This is a watchlist composed of the current stocks we are looking to trade none of these are alerts all alerts will be alerted upon entry just like the others on the weekly investment letter.

Company: nCino, Inc

Quote: $NCNO

BT: $25

ST: $40

Sharks Opinion:

nCino isn’t new to us we’ve traded this name multiple times in past cycles, often capitalizing on volatility around broader economic shifts. The recent pullback in share price, driven largely by macroeconomic fears rather than company-specific issues, has once again created an attractive entry point for traders and long-term investors alike.

This reset in valuation presents a compelling setup given the company’s improving fundamentals, deep customer stickiness, and growing role within the digital transformation of the banking sector.

At its core, nCino operates a cloud-based banking platform designed to help financial institutions streamline complex workflows, from loan origination and mortgage processing to account management and regulatory compliance. The company’s end-to-end digital banking solutions are particularly valuable for smaller and mid-sized banks navigating both modernization and compliance burdens in a heavily regulated market.

nCino’s software effectively replaces the legacy systems that many banks still rely on, reducing operational inefficiencies while providing an integrated data layer that enhances decision- making.

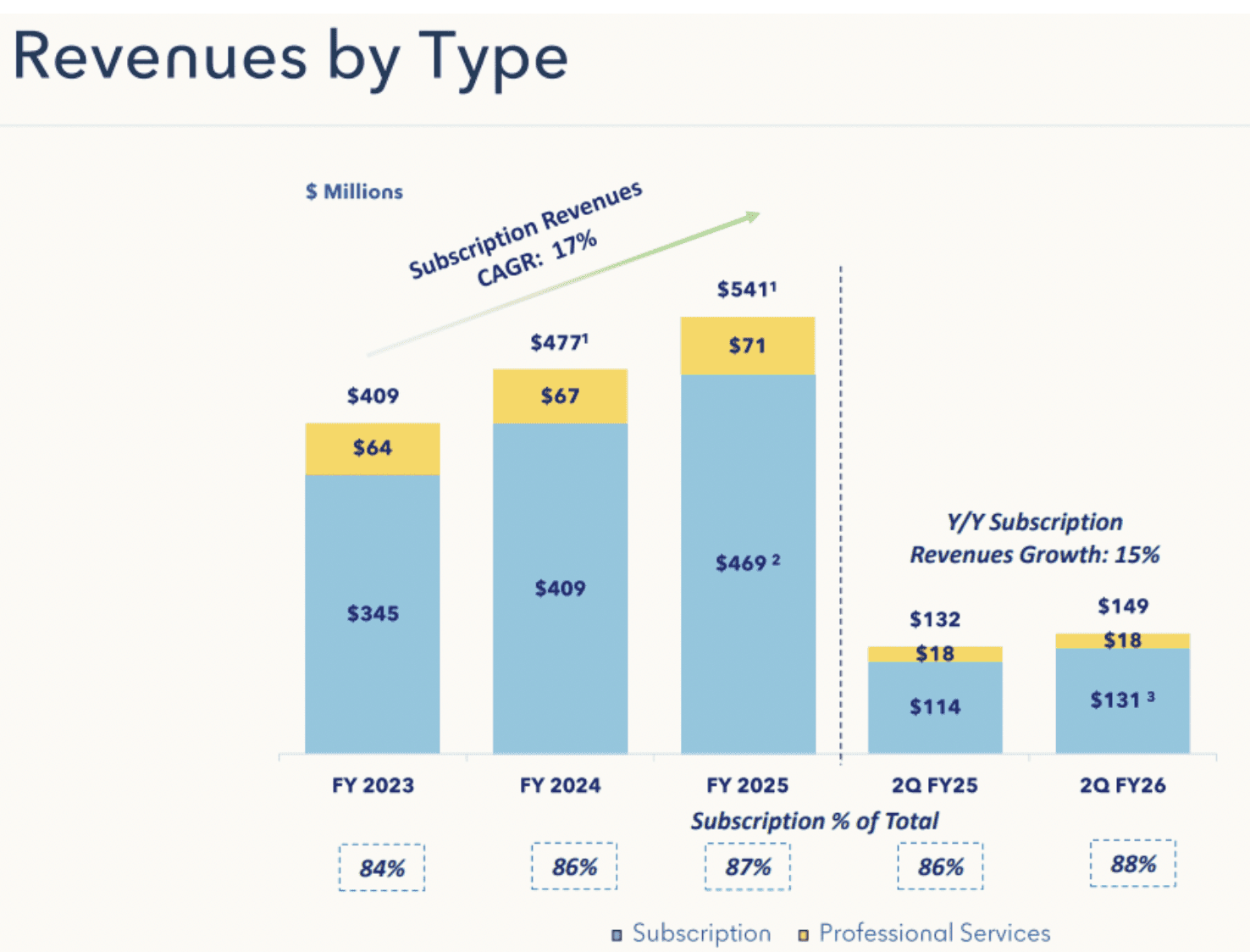

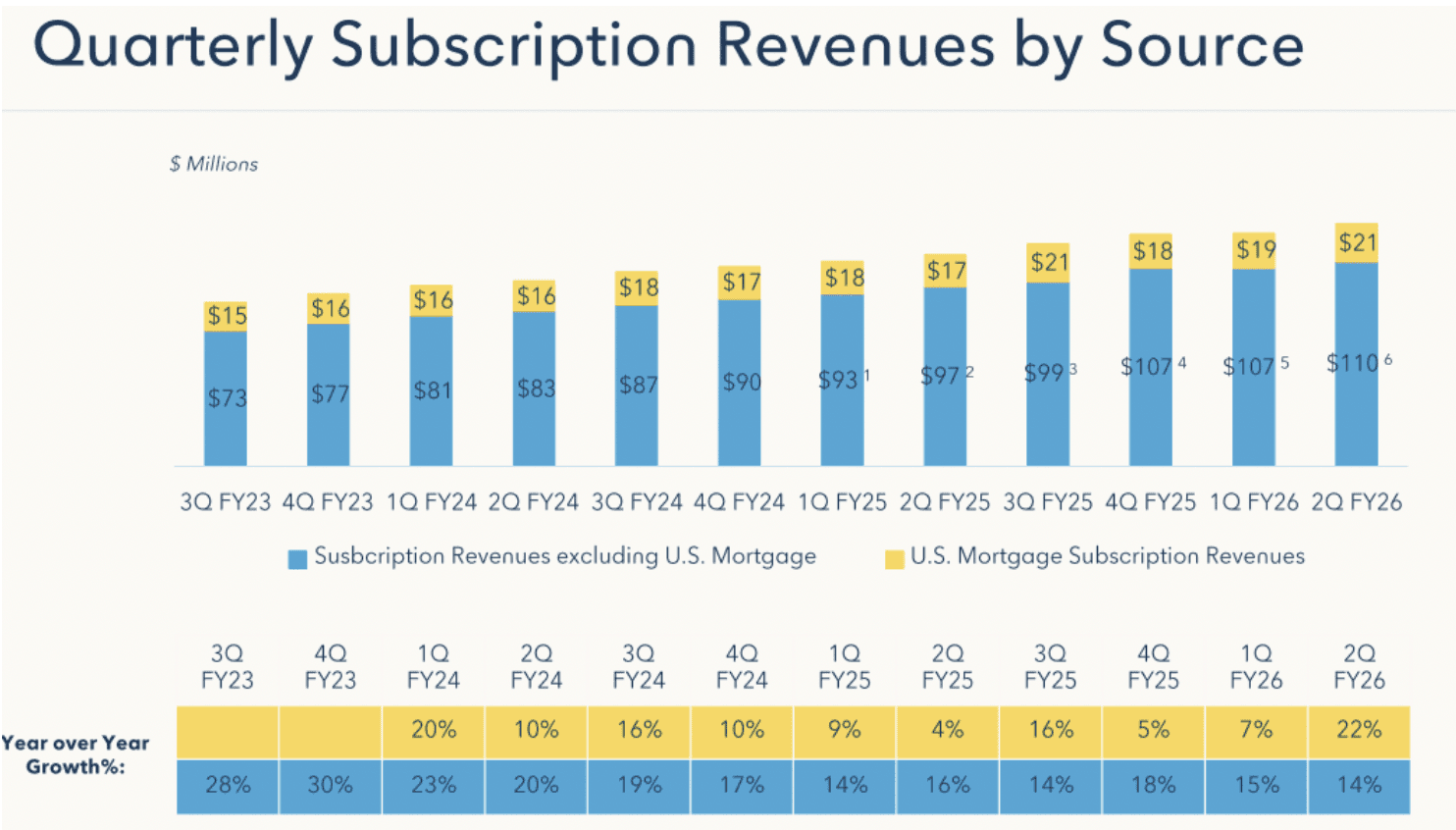

One of nCino’s strongest assets is its business model roughly 90% of revenues are recurring, supported by sticky customer relationships and a renewal rate trending toward historical highs. This recurring revenue foundation gives the company both visibility and pricing power, reflected in recent 5–7% price increases across its client base. Even as credit risk and AI-driven uncertainty linger across the financial services industry, nCino’s expanding gross margins and efficient cost structure reinforce the company’s resilience.

Additional growth drivers are beginning to reaccelerate. Mortgage activity is stabilizing, enterprise demand has rebounded, and international expansion continues to gain traction.

Perhaps most notably, a rebound in bank M&A could serve as a tailwind, since new combinations often trigger platform consolidations and broader adoption of nCino’s solutions.

Description: nCino, Inc., a software-as-a-service company, provides software solutions to financial institutions in the United States, the United Kingdom, and internationally. It offers solutions on the nCino Platform, including Onboarding solution that streamlines and enhances the customer onboarding process through a digital platform for credit and non-credit onboarding, commercial account opening, and enterprise-level onboarding; and Account Opening solution, which includes Deposit Account Opening solution for consumers and small businesses.

nCino continues to solidify its reputation as the backbone of modern cloud banking infrastructure. Built initially on Salesforce’s Force.com platform much like Veeva Systems did for the life sciences industry and increasingly expanding into AWS for cross-sell and integration opportunities, nCino’s architecture is both scalable and deeply embedded within its clients’ core systems. The company provides mission-critical loan origination and workflow automation software for banks, credit unions, and mortgage lenders sectors that have historically been slow to modernize but are now under immense pressure to digitize.

The complexity of loan issuance which requires rigorous documentation, strict regulatory compliance, and intricate approval chains makes this software indispensable. Despite the modernization wave in fintech, a surprising number of institutions still operate on legacy systems dating back to the 1980s, or worse, rely on spreadsheets and manual processes in Microsoft Excel. Fo many of nCino’s end users, the company’s cloud-based platform has become one of the most essential components of their technology stack, enabling real- time visibility, automation, and collaboration across departments that were previously siloed.

This is where nCino has carved out a durable moat: it’s not just selling a product it’s embedding itself into the operational fabric of regulated financial institutions. Once integrated, nCino becomes difficult to displace, driving long- term recurring revenue and providing strong pricing power.

The broader context for nCino’s growth fits within a larger software industry trend: the rise of vertical SaaS. While horizontal software solutions (like Slack, Zoom, or Asana) serve broad use cases across industries, vertical SaaS targets specialized, mission-critical workflows for specific sectors — whether that’s life sciences (Veeva), education (PowerSchool), or banking (nCino).

These vertical platforms are typically harder to build and slower to scale, but once established, they command deep customer loyalty and high margins.

From a financial standpoint, nCino continues to perform ahead of expectations. In its most recent quarter, the company reported revenues of $148.8 million, representing 12.4% year-over-year growth and beating analyst estimates by nearly 4%. It also exceeded billing forecasts and raised EPS guidance for the following quarter signaling strong demand, efficient execution, and expanding profitability.

What’s particularly noteworthy is that nCino’s growth is occurring in a subdued lending environment, underscoring the stickiness of its product and the non- cyclical nature of its software revenue. As banks and credit unions continue to modernize their lending operations, nCino’s platform remains a cornerstone of digital transformation in the financial sector — a quiet but powerful compounder with long-term upside potential.

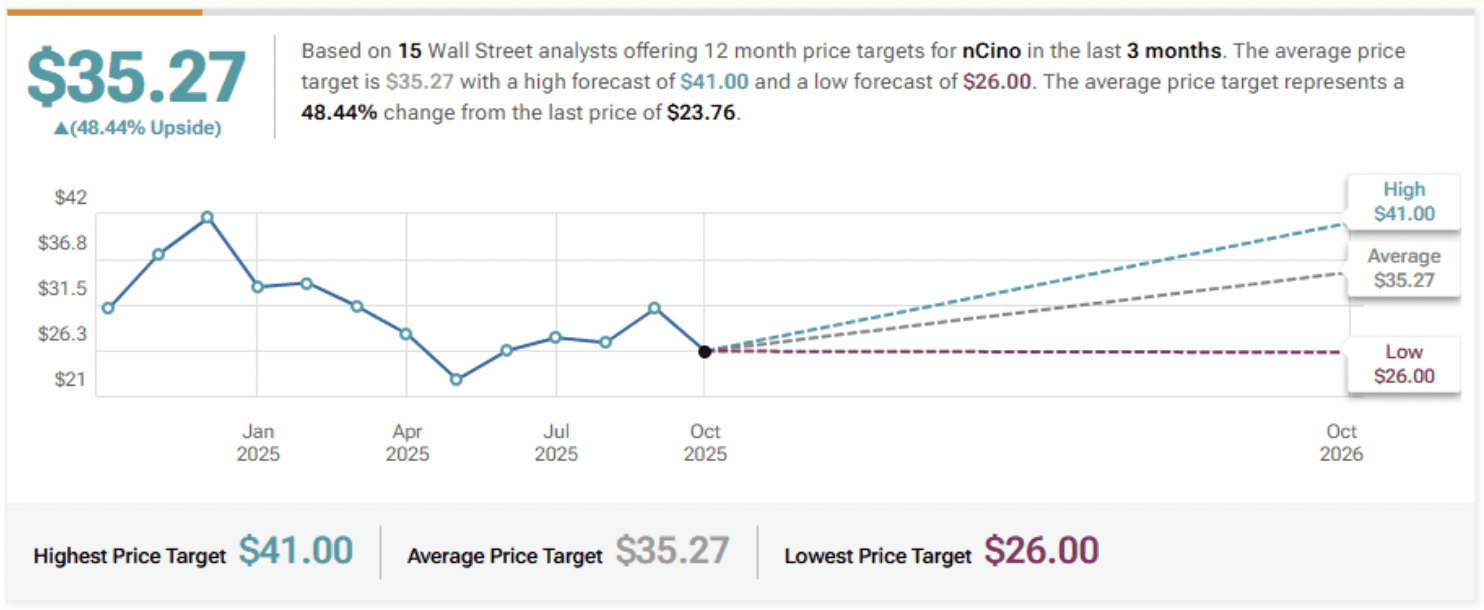

Raymond James Upgrades Ncino to Strong Buy, Announces $36 Price Target

Morgan Stanley Upgrades Ncino to Overweight, Raises Price Target to $36

Barclays Maintains Overweight on Ncino, Raises Price Target to $37

Morgan Stanley Maintains Equal-Weight on Ncino, Raises Price Target to $35

B of A Securities Maintains Neutral on Ncino, Raises Price Target to $38

Company: Lyft, Inc

Quote: $LYFT

BT: $18-$20

ST: $34-$40

Sharks Opinion:

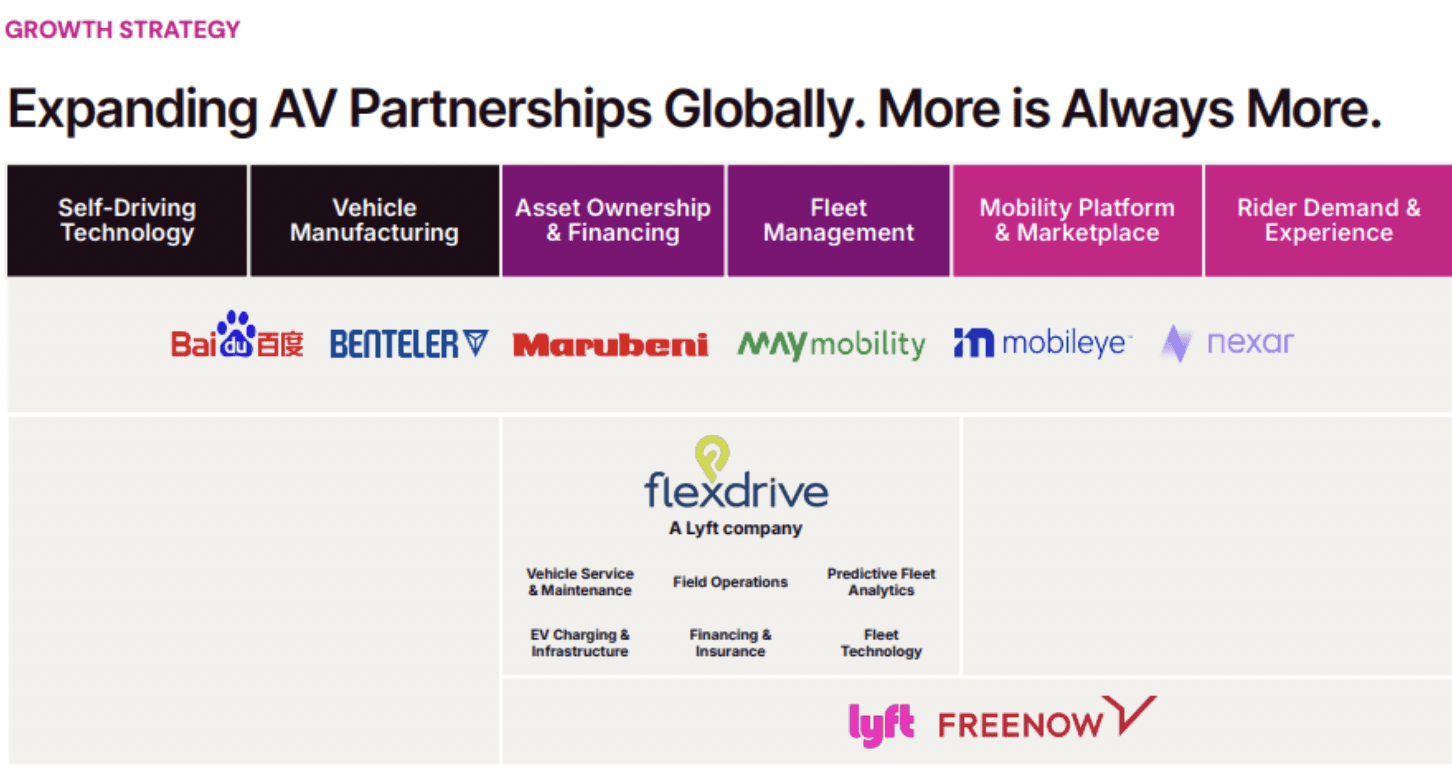

We believe the odds of a Lyft acquisition are rising and not just as speculation. Market signals, capital constraints, and the coming wave of autonomous vehicles (AVs) all point to consolidation ahead.

The AV landscape has shifted: Tesla, Waymo, and Amazon’s Zoox have largely cracked the tech and hardware, but none of them have the rideshare network the real-time scale and liquidity that make platforms like Lyft and Uber valuable. That’s Lyft’s leverage.

While Lyft has cleaned up operations and focused on its core rideshare business, it lacks the capital to compete long-term in an AV-driven world.

Running and insuring self-driving fleets will require deep pockets, favoring trillion-dollar companies like Tesla, Amazon, and Alphabet.

That’s why a deal makes sense. Tesla could plug Lyft into its FSD network; Amazon could fold it into Zoox; Waymo could scale faster with Lyft’s infrastructure; and DoorDash could expand its logistics reach.

We exclude Uber from consideration antitrust hurdles aside, Uber can capture Lyft’s share organically.

Bottom line: Lyft’s future likely depends on partnership or acquisition. The AV era won’t wait and Lyft’s platform is too valuable to stay independent forever.

Description: Lyft, Inc. operates a peer-to-peer marketplace for on-demand ridesharing in the United States and Canada. The company operates multimodal transportation networks that offer access to various transportation options through the Lyft platform and mobile-based applications.

Lyft shares have been trending higher as the company takes tangible steps toward autonomous mobility through two major partnerships. The most notable a deal with Alphabet’s Waymo will see Lyft power fleet management for Waymo’s upcoming AV service in Nashville, handling maintenance, depots, and infrastructure. The service is set to launch via the Waymo app in 2026, with Lyft integration expected soon after.

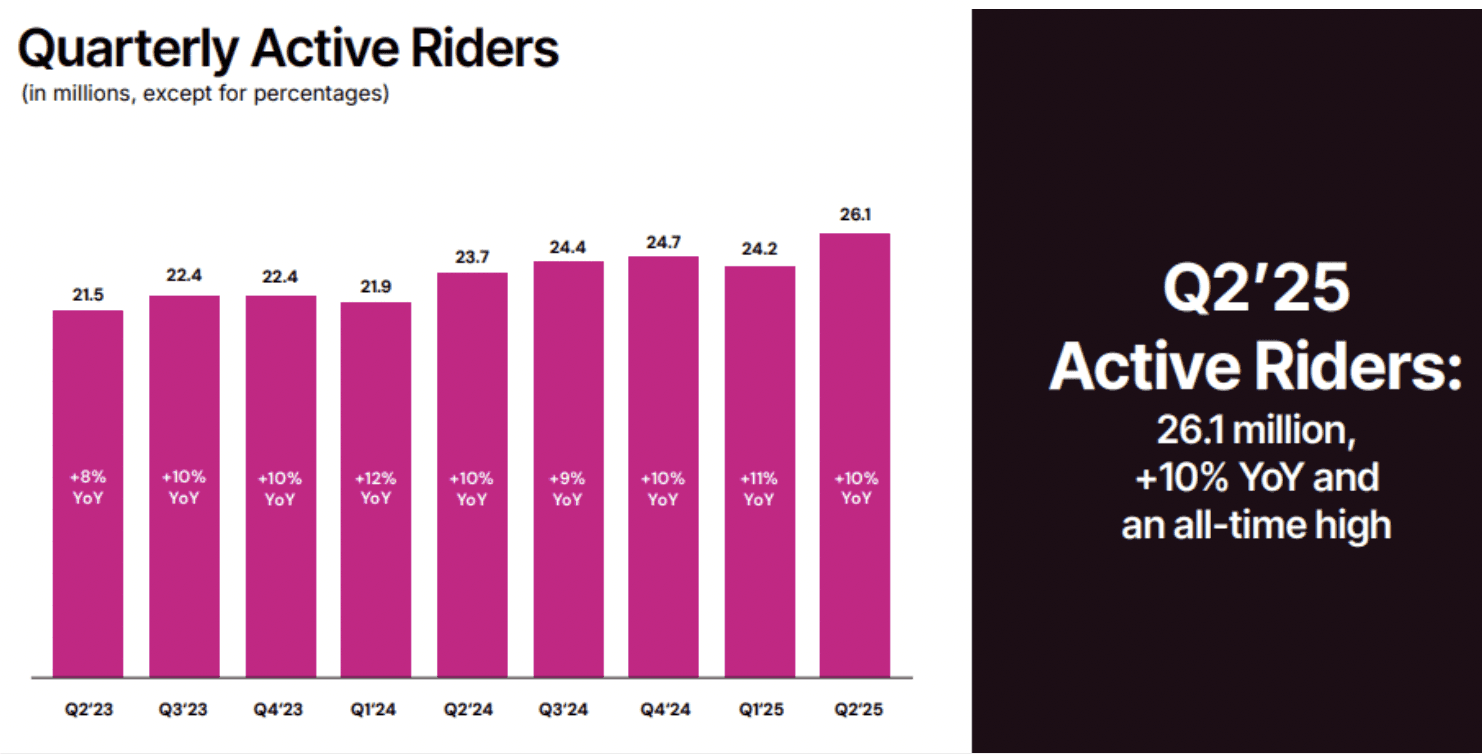

Momentum has also been fueled by Lyft’s acquisition of FreeNow, launch of Lyft Silver, and improving fundamentals, prompting several Wall Street upgrades and higher price targets. The company’s operational scale is massive 5.5 million weekly active passengers, 500,000 drivers, and over 2 million rides arranged daily. Gross bookings surged 17% year-over-year to more than $16 billion in 2024, translating to about $6 billion in revenue and a double-digit free cash flow margin.

Profitability continues to improve as Lyft’s adjusted EBITDA margin, measured as a share of gross bookings, rose from 1.6% in 2023 to 2.3% in 2024, with projections nearing 4% by 2027. While a small net loss remains possible this year, it could be the last signaling a company on the verge of sustained profitability, just as it leans into the next evolution of ridesharing.

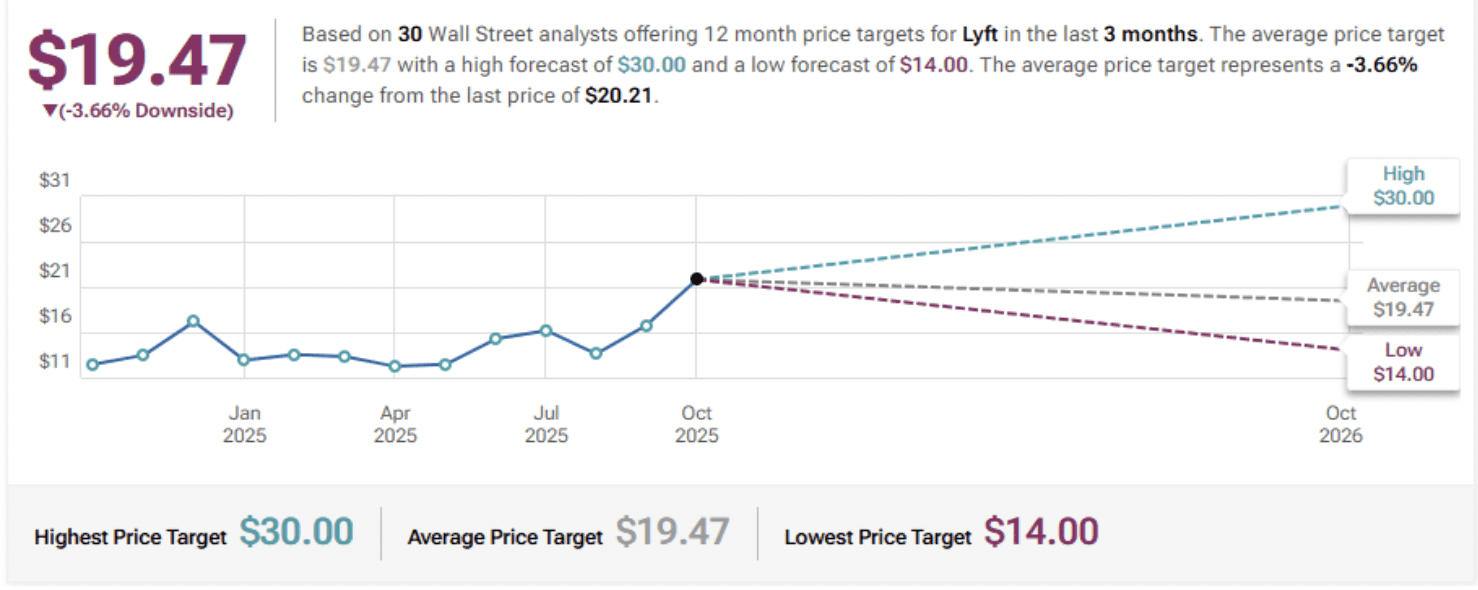

Guggenheim Initiates Coverage On Lyft with Buy Rating, Announces Price Target of $22

Mizuho Initiates Coverage On Lyft with Neutral Rating, Announces Price Target of $24

TD Cowen Maintains Buy on Lyft, Raises Price Target to $30

Benchmark Maintains Buy on Lyft, Raises Price Target to $26

Company: C3.ai, Inc.

Quote: $AI

BT: $15 - $18

ST: $30

Sharks Opinion:

C3.ai remains one of the more speculative names in the artificial intelligence space not because of its fundamentals, but because of its ticker. The company, once seen as a pioneer in enterprise AI, has long struggled to live up to its early hype.

Since going public in 2020, C3’s stock performance has been weak, overshadowed by peers like Palantir and newer entrants with more robust ecosystems.

That said, in a market that often values narrative over numbers, the “AI” ticker alone might be its most valuable asset. With a market cap of around $2.5 billion and roughly $400 million in annual revenue, C3 could be an attractive reverse takeover (RTO) target for a fast-growing private AI firm like Anthropic or Perplexity companies seeking a quick path to public markets and brand recognition.

It’s a pure speculative play, not grounded in traditional metrics or profitability. But in a market driven by momentum and headlines, it’s not far- fetched to imagine that C3’s ticker paired with its existing enterprise and government contracts — could become the gateway for another AI heavyweight looking to go public fast.

Description: C3.ai, Inc. operates as an enterprise artificial intelligence application software company.

The company offers C3 agentic AI platform, an application development and runtime environment that enables customers to design, develop, and deploy enterprise AI applications

C3.ai sits on a solid financial cushion, holding roughly $700 million in cash reserves against an annual cash burn of about $80 million enough runway to push toward breakeven or attract a potential acquirer.

The company’s most valuable asset may be its PANDA platform, a predictive maintenance system used by the U.S. Air Force across key aircraft such as the B1-B Lancer, C-5 Galaxy, and C-130J Super Hercules. That contract alone carries a potential $450 million value over several years, anchoring C3’s credibility in high-stakes defense analytics.

Beyond defense, C3 has shifted its strategy to deepen ties with major cloud providers, forming alliances that now drive over 70% of total sales up 68% year-over-year.

Its partnership with Microsoft stands out, integrating C3’s AI applications into Azure’s sales ecosystem and closing multiple joint deals in the manufacturing and chemical sectors.

Taken together, C3’s defense contracts, cloud alliances, and sizable liquidity position the company as a strategic acquisition target or turnaround candidate.

The fundamentals remain mixed, but its foothold in government AI infrastructure and enterprise cloud ecosystems keeps it relevant in an increasingly crowded AI market.

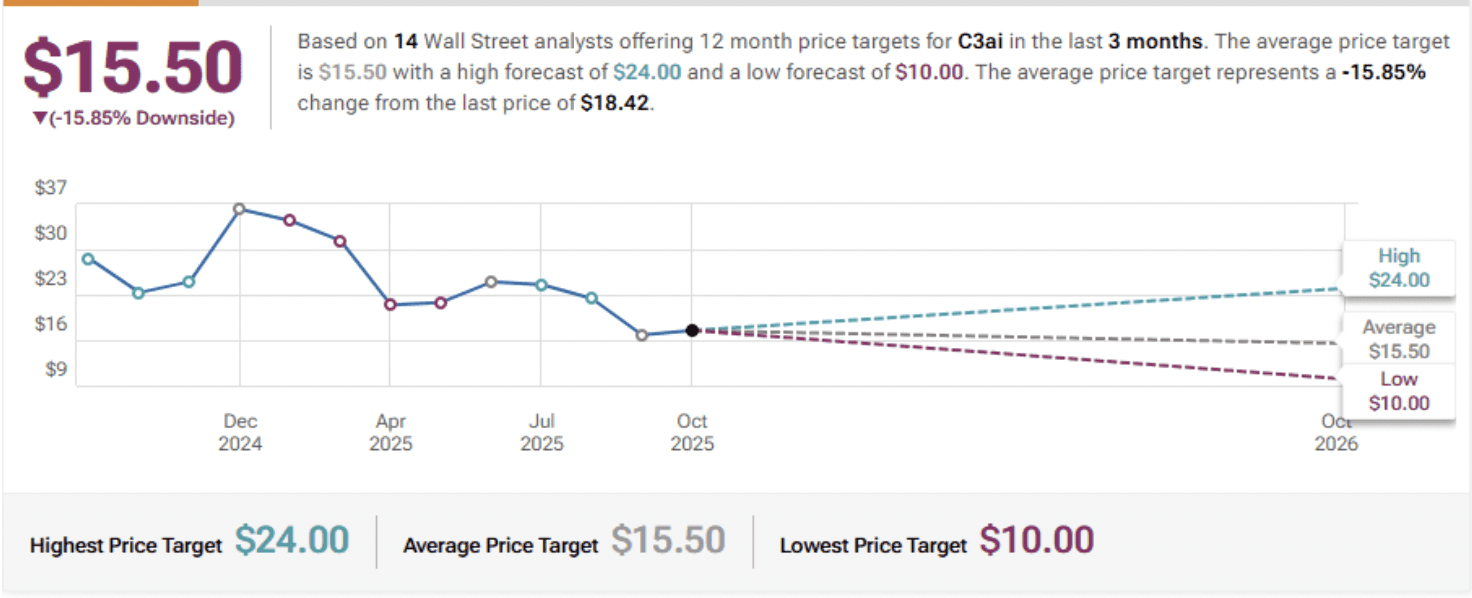

UBS Maintains Neutral on C3.ai, Raises Price Target to $17

Morgan Stanley Maintains Underweight on C3.ai, Lowers Price Target to $11

Canaccord Genuity Maintains Hold on C3.ai, Lowers Price Target to $16

JMP Securities Maintains Market Outperform on C3.ai, Lowers Price Target to $24

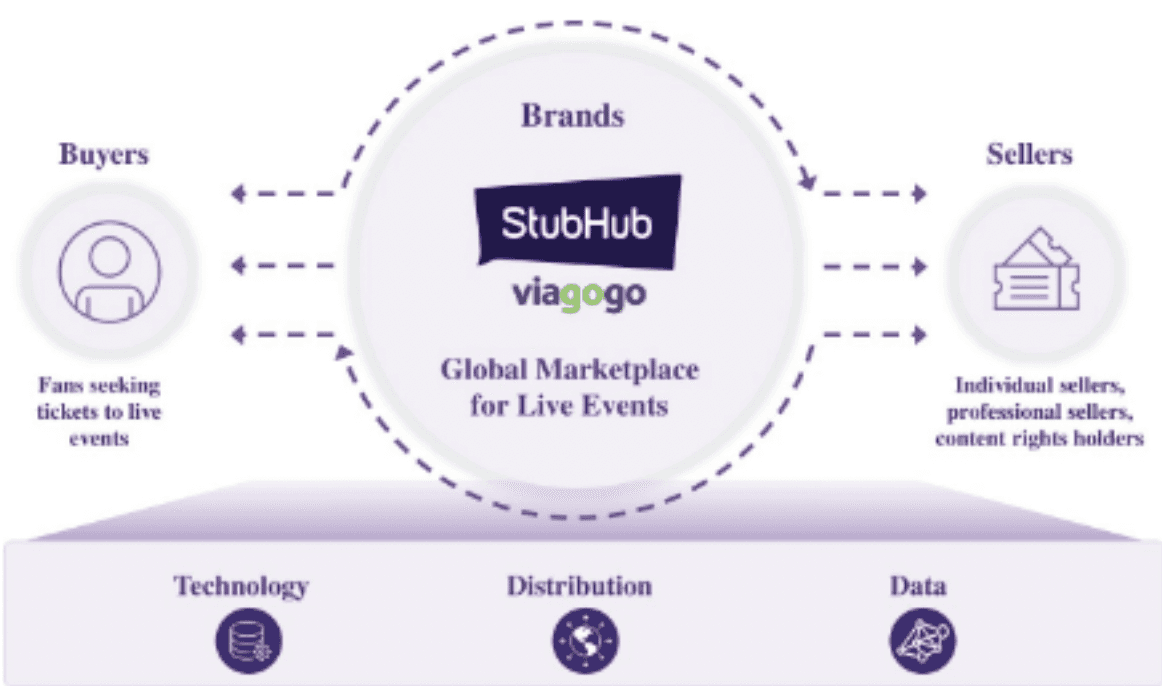

Company: StubHub Holdings

Quote: $STUB

BT: $18

ST: $28- $30

Sharks Opinion:

StubHub recently made its public debut, completing a successful IPO last quarter. Since listing, shares have drifted lower as early investors took profits and broader market sentiment cooled.

However, we see a clear short-term opportunity for a rebound back toward the company’s initial offering price, effectively a return to its net asset value (NAV) assigned at listing.

There’s no grand narrative here no AI angle, no crypto tie-in, no speculative hype just a straightforward swing trade setup on a newly public company with strong brand recognition and consistent transaction volume. Many Wall Street analysts share this view, calling StubHub a technical recovery play rather than a growth story.

In our view, this is a classic case of early post-IPO weakness creating a short-term mispricing a trade to capture the market’s eventual mean reversion rather than a long-term bet on disruption.

Description: StubHub Holdings, Inc. operates ticketing marketplace for live event tickets worldwide. It buys and sells sports, concerts, theatre, and other live events tickets through its websites and mobile applications under the StubHub and viagogo brand name.

StubHub may draw constant criticism from fans over its high fees, yet few companies in tech have a more durable and defensible business model. The company captures roughly 20% of gross merchandise value (GMV) in transaction fees and buyers continue to pay because StubHub sells certainty.

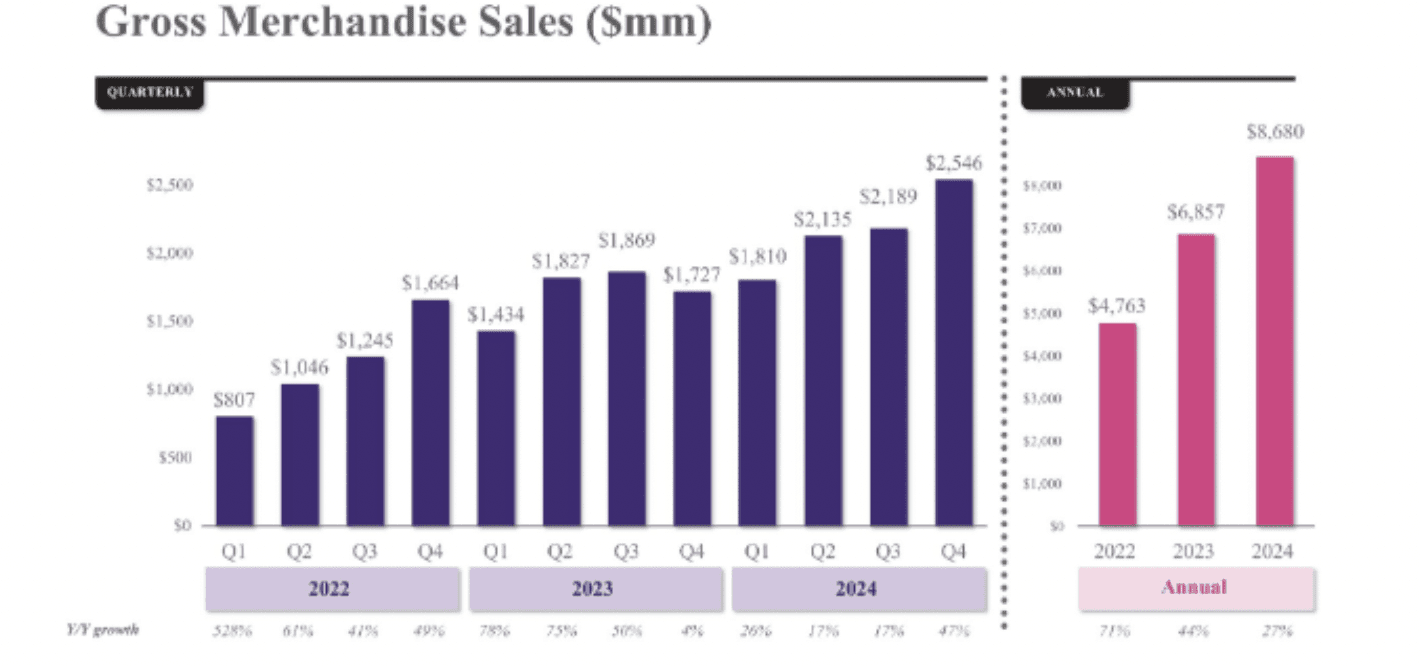

That certainty verified tickets, guaranteed refunds, multilingual support across 33 countries is the true moat. Competitors like SeatGeek or TickPick can’t match the platform’s trust and global infrastructure. StubHub’s network effects make it nearly impossible to dislodge: buyers go where tickets are, and sellers follow the buyers. With $8.7 billion in GMV last year and $4.4 billion in the first half of 2025, it’s the undisputed marketplace of record.

Even as GAAP profitability fluctuates, StubHub’s cash flow engine is elite. Its negative working capital model customers pay first, suppliers later has generated $255 million in free cash flow last year (14% margin) and $161 million in the first half of 2025 (19% margin). In short: fans may complain, but investors see what matters most a high-trust platform printing real cash.

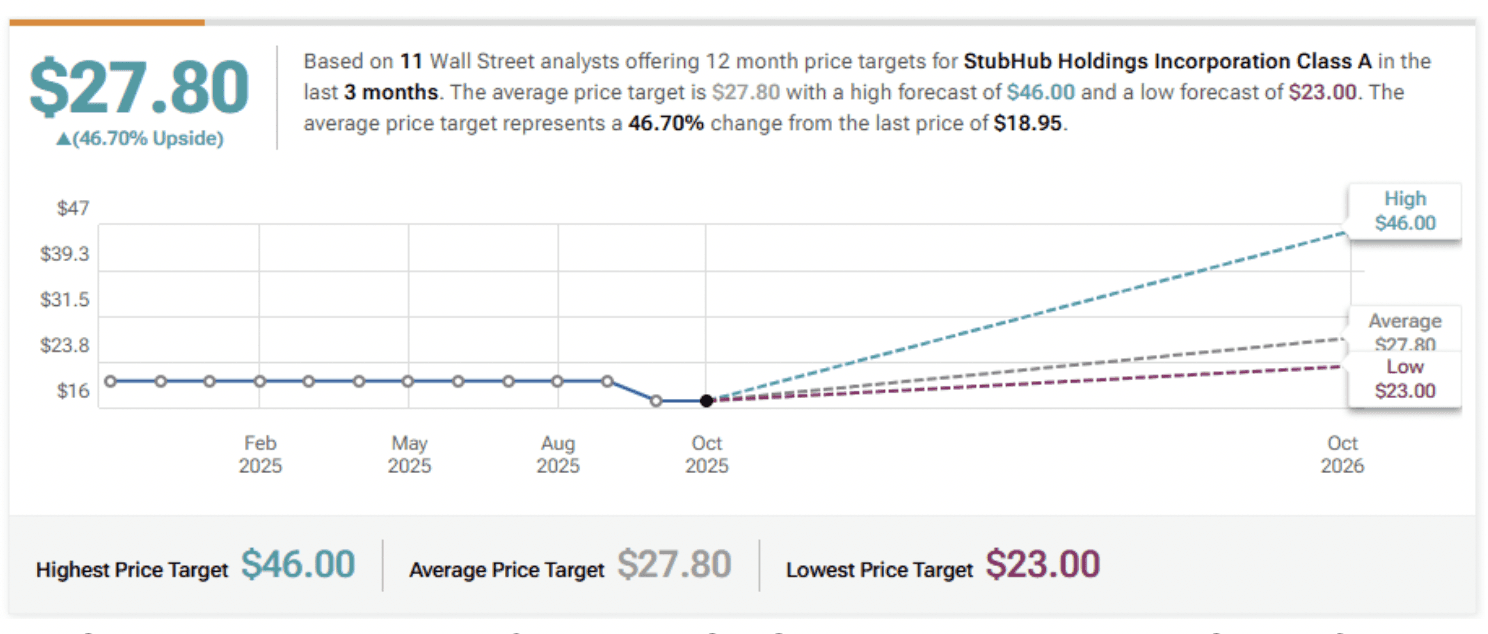

Oppenheimer Initiates Coverage On Stubhub Holdings with Outperform Rating, Announces Price Target of $23

Goldman Sachs Initiates Coverage On Stubhub Holdings with Buy Rating, Announces Price Target of $46

JP Morgan Initiates Coverage On Stubhub Holdings with Overweight Rating, Announces Price Target of $24

Evercore ISI Group Initiates Coverage On Stubhub Holdings with Outperform Rating, Announces Price Target of $29