This watchlist highlights the current names we’re actively tracking for potential trade setups.

These are not trade alerts. All official entries will be sent in real time, consistent with the format used in the weekly investment letter.

Company: Qnity Electronics

Quote: $Q

BT: We didn't get the dip we wanted on earnings so now we hawk tape volume daily to see when an ideal entry will be, At the moment the stock is ranging with the overall stock market hasn't made a clear stance in which direction its going despite the recent milestone and parterships the company has won.

ST: $145 (long term)

Sharks Opinion:

Digging through the latest 13F filings, one name consistently showed up across a wide range of institutional portfolios Qnity.

That kind of repeat exposure is usually a signal worth paying attention to, especially when it’s happening quietly without much retail attention.

When most investors think about the AI arms race, they immediately jump to chip designers like NVIDIA or AMD, and sometimes the foundries like TSMC.

But what often gets overlooked is the layer underneath all of that the consumables. The highly specialized chemicals and materials required to actually manufacture those chips at scale.

That’s exactly where Qnity sits. Similar to Chemours, Qnity was spun out of DuPont, but the business model is fundamentally different. While Chemours leans more into cooling and infrastructure tied to data centers, Qnity operates directly inside the semiconductor production process itself.

That creates a much more recurring and volumedriven revenue stream, rather than one dependent on big-ticket fab buildouts.

In simple terms, they’re selling the “ingredients,” not the machines.

That gives Qnity a different kind of exposure to the AI trade. It’s less about timing the capex cycle and more about ongoing production demand, which tends to be more stable and predictable.

On top of that, specialized chemical suppliers often benefit from pricing power due to high switching costs and tight integration into customer processes.

From our perspective, this is one of those underthe-radar ways to play the semiconductor and AI theme without chasing the obvious names that have already seen massive multiple expansion.

The story here isn’t flashy, but it’s structurally strong recurring demand, embedded positioning, and a valuation that still hasn’t fully caught up to where it probably should be relative to peers.

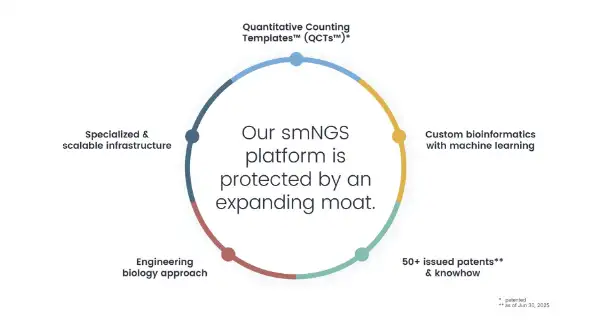

Description: Qnity is a specialty chemicals company created in 2025 after being spun off from DuPont. It sells chemicals and materials to the semiconductor industry, which generates the majority of sales, and also the electronics industry. Qnity specializes in materials science, including supplying key materials required to manufacture semiconductors and interconnected devices.

Qnity is stepping out as one of the largest pure-play electronics materials companies in the market backed by a 50+ year legacy, 10,000 employees globally, nearly 40 manufacturing sites, and close to 20 R&D facilities.

This isn’t a startup story. It’s an infrastructure story.

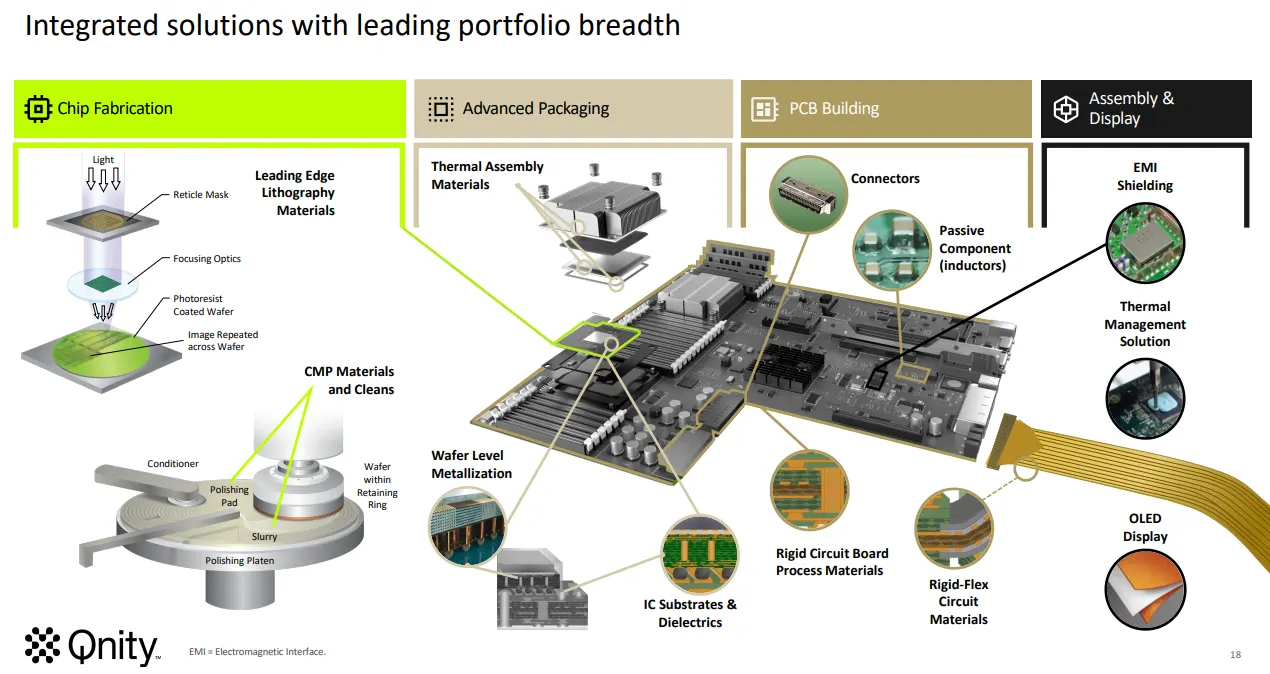

The company focuses on differentiated electronic materials supplying the critical consumables used in semiconductor manufacturing, advanced packaging, interconnects, thermal management, and display technologies.

Roughly 90% of revenue comes from consumables and unit-driven products, which creates recurring demand tied directly to chip volumes rather than volatile CapEx cycles.

Core segments break down as follows:

Semiconductor Technologies (~55% of revenue)

Solutions for chip fabrication, including CMP pads and photoresists materials required every time a wafer is processed.

Interconnect Solutions (~45% of revenue)

Advanced packaging, thermal management, and circuit imaging solutions that enable increasingly complex chip architectures.

Revenue exposure is diversified across the electronics ecosystem:

Chip fabrication: 50%

PCB building: 20%

Assembly & display: 20%

Advanced packaging: 10%

With customers in more than 80 countries, Qnity isn’t dependent on a single region, foundry, or end market. It sits across the full electronics value chain positioned in the consumables layer where recurring demand, pricing power, and scale matter most.

Qnity Electronics operates as a true “picks and shovels” provider to the semiconductor industry supplying the materials that make advanced AI and high-performance computing (HPC) chips possible.

Roughly two-thirds of its portfolio is directly tied to the semiconductor value chain, giving it embedded exposure to global chip production.

Core capabilities include:

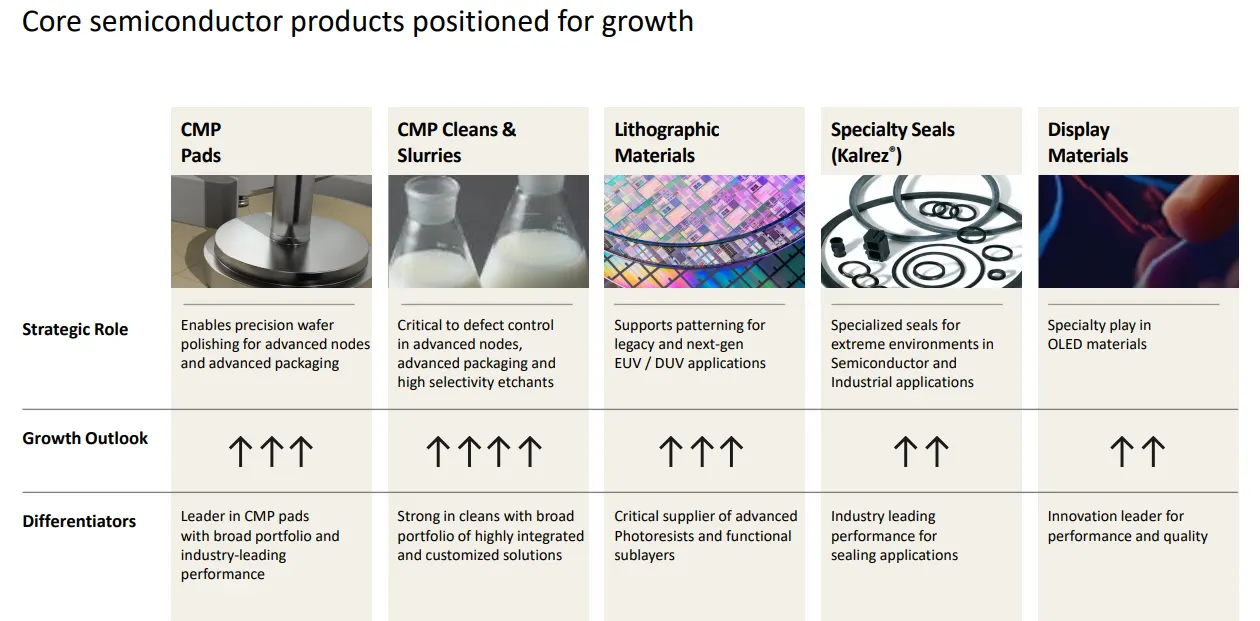

Chemical Mechanical Planarization (CMP)

Industry-standard polishing pads such as Ikonic and Visionpad, along with slurries used for ultra-precise wafer planarization. Every advanced chip requires multiple polishing steps making this a recurring, high-volume business.

Photolithography Materials

Photoresists, anti-reflective coatings, and advanced overcoats essential for transferring increasingly complex circuit patterns onto wafers. As nodes shrink, material precision becomes even more critical.

Advanced Cleans

High-purity removal chemistries used in post-etch and post-CMP processes to maintain wafer integrity and yield reliability. Beyond front-end fabrication, Qnity is positioned in one of the fastest-growing areas of the industry:

Advanced Packaging (Heterogeneous Integration)

As performance gains shift from transistor scaling to system-level integration, Qnity provides materials that enable the stacking and interconnection of logic, memory, and I/O components critical for next-generation AI workloads.

Thermal Management & Reliability

AI-driven processors, particularly GPUs, generate extreme heat loads. Through Laird Thermal Interface Materials, Qnity addresses thermal dissipation challenges that directly impact chip performance and longevity.

Strategically, Qnity maintains relationships with companies representing approximately 80% of the global semiconductor market embedding it across leading fabs and device manufacturers.

Importantly, around 90% of its portfolio consists of unit-driven consumables.

That means revenue scales with chip volumes, not just equipment spending cycles creating structural exposure to semiconductor demand growth rather than lumpier CapEx waves.

This is infrastructure inside the AI ecosystem tied to volume, complexity, and the relentless push for performance.

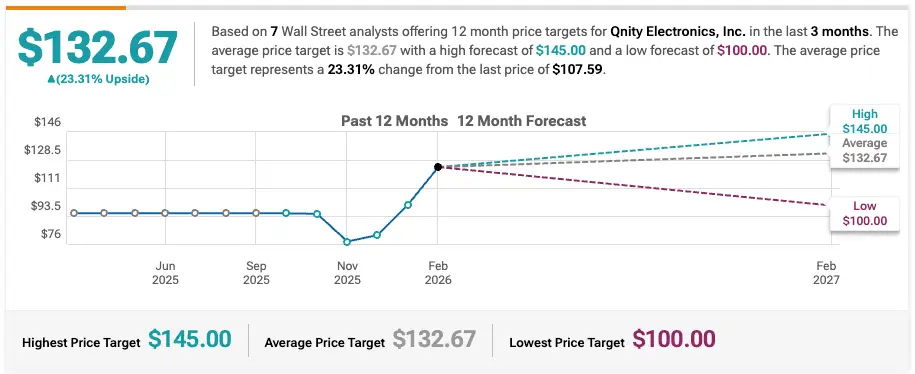

RBC Capital Maintains Outperform on Qnity Electronics, Raises Price Target to $139

Keybanc Maintains Overweight on Qnity Electronics, Raises Price Target to $147

Deutsche Bank Initiates Coverage On Qnity Electronics with Buy Rating, Announces Price Target of $92

Mizuho Maintains Outperform on Qnity Electronics, Lowers Price Target to $100

Company: BillionToOne, Inc

Quote: $BLLN

BT: Ideally, we’d like to see BLLN drift a bit lower into the IPO lockup expiration window that’s typically where early venture money starts ringing the register and supply quietly hits the tape.

That kind of overhang doesn’t always show up in headlines, but you’ll feel it in the price action.

Insider selling in these windows tends to create that short-term pressure we look for not as a red flag, but as a mechanism for better entries.

That said, this isn’t a liquid name. Volume is thin, spreads can widen, and when it moves, it tends to move fast.

Because of that, there’s no reason to force anything here. We’re content sitting back and letting the tape show its hand before stepping in.

ST: That range is anchored almost entirely on 2026 guidance.

If the company strings together a few clean quarters and shows a real path toward ~$500M in ARR, you can justify the market stretching toward a ~10x multiple which gets you into that range.

Sharks Opinion:

BLLN fits the exact profile we tend to stalk recent IPO, sharp post-listing drawdown, and now starting to settle into a more realistic valuation zone. That type of reset is usually where opportunity starts to build, not where it ends.

Under the hood, this isn’t just another biotech story. The core here is their QCT platform, and everything else ladders off that prenatal diagnostics today, oncology tomorrow, and eventually a broader push into areas like MRD, early detection, and AI-assisted personalized medicine.

They’re positioning themselves right at the intersection of molecular diagnostics and precision medicine which, if executed properly, is one of the more powerful long-term themes in healthcare.

What stands out is the balance: strong top-line growth paired with a credible path toward profitability. That’s not something you see often in earlier-stage names in this space.

After the pullback into the ~$70 range, valuation has compressed to roughly ~10x sales on Q4 numbers. Still not cheap but materially more digestible given the growth profile.

From here, the entire story hinges on execution. If they continue to hit guidance, maintain growth velocity, and drive adoption of their testing platform, the market will likely reward that with multiple expansion over time.

If adoption slows or volumes plateau, this kind of name can unwind just as quickly as it built momentum.

So for now, this sits in that bucket: high-upside, higher-volatility, and very much tape-dependent. We’re not chasing we’re watching

Description: BillionToOne Inc is a precision diagnostics company revolutionizing molecular testing with its patented Quantitative Counting Templates (QCT) platform. This technology enables ultrasensitive, single-molecule DNA quantification, making genetic testing more accurate, affordable, and accessible. The company serves prenatal screening and oncology markets with non-invasive tests that detect fetal genetic risks and monitor cancer therapy response.

BillionToOne, Inc. is a healthcare diagnostics company focused on molecular counting technology for single-molecule DNA detection.

The company specializes in non-invasive prenatal testing (NIPT) and oncology liquid biopsy solutions, enabling earlier and more precise disease detection. Through its differentiated technology platform and expanding test portfolio, BillionToOne is positioning itself to address critical gaps in precision medicine and modern clinical diagnostics.

The company’s broader mission is to democratize access to precision diagnostics by making advanced molecular testing more affordable, accurate, and scalable across healthcare systems.

At the center of this strategy is its proprietary technology platform known as Quantitative Counting Templates (QCT). QCT enables highly precise DNA quantification without relying on complex next-generation sequencing infrastructure.

As a result, hospitals and clinical laboratories can run highly sensitive genetic tests using standard laboratory equipment, improving accessibility while also reducing costs and turnaround times.

BillionToOne has applied this core technology across two major healthcare verticals. The first is prenatal screening, where the company has become one of the fastest-growing providers of non-invasive prenatal testing in the United States. The second is oncology diagnostics, where the platform is being expanded into liquid biopsy applications for cancer monitoring, therapy response tracking, and minimal residual disease detection.

Product Portfolio

UNITY Screen™ – A non-invasive prenatal screening test capable of detecting fetal chromosomal abnormalities and recessive genetic conditions using a single maternal blood sample.

UNITY Complete™ – A comprehensive prenatal testing solution that combines maternal carrier screening with fetal chromosomal analysis in a single integrated test.

ONCOCOUNT™ An oncology-focused platform designed to quantify circulating tumor DNA (ctDNA), enabling cancer monitoring, recurrence detection, and treatment response tracking through minimally invasive liquid biopsy testing.

Through these products and its scalable molecular counting platform, BillionToOne is building a diagnostics ecosystem aimed at expanding the reach of precision medicine across both prenatal care and oncology.

Financial Highlights

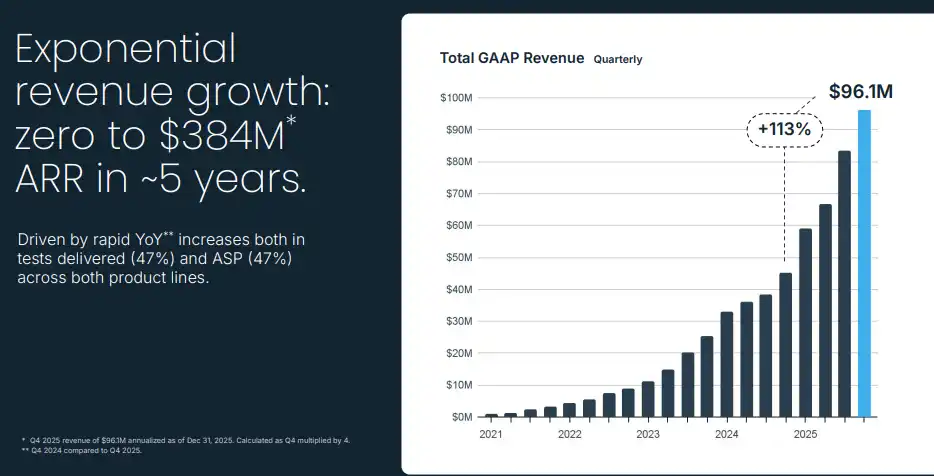

BillionToOne delivered a strong finish to 2025, with results highlighting rapid revenue expansion, improving profitability, and accelerating clinical adoption across both its prenatal and oncology testing platforms.

Revenue Growth:

Total revenue reached $96.1 million in Q4 2025, compared to $45.1 million in Q4 2024, representing 113% year-over-year growth.

Prenatal Testing Revenue:

Prenatal clinical testing generated $86.1 million in Q4 2025, an increase of 99% year-over-year, continuing to be the company’s primary growth driver.

Oncology Testing Revenue:

Oncology clinical testing revenue totaled $9.1 million, more than eight times higher than the $1.1 million recorded in Q4 2024, reflecting rapid early adoption of the company’s oncology diagnostics platform.

Profitability Expansion:

Gross profit margin improved significantly to 71% in Q4 2025, compared to 57% in Q4 2024, representing a 14-percentage-point expansion year-over-year as scale and operational efficiency improved.

Testing Volume:

BillionToOne delivered approximately 170,000 tests in Q4 2025, up from 116,000 tests in Q4 2024, representing 47% growth in testing volume.

Operating Income:

The company generated $10.3 million in operating income during the quarter, a notable improvement compared to an operating loss of $11.7 million in Q4 2024, signaling the business is moving toward sustained profitability.

Cash Flow:

Net cash flow, excluding proceeds from the company’s IPO, totaled $8.8 million in Q4 2025 and $12.5 million for the full year 2025, demonstrating improving financial sustainability.

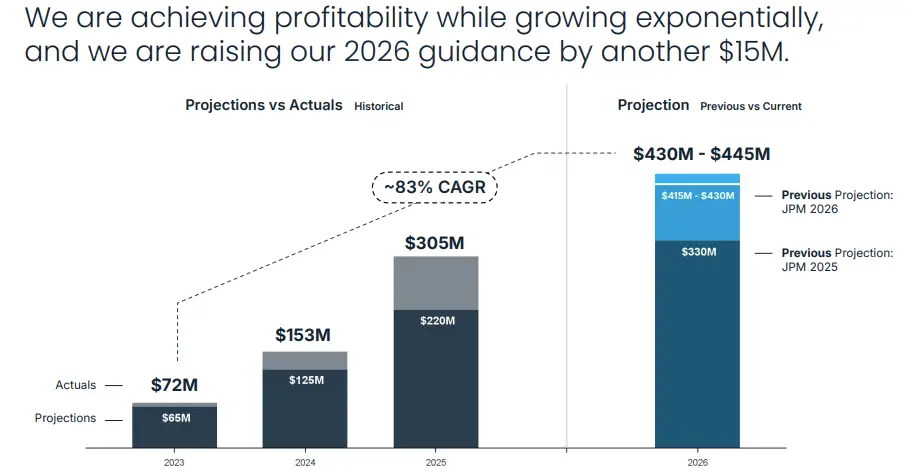

Forward Guidance:

Management raised full-year 2026 revenue guidance to a range of $430 million to $445 million, representing 41% to 46% expected growth compared to 2025. Additionally, the company expects to achieve positive operating income for the full year 2026, marking a key milestone in BillionToOne’s transition from highgrowth startup to profitable diagnostics platform.

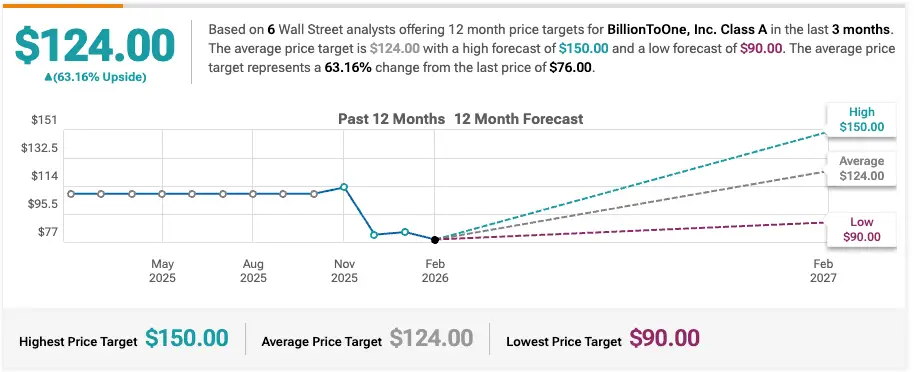

Wells Fargo Maintains Equal-Weight on BillionToOne, Lowers Price Target to $90

Guggenheim Reiterates Buy on BillionToOne, Maintains $120 Price Target

BTIG Maintains Buy on BillionToOne, Lowers Price Target to $140

JP Morgan Maintains Overweight on BillionToOne, Lowers Price Target to $145

Company: Bullish

Quote: $BLSH

BT: $35-$40

ST: $60 + its all pending on BTC price

Sharks Opinion:

Bullish came public right into the peak of the crypto euphoria one of those IPOs where hype did most of the heavy lifting early. Since then, reality has set in. The stock has round-tripped back toward its listing price around $31 after shedding roughly $100 from the highs.

That type of unwind isn’t unique it’s what most “theme-first” IPOs do once the narrative cools off and liquidity dries up.

Now you’ve got it sitting back near its base while crypto, specifically Bitcoin, has softened.

That combination starts to get interesting not because it’s cheap outright, but because expectations have been reset.

This becomes less about chasing momentum and more about positioning ahead of a potential turn in the underlying asset.

Key Catalysts:

Bullish isn’t just another proxy they’re a meaningful holder themselves.

Sitting on ~24,300 BTC (~$1.5B), they’ve effectively embedded balance sheet exposure into the story. That cuts both ways, but in a recovering tape, it becomes a tailwind.

The broader angle here is the institutionalization trade.

They’re leaning into a regulatory-first framework, which, whether the market likes it or not, is likely the direction the space continues moving. As traditional finance slowly integrates with crypto infrastructure, platforms positioned to bridge that gap tend to capture outsized flows.

It’s not just about trading volumes it’s about becoming part of the rails.

At its core, BLSH is a levered bet on two things:

A recovery in digital assets

Continued institutional adoption of crypto If both of those trends reaccelerate, names like this don’t just recover they tend to rerate.

If not, you’re left with a stock that trades sideways with the underlying sentiment.

For now, it’s another one where the setup is improving, but confirmation still needs to come from the tape.

Description: Bullish is an institutionally focused global digital asset platform focused on providing market infrastructure and information services. Its objective is to provide mission critical products and services that are designed to help institutions grow their businesses, empower individual investors, and drive the adoption of stablecoins, digital assets, and blockchain technology. It expanded its product offering to provide trusted insights, authoritative news, data, indices and transparent analysis to the digital assets industry while facilitating partnerships, investment opportunities, and community engagement through its flagship Consensus conference.

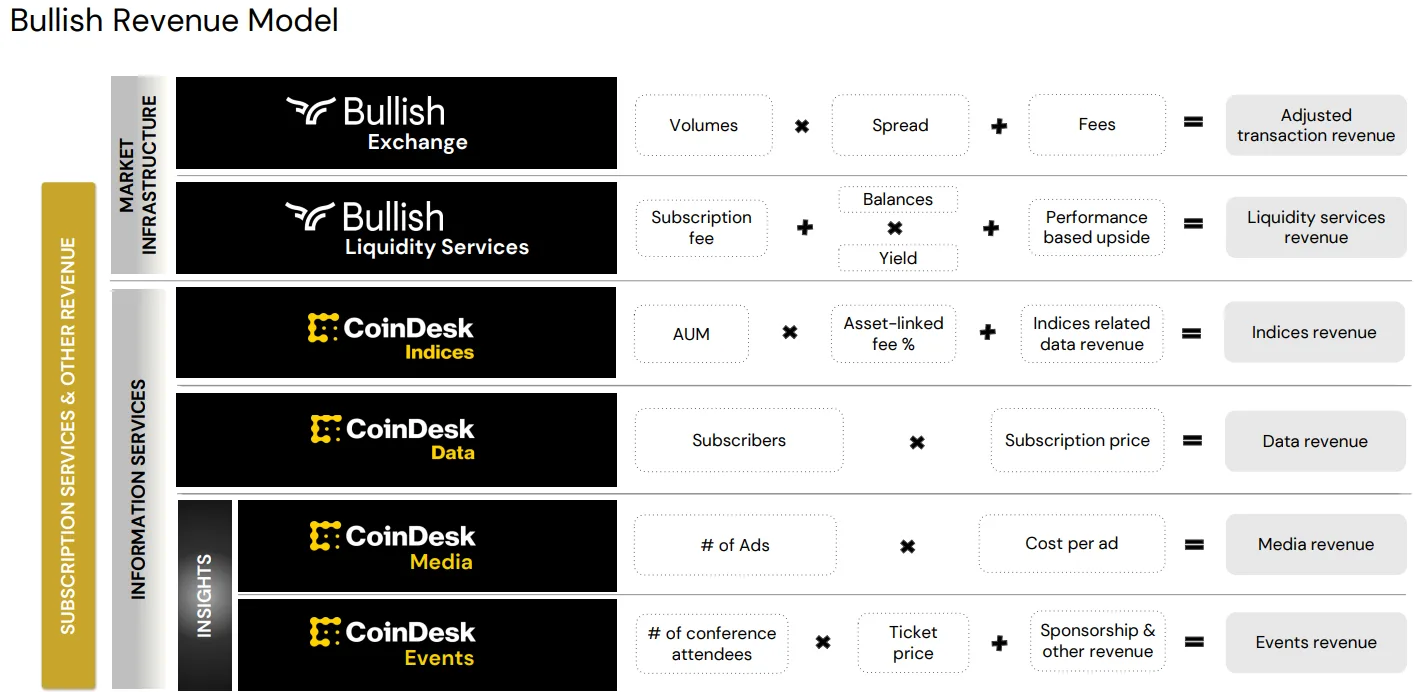

Bullish is an institutionally-focused digital asset platform with a dual business model: a regulated global exchange (Market Infrastructure) and a data/media/events arm.

Revenue Engines:

Exchange Operations (Transaction-Based)

Trading Fees: Charges on spot, margin, and derivatives trades. In 2026, the focus has shifted toward regulated derivatives, which carry higher margins.

Automated Market Making (AMM): Bullish uses proprietary algorithms and its treasury to provide liquidity, earning from the bid-ask spread.

Liquidity & Stablecoin Services: Institutional clients pay for guaranteed access to deep liquidity and stablecoins.

Information Services (Recurring Revenue)

CoinDesk Indices: Licenses proprietary benchmarks like the XBX Bitcoin Index to ETFs and banks, tracking over $41B in AUM.

CoinDesk Data & Insights: Sells real-time and historical market data, research, and APIs to hedge funds and trading firms.

Media & Events: Generates advertising revenue and hosts the Consensus conference, one of the largest crypto industry gatherings globally.

Thesis: Bullish aims to leverage its regulatory-first approach, dual revenue streams, and experienced management to become the dominant market infrastructure and information services provider in the institutional digital asset economy.

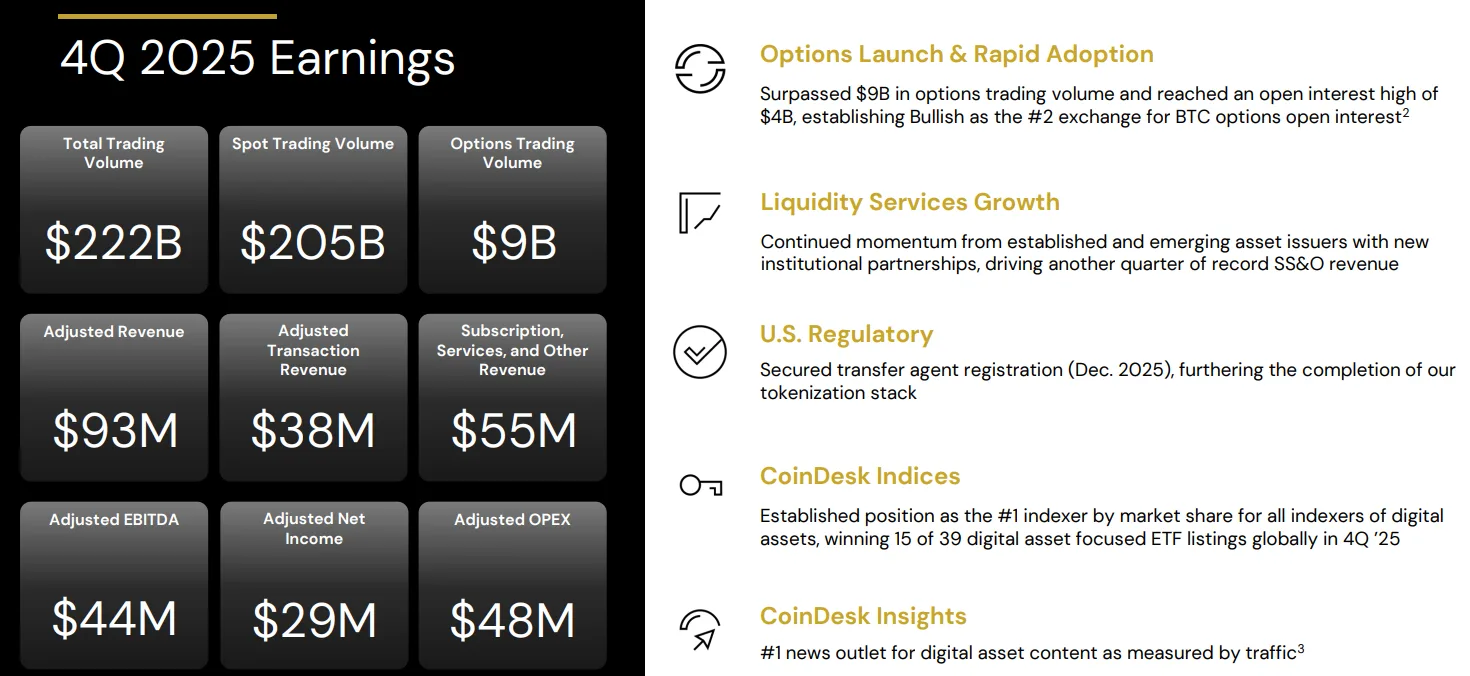

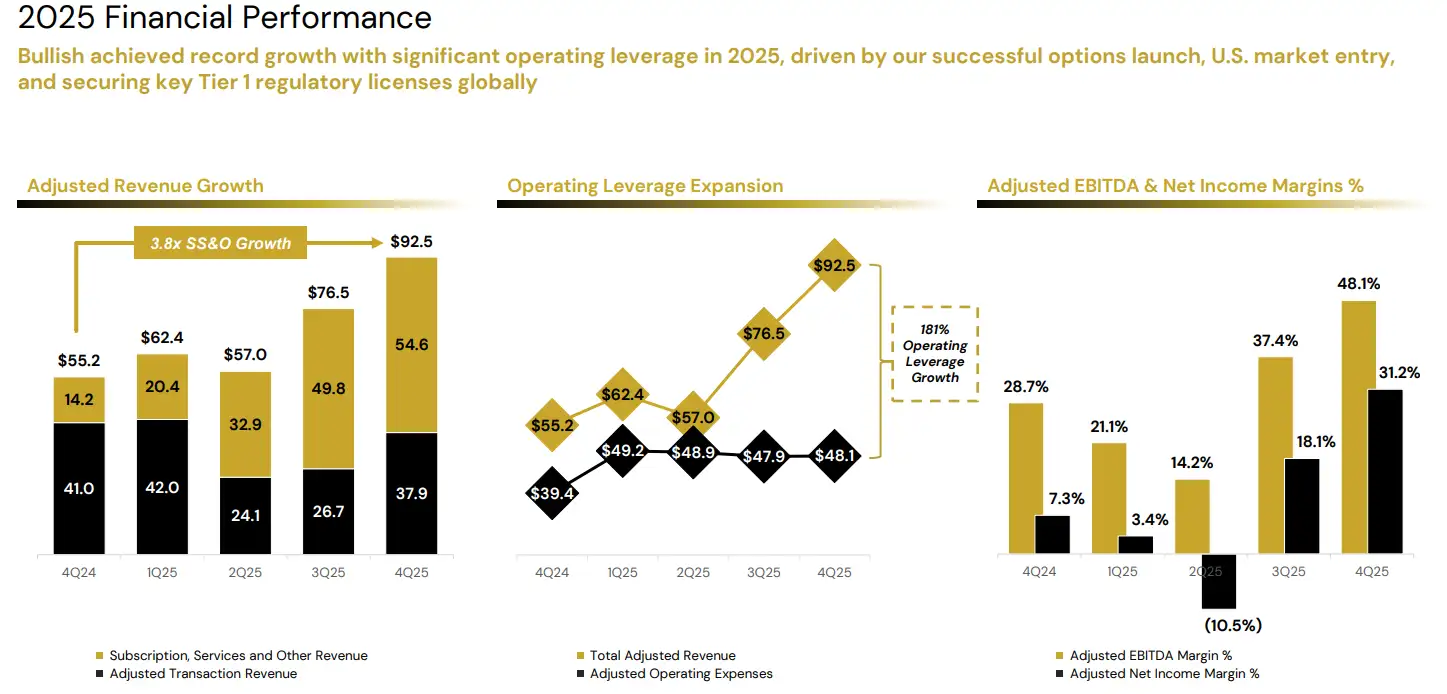

Q4 2025:

Adjusted Revenue: $92.5M, up nearly 70% YoY.

Adjusted EBITDA: $44.5M, hitting a record 48% margin.

GAAP Net Income: Loss of $563.6M ($3.73/share), mainly due to digital asset remeasurement.

Options Trading: Surpassed $9B in total volume, capturing ~29% of the Bitcoin options market.

Full Year 2025:

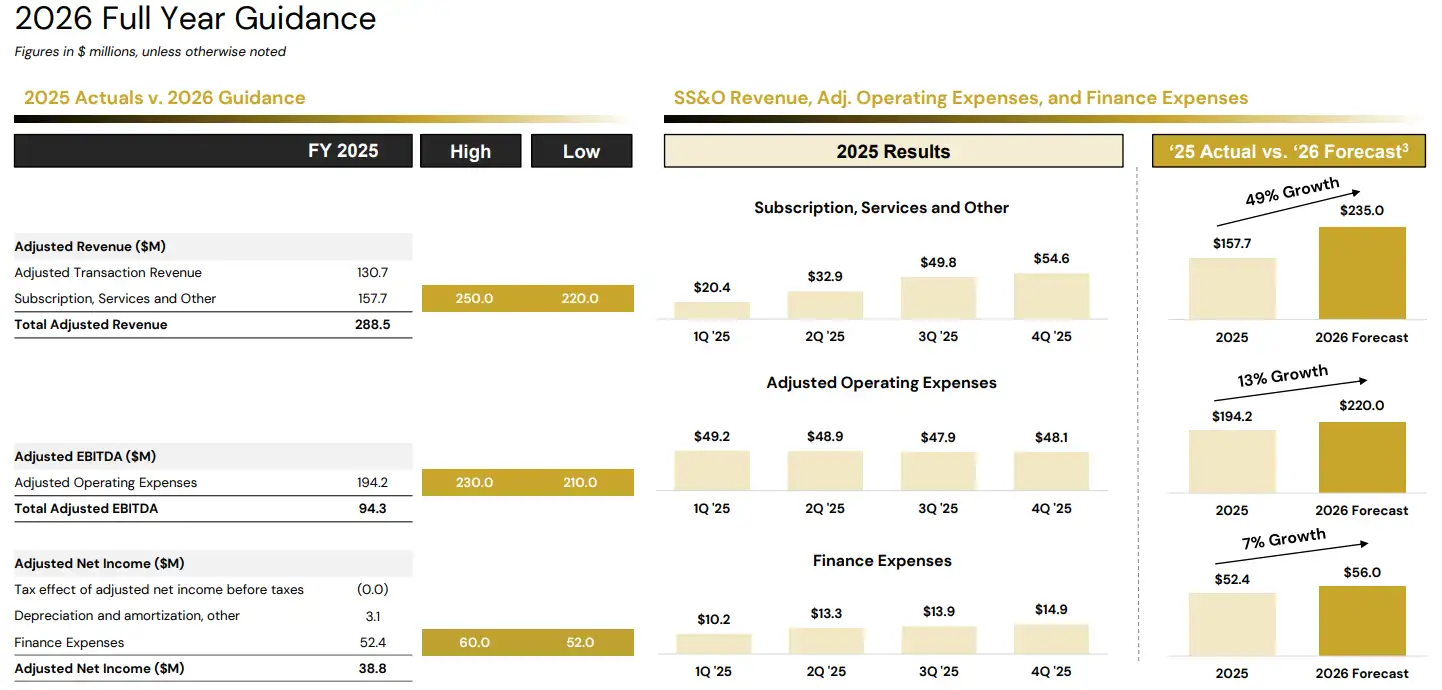

Total Adjusted Revenue: $288.5M, +35% YoY.

Subscription & Services (SS&O): $157.7M, up 160% YoY, showing a clear shift toward recurring revenue.

Adjusted EBITDA: $94.3M.

Context:

Bullish has seen a dramatic turnaround over the past two years:

2022: Net loss of $4.25B

2023: Net income of $1.30B

2024: Net income of $79.6M

These swings reflect fair value accounting on its large digital asset holdings, which causes extreme volatility in GAAP results. Adjusted (non-IFRS) metrics provide a clearer picture of operational performance. For Q1 2025 the company reported a net loss of $349M, but Adjusted EBITDA remained positive at $13M, underscoring the underlying operational strength.

Bullish – 2026 Outlook

Management issued optimistic guidance for fiscal 2026:

SS&O Revenue: $220M–$250M, implying ~50% YoY growth.

Adjusted Operating Expenses: $210M–$230M.

Next Earnings Date: Q1 2026 results expected April 23, 2026.

This outlook highlights continued growth in recurring revenue streams and operational scalability as Bullish further solidifies its position in institutional digital assets.

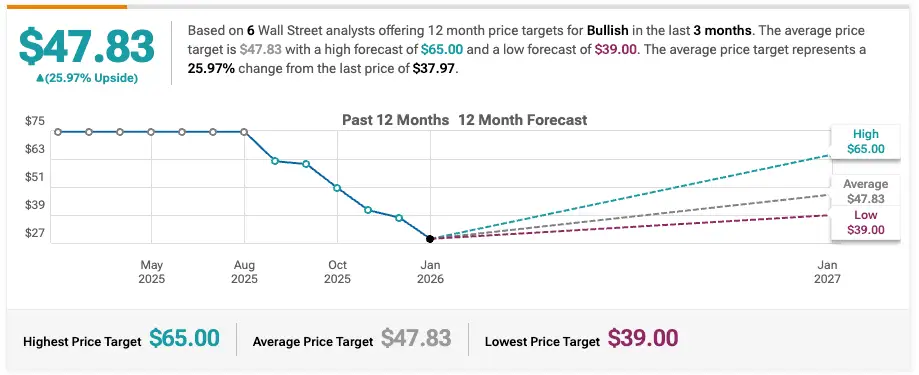

JP Morgan Maintains Neutral on Bullish, Lowers Price Target to $41

Rosenblatt Maintains Buy on Bullish, Lowers Price Target to $39

Citigroup Maintains Buy on Bullish, Lowers Price Target to $67

Canaccord Genuity Maintains Buy on Bullish, Lowers Price Target to $50

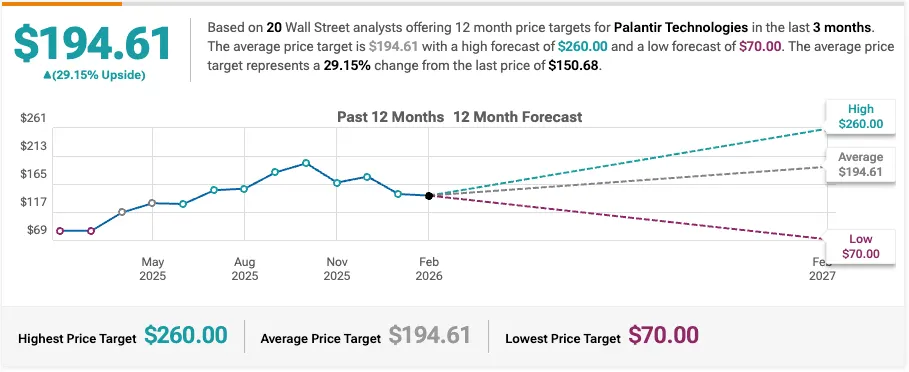

Company: Palantir Technologies Inc

Quote: $PLTR

BT: $120-$130

ST: $207 -$215

Sharks Opinion: We’ve put in enough work on PLTR over the past few years this isn’t a name where the edge comes from rehashing earnings line by line.

It comes from understanding when the narrative, macro, and tape all start to align.

Last month’s pullback combined with the current geopolitical backdrop is what’s setting this up. You’ve got a reset in price, followed immediately by a new catalyst cycle and that’s typically where bounce trades begin to form.

Primary Signal:

The Iran conflict shifts the conversation back toward sustained defense and AI-driven government spending.

This plays directly into PLTR’s strengths defense AI, operational software, and embedded government infrastructure.

You’re looking at continued expansion of platforms like ShipOS, alongside large-scale frameworks like the $10B Army AIP program.

Layer in a 61% 2026 growth guide, and fundamentally, the demand side hasn’t slowed it’s potentially accelerating under a new lens.

Druckenmiller exiting adds an interesting wrinkle, but in this case, macro may matter more than individual positioning. A prolonged conflict creates a fresh catalyst arc that wasn’t priced in during the initial unwind.

Financials:

Q4 came in strong across the board:

Revenue at $1.41B (+70% YoY)

US government revenue up 66%

US commercial up 137% Guidance for 2026 sits around $7.18–$7.20B with

EBITDA margins at 32%. This isn’t a company struggling to grow it’s one trying to justify how much growth is already priced in.

Valuation Risk:

This is where things get tight.

At ~241x trailing earnings, ~395x TTM, and ~145x forward, the margin for error is basically nonexistent.

Any slip whether it’s growth, contracts, or sentiment and the stock can reprice aggressively.

That’s part of what drove the last drawdown, and it’s something that doesn’t go away just because the narrative improves.

Catalysts:

May 11 earnings becomes the next checkpoint. Beyond that, the real variable is duration — how long the geopolitical backdrop sustains elevated government demand and contract velocity. Expansion of systems like Maven, alongside ongoing platform adoption, continues to support the story.

There’s also the underlying competitive risk any shift in AI infrastructure (including potential displacement cycles involving major model providers) could create friction, but those transitions tend to play out over months, not overnight.

Technical Setup:

The chart did what it needed to do flush from $207 highs down to ~$126, and now starting to recover into the $150s.

That type of move resets positioning and shakes out weaker hands.

Now the focus shifts to whether it can reclaim higher levels, with the 50-week sitting around $170 acting as a key area. That’s both resistance and, if reclaimed, a signal that momentum is rebuilding.

The opportunity is there but it’s not forgiving. This isn’t a name you chase blindly. It’s one you let confirm, because when it moves, it tends to reward timing more than conviction.

Description: Palantir is an artificial intelligence, analytics, and automated decision-making company that leverages data to drive efficiency across its clients' organizations. The firm serves commercial and government clients via its Foundry and Gotham platforms, respectively. Palantir works only with entities in Western-allied nations and reserves the right not to work with anyone that is antithetical to Western values. The company was founded in 2003 and went public in 2020.

UBS Maintains Buy on Palantir Technologies, Raises Price Target to $200

Wedbush Reiterates Outperform on Palantir Technologies, Maintains $230 Price Target

Rosenblatt Maintains Buy on Palantir Technologies, Raises Price Target to $200

Mizuho Upgrades Palantir Technologies to Outperform, Announces $195 Price Target