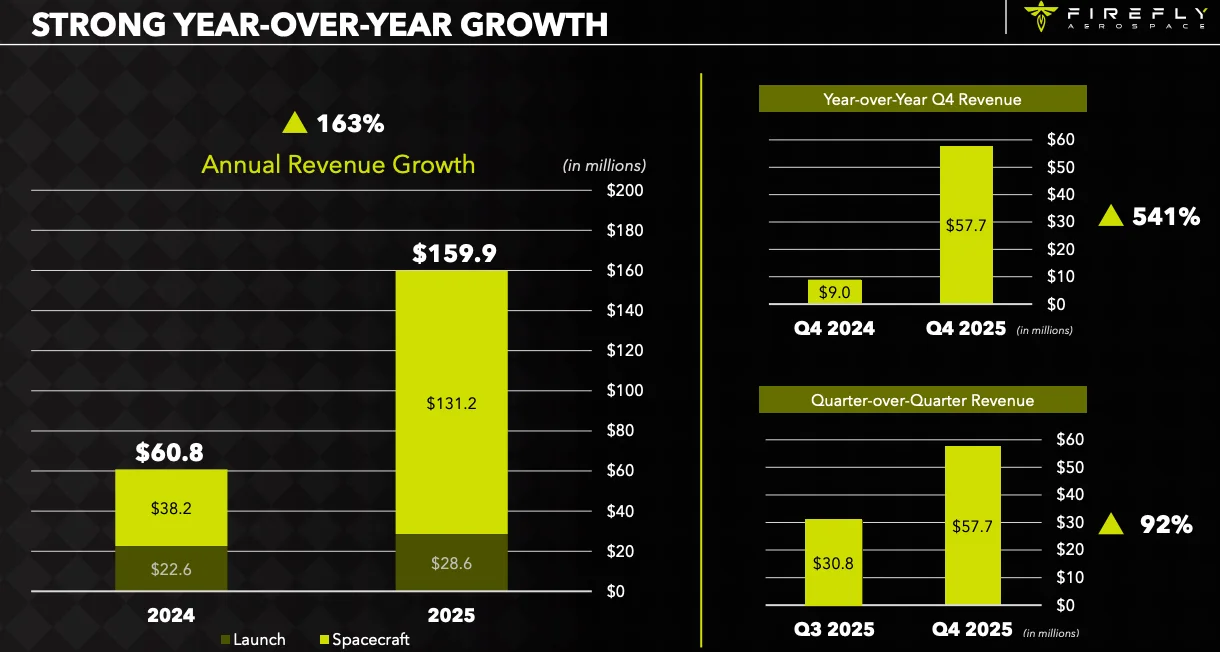

Company: Firefly Aerospace Inc

Quote: $FLY Bull case: Firefly Aerospace represents a highrisk, high-reward opportunity. The company has demonstrated technical capabilities that few competitors match, positioning it as a potential leader in a strategically critical and rapidly expanding sector. That said, substantial financial, operational, and governance challenges remain. Investment decisions depend heavily on confidence in the management team’s ability to resolve the current Alpha vehicle grounding, successfully transition to the Eclipse rocket, and scale operations efficiently enough to reach profitability before capital resources are depleted.

Bear case: Conversely, the bear case is equally formidable and rooted in the Company's financial and operational realities. Firefly is consuming capital at an alarming rate, posting a net loss of $231.1 million in 2024 on revenues of just $60.8 million, with a negative free cash flow of $190.3 million for the same period. A clear path to profitability remains distant and is heavily contingent on the flawless and timely execution of its next-generation platforms, particularly Eclipse. This operational risk was starkly highlighted by the April 29, 2025, anomaly during an Alpha mission, which has resulted in the grounding of its primary revenue-generating vehicle pending an FAA investigation. This event not only halts a key revenue stream but also introduces significant uncertainty into the Company's launch cadence and customer confidence.

Sharks Opinion:

Considering the ongoing global launch shortage, Firefly has a potential opportunity to establish itself as a meaningful player in the space sector.

Currently, the stock trades at a reasonable level relative to its IPO, but much of the upside premium reflects expectations that the company will achieve orbit in the near term.

The primary investor concern is whether delays or competition could prevent this milestone if Firefly fails to reach orbit before rivals, the premium could erode.

That said, the company does generate revenue from other parts of the space supply chain, giving it intrinsic value beyond its launch ambitions.

We outline two scenarios with corresponding price targets. In the bearish case, reflecting an inconsistent launch system and operational hurdles, the equity is valued between $8 and $15.

In the bullish case, assuming successful competition with Rocket Lab and SpaceX and a proven launch capability, the upside is substantial, with a potential return to its IPO price of $75.

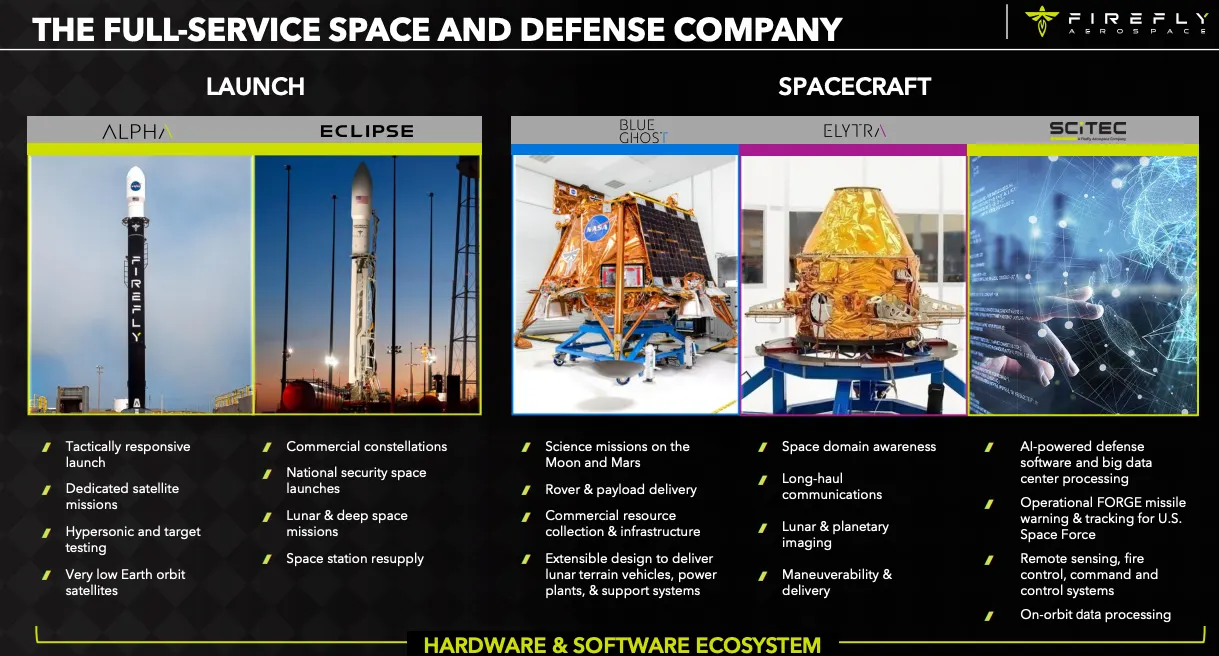

Description: Firefly Aerospace Inc is a space and defense technology company with an established track record of success providing comprehensive mission solutions to national security, government, and commercial customers. The company enables government and commercial customers to launch, land and operate in space

Firefly’s competitive edge stems from its full vertical integration and “end-to-end” operational model, distinguishing it from companies that specialize in only one segment of the space value chain launch vehicles, satellites, or ground systems.

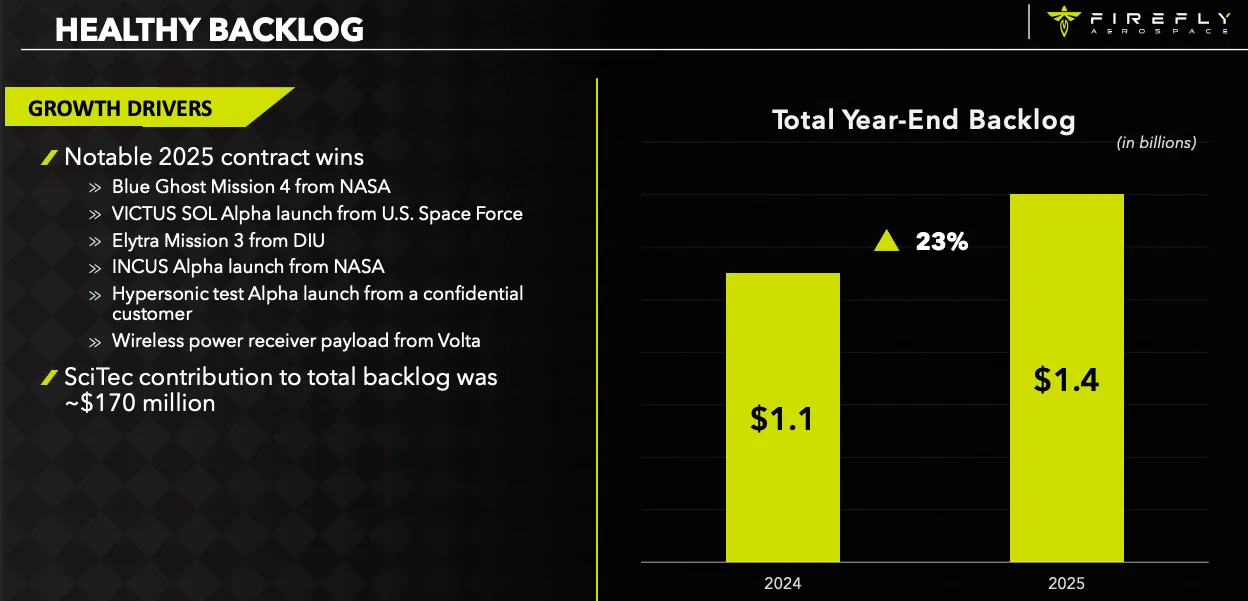

The acquisition of SciTec further strengthens this integrated capability, signaling the company’s evolution toward a mature, strategically robust player.

Firefly’s offerings are organized into two core segments Launch Solutions and Spacecraft Solutions each supported by operational products and nextgeneration platforms.

Launch Vehicles (Alpha & Eclipse)

Alpha: Firefly’s current small-to-medium lift launch vehicle, uniquely the only U.S.-based orbital rocket in the 1,000-kg payload class to have successfully reached orbit.

It can deliver up to 1,030 kg to LEO and 630 kg to SSO, with six flights completed by March 2025, four of which were successful. Alpha anchors the company’s existing launch business.

Eclipse: Designed as the future growth engine, Eclipse is a medium-lift, partially reusable rocket being developed in partnership with Northrop Grumman.

Its reusability is key to achieving long-term cost competitiveness.

Spacecraft Solutions (Blue Ghost & Elytra)

Blue Ghost: Firefly’s lunar lander, which made history on March 2, 2025, completing the first successful commercial Moon landing and the first U.S. lunar surface mission since Apollo 17. Multiple future CLPS program missions are already under contract.

Elytra: A versatile orbital “space tug” built on Blue Ghost technology, capable of satellite delivery, on-orbit transfers, hosted payloads, and communications relay, providing a broad suite of in-space services for commercial and government clients.

Financially, Firefly has demonstrated significant momentum.

Full-year 2025 revenue surged 163% to nearly $160 million, driven by successful launch operations and high-margin software contributions from SciTec.

Looking ahead, the company’s 2026 guidance points to another exponential leap, with projected revenues of $420 million to $450 million approximately 80% of which is already secured through long-term contracts, providing strong visibility into future performance.

Part 2: Satellite Communications & Imagery

Satellites remain the backbone of the modern space economy, serving as essential infrastructure for global communications and data transmission. Investing in satellite companies provides direct exposure to the commercialization of space, spanning consumer telecommunications, government communications contracts, and defense applications sectors poised for significant growth over the next decade. The integration of satellites with terrestrial telecom networks accelerated in 2025, highlighted by major carriers like T-Mobile and Verizon launching directto-device services, alongside Apple entering the space-enabled connectivity arena, underscoring the expanding convergence between satellite and consumer technology markets.

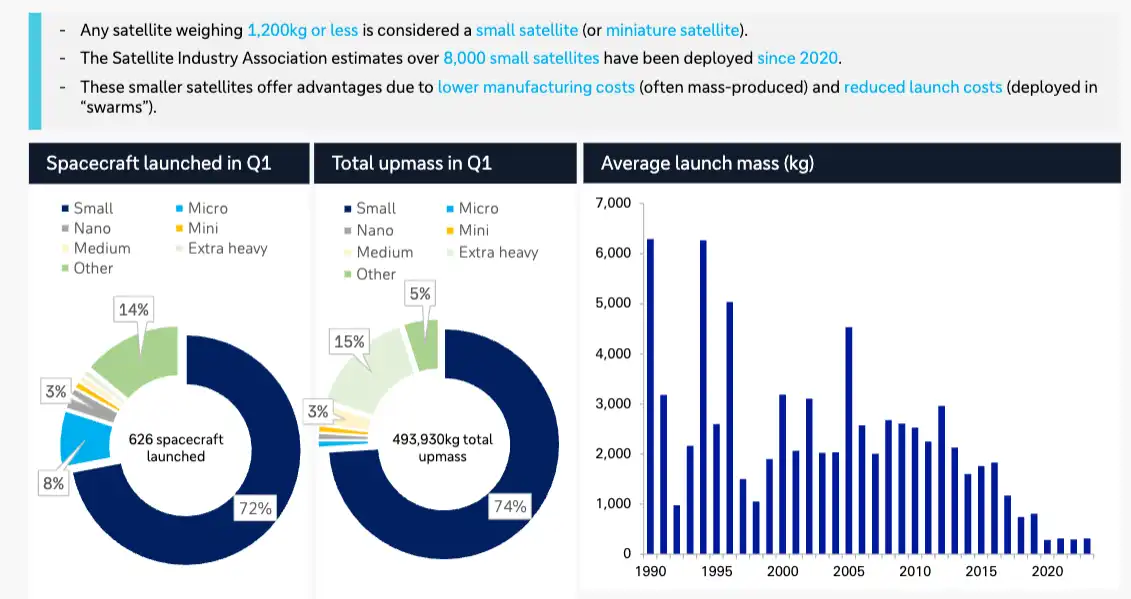

As the skies grow increasingly crowded, satellites are getting smaller and more capable.

This trend is driven by rapid technological advancements that have enhanced the functionality of SmallSats.

Defined by NASA as satellites weighing less than 180 kg and roughly the size of a large kitchen refrigerator, SmallSats are far more cost-effective than traditional large satellites.

Their reliance on commercially available components allows for mass production, making space access feasible for a wider range of organizations. The impact is clear: global SmallSat launches have surged, growing at a CAGR of 44.9% from just 39 launches in 2011 to 2,304 in 2022, according to Statista.

Company: AST SpaceMobile

Quote: $ASTS

Bull case: AST SpaceMobile Inc. is wellpositioned to strengthen its financial footing, with cash projected to reach $3.7 billion by Q1 2026, supported by the issuance of 2.25% senior unsecured notes and a highly integrated satellite manufacturing process covering 95% of production. The company stands to benefit from the growing direct-to-cell market, with anticipated revenue from international mobile network operator (MNO) agreements and the rollout of its SpaceMobile Service. Successful satellite launches in 2026 are expected to reinforce confidence in AST’s advanced technology, potentially driving positive EBITDA and positioning the company for an enterprise value near $38 billion by the end of fiscal year 2026.

Bear case: AST SpaceMobile faces considerable headwinds, having lost over half its market value in a short period, reflecting execution risks and market volatility. Dependence on third-party launch vehicles introduces potential delays and cost uncertainties that could impact operations and profitability. The company is also expected to incur significant future expenses to execute its growth strategy, and its ability to secure sufficient funding while managing costs remains uncertain, creating a challenging outlook.

Sharks Opinion: ASTS wasn’t initially a favorite when it first listed we preferred TSAT at the time but it has since become one of the top-performing space stocks.

While we still view it as overvalued, the company’s recent wins across various segments highlight a strong trajectory for future growth. That said, assigning a meaningful price target is extremely challenging.

ASTS trades at an extraordinary price-to-sales ratio of 346x, with $54 million in revenue and a net loss of $74 million, yet commands a market capitalization approaching $30 billion.

The valuation disconnect makes it nearly impossible to establish a realistic target.

Description: AST SpaceMobile Inc is currently designing, developing and manufacturing the constellation of BlueBird (BB) satellites and has begun launching its planned space-based Cellular Broadband network distributed through a constellation of low Earth orbit (LEO) satellites. The company is building a cellular broadband network in space to operate directly with standard, unmodified mobile devices, and off-the-shelf mobile phones based on extensive IP and patent portfolio. It has focused on eliminating the connectivity gaps faced by mobile subscribers. The Company's spaceMobile Service is being designed to provide cost-effective, high-speed Cellular Broadband services to end-users who are out of terrestrial cellular coverage using existing mobile devices.

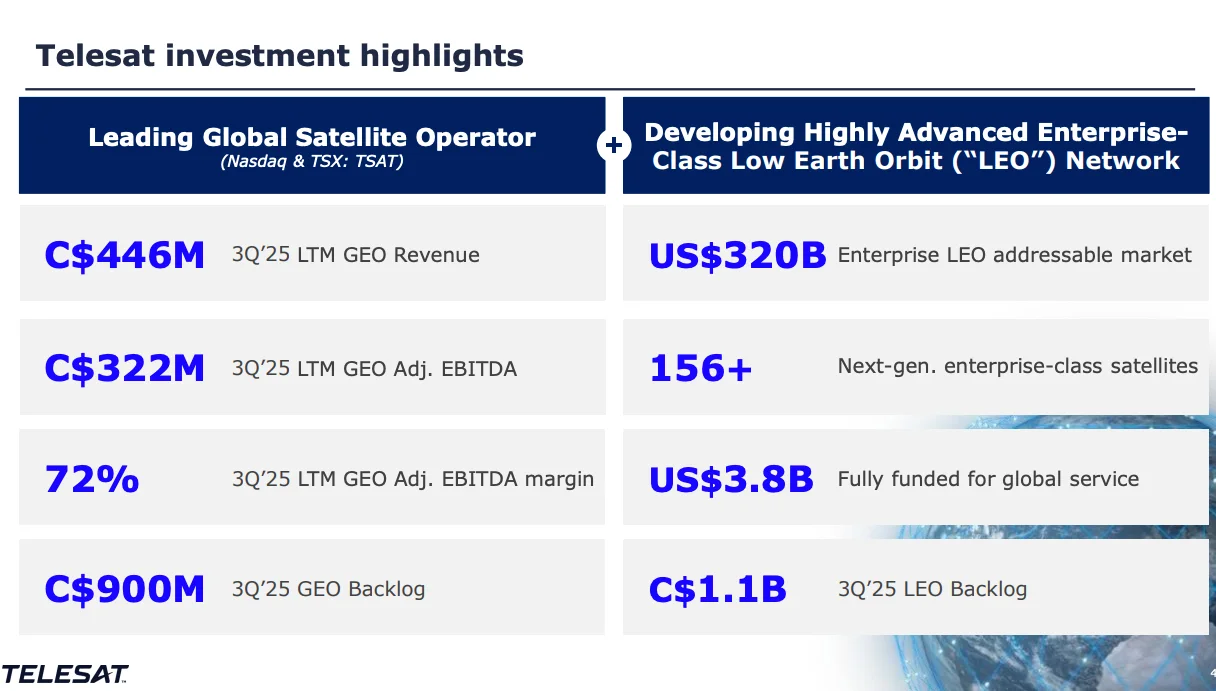

Company: Telesat Corporation

Quote: $TSAT

BT: $28-$32

ST: $60+ (2028 Target)

Sharks Opinion: The thesis for Telesat mirrors a lot of what we’ve highlighted for MDA: a Canadian satellite operator with a strong position in the space ecosystem and familiarity from prior trades that delivered solid returns.

The broader space sector appears primed for a rerating, especially with the looming SpaceX IPO bringing renewed investor focus.

That said, Telesat presents a slightly different risk/reward profile. Their main next-generation product isn’t expected to go live for another year, meaning revenue catalysts are still off in the distance.

Meanwhile, the company is actively rebalancing its balance sheet and managing a substantial debt load a factor that is currently compressing profit margins and could pressure near-term earnings.

Given these dynamics, we anticipate a potential pullback before the market fully factors in Telesat’s long-term story.

That correction could create a high-asymmetry entry point, allowing investors to position ahead of both product ramp-up and a broader sector rerating once debt metrics improve and growth begins to materialize.

In short, Telesat combines a familiar sector thesis with a near-term tactical setup: the stock may dip before it climbs, offering a disciplined, opportunitydriven entry.

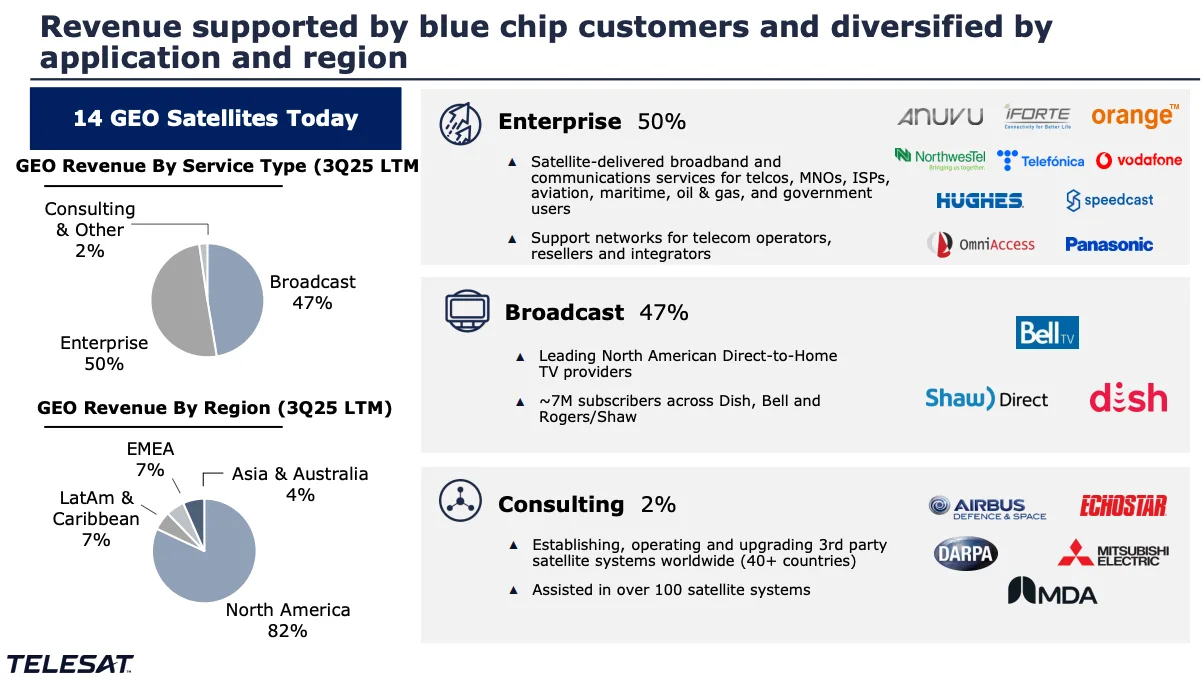

Description: Telesat Corp is a satellite operator, that provides its customers with mission-critical communications services. It operates in a single operating segment, in which it provides satellitebased services to its broadcast, enterprise, and consulting customers around the world. Geographically, it derives a majority of its revenue from Canada. It derives revenue from Broadcast, Enterprise, Consulting, and others.

Telesat faced a challenging 2025, reporting total revenue of $418 million, down 27% from $571 million in 2024, with Q4 revenue at $67.5 million.

The company posted a net loss of $111.2 million for the year, while adjusted EBITDA fell 45% year-over-year to $213 million.

Revenue Drivers & Trends:

Legacy GEO Decline: The Geostationary (GEO) business faced structural pressure. North American Direct-to-Home (DTH) customers reduced capacity and rates, while rural broadband demand softened, driving the revenue contraction.

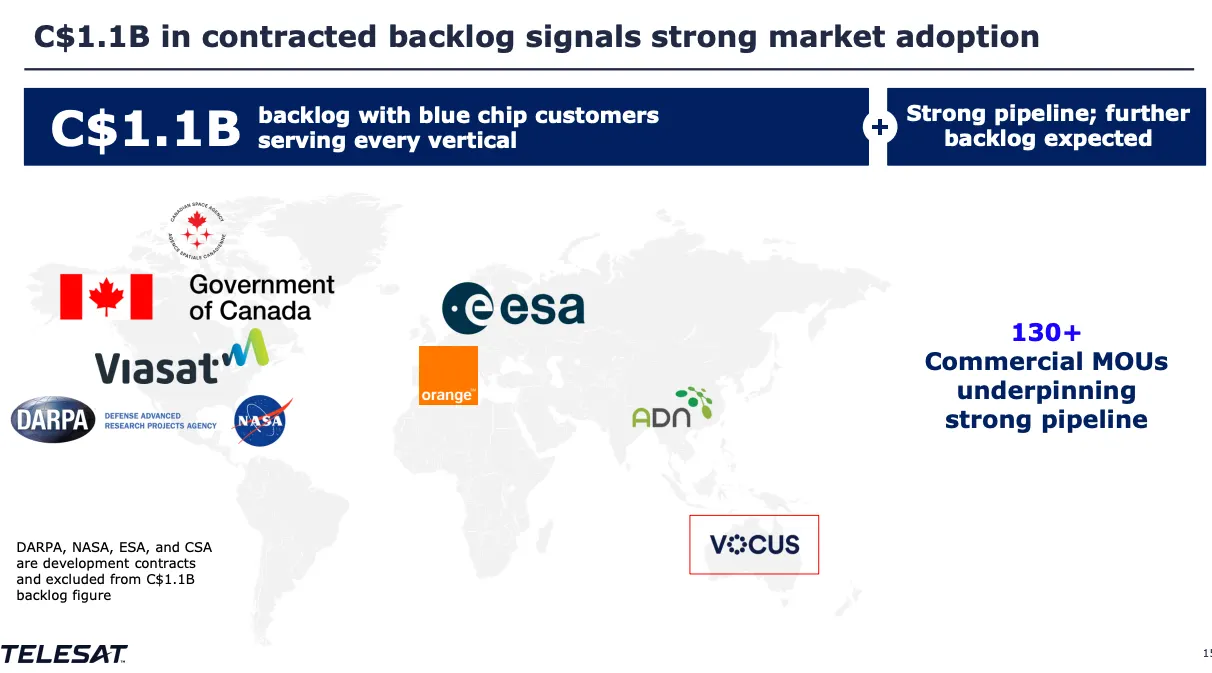

Backlog: Despite near-term revenue pressure, Telesat ended 2025 with ~$1.0 billion in LEO backlog and $800 million in GEO backlog, providing a solid runway for future growth as the LEO constellation ramps.

2026 Outlook:

For the legacy GEO unit, management expects revenue of $300–$320 million in 2026. The LEO segment will be the key driver of upside, but near-term earnings and margin pressure could create volatility before the ramp is fully realized.

Telesat’s 27% revenue decline in 2025 stemmed from structural shifts across its core service lines:

Broadcast / Direct-to-Home (DTH): Still a foundational revenue source, this segment faced significant headwinds. Lower renewal rates and reduced capacity requirements from major North American providers drove roughly half of the year’s total revenue decline.

Enterprise & Government Services:

Revenue slipped due to softer demand in rural broadband markets, particularly from international projects such as Indonesia’s rural broadband program.

Consulting & Other:

A smaller segment, including LEO-related consulting services, also experienced modest declines, reflecting the longer ramp timeline for Lightspeed adoption.

Key Customers & Market Segments:

Major Video Clients: DTH providers remain critical, but ongoing pricing pressure emphasizes the limitations of legacy GEO revenue.

Government & Military: This is where the growth thesis shifts. Telesat is actively targeting the sovereign defense market, recently securing a contract with the U.S. Department of War and allocating 25% of Lightspeed capacity to dedicated Military Ka-band spectrum positioning the company for highermargin, mission-critical applications.

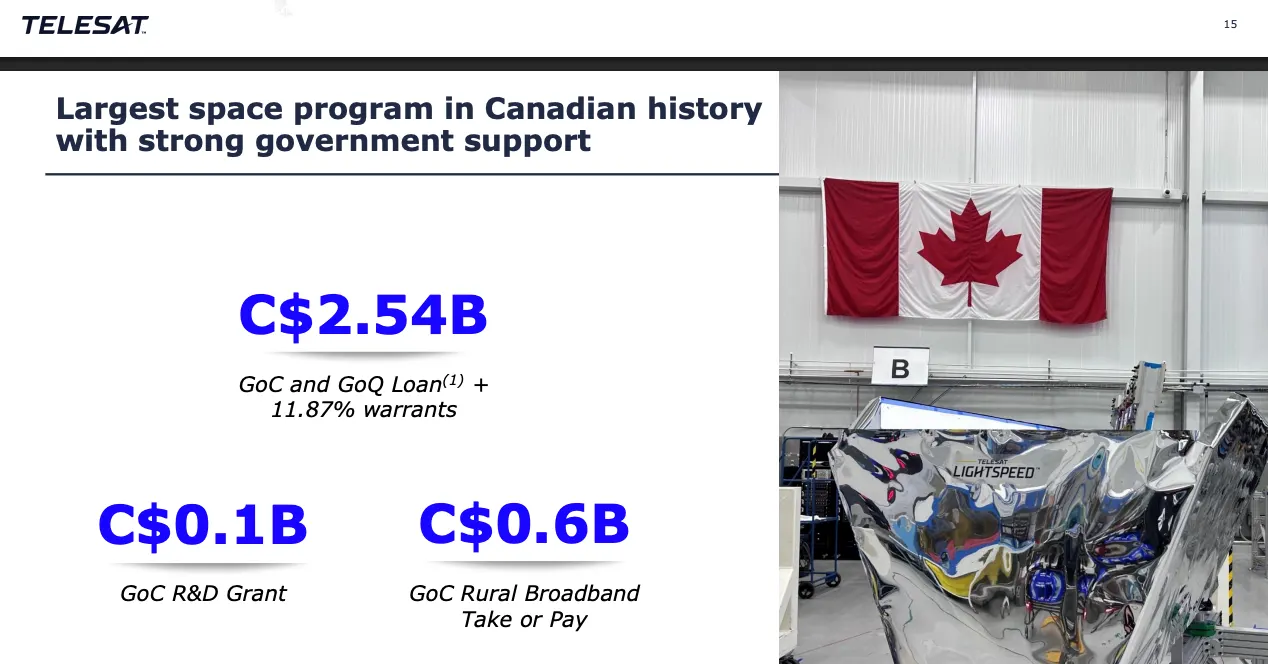

Telesat’s growth and LEO deployment are being heavily supported by major government funding packages, providing both capital and strategic validation for the Lightspeed program.

Government of Canada:

Loan: $2.14 billion repayable loan, managed through the Canada Development Investment Corporation (CDEV).

Terms: 15-year maturity with a floating rate of 4.75% above CORRA. Equity: The federal government received warrants for 10% of Telesat LEO Inc. common shares, aligning public support with long-term upside potential.

Government of Québec: Loan: $400 million, structured with terms mirroring the federal agreement. Equity: Québec received warrants for 1.87% of the Lightspeed business, ensuring regional participation in the project’s upside.

Previous Commitments:

A 10-year, $600 million agreement from 2020 pre-purchased LEO capacity for subsidized broadband in rural and remote communities.

Company: MDA Space Ltd.

Quote: $MDA

BT: $18-$21

ST: $44

Sharks Opinion:

MDA Space is a name we know well it’s the former parent of one of our Stock Sharks favorites, Maxar Technologies. Recently uplisting to the Nasdaq, MDA is benefiting from a broader revival in the space sector, and the timing is compelling.

We consider MDA one of the premier space companies a core holding in a space-focused portfolio but only at the right entry point. Based on our experience, fair value sits somewhere in the $20s. Once the shares correct into that zone, we’ll be ready to act.

MDA occupies a unique middle ground in the space ecosystem. On one end, you have megaplayers like Boeing, SpaceX, and Airbus; on the other, high-risk, often unprofitable “new space” names. MDA bridges the gap a profitable, established company with 55 years of experience, 3,000+ employees, and a track record of delivering cutting-edge technologies.

It’s a rare combination of stability and innovation in a sector that is otherwise heavily skewed toward volatility.

With the SpaceX IPO on the horizon, we anticipate renewed investor attention and a potential rerating across the space sector.

MDA, as a critical infrastructure and technology provider within that ecosystem, is well-positioned to benefit from that rotation. When the broader space narrative accelerates, MDA could move higher not just on fundamentals, but on sector momentum.

Description: MDA Space Ltd is a developer and manufacturer of technology and services to the space industry. It is an international space mission partner and robotics, satellite systems, and geointelligence pioneer. It is engaged in communications satellites, Earth and space observation, space exploration, and infrastructure. The Company collaborates and partners with governments and space agencies, commercial space companies, and defence and aerospace prime contractors in the space industry. Geographically, it generates the majority of its revenue from Canada.

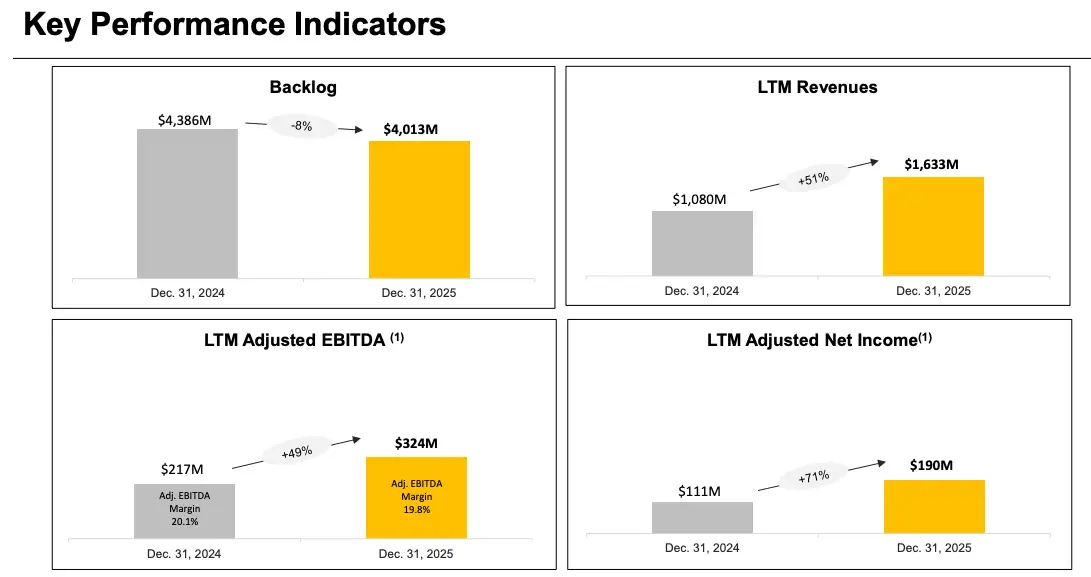

MDA Space has been publicly traded on the Toronto Stock Exchange since April 2021, and 2025 was a milestone year.

The company reported record revenue of $1.63 billion, up 51.2% year-overyear, fueled primarily by strong growth in its satellite systems business.

The estimated $300 million raised strengthens the balance sheet and provides flexibility for growth initiatives, including potential acquisitions or other strategic investments.

MDA operates through three complementary divisions:

Robotics & Space Operations (32% of revenues): Focused on space robotics, on-orbit servicing, assembly, and exploration missions, including rovers.

Satellite Systems (44% of revenues): The largest segment, producing LEO, MEO, and GEO satellites along with critical subsystems such as antennas, payloads, and specialized electronics.

Geointelligence (22% of revenues): Provides earth observation, ground station services, and geospatial analytics.

MDA Space had a standout year in 2025, reporting total revenue of $1.63 billion CAD, up 51.2% year-over-year, and adjusted EBITDA of $323.9 million, a 49.2% increase.

The company’s backlog sits at $4.0 billion, reflecting strong forward visibility across its satellite and defense programs.

Revenue by Division:

Satellite Systems:

$1.11 billion (+85.5%)

Robotics & Space Operations: $309.3 million

Geointelligence: $214.4 million

Recent Performance & Drivers: Q4 2025 revenue came in at $499.1 million, a 44% jump from the prior year, reflecting increased activity on large LEO constellations like Telesat Lightspeed and Globalstar, alongside defense contracts.

The broader takeaway: MDA’s growth continues to be heavily anchored in satellite manufacturing, a sector with high technical barriers, recurring defense demand, and strategic importance in the space economy.

Company: Planet Labs PBC

Quote: $PL

Bull case: Planet Labs PBC has demonstrated strong financial momentum, with total remaining performance obligations (RPO) soaring 371% year-over-year to $672 million and current RPO (cRPO) rising 86% to $222 million, driven largely by successful contracts in Japan and Germany. Cash reserves ended F3Q26 at $678 million, up sharply from $278 million the previous quarter, reflecting solid operational execution and financial stability. Total revenue reached $81.3 million, a 33% increase year-over-year, exceeding guidance and analyst expectations, with the Defense and Intelligence segment surging 72%, highlighting growing global demand for the company’s Earthimaging solutions.

Bear case: Despite strong year-over-year growth in RPO and total backlog, Planet Labs saw sequential declines in both metrics, signaling potential softness in the commercial segment and a shift toward larger accounts. Free cash flow fell dramatically to $0.9 million from $46.3 million previously, underscoring challenges in converting revenue into cash amid ongoing capital expenditures. Additionally, longer sales cycles and slowing customer growth suggest market hesitation toward geospatial data in new verticals, which could limit future product expansion and revenue potential.

Sharks Opinion: Planet Labs has been the standout performer in the space sector over the past two years, capitalizing on both the AI and space-based data center narratives credit where it’s due.

That said, the stock trades at a significant premium, around 35x price-to-sales.

Narrative-driven stocks can only sustain momentum for so long, and while we see nearterm upside potential, a long-term correction seems likely unless Planet Labs can rapidly grow into its lofty valuation.

Description: Planet Labs PBC is an Earthimaging company. It uses space to help life on Earth by imaging the world every day and making change visible, accessible, and actionable. Its platform includes imagery, insights, and machine learning that empower companies, governments, and communities around the world to make timely decisions about the evolving world. Its solutions are Broad Area Management. Its products are Planet Monitoring, Planet Tasking, Planet Analytic Feeds, Planetary Variables, Planet Basemaps, Planet Insights, and Platform Pricing. The group provides solutions to the Agriculture Science Program, Energy & Infrastructure, Forestry & Land Use, Mapping, Sustainability, Maritime, Civil Government, U.S. State and Local, Europe, Planet Federal, Defense & Intelligence, and Armed Services.

Planet Labs capped FY2026 with strong top-line growth and operational progress.

Fourth-quarter revenue surged 41% year-over-year to a record $86.8 million, contributing to full-year revenue of $307.7 million, up 26% from FY2025.

Recurring annual contract value (ACV) remained exceptionally high at 98%, reflecting the company’s transition to a subscription-driven model.

Gross margins moderated slightly, with Q4 GAAP at 54% (vs. 62% in Q4 FY2025) and non-GAAP at 57% (vs. 65% prior year),

Backlog expanded sharply to $900.4 million, up 79% year-over-year, providing significant revenue visibility. Defense revenue grew 50% year-over-year, fueled by geopolitical tensions and increasing sovereign satellite demand.

Planet Labs has successfully pivoted from a capital-intensive satellite manufacturer to a high-margin, recurring revenue data platform.

Part 3: Space Infrastructure & New Listings

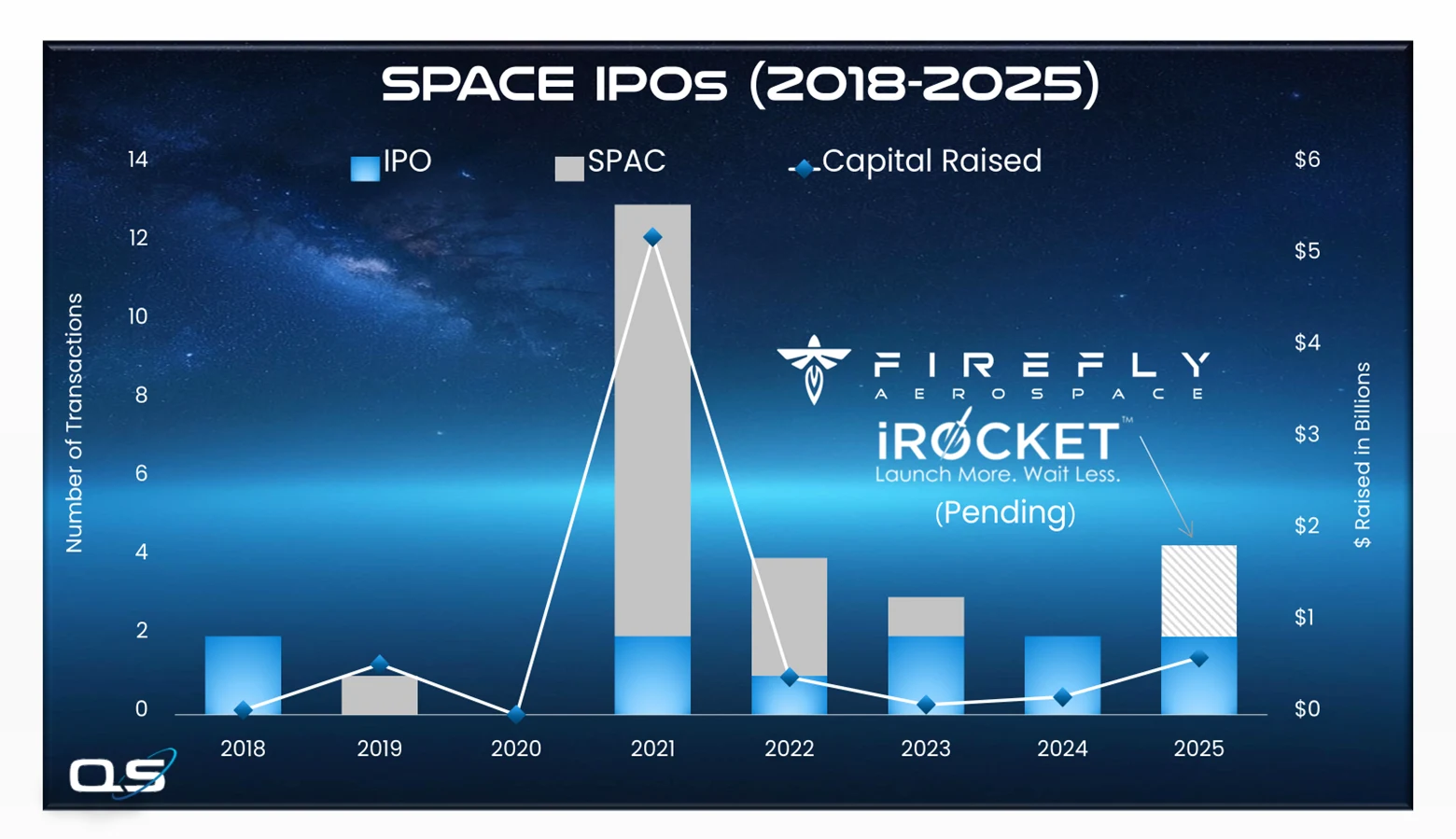

Following the 2021 SPAC surge, the space sector underwent a reality check, as many companies faced heightened scrutiny over long-term sustainability and capital efficiency. In response, the market shifted back toward traditional fundraising approaches.

Investment banks are increasingly structuring private placements, convertible debt offerings, and milestone-based financing to better balance risk and return for investors.

Meanwhile, sovereign wealth funds, infrastructure investors, and strategic corporate partners have become more active, frequently collaborating with banks on syndicated deals or joint ventures.

These customized financial structures are enabling space companies to secure the capital necessary to scale operations while addressing investor concerns about risk management.

Company: York Space Systems

Quote: $YSS

Bull case: York Space Systems Inc. is wellpositioned within the expanding space and defense sector, supported by an anticipated 11.3% increase in the USSF’s PWSA Transport Layer budget and a projected 32% growth in the SDA budget through 2029. The company’s historical revenue growth of roughly 27% CAGR since 2023, combined with expectations of over 50% yearover-year growth in fiscal 2025 and a sustained pace through fiscal 2027, underscores its robust growth trajectory. Investments in advanced testing infrastructure are enhancing production efficiency, which should support strong future revenue as demand for small satellite launches continues at an estimated 20% CAGR.

Bear case: York Space Systems faces headwinds due to a roughly 32% decline in backlog over the past two years, signaling potential future revenue challenges. Contribution margins have deteriorated from 38% in FY23 to an estimated 30% in FY24, with FY25 projections around 32%, largely driven by unfavorable EAC adjustments. Coupled with Defense Department budget constraints such as an 11% reduction in SDA funding for FY25 and a slowdown in the satellite launch industry, these factors increase operational risk and competitive pressure, casting uncertainty over the company’s growth outlook.

Sharks Opinion: York Space Systems is a compelling pick for investors who believe in the space vision of AE Industrial Partners. Due diligence is critical, as AE Industrial Partners (AEI), a private equity firm focused on aerospace and defense, remains the largest shareholder and retains significant voting control after acquiring a 51% stake in 2022. Investment in this stock hinges on confidence in AEI’s strategic direction and influence over York’s operations.

Description: York Space Systems Inc is a U.S.- based space and defense company that provides mission-related solutions for national security, government, and commercial customers. The company develops its own hardware and software, offering capabilities intended to support customer requirements across various elements of the space mission lifecycle. It offers mission solutions across several complementary product categories: Components, Subsystems, Spacecraft Platforms, Ground Operation, Global Downlink, and Software-Enabled Services. The company derives the majority of revenue from long-term firm-fixedprice (FFP) production contracts for the design of small satellites, launch services, and ground services with both U.S. federal governmentcontrolled agencies as well as domestic commercial customers.

Top DoD Provider: York Space Systems is recognized as the leading provider to the U.S. Department of Defense’s Proliferated Warfighter Space Architecture (PWSA) based on the number of operational spacecraft.

Space & Defense Prime: Distinguishing itself from many startups that function as subcontractors, York operates as a prime contractor, delivering end-to-end mission solutions for national security, government, and commercial clients.

Full-Year 2025 Financial Summary: York reported revenue of $386.2 million, a 52% increase from $253.5 million in 2024.

The company narrowed its net loss to $84.5 million ($0.89 per share), improving from a $98.9 million loss the prior year.

Gross profit surged 133% year-over-year to $75.5 million, pushing gross margin up to 19.5% from 12.7% in 2024. Adjusted EBITDA improved dramatically, with a loss of $8.3 million compared to a $43 million loss in 2024.

2026 Outlook & Liquidity: York expects 2026 revenue in the range of $545 million to $595 million. With a year-end backlog of $543 million, the company anticipates that over 70% of next year’s revenue will be covered, providing strong visibility and support for continued growth.

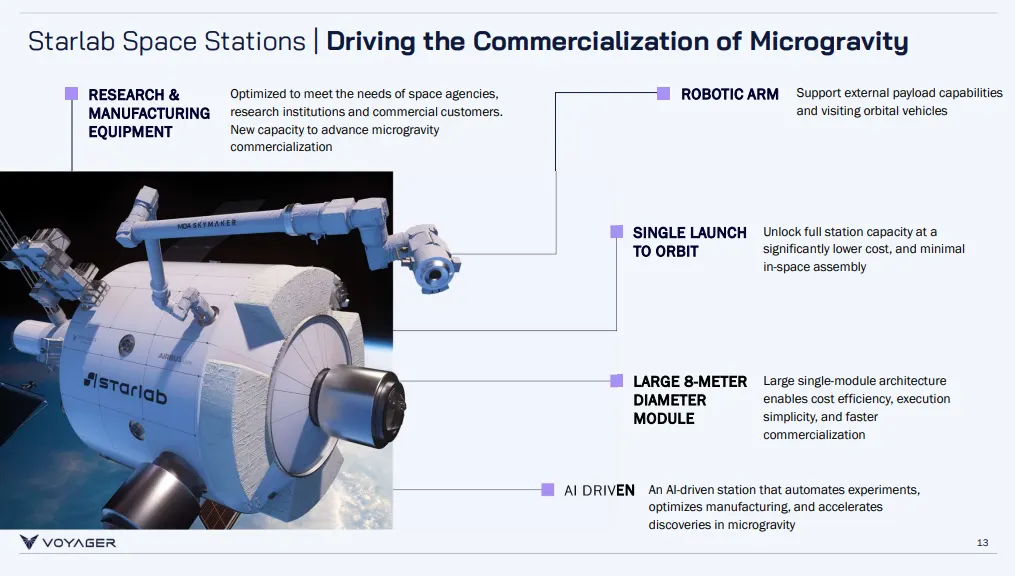

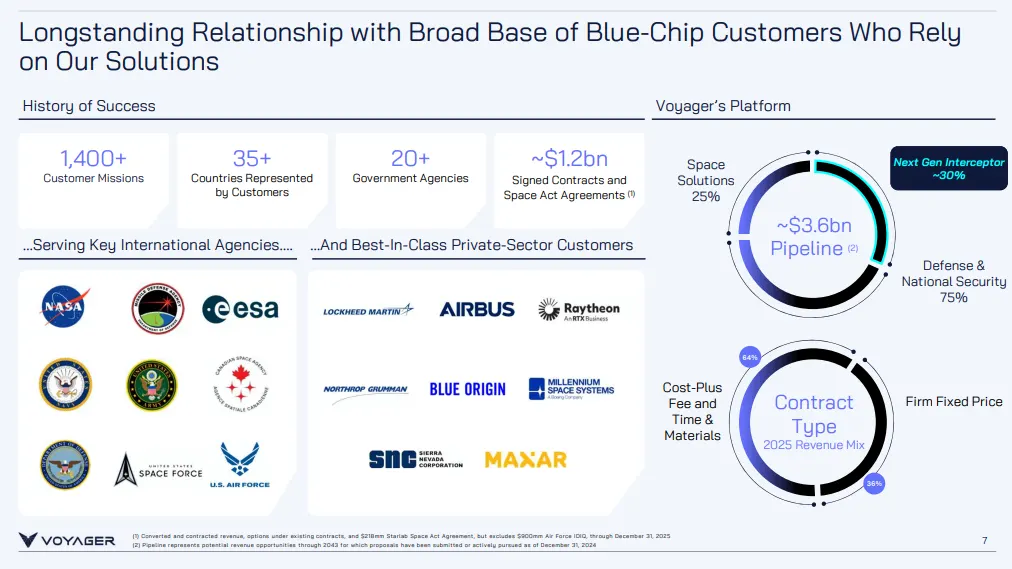

Company: Voyager Technologies

Quote: $VOYG

Bull case: Voyager Technologies is wellpositioned for meaningful revenue expansion, fueled by rising demand across its defense and space solutions divisions. The microgravity market, projected to grow at a 10% CAGR, supports the company’s forecast of reaching approximately $4 billion in annualized revenue as the Starlab project advances toward completion. Transitioning from a NASA services contract is expected to further accelerate top-line growth, with potential revenue gains exceeding 50% by FY27, driven by combined government and commercial sector demand.

Bear case: Voyager Technologies faces notable headwinds that temper optimism. Revenue from space solutions is currently negative due to the expiration of a low-margin NASA services contract.

Delays in the Starlab launch could require the company to reduce its equity stake to secure additional funding, limiting revenue growth and profitability.

Furthermore, the reliance on debt and equity financing to reach its $900 million target raises dilution concerns and casts uncertainty on the conversion of its substantial backlog into actual revenue, potentially postponing profitability well into the future.

Sharks Opinion: Voyager operates as a “space + defense tech” roll-up, aiming to provide immediate value to the Pentagon while also capturing a piece of the commercial LEO infrastructure market in the future.

Its focus spans defense and national security programs including missile defense space systems and services, and the ambitious Starlab project, a planned commercial space station targeting late-decade deployment.

Valuation is reasonable, but the company lacks standout differentiation to command a long-term premium. It’s more of a “trade around catalysts” type name than a stock to hold for the long term.

Description: Voyager Technologies Inc is a defense and space technology company committed to advancing and delivering transformative, mission-critical solutions. It operates across three primary divisions namely Defense and National Security, Space Solutions and Starlab Space Stations.

Revenue is trending up, but Voyager is far from being a mature cashgenerating machine.

The main challenge is that the company remains unprofitable and continues to spend heavily on R&D, particularly with Starlab in the mix.

In practical terms:

Near term cash burn is high, and execution is critical.

Long term – if scale and contracts materialize, margins could improve rapidly, especially given the high-quality nature of defense work once fully ramped.

The balance sheet and liquidity profile are healthier than many peers thanks to recent capital raises and structured financing. This provides runway but doesn’t eliminate the risk of dilution it just delays it.

Key catalysts driving the stock:

Defense momentum (near term): Continued awards and scaling of existing programs could shift market perception, valuing Voyager more like a traditional defense growth contractor rather than a speculative “space lottery ticket.”

Delays could hurt sentiment, while successful milestones could propel valuation sharply.

Space manufacturing / new tech optionality:

Voyager is developing IP in in-orbit manufacturing, such as advanced materials and fibers.

While this has potential, the market will only reward it once there’s a clear path to revenue.