This is a watchlist composed of the current stocks we are looking to trade none of these are alerts all alerts will be alerted upon entry just like the others on the weekly investment letter.

Company: WhiteFiber, Inc

Quote: $WYFI BT: $15-$18

ST: Currently, we have three internal price targets mapped out, as we’re approaching this primarily as a longer-term position. That said, given the company’s early-stage profile and the potential for heightened volatility, we’re choosing to stay conservative for now with a $32 base price target. As execution progresses and visibility improves, we can reassess upside scenarios. For the moment, capital preservation and disciplined sizing remain the priority while the thesis plays out.

Sharks Opinion:

WhiteFiber is a new name for us, uncovered through last week’s 13F review process. While we may be early especially with the stock selling off into year-end the AI infrastructure theme remains firmly intact.

At current levels, we think it could justify a starter position given the potential asymmetric upside.

The AI infrastructure thesis is straightforward: specialized compute capacity is scarce, demand is accelerating rapidly, and customers are willing to pay premium pricing for access.

WhiteFiber represents one of the few pure-play vehicles tied directly to this buildout. Instead of owning a small slice of a diversified cloud giant like Amazon or Microsoft, investors are gaining exposure to a focused operator that could control 200–300 MW of high-value data center capacity purpose-built for AI workloads.

There are risks. Bit Digital owns roughly 80% of WhiteFiber, meaning any sizable share sale could pressure the stock. That said, it also creates strategic alignment Bit Digital is incentivized to see WhiteFiber scale successfully. The AI gold rush is underway. WhiteFiber is positioning itself to supply the pickaxes and shovels while also building the mines.

The real question is not whether AI infrastructure will be valuable. It’s whether WhiteFiber can execute quickly enough to secure meaningful share before the competitive window narrows.

Description: Whitefiber Inc is a provider of artificial intelligence infrastructure solutions. The company owns high-performance computing data centers and provide cloud-based HPC graphics processing units services, which it terms cloud services, for customers such as AI application and machine learning developers. Its Tier-3 data centers provide hosting and colocation services. Its cloud services support generative AI workstreams, especially training and inference. It has two reportable segments: cloud services and colocation services. The cloud services segment generates revenue from providing high performance computing services to support generative AI workstreams. Colocation services generate revenue by providing customers with physical space, power and cooling within the data center facility.

WhiteFiber is a cloud infrastructure company purpose-built for AI workloads.

Traditional cloud data centers operated by hyperscalers like Google, Amazon, and Microsoft were architected years ago for general-purpose computing.

Retrofitting them for high-density AI workloads often requires costly upgrades and redesigns.

WhiteFiber’s model is different. It owns and operates the full stack of infrastructure Tier-3 data centers equipped with 4,500+ NVIDIA GPUs, advanced liquid cooling systems capable of handling 150kW+ per rack, and proprietary orchestration software that links facilities into virtual “superclusters.”

That differentiation matters. AI workloads generate extreme heat and demand enormous bandwidth.

Purpose-built, high-density facilities are increasingly necessary not optional as compute intensity rises.

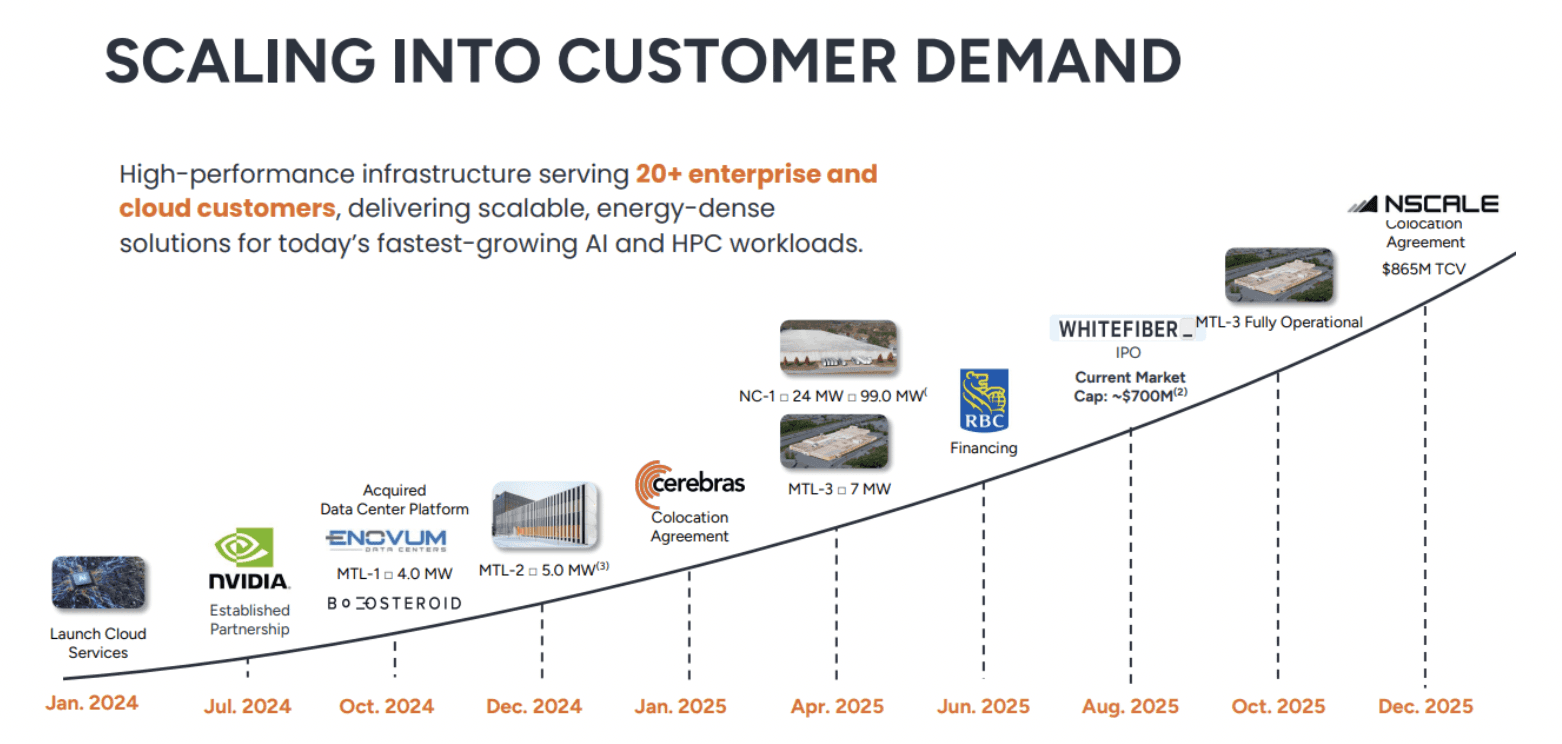

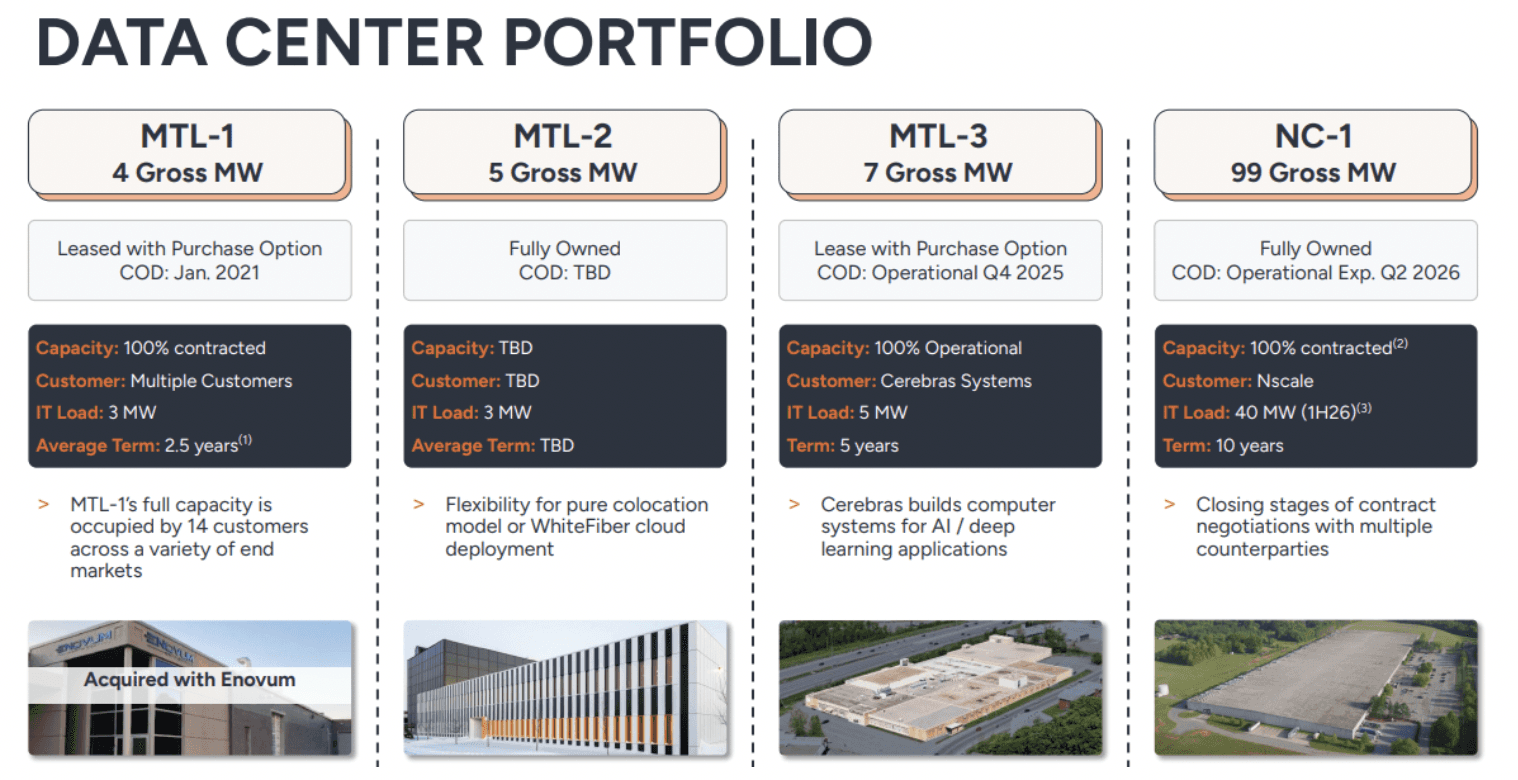

On the expansion front, WhiteFiber acquired 96 acres in North Carolina for what is planned to be a flagship 200 MW AI data center campus one of the largest dedicated AI-focused developments in the United States.

• Phase 1 (24 MW) is expected to go live by mid 2026, with power secured through Duke Energy

• Full 200 MW buildout could generate approximately $340 million in annual revenue, assuming ~$1.7 million per MW (in line with industry benchmarks)

• The broader pipeline includes 1,300 MW under review, with 800 MW under letters of intent

For comparison, Applied Digital’s 250 MW agreement is expected to generate roughly $7 billion over 15 years or about $1.87 million per MW annually.

Against that backdrop, WhiteFiber’s underwriting at roughly $1.6–1.7 million per MW appears relatively conservative.

The opportunity is straightforward: if execution matches the buildout plans, the revenue potential scales rapidly with each incremental megawatt brought online.

WhiteFiber’s customer growth has accelerated rapidly.

The company went from just one customer in early 2024 to more than 20 by early 2025.

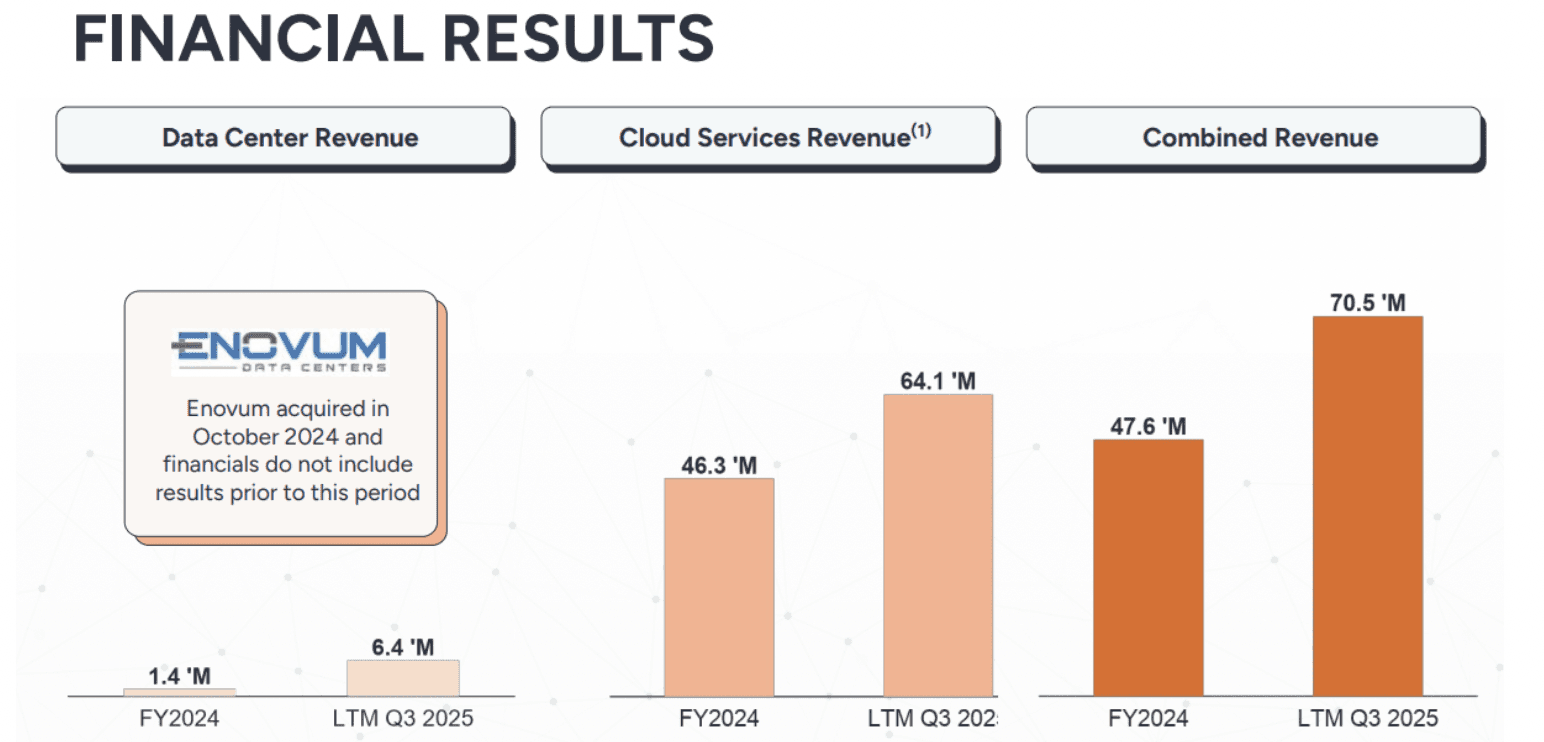

Revenue reached $45.7 million in its first full year of operations, with $14.8 million generated in Q1 2025 alone signaling strong early demand ramp.

Several meaningful contracts are already in place:

• Cerebras Systems 5 MW deployment under a five-year agreement

• Boosteroid 489 GPUs valued at $7.9 million through 2029, with expansion options up to 50,000 servers

Q3 2025 Highlights (Quarter Ending September 30):

• Revenue: $20.2 million, up 65% year over year

• Net Loss: -$15.8 million versus -$0.4 million last year

• EPS: -$0.47

• Adjusted EBITDA: $2.3 million

• Gross Margin: Approximately 63–65%

• Cash: $166.5 million as of September 30, 2025

The story remains one of rapid top-line growth paired with early-stage investment and scaling costs.

Margins are healthy at the gross level, but profitability will depend on execution and disciplined expansion as capacity ramps.

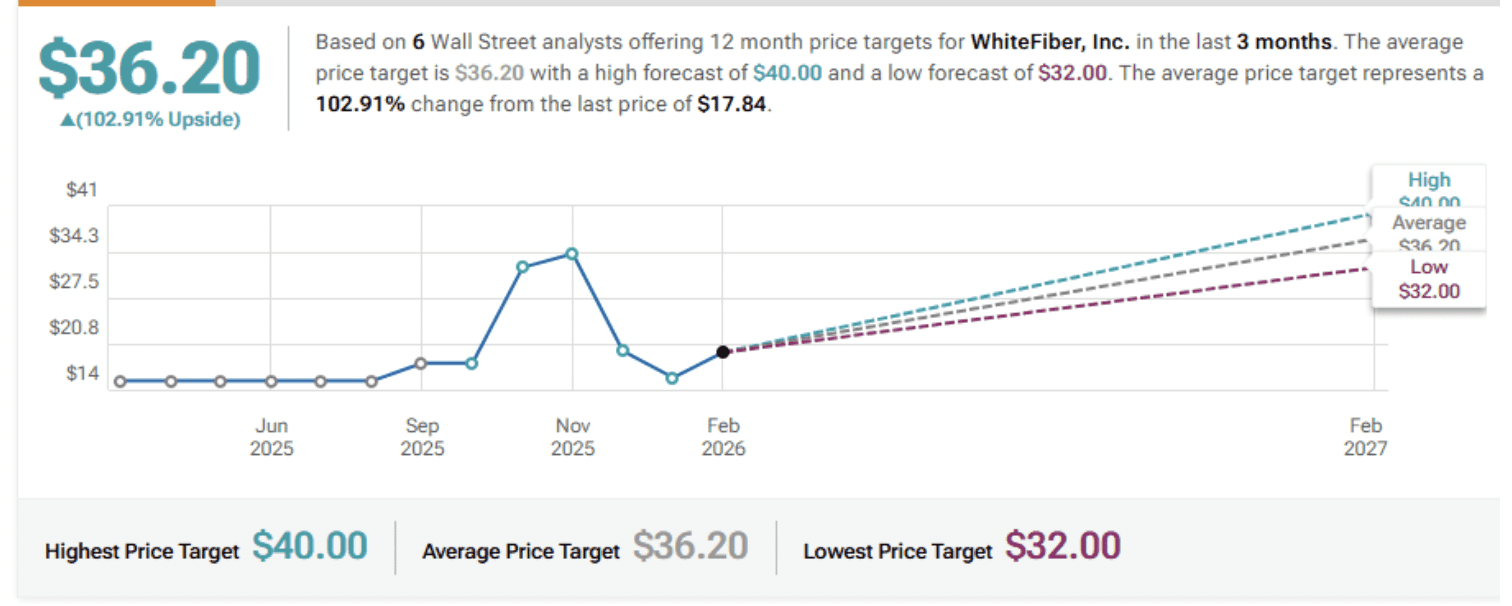

HC Wainwright & Co. Reiterates Buy on Whitefiber, Maintains $34 Price Target

B. Riley Securities Maintains Buy on Whitefiber, Lowers Price Target to $40

Compass Point Initiates Coverage On Whitefiber with Buy Rating, Announces Price Target of $32

Citizens Initiates Coverage On Whitefiber with Market Outperform Rating, Announces Price Target of $37

Roth Capital Maintains Buy on Whitefiber, Lowers Price Target to $37

Needham Maintains Buy on Whitefiber, Lowers Price Target to $38

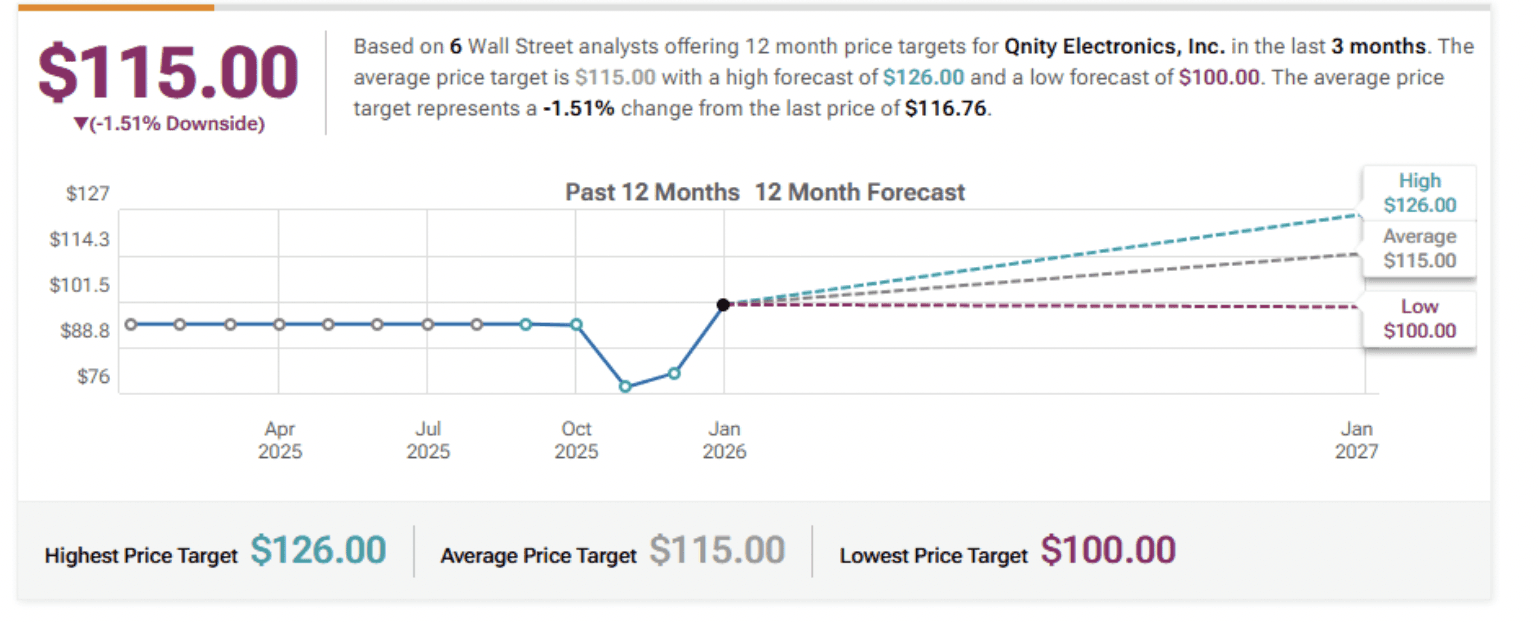

Company: Qnity Electronics

Quote: $Q

BT: $85 (would be ideal on a earnings dip)

ST: $145 (long term)

Sharks Opinion:

Looking through last quarter’s 13F filings, one name kept appearing across a majority of the funds we track.. that being $Q Qnity

When investors discuss the AI arms race, they usually focus on the chip designers like NVIDIA and AMD, or the foundries like TSMC. What often gets overlooked are the consumables the highly specialized chemicals and materials required to manufacture every advanced chip.

That’s where Qnity fits.

Much like Chemours, Qnity was independently spun off from DuPont.

But while the Chemours thesis centers more on cooling infrastructure for data centers, Qnity operates in the consumables layer of semiconductor manufacturing.

Unlike capital equipment companies such as ASML or Lam Research whose revenues can be lumpy and highly dependent on large fab CapEx cycles Qnity sells materials that are required every time a wafer is processed.

That creates a more recurring, embedded revenue model tied directly to production volume rather than build cycles.

In that sense, Qnity offers exposure to the AI boom with a different risk profile: pricing power in specialized chemistry, recurring demand characteristics, and a valuation that has not fully converged with peers.

That said, 13Fs reflect prior-quarter positioning, not real-time flows.

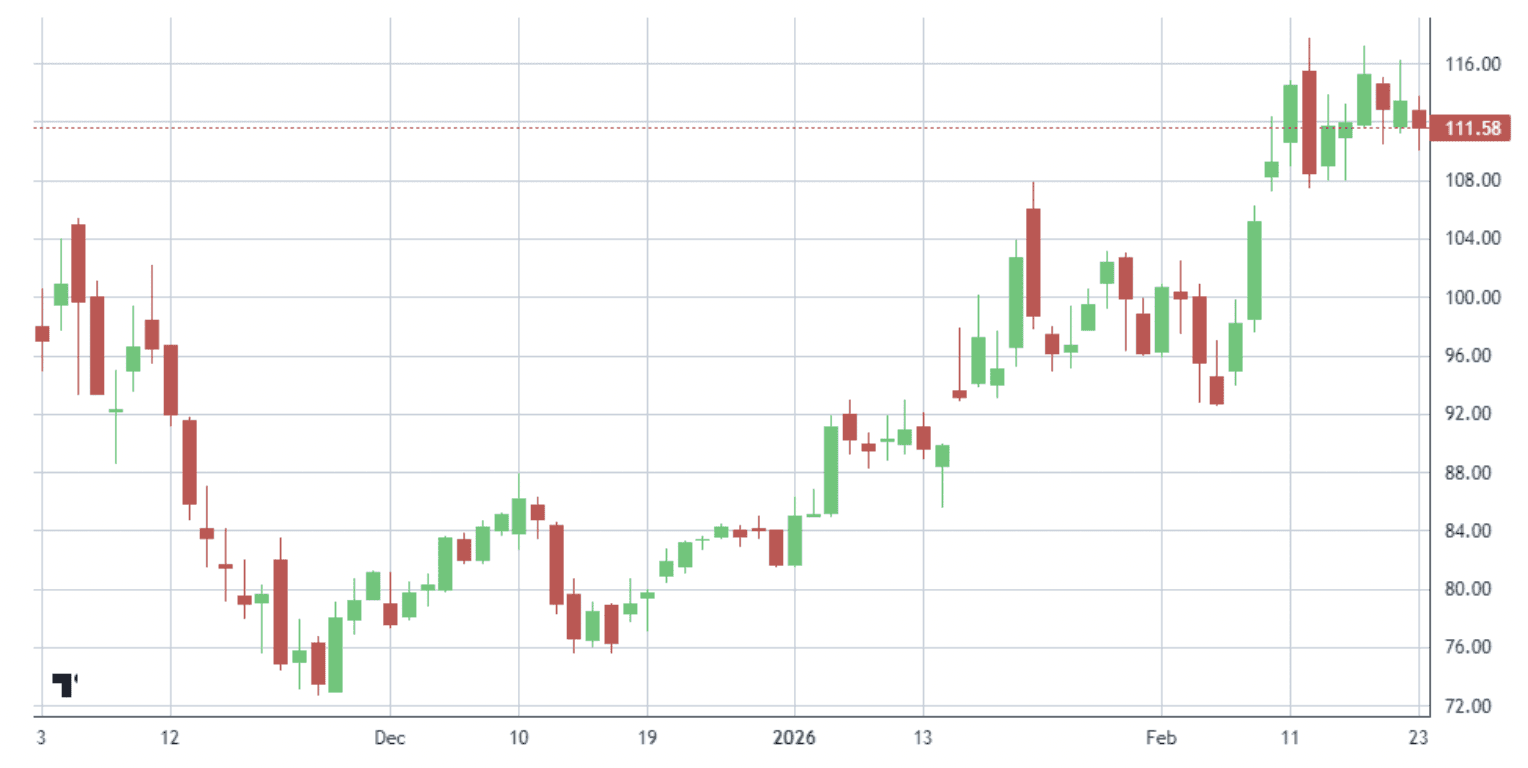

The stock is already up 22% over the past month, with earnings due in a few days. After seeing the volatility in Chemours post-earnings, we prefer to wait and evaluate the reaction.

If a similar sharp move materializes, we would look to take advantage of a potential dip rather than chase strength.

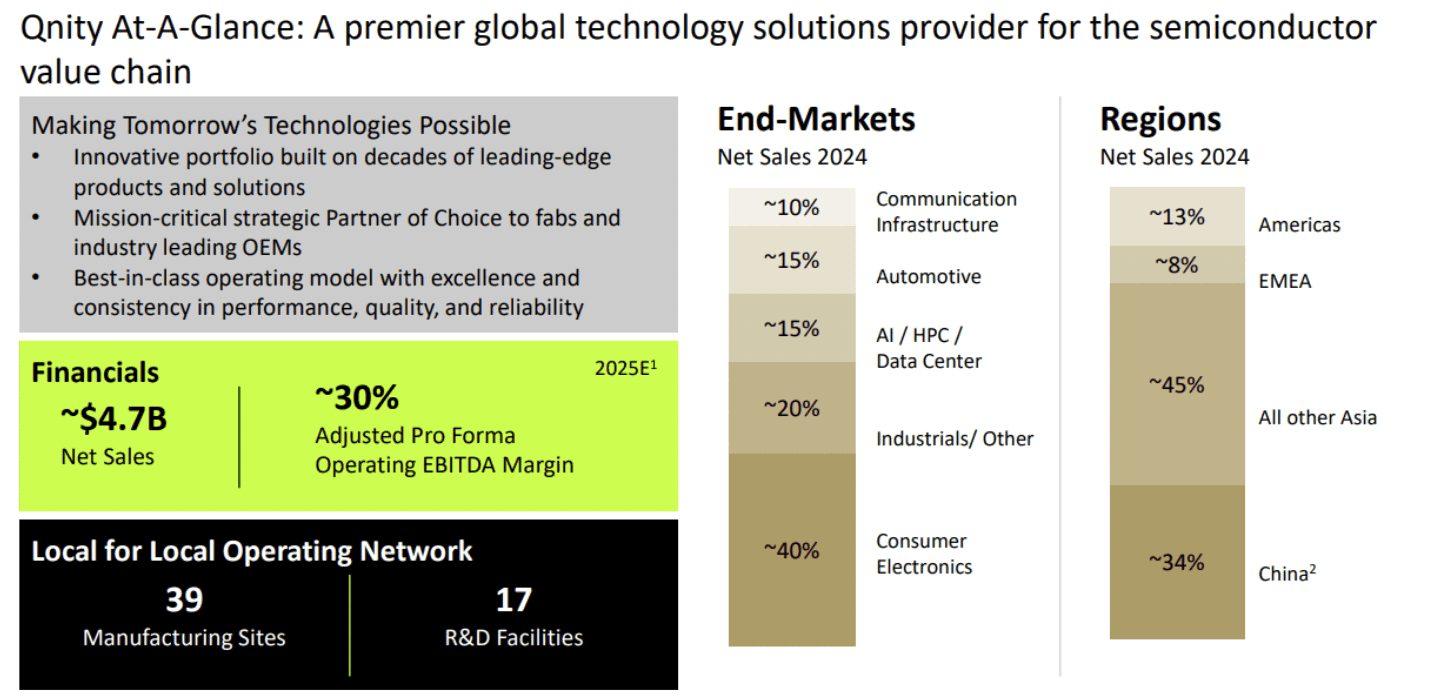

Description: Qnity is a specialty chemicals company created in 2025 after being spun off from DuPont. It sells chemicals and materials to the semiconductor industry, which generates the majority of sales, and also the electronics industry.

Qnity specializes in materials science, including supplying key materials required to manufacture semiconductors and interconnected devices.

Qnity is stepping out as one of the largest pure-play electronics materials companies in the market backed by a 50+ year legacy, 10,000 employees globally, nearly 40 manufacturing sites, and close to 20 R&D facilities.

This isn’t a startup story. It’s an infrastructure story.

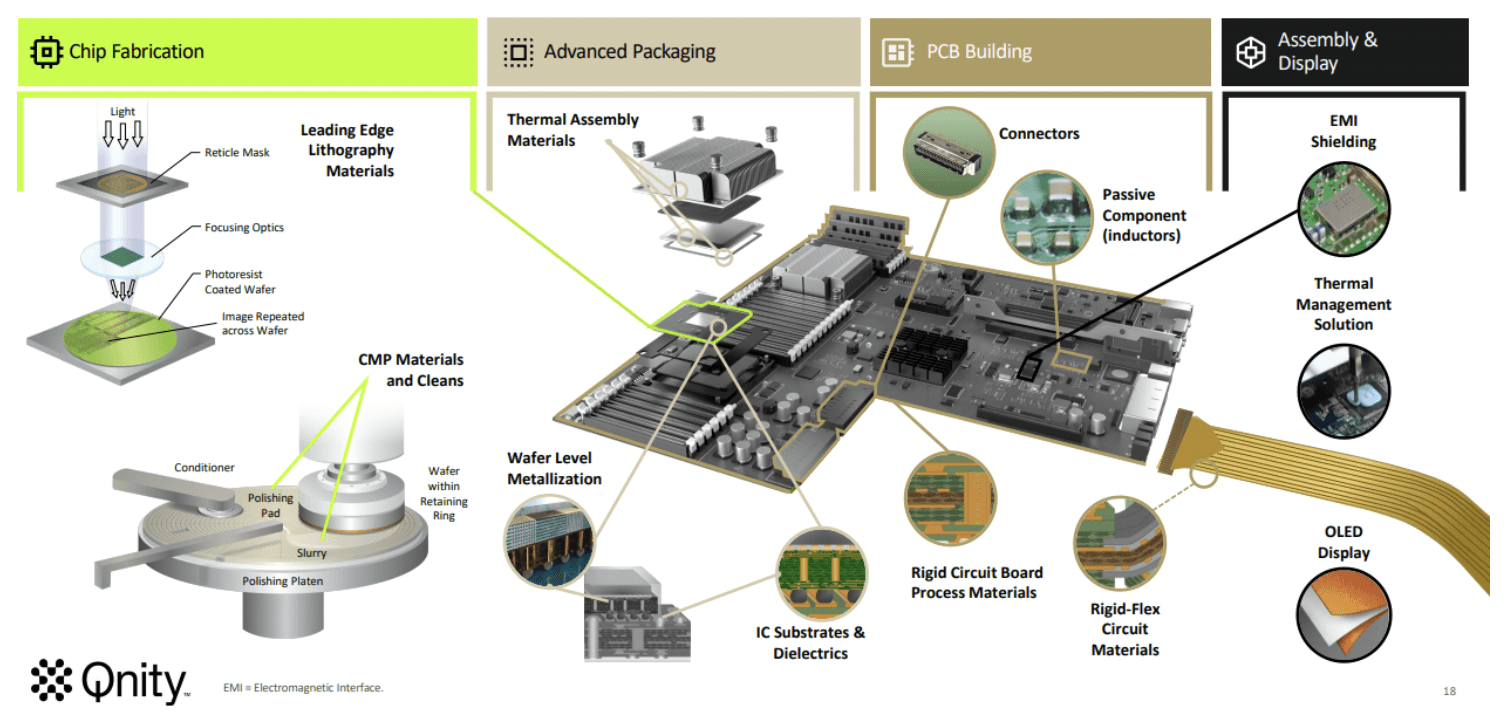

The company focuses on differentiated electronic materials supplying the critical consumables used in semiconductor manufacturing, advanced packaging, interconnects, thermal management, and display technologies.

Roughly 90% of revenue comes from consumables and unit-driven products, which creates recurring demand tied directly to chip volumes rather than volatile CapEx cycles.

Core segments break down as follows:

Semiconductor Technologies (~55% of revenue)

Solutions for chip fabrication, including CMP pads and photoresists materials required every time a wafer is processed.

Interconnect Solutions (~45% of revenue)

Advanced packaging, thermal management, and circuit imaging solutions that enable increasingly complex chip architectures.

Revenue exposure is diversified across the electronics ecosystem:

• Chip fabrication: 50%

• PCB building: 20%

• Assembly & display: 20%

• Advanced packaging: 10%

With customers in more than 80 countries, Qnity isn’t dependent on a single region, foundry, or end market. It sits across the full electronics value chain positioned in the consumables layer where recurring demand, pricing power, and scale matter most.

Qnity Electronics operates as a true “picks and shovels” provider to the semiconductor industry supplying the materials that make advanced AI and high-performance computing (HPC) chips possible.

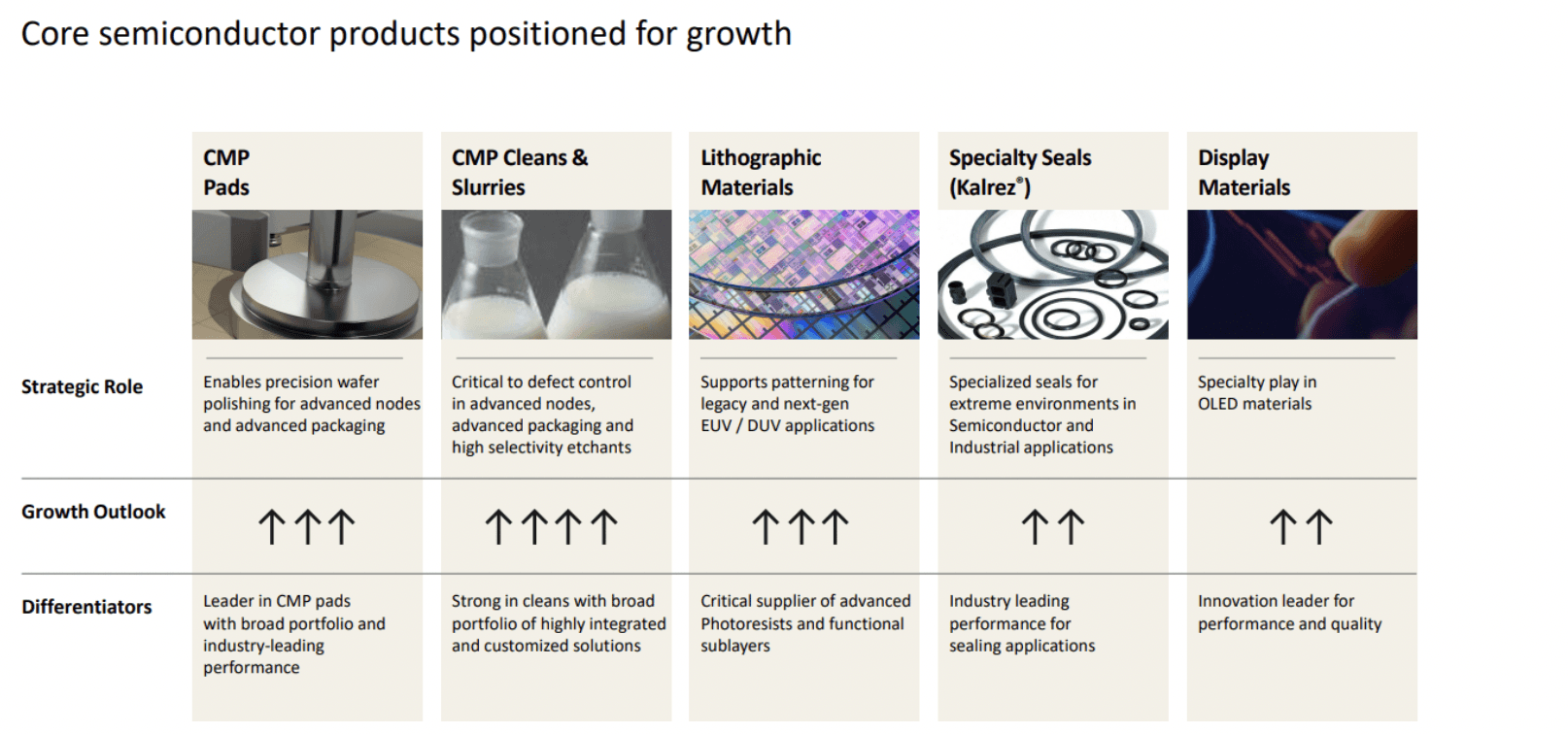

Roughly two-thirds of its portfolio is directly tied to the semiconductor value chain, giving it embedded exposure to global chip production.

Core capabilities include:

Chemical Mechanical Planarization (CMP)

Industry-standard polishing pads such as Ikonic and Visionpad, along with slurries used for ultra-precise wafer planarization. Every advanced chip requires multiple polishing steps making this a recurring, high volume business.

Photolithography Materials

Photoresists, anti-reflective coatings, and advanced overcoats essential for transferring increasingly complex circuit patterns onto wafers. As nodes shrink, material precision becomes even more critical.

Advanced Cleans

High-purity removal chemistries used in post-etch and post-CMP processes to maintain wafer integrity and yield reliability.

Beyond front-end fabrication, Qnity is positioned in one of the fastest-growing areas of the industry:

Advanced Packaging (Heterogeneous Integration)

As performance gains shift from transistor scaling to system-level integration, Qnity provides materials that enable the stacking and interconnection of logic, memory, and I/O components critical for next-generation AI workloads.

Thermal Management & Reliability

AI-driven processors, particularly GPUs, generate extreme heat loads.

Through Laird Thermal Interface Materials, Qnity addresses thermal dissipation challenges that directly impact chip performance and longevity.

Strategically, Qnity maintains relationships with companies representing approximately 80% of the global semiconductor market embedding it across leading fabs and device manufacturers.

Importantly, around 90% of its portfolio consists of unit-driven consumables.

That means revenue scales with chip volumes, not just equipment spending cycles creating structural exposure to semiconductor demand growth rather than lumpier CapEx waves.

This is infrastructure inside the AI ecosystem tied to volume, complexity, and the relentless push for performance.

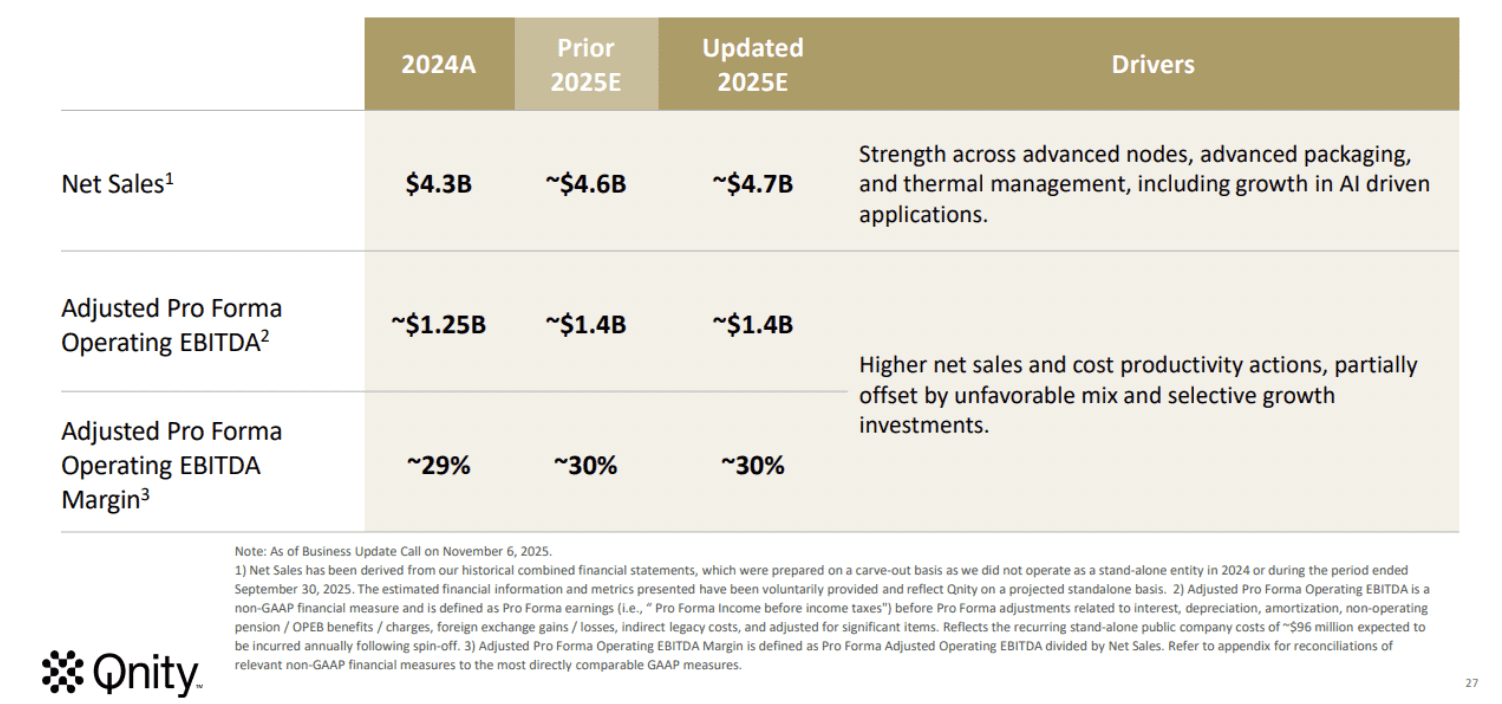

Full Year 2025 Pro Forma Estimates

The following projections reflect Qnity’s expected standalone performance for the fiscal year ending December 31, 2025:

• Net Sales: ~$4.7 billion (raised from prior guidance of $4.6 billion).

• Adjusted Pro Forma Operating EBITDA: ~$1.4 billion.

• Adjusted EBITDA Margin: ~30%.

• Pro Forma & Management Adjusted Net Income: ~$540 million.

• Estimated GAAP Net Income: ~$800 million.

• Adjusted Free Cash Flow: $600 million+.

At a 30% EBITDA margin and over $600 million in projected free cash flow, the numbers reinforce the consumables-driven model we’ve been highlighting high margins, strong cash conversion, and scalability tied to semiconductor volume growth rather than purely cyclical equipment demand.

RBC Capital Maintains Outperform on Qnity Electronics, Lowers Price Target to $110

Deutsche Bank Initiates Coverage On Qnity Electronics with Buy Rating, Announces Price Target of $92

Mizuho Maintains Outperform on Qnity Electronics, Lowers Price Target to $100

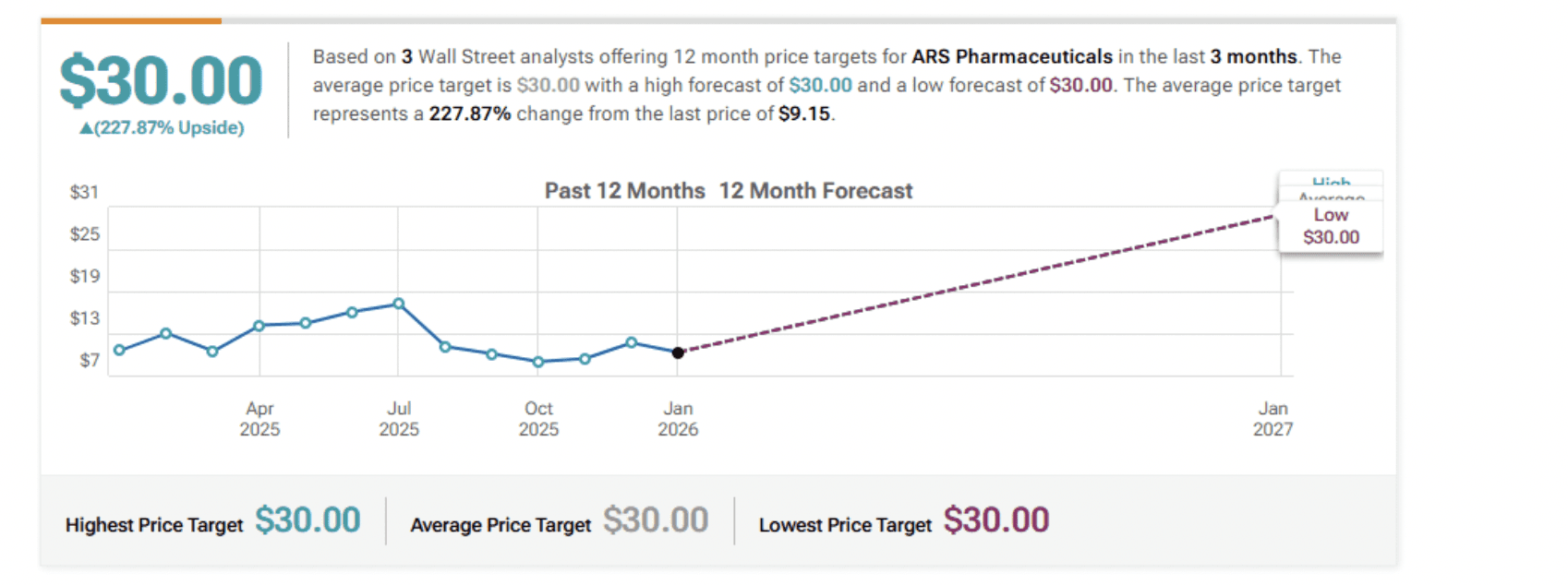

Company: ARS Pharmaceuticals

Quote: $SPRY

BT: $8-$12

ST: $18-$30

Sharks Opinion:

ARS Pharma has been on our radar for some time, and it caught attention last quarter with significant buying activity. The thesis is straightforward: the company is targeting the EpiPen market with an FDA-approved alternative that now has access to the China market a key catalyst that drove the stock higher last year.

Key Drivers:

Regulatory Approval: The lead product received FDA approval for use in China, boosting global commercial potential.

Competitive Edge: ARS’s main competitor was recently rejected by the FDA, expanding ARS’s market moat at a crucial moment.

Growth & M&A Potential: The company is positioned for strong organic growth and could be an attractive takeover target, thanks to its differentiated product and improved regulatory standing.

Context:

ARS Pharma has a seasoned management team that previously captured roughly 95% market share in the EpiPen segment, though under a less competitive environment. With a stronger regulatory position and access to new markets ARS now stands to benefit from both market expansion and strategic opportunities.

The setup suggests ARS is well-positioned for both near-term momentum and long-term value creation.

Description: ARS Pharmaceuticals Inc is a biopharmaceutical company focused on the development of novel, potentially first-in-class product candidate, neffy for the emergency treatment of Type I allergic reactions, including anaphylaxis. neffy is a proprietary composition of epinephrine with an absorption enhancer called Intravail, which allows neffy to provide injection- like absorption of epinephrine at a low dose, in a small, easy-to-carry, easy-to-use, rapidly administered and reliable nasal spray.

ARS Pharmaceuticals has built a meaningful moat around its epinephrine nasal spray platform, with patents covering composition of matter, formulation and dosing, methods of treatment, and proprietary delivery devices.

These protections extend through 2039 and center on a nasal spray that pairs epinephrine with a companion agent designed to enhance absorption through the nasal membrane eliminating the need for an injection.

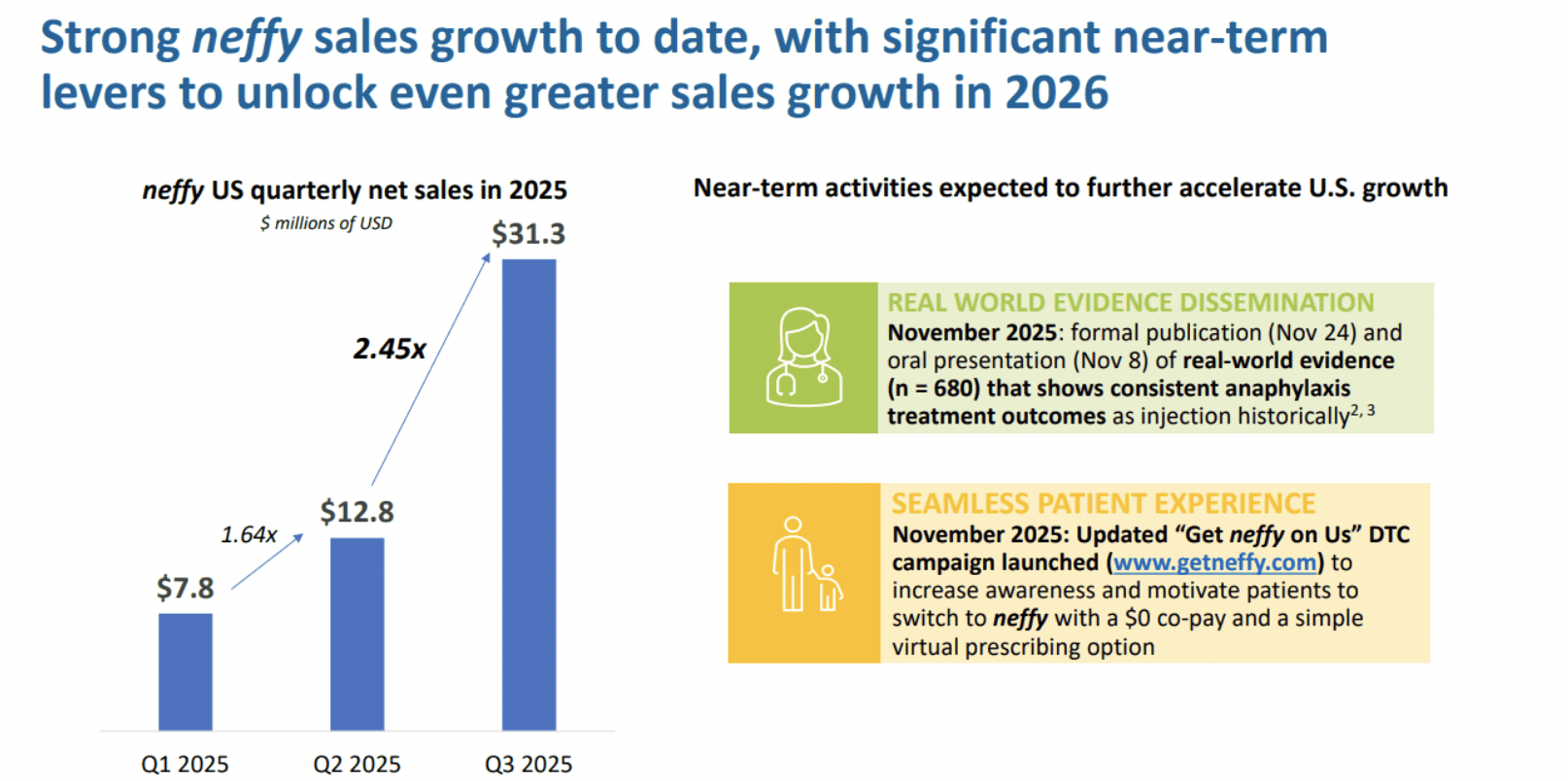

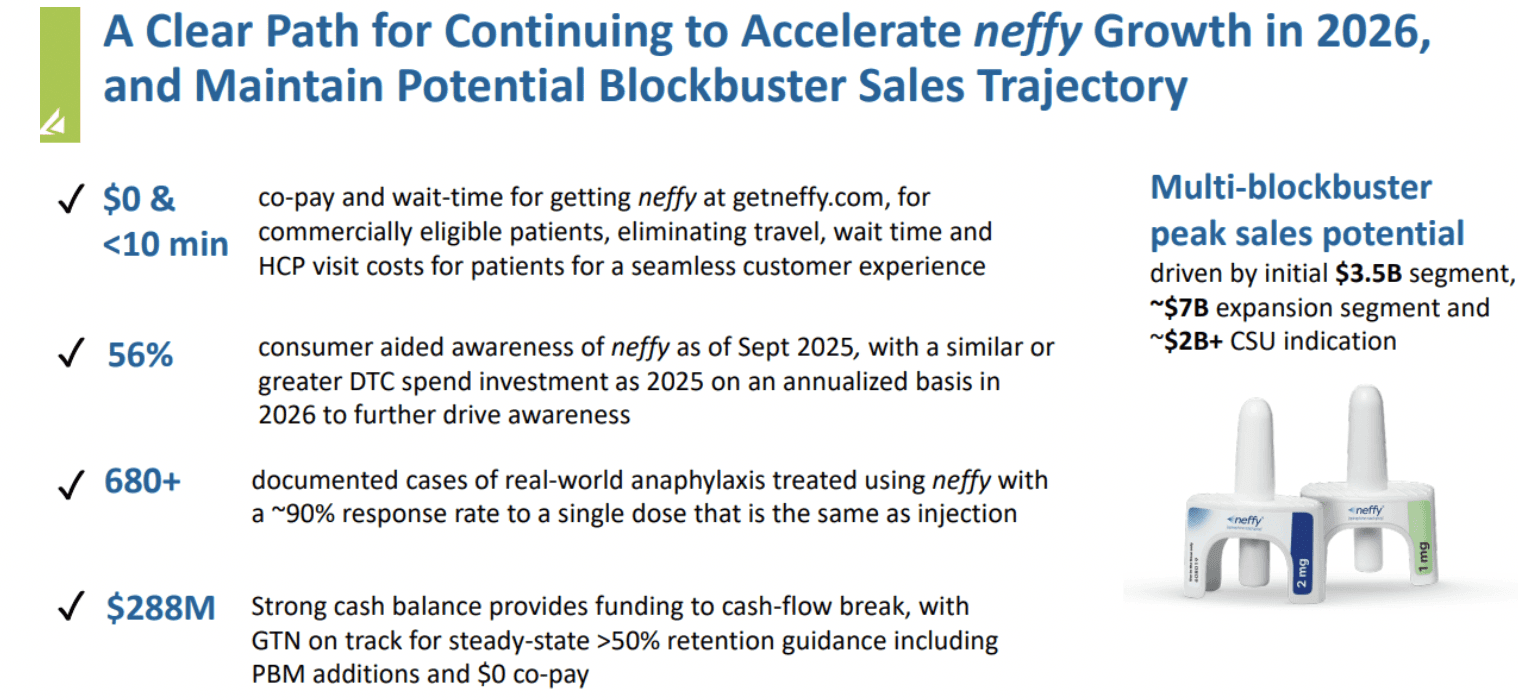

The market opportunity is substantial. Roughly 40 million Americans suffer from severe allergies, with about 20 million formally diagnosed and under physician care. That has translated into approximately 6.5 million epinephrine prescriptions, yet only 3.2 million patients actually fill them.

Needle hesitation remains a major friction point. A needle-free alternative like Neffy has the potential to expand both prescribing behavior and adherence. If Neffy were to meaningfully penetrate the U.S. EpiPen market at roughly $199 per dose, the opportunity could approach $600 million annually, excluding incremental demand from first responders, schools, and clinical inventory.

International markets add another layer of upside. While pricing outside the U.S. is typically lower, global allergy prevalence and expanding regulatory approvals still represent a meaningful growth vector over time.

Roth Capital Initiates Coverage On ARS Pharmaceuticals with Buy Rating, Announces Price Target of $40

Scotiabank Initiates Coverage On ARS Pharmaceuticals with Sector Outperform Rating, Announces Price Target of $30

Raymond James Maintains Strong Buy on ARS Pharmaceuticals, Raises Price Target to $28

Company: Bullish

Quote: $BLSH

BT: $28

ST: $42 (until btc re rates)

Sharks Opinion:

Bullish went public last year during the crypto frenzy, experiencing a heavily hyped IPO. Since then, the stock has retraced from its peak, now trading near its original listing price of $31 after a $100 drop. With Bitcoin prices softening, this presents a potential entry point for exposure to the digital asset sector ahead of a potential rebound.

Key Catalysts:

Bullish is the 6th largest institutional holder of Bitcoin, with roughly 24,300 BTC (~$1.5B USD at current prices).

Institutionalization Thesis: The company is positioned to benefit from the growing entry of traditional finance into crypto. Its regulatory-first approach, strong balance sheet, and synergistic business model aim to capture a significant portion of value as digital assets become mainstream. BLSH represents a strategic way to gain institutional crypto exposure while betting on broader market adoption and recover

Description: Bullish is an institutionally focused global digital asset platform focused on providing market infrastructure and information services. Its objective is to provide mission critical products and services that are designed to help institutions grow their businesses, empower individual investors, and drive the adoption of stablecoins, digital assets, and blockchain technology. It expanded its product offering to provide trusted insights, authoritative news, data, indices and transparent analysis to the digital assets industry while facilitating partnerships, investment opportunities, and community engagement through its flagship Consensus conference.

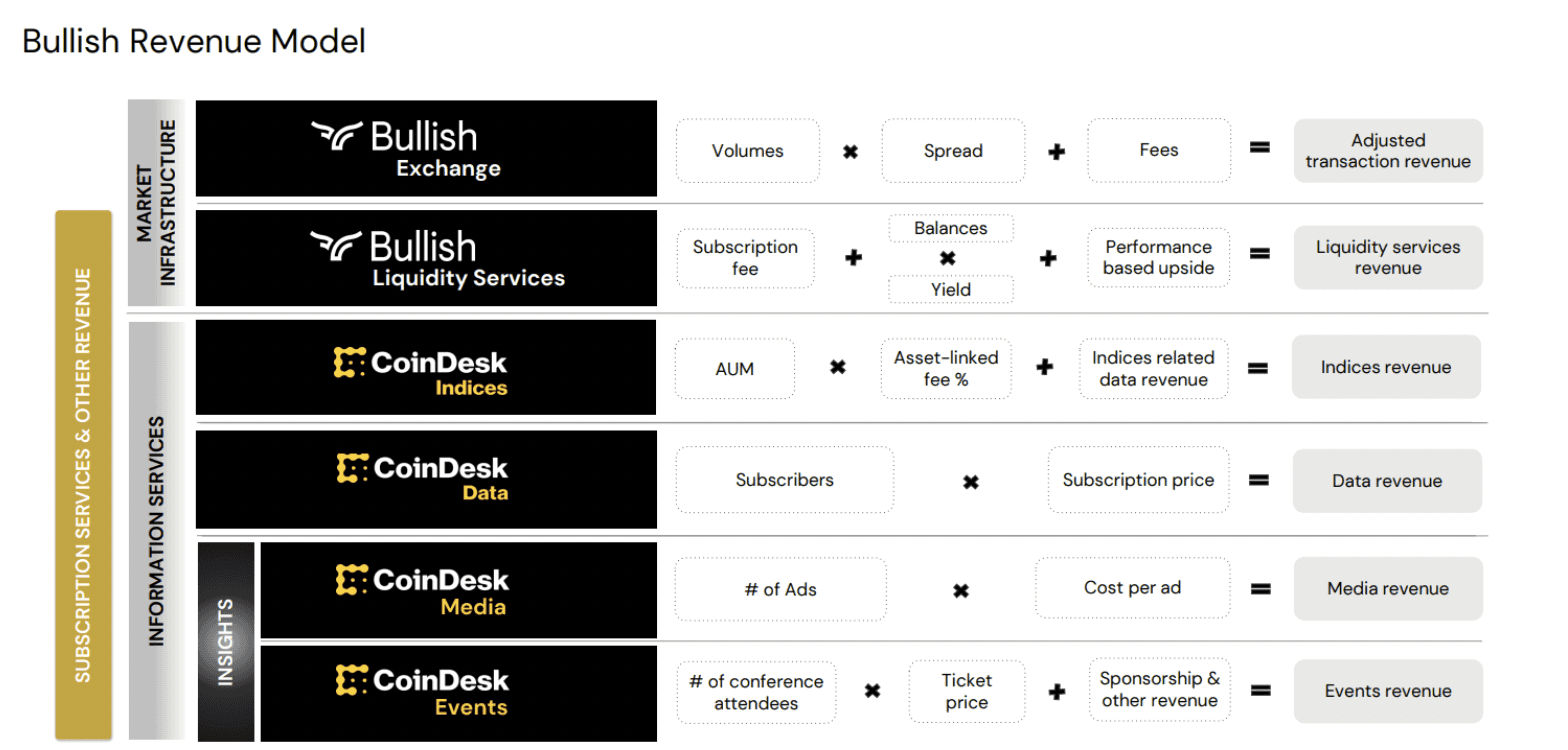

Bullish is an institutionally-focused digital asset platform with a dual business model: a regulated global exchange (Market Infrastructure) and a data/media/events arm.

Revenue Engines:

Exchange Operations (Transaction-Based)

Trading Fees: Charges on spot, margin, and derivatives trades. In 2026, the focus has shifted toward regulated derivatives, which carry higher margins.

Automated Market Making (AMM): Bullish uses proprietary algorithms and its treasury to provide liquidity, earning from the bid-ask spread.

Liquidity & Stablecoin Services: Institutional clients pay for guaranteed access to deep liquidity and stablecoins.

Information Services (Recurring Revenue)

CoinDesk Indices: Licenses proprietary benchmarks like the XBX Bitcoin Index to ETFs and banks, tracking over $41B in AUM.

CoinDesk Data & Insights: Sells real-time and historical market data, research, and APIs to hedge funds and trading firms.

Media & Events: Generates advertising revenue and hosts the Consensus conference, one of the largest crypto industry gatherings globally.

Thesis: Bullish aims to leverage its regulatory-first approach, dual revenue streams, and experienced management to become the dominant market infrastructure and information services provider in the institutional digital asset economy.

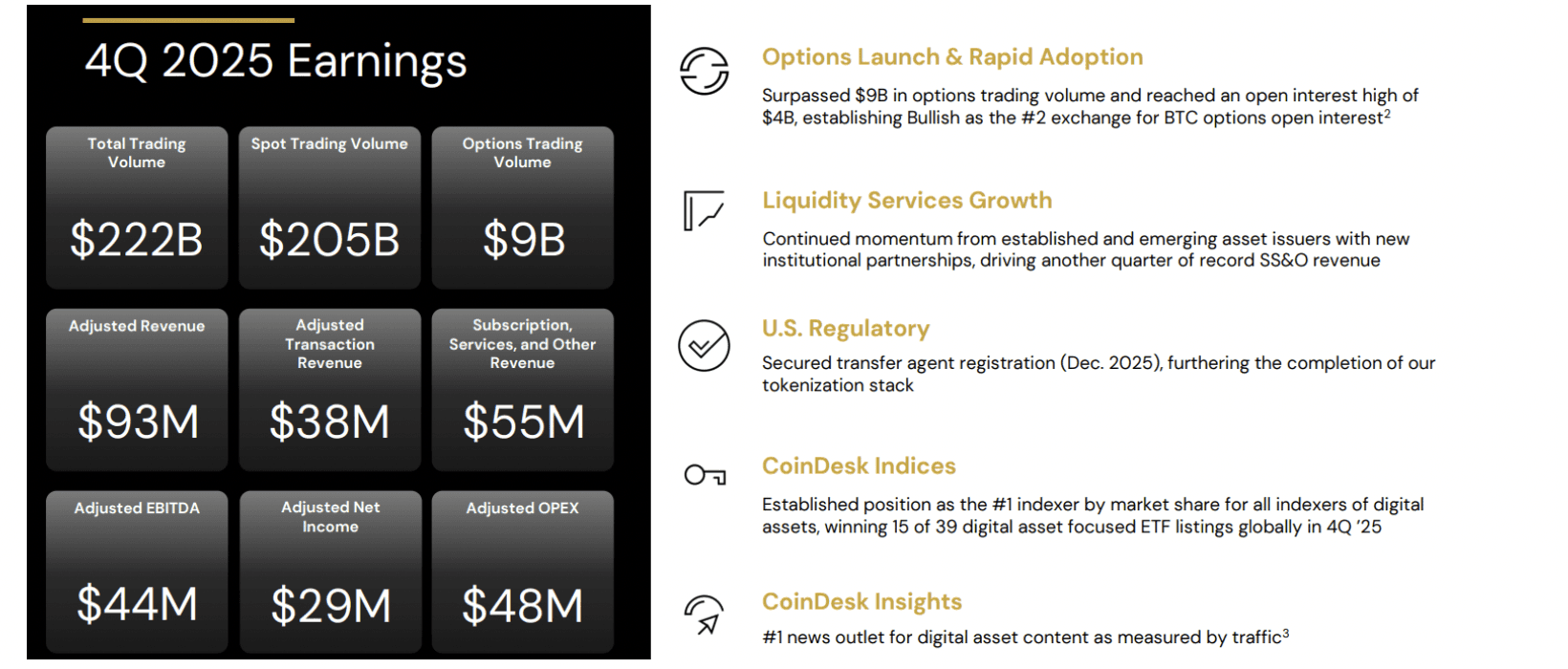

Q4 2025:

Adjusted Revenue: $92.5M, up nearly 70% YoY.

Adjusted EBITDA: $44.5M, hitting a record 48% margin.

GAAP Net Income: Loss of $563.6M ($3.73/share), mainly due to digital asset remeasurement.

Options Trading: Surpassed $9B in total volume, capturing ~29% of the Bitcoin options market.

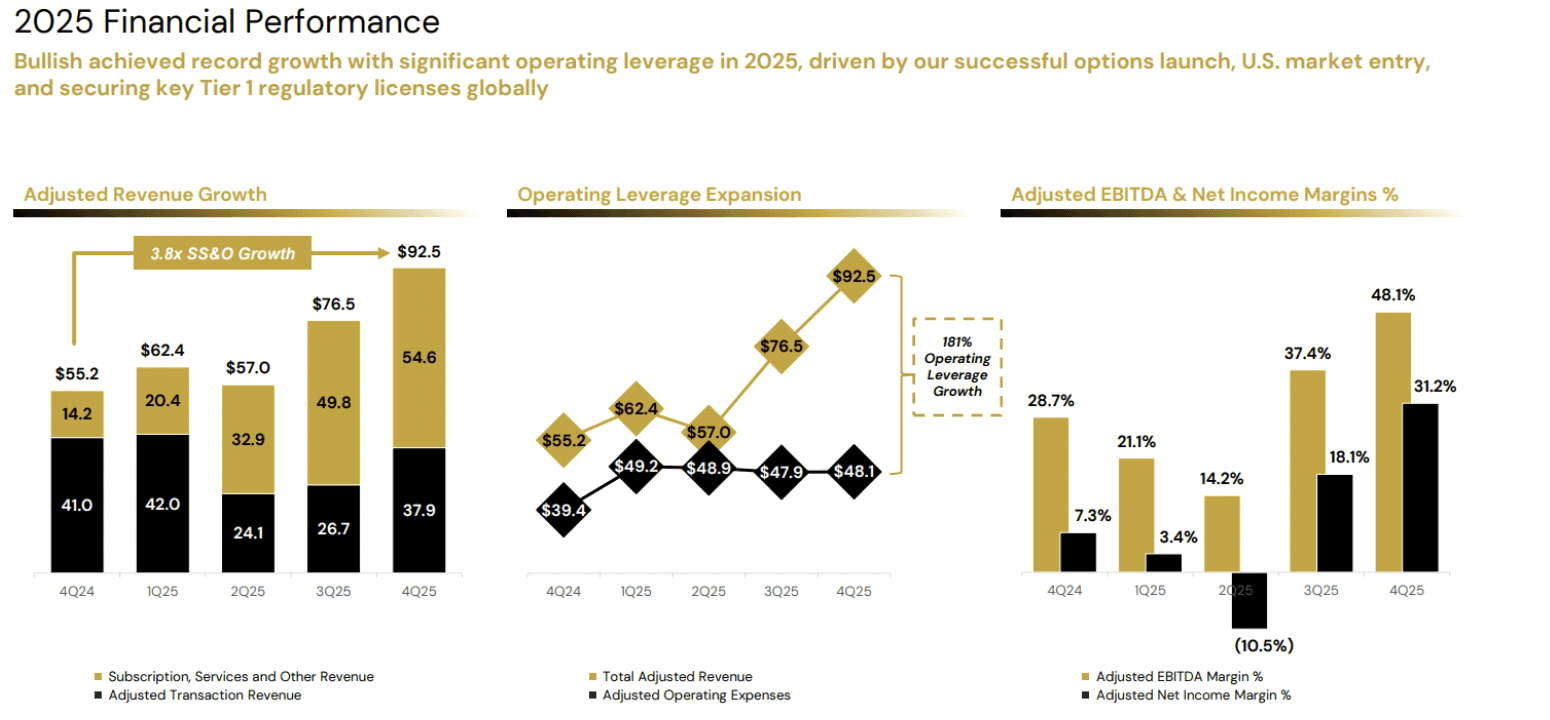

Full Year 2025:

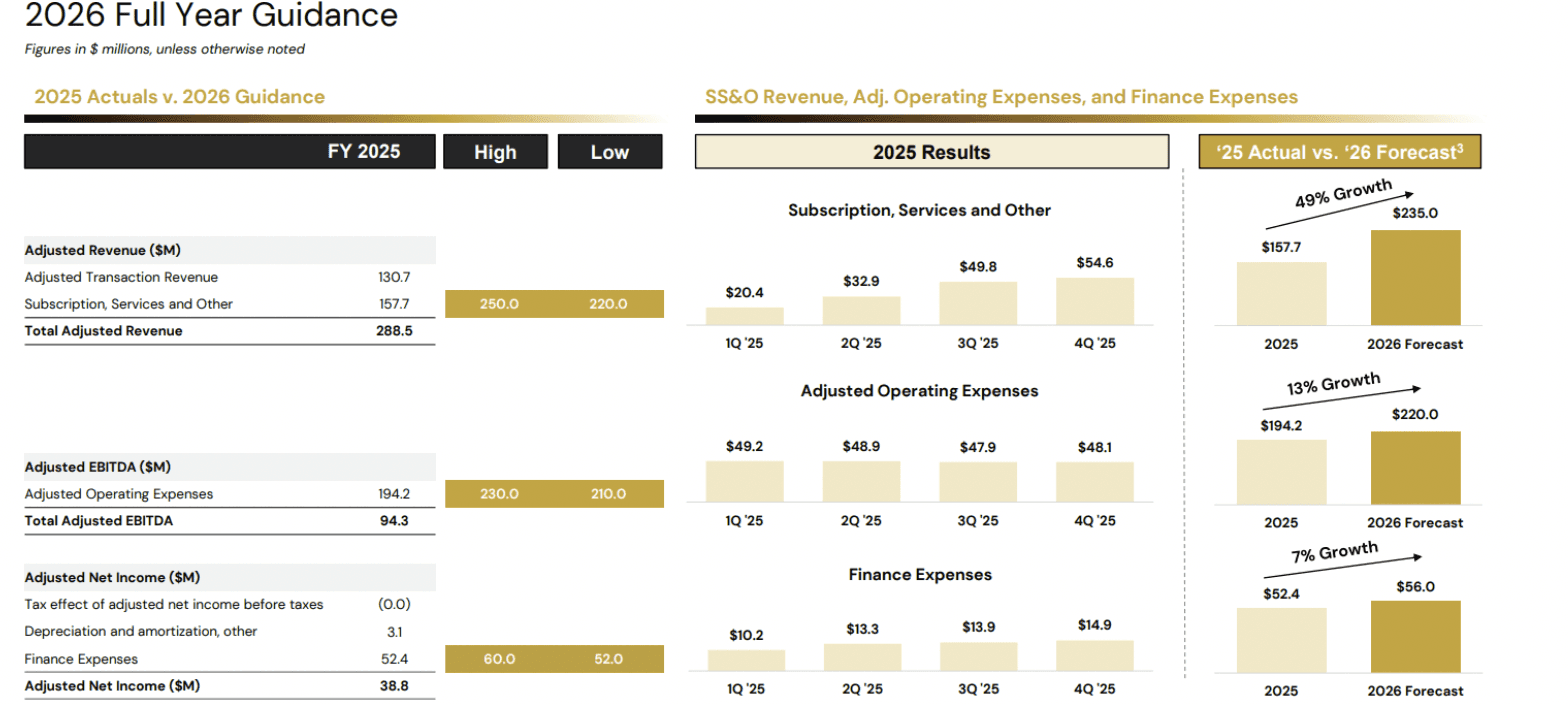

Total Adjusted Revenue: $288.5M, +35% YoY.

Subscription & Services (SS&O): $157.7M, up 160% YoY, showing a clear shift toward recurring revenue.

Adjusted EBITDA: $94.3M.

Context:

Bullish has seen a dramatic turnaround over the past two years:

2022: Net loss of $4.25B

2023: Net income of $1.30B

2024: Net income of $79.6M

These swings reflect fair value accounting on its large digital asset holdings, which causes extreme volatility in GAAP results. Adjusted (non-IFRS) metrics provide a clearer picture of operational performance. For Q1 2025 the company reported a net loss of $349M, but Adjusted EBITDA remained positive at $13M, underscoring the underlying operational strength.

Bullish – 2026 Outlook

Management issued optimistic guidance for fiscal 2026: SS&O Revenue: $220M–$250M, implying ~50% YoY growth.

Adjusted Operating Expenses: $210M–$230M.

Next Earnings Date: Q1 2026 results expected April 23, 2026.

This outlook highlights continued growth in recurring revenue streams and operational scalability as Bullish further solidifies its position in institutional digital assets.

JP Morgan Maintains Neutral on Bullish, Lowers Price Target to $41

Rosenblatt Maintains Buy on Bullish, Lowers Price Target to $39

Citigroup Maintains Buy on Bullish, Lowers Price Target to $67

Canaccord Genuity Maintains Buy on Bullish, Lowers Price Target to $50