This watchlist highlights the current industrial-focused names we’re tracking for potential trade setups. These are not active alerts.

All entries will be communicated in real time upon execution, consistent with the format used in the weekly investment letter.

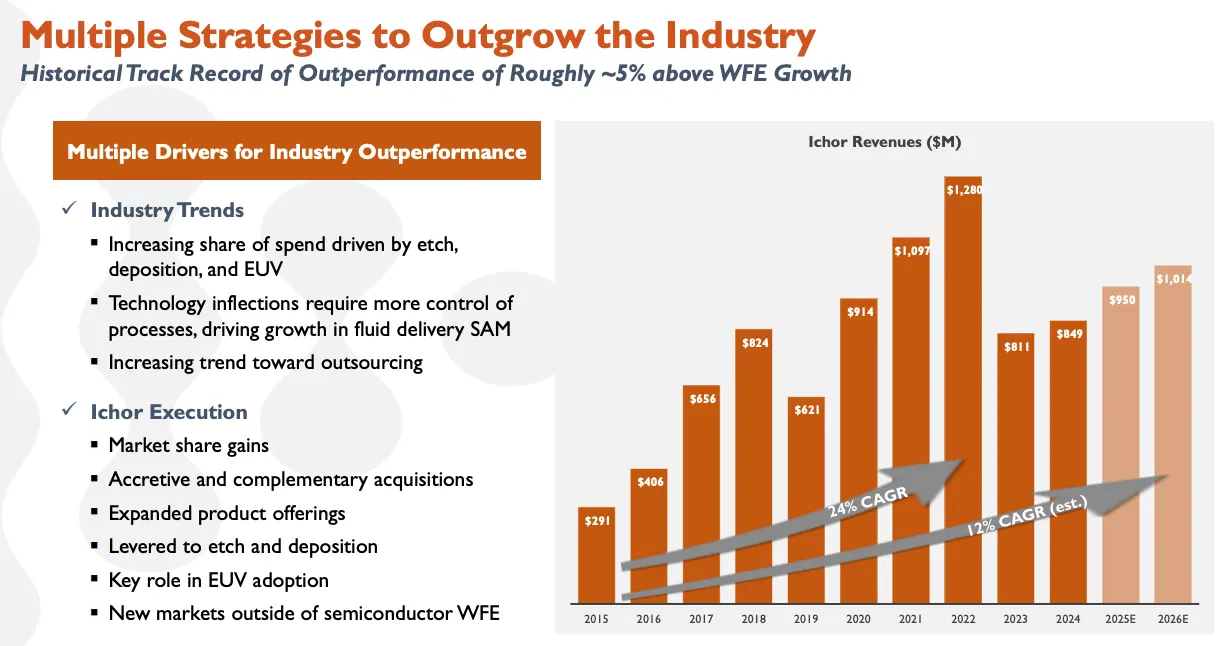

Company: Ichor Holdings

Quote: $ICHR

ST: $56 Short Term, $96 Long Term

Sharks Opinion:

Ichor was the first name that lit up when we backtested the AI data prompt we walked through on the webinar and it wasn’t random. It fits cleanly into one of the core themes we’ve been building toward for 2026:

semiconductor infrastructure and the chemical layer that actually enables the entire AI buildout.

This is the part of the stack most people ignore. Everyone crowds into the obvious trades chips, hyperscalers, AI models but the real bottlenecks, and often the highest asymmetry opportunities, sit one layer beneath that. Flow control systems, gas delivery, specialty chemicals, deposition environments the unsexy but critical components required to actually manufacture advanced semiconductors at scale.

That’s where Ichor lives.

They’re deeply embedded in the supply chain, primarily serving names like Lam Research and Applied Materials which effectively makes them a levered bet on wafer fab equipment demand without paying the premium multiples those names command.

From an operational standpoint, the story is starting to clean up.

New leadership is shifting focus toward execution tightening margins, optimizing production, and leaning into higher-value proprietary components. At the same time, they’ve got flexibility on the balance sheet to pursue M&A, which matters in a fragmented supply chain where scale and integration can drive meaningful margin expansion.

As orders from key customers begin to reaccelerate into the next cycle, you’re looking at a business that has the ability to snap margins back toward historical levels fairly quickly.

What makes this setup stand out right now is positioning. This is still a thinly traded name with a tight float which means when volume comes in, it’s noticeable. That’s exactly what we started to see with the +11% move on March 16, which aligns with the broader “cycle trough” thesis beginning to play out.

Management has already framed Q4 as the bottom, with recovery expected into the back half of 2026.

So now it becomes less about calling the exact bottom and more about identifying whether the stock can start building a base.

That ~$45 level is key if it can consolidate and hold above that zone, you start to build a structure for the next leg higher.

The asymmetry here is what keeps it on top of the watchlist.

You’ve got roughly a $1.4B market cap sitting against a ~$96 fair value estimate. That gap doesn’t close overnight but it doesn’t need to.

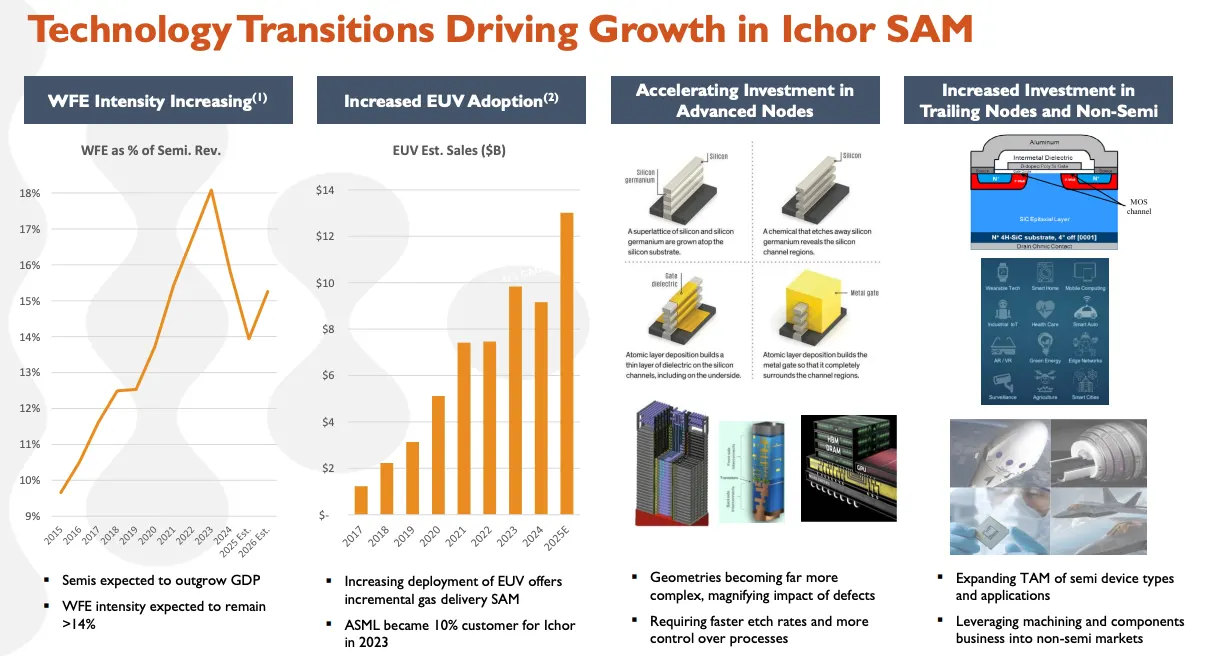

Description: Ichor Holdings Ltd designs, engineers, and manufactures critical fluid delivery subsystems and components mainly for semiconductor capital equipment, along with solutions for defense/aerospace and medical industries. Its product portfolio includes gas and chemical delivery subsystems that enable precise delivery, monitoring, and control of specialized gases and reactive liquid chemistries used in semiconductor manufacturing processes such as etch, electroplating, and cleaning. The company also provides precision-machined components, weldments, e-beam and laser-welded components, as well as precision vacuum and hydrogen brazing. Geographically, the company operates across the United States, Singapore, Europe, and other regions, with Singapore contributing the majority of revenue.

At its core, Ichor sits inside the machines that actually make semiconductors work.

Not the headline tools themselves but the infrastructure inside them.

The gas delivery systems, flow control units, precision assemblies all the components responsible for moving and regulating the chemicals required in etch and deposition.

When companies like Lam and Applied build out their tools, this is the layer that makes those tools functional.

That’s Ichor’s lane.

They’re not just assembling parts either the model is shifting. There’s a clear push toward designing and manufacturing more proprietary components in-house, while expanding their footprint across the US and Asia.

The goal is pretty straightforward: reduce reliance on third-party suppliers, gain tighter control over production, and ultimately expand margins while increasing content per tool.

It’s a quiet transition, but an important one.

Because in this part of the supply chain, control equals leverage. Now zoom out to the bigger picture.

The AI trade has created a massive demand shock — but it doesn’t stop at GPUs or data centers. It flows all the way down into fabrication capacity.

More AI demand → more chips

More chips → more wafer starts

More wafer starts → more etch and deposition tools

And every one of those tools requires the kind of subsystems Ichor provides. That’s the real thesis here.

This isn’t a direct AI play it’s a second-order beneficiary tied to the physical buildout of semiconductor infrastructure.

As advanced nodes become more complex, they require more process steps, more precision, and more chemical control. That naturally increases the value and necessity of Ichor’s systems.

Layer in reshoring fabs being built out across the US and Asia and you’re looking at a multi-year tailwind that isn’t dependent on short-term sentiment.

Ichor’s Q4 report came in with a clear punch above expectations. Adjusted EPS hit $0.07 easily beating the Street’s forecast of a $0.06 loss while revenue landed at $223.6 million, slightly above consensus by $2.76 million.

Small beats, but in a thinly traded name like this, that kind of outperformance gets noticed.

Revenue was still down 4% year-over-year, but the story underneath matters more than the headline. Semiconductor demand remained steady, and commercial manufacturing growth started to accelerate, providing enough tailwind to deliver a strong earnings beat.

Gross margins dipped slightly to 11.7% from 12%, but management emphasized this is early in their margin expansion journey the initiatives they’ve put in place for operational discipline and proprietary component focus are just starting to show results.

Looking ahead, the company is projecting Q1 sales between $240 million and $260 million. That midpoint implies roughly 12% year-over-year growth, paired with gross margins expanding back toward 12–13%.

On the earnings side, management expects adjusted EPS of $0.08–$0.16 roughly flat with last year, which is impressive considering the company continues to invest in growth initiatives.

The broader takeaway: Ichor is executing through the cycle. Even in a softer revenue environment, operational improvements, semiconductor demand, and commercial expansion are all starting to align. If the company can continue scaling margins while riding the wave of fab expansions and AI-driven chip demand, the earnings trajectory over the next few quarters could begin to look much more compelling, especially for a name that remains under the radar.

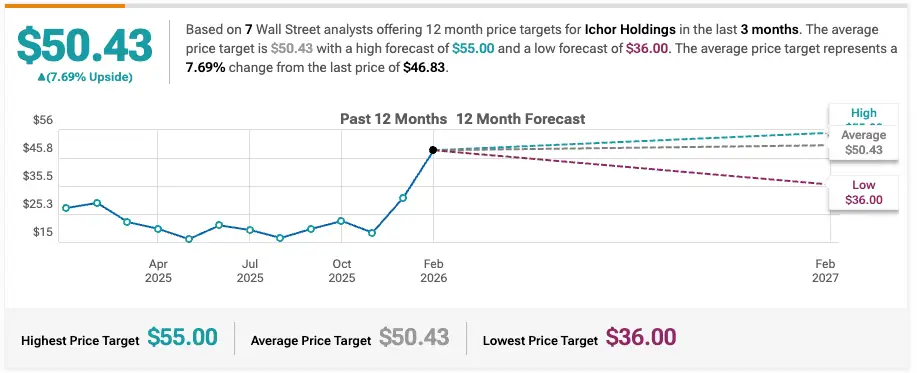

B. Riley Securities Upgrades Ichor Holdings to Buy, Raises Price Target to $52

Oppenheimer Maintains Perform on Ichor Holdings, Raises Price Target to $36

Stifel Upgrades Ichor Holdings to Buy, Raises Price Target to $55

Company: Xometry, Inc.

Quote: $XMTR

BT: $28-$40

ST: $68-$75

Sharks Opinion:

Xometry is one we swung last year and in hindsight, we definitely sold too early. The stock has since softened below its 52-week low, and now, after digesting that sell-off, it’s starting to carve out a base at a more reasonable valuation. That makes it worth circling back for another look.

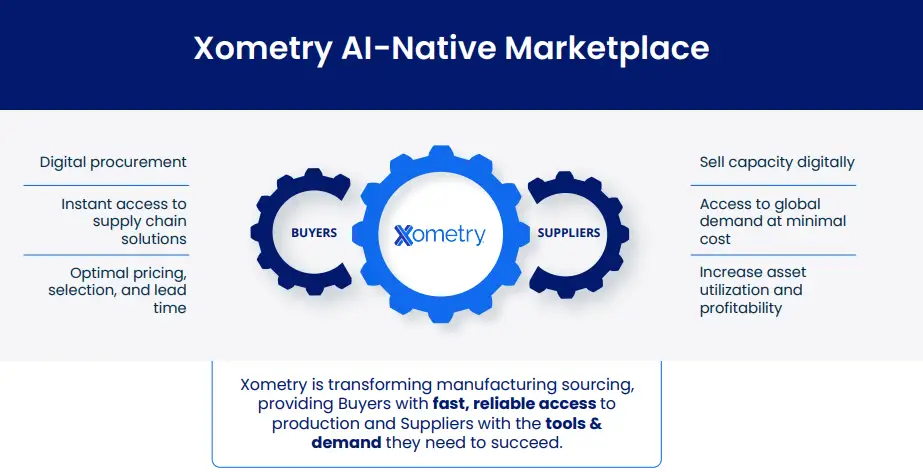

The core story remains intact: Xometry’s AI-driven digital platform efficiently connects buyers and suppliers, smoothing supply chain operations and reducing the friction that typically slows procurement.

Their algorithmic matching isn’t just convenience it’s efficiency baked into every transaction, and as the platform grows, each interaction feeds more data into the algorithms, reinforcing network effects over time.

Growth is still accelerating. The company is producing meaningful operating leverage and edging toward positive cash flow. And yet, despite that trajectory, the shares still trade on a relatively modest sales multiple — a disconnect we think the market will eventually recognize.

Leadership is in transition, but the strategic blueprint is consistent: build a seamless ecommerce experience, reduce buyer-seller friction, and expand the addressable market with AI enhancements.

It’s a repeatable, scalable model that benefits from both secular tailwinds in digital supply chains and the compounding effect of data-driven network growth.

At current levels, this looks like a low-risk re-entry for a high-quality, high-growth infrastructure play that still flies under the radar.

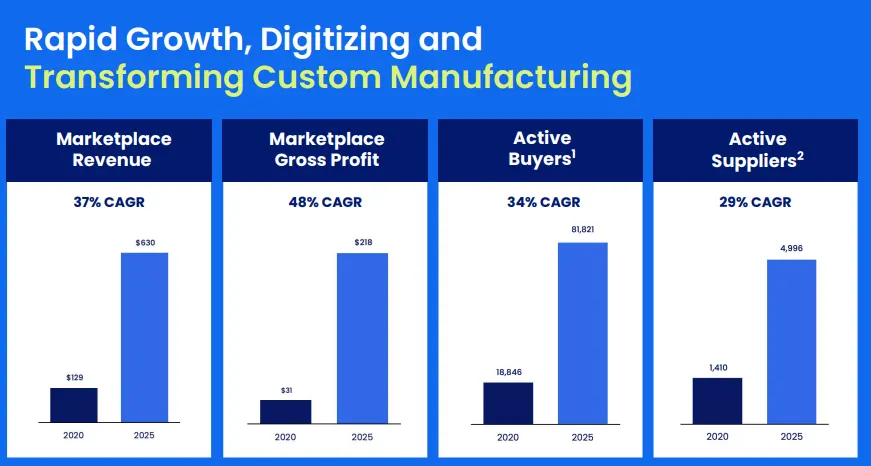

Description: Xometry Inc is engaged in providing AI-enabled manufacturing equipment. Its buyers include engineers, product designers, procurement and supply chain personnel, inventors, and business owners. The manufacturing processes offered by the company include CNC Machining, Injection Molding, Urethane Casting, 3D Printing, and Die Casting. The company is organized into two segments referred to as the U.S. and the International. The majority of its revenue is derived from the U.S. segment.

Xometry operates as a two-sided marketplace for non-contract manufacturing think small production runs, prototypes, and custom parts.

On the buyer side, the platform gives both small and large manufacturers seamless access to a fragmented network of suppliers across CNC machining, 3D printing, die casting, injection molding, sheet metal, finishing, and rapid prototyping. Buyers get instant quotes, transparent pricing, and a streamlined procurement process that would otherwise be fragmented and timeconsuming.

On the seller side, manufacturers gain access to a broader customer base they wouldn’t normally reach, with the flexibility to bid on projects based on current capacity.

Xometry also layers in value-added services: SaaS productivity tools, access to materials and tooling suppliers, financial services like advanced payments, and advertising opportunities. That combination turns a marketplace into a fullstack operational platform.

Because Xometry focuses on custom manufacturing, it’s brokering an opaque market where end demand is typically non-discretionary meaning customers have to buy.

That makes the platform sticky. The impact shows in their improving Marketplace Gross Margin: customers get selection, pricing certainty, quality assurance, and a smoother overall experience.

Network effects are at the core of the model.

On the demand side, the instant quoting engine leverages a rich dataset to optimize pricing and quality and Xometry guarantees the product, absorbing the cost of errors, which builds trust.

On the supply side, the matching algorithm and fulfillment system drive efficiency and utilization, creating a flywheel where more suppliers and buyers strengthen the marketplace for everyone.

In short, Xometry isn’t just connecting buyers and sellers it’s structuring an opaque, fragmented industry in a way that scales operationally while reinforcing trust and efficiency on both sides of the network.

Xometry delivered a strong Q4, showing the traction we’ve been highlighting for the marketplace model.

Revenue came in at $192.4 million, up 30% year-over-year, while adjusted EPS hit $0.16 beating the Street’s $0.12 estimate by $0.04.

Marketplace revenue continues to drive the engine, up 33% to $178 million, and adjusted EBITDA turned positive at $8.4 million, marking a clear operational inflection from prior losses.

Active buyers increased 20% to 81,821, with high-value accounts ($50k+ spend) rising 18% to 1,760. These metrics show that both user acquisition and monetization are scaling simultaneously exactly what you want to see from a network-driven platform.

Key Takeaways & Outlook:

Profitable Growth: Management continues to emphasize operational efficiency and enterprise adoption. The combination of AI-driven matchmaking and streamlined procurement is translating into a move toward sustainable profitability.

Guidance: For Q1 2026, the company expects revenue of ~$184.6 million and EPS of $0.13, signaling continued growth momentum while navigating normal seasonality and ongoing investment in expansion.

Headwinds: Despite the beat, shares initially traded lower, likely due to elevated multiples and cautious sentiment around costs tied to international expansion. Execution overseas will be a key variable to watch, but the domestic marketplace remains robust.

Overall, Xometry is executing on both sides of its network growing buyers, expanding high-value accounts, and turning EBITDA positive while building the foundation for long-term operational leverage and scale. It’s the kind of setup that benefits from both structural demand and improved unit economics.

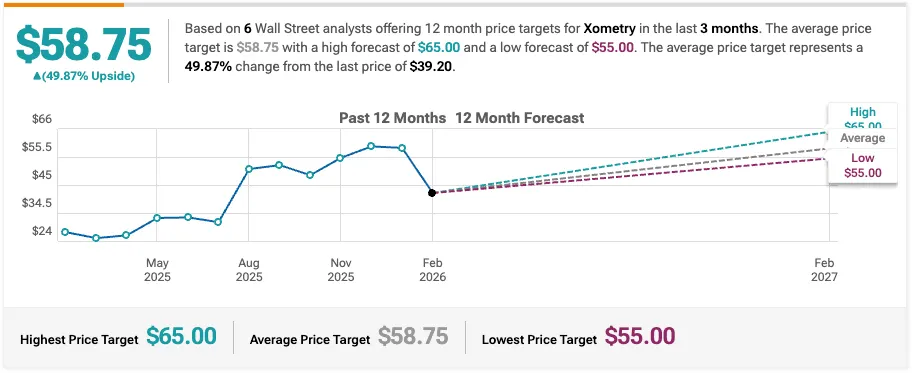

Citigroup Maintains Buy on Xometry, Lowers Price Target to $65

RBC Capital Maintains Sector Perform on Xometry, Lowers Price Target to $55

Wedbush Maintains Outperform on Xometry, Lowers Price Target to $60

Company: Kodiak AI, Inc.

Quote: $KDK

BT: $6.50-$7.00

ST: $12-$14

Sharks Opinion:

We exited Kodiak (KDK) last month for one primary reason: earnings risk.

In hindsight, the reaction was muted, and our caution proved somewhat overstated, which now shifts our focus toward identifying the right opportunity to re-enter the name.

From a purely fundamental standpoint, trimming ahead of earnings may have seemed overly cautious.

But this is not a purely fundamentals-driven market right now it is reaction-driven, where positioning around events often matters more than the results themselves.

The initial plan was straightforward: step aside into earnings, reassess the reaction, and look to reenter once volatility cleared.

However, given the lack of meaningful movement in both price action and volume, we are now waiting for a clear catalyst and stronger tape confirmation before stepping back in.

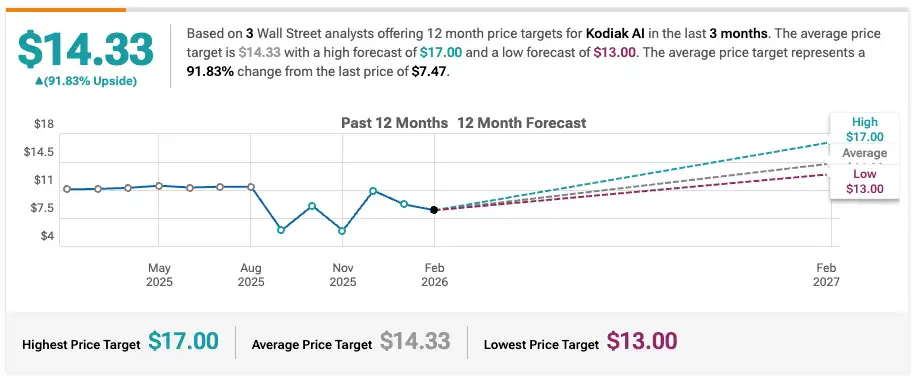

That said, our broader view on the company remains unchanged. We continue to maintain a $14 price target for the year, but for now, we are taking a wait-and-see approach until momentum returns.

From a valuation perspective, Kodiak still screens as one of the most undervalued names in the autonomous driving space.

For context, Waymo (Alphabet) carries an estimated valuation of roughly $45 billion, while Aurora Innovation (AUR) has averaged around $11.7 billion over the past six months.

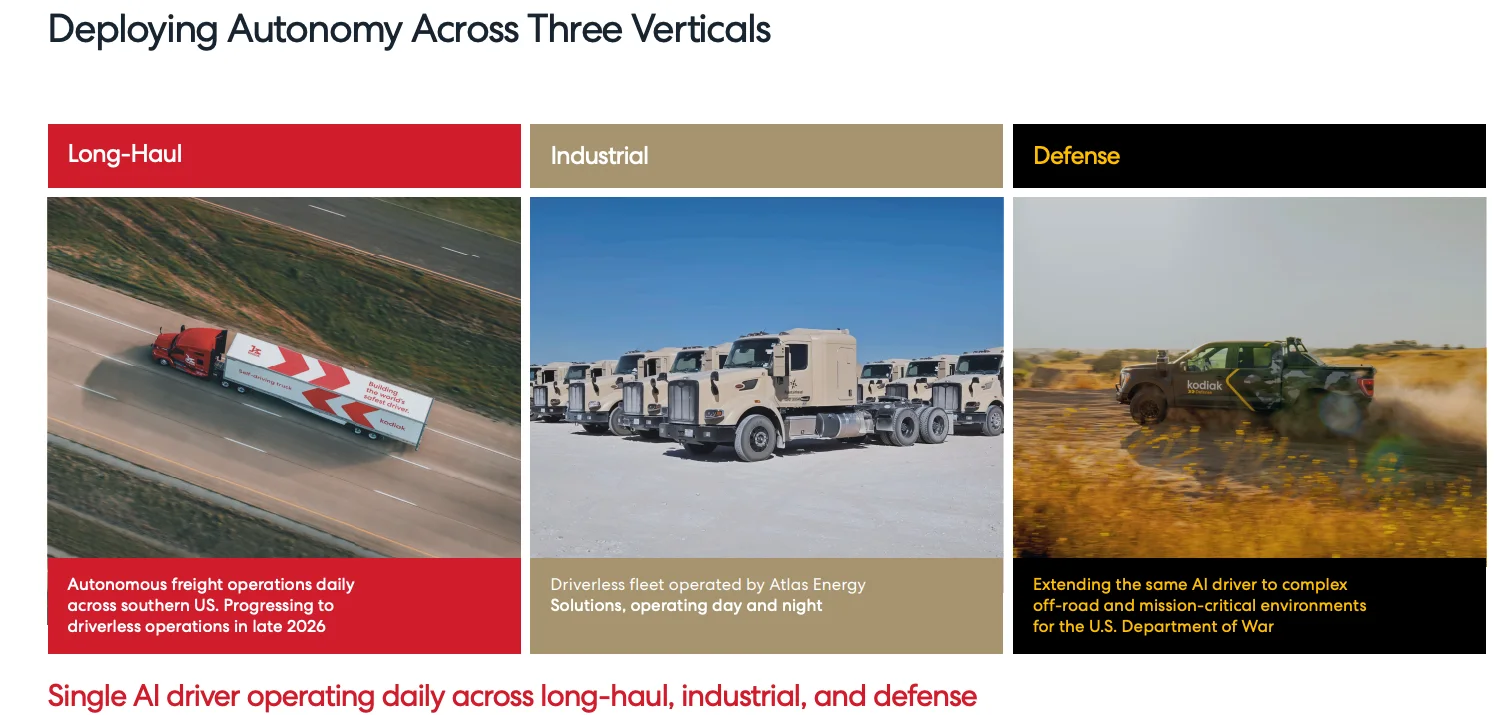

Kodiak, in comparison, trades at a fraction of those valuations, despite already generating revenue, securing government and military contracts, and hitting key operational milestones.

The company is now approved to operate in 24 states, with both commercial and defense partnerships in place, and plans to deploy thousands of autonomous trucks by 2027.

This is no longer a concept-stage story Kodiak is actively executing on its roadmap.

We continue to approach this trade with measured conviction, targeting a short-term swing to $14 (roughly aligned with its initial listing range) and a longer-term upside above $20 as adoption scales and institutional ownership increases

Description: Kodiak AI Inc is a provider of artificial intelligence (AI)-powered autonomous vehicle technology. This technology addresses the needs of the long-haul trucking, industrial trucking, and defense industries. The company's core offering, the Kodiak Driver, is a single-platform virtual driver that combines advanced AI software with modular hardware for customer deployments. All company operations are conducted in the United States. The company has one operating and reportable segment related to the development of autonomous vehicle technology and related services that can be applied at scale across a broad range of industries and environments.

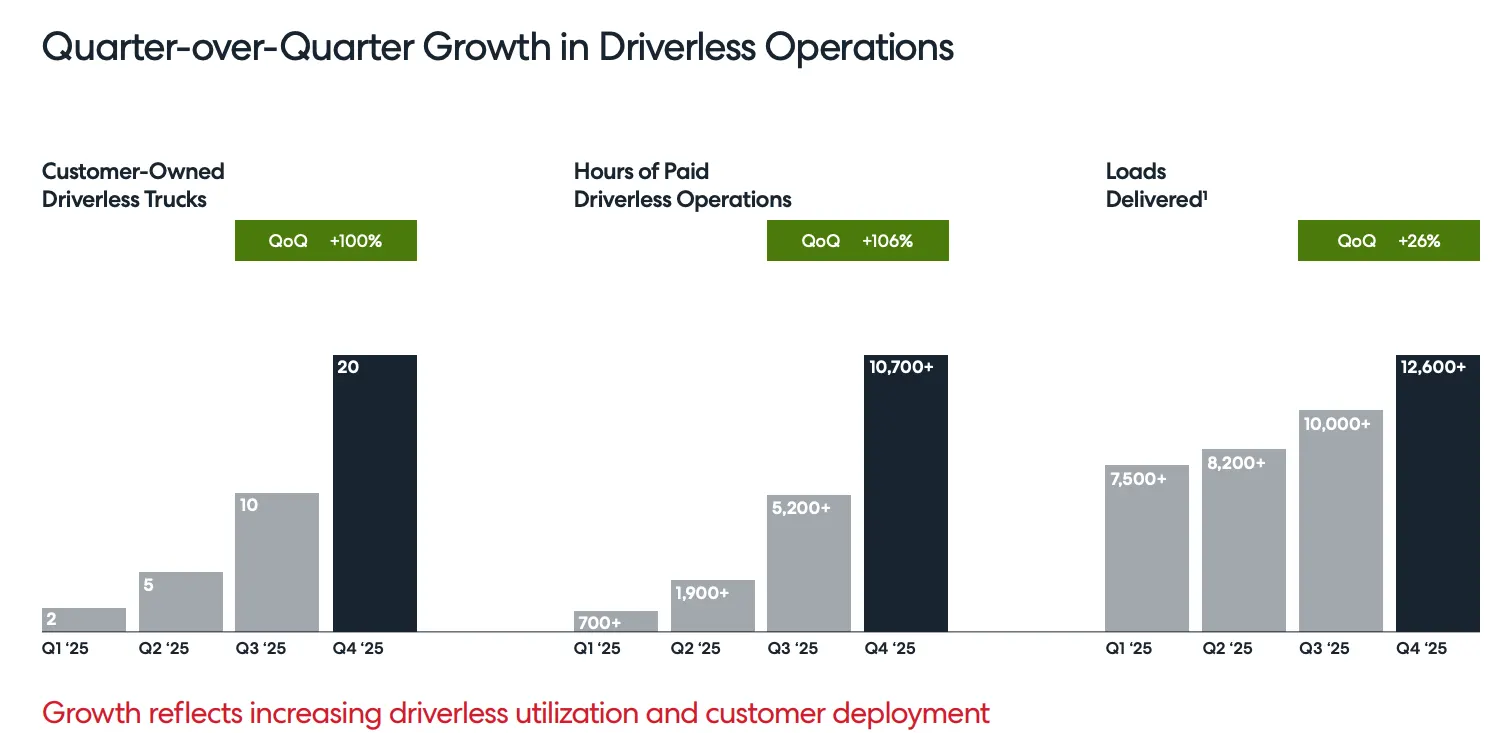

Key Operational Highlights

Fleet Expansion:

Kodiak deployed 10 additional driverless trucks to Atlas Energy Solutions, bringing the total fleet to 20 fully driverless trucks, a 100% increase from Q3.

Safety Progress:

The company continues to make meaningful strides toward regulatory and operational readiness, with its Kodiak Autonomy Readiness Measure reaching 84% as of February 2026 a key internal benchmark for launch preparedness.

Driverless Operations Growth:

Kodiak has now accumulated over 10,700 cumulative hours of paid driverless operations, representing a 106% increase quarter-over-quarter, and positioning the company as a leader in real-world autonomous trucking deployment.

Kodiak AI continues to show steady operational progress, particularly around its Atlas platform, while also delivering a lower-than-expected fourth-quarter free cash flow burn relative to prior guidance.

The company also highlighted advancements in its AI initiatives and defenserelated business, reinforcing the broader strategic positioning of Kodiak beyond just commercial trucking. However, these positives were partially offset by slightly higher projected free cash flow usage for 2026, indicating continued investment as the company scales.

One notable update is the timeline shift for driverless long-haul commercialization, which is now framed as a late-2026 milestone, rather than earlier expectations of the second half of the year. While not a major delay, it does reflect the complexity of final safety validation and deployment at scale.

TD Cowen Maintains Buy on Kodiak AI, Lowers Price Target to $13

Chardan Capital Maintains Buy on Kodiak AI, Maintains $22 Price Target

Cantor Fitzgerald Reaffirms Their Buy Rating on Kodiak AI

Company: MDA Space Ltd.

Quote: $MDA

BT: $18-$21

ST: $44

Sharks Opinion:

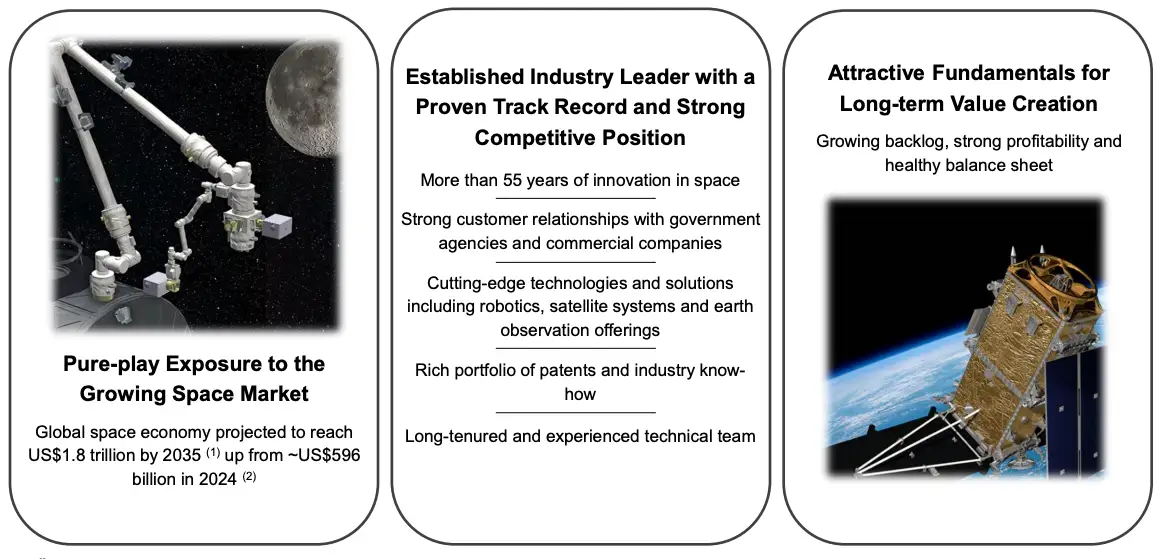

MDA Space is a name we know well it’s the former parent of one of our Stock Sharks favorites, Maxar Technologies. Recently uplisting to the Nasdaq, MDA is benefiting from a broader revival in the space sector, and the timing is compelling.

We consider MDA one of the premier space companies a core holding in a space-focused portfolio but only at the right entry point. Based on our experience, fair value sits somewhere in the $20s. Once the shares correct into that zone, we’ll be ready to act.

MDA occupies a unique middle ground in the space ecosystem. On one end, you have megaplayers like Boeing, SpaceX, and Airbus; on the other, high-risk, often unprofitable “new space” names. MDA bridges the gap a profitable, established company with 55 years of experience, 3,000+ employees, and a track record of delivering cutting-edge technologies.

It’s a rare combination of stability and innovation in a sector that is otherwise heavily skewed toward volatility.

With the SpaceX IPO on the horizon, we anticipate renewed investor attention and a potential rerating across the space sector.

MDA, as a critical infrastructure and technology provider within that ecosystem, is well-positioned to benefit from that rotation. When the broader space narrative accelerates, MDA could move higher not just on fundamentals, but on sector momentum.

Description: MDA Space Ltd is a developer and manufacturer of technology and services to the space industry. It is an international space mission partner and robotics, satellite systems, and geointelligence pioneer. It is engaged in communications satellites, Earth and space observation, space exploration, and infrastructure. The Company collaborates and partners with governments and space agencies, commercial space companies, and defence and aerospace prime contractors in the space industry. Geographically, it generates the majority of its revenue from Canada.

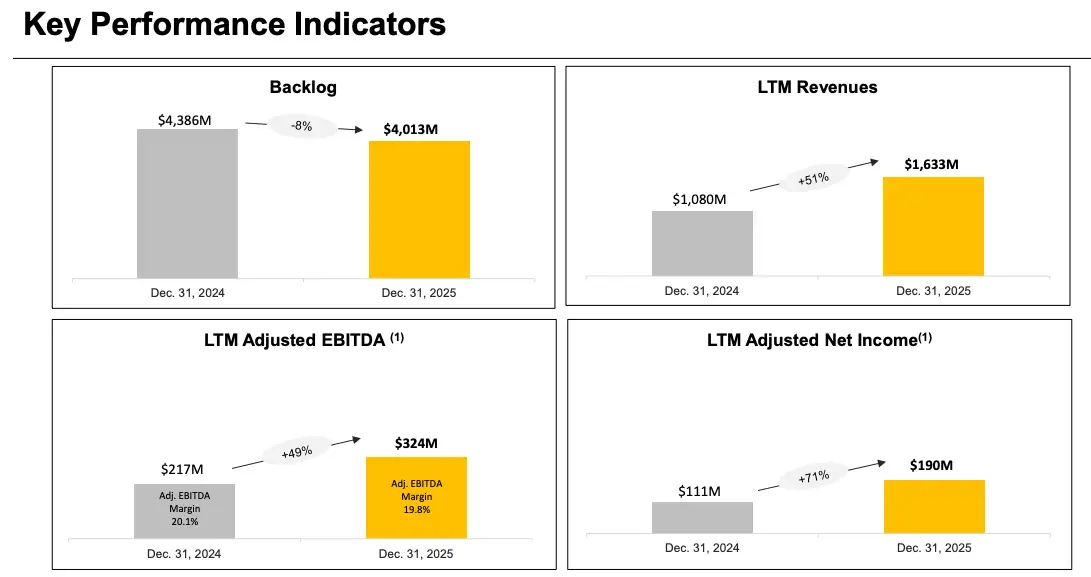

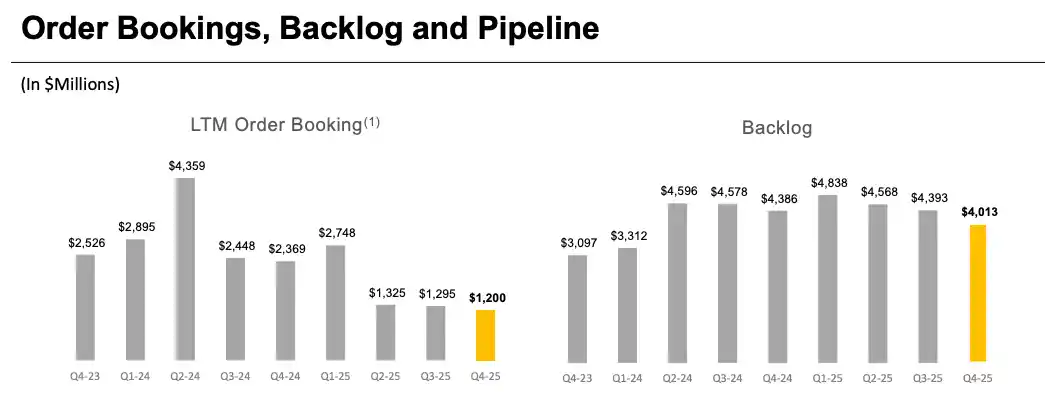

MDA Space has been publicly traded on the Toronto Stock Exchange since April 2021, and 2025 was a milestone year.

The company reported record revenue of $1.63 billion, up 51.2% year-overyear, fueled primarily by strong growth in its satellite systems business.

That performance underscores MDA’s ability to capture demand across multiple segments of the space economy while scaling efficiently.

The recent U.S. listing wasn’t strictly about raising capital management noted the company “didn’t really need the capital right now.” The move was strategic: entering the U.S. market attracts American investors, expands analyst coverage, and builds credibility with U.S.-based banks.

The estimated $300 million raised strengthens the balance sheet and provides flexibility for growth initiatives, including potential acquisitions or other strategic investments.

MDA operates through three complementary divisions: Robotics & Space Operations (32% of revenues): Focused on space robotics, on-orbit servicing, assembly, and exploration missions, including rovers. This division represents the cutting-edge hardware and operational capabilities that differentiate MDA from peers.

Satellite Systems (44% of revenues): The largest segment, producing LEO, MEO, and GEO satellites along with critical subsystems such as antennas, payloads, and specialized electronics. This division drives the bulk of revenue and positions MDA as a key supplier to both commercial and governmental satellite programs.

Geointelligence (22% of revenues): Provides earth observation, ground station services, and geospatial analytics. This division leverages MDA’s technology infrastructure to offer actionable insights adding recurring revenue streams and strategic value across defense, commercial, and research markets.

Overall, MDA’s diversified portfolio, strong revenue growth, and strategic U.S. market entry position it as a uniquely balanced space company combining innovation, operational experience, and long-term growth optionality.

MDA Space had a standout year in 2025, reporting total revenue of $1.63 billion CAD, up 51.2% year-over-year, and adjusted EBITDA of $323.9 million, a 49.2% increase. The company’s backlog sits at $4.0 billion, reflecting strong forward visibility across its satellite and defense programs.

Revenue by Division:

Satellite Systems: $1.11 billion (+85.5%) — the clear growth engine, driven by LEO, MEO, and GEO satellite builds and critical subsystems. Robotics & Space Operations: $309.3 million, contributing advanced robotics, on-orbit servicing, and exploration projects. Geointelligence: $214.4 million, providing earth observation, analytics, and ground station services.

Recent Performance & Drivers:

Q4 2025 revenue came in at $499.1 million, a 44% jump from the prior year, reflecting increased activity on large LEO constellations like Telesat Lightspeed and Globalstar, alongside defense contracts. The company’s expansion strategy included a U.S. IPO in March 2026, generating approximately $341 million in gross proceeds, strengthening its balance sheet for growth initiatives and potential acquisitions.

The broader takeaway: MDA’s growth continues to be heavily anchored in satellite manufacturing, a sector with high technical barriers, recurring defense demand, and strategic importance in the space economy. With strong divisional performance and solid backlog, the company is positioned to capture ongoing opportunities as the space sector re-rates globally.

Company: Telesat Corporation

Quote: $TSAT

BT: $28-$32

ST: $60+ (2028 Target)

Sharks Opinion:

The thesis for Telesat mirrors a lot of what we’ve highlighted for MDA: a Canadian satellite operator with a strong position in the space ecosystem and familiarity from prior trades that delivered solid returns.

The broader space sector appears primed for a rerating, especially with the looming SpaceX IPO bringing renewed investor focus.

That said, Telesat presents a slightly different risk/reward profile. Their main next-generation product isn’t expected to go live for another year, meaning revenue catalysts are still off in the distance.

Meanwhile, the company is actively rebalancing its balance sheet and managing a substantial debt load a factor that is currently compressing profit margins and could pressure near-term earnings.

Given these dynamics, we anticipate a potential pullback before the market fully factors in Telesat’s long-term story.

That correction could create a high-asymmetry entry point, allowing investors to position ahead of both product ramp-up and a broader sector rerating once debt metrics improve and growth begins to materialize.

In short, Telesat combines a familiar sector thesis with a near-term tactical setup: the stock may dip before it climbs, offering a disciplined, opportunitydriven entry.

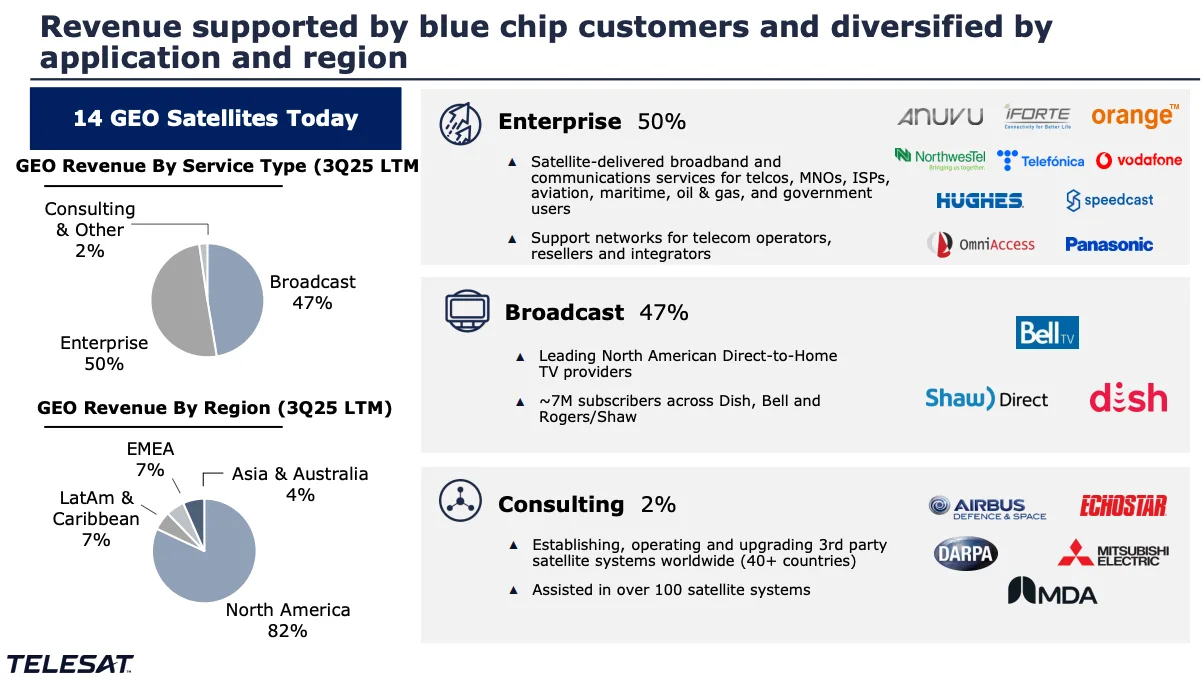

Description: Telesat Corp is a satellite operator, that provides its customers with mission-critical communications services. It operates in a single operating segment, in which it provides satellitebased services to its broadcast, enterprise, and consulting customers around the world. Geographically, it derives a majority of its revenue from Canada. It derives revenue from Broadcast, Enterprise, Consulting, and others.

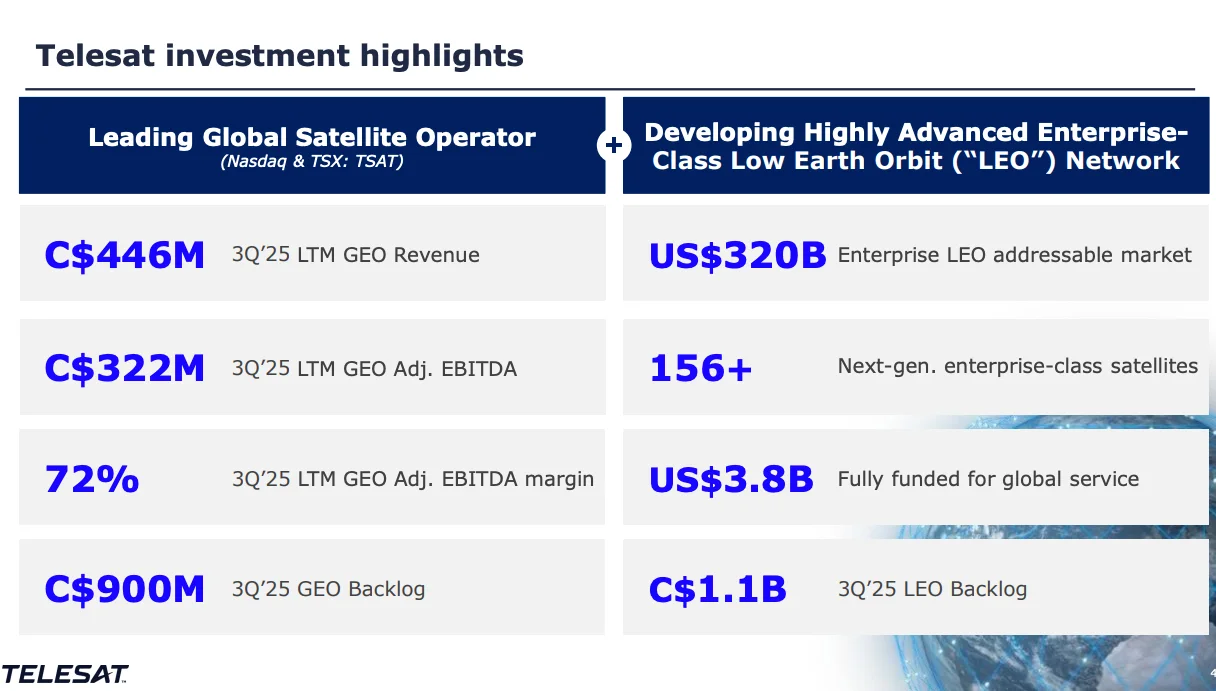

Telesat faced a challenging 2025, reporting total revenue of $418 million, down 27% from $571 million in 2024, with Q4 revenue at $67.5 million. The company posted a net loss of $111.2 million for the year, while adjusted EBITDA fell 45% year-over-year to $213 million.

Revenue Drivers & Trends:

Legacy GEO Decline: The Geostationary (GEO) business faced structural pressure. North American Direct-to-Home (DTH) customers reduced capacity and rates, while rural broadband demand softened, driving the revenue contraction.

Strategic Pivot to LEO: The company is shifting focus toward the Telesat Lightspeed Low Earth Orbit (LEO) constellation. As part of this pivot, roughly 25% of capacity has been reallocated to dedicated military spectrum, targeting global defense spending opportunities — a higher-margin segment with strong structural tailwinds.

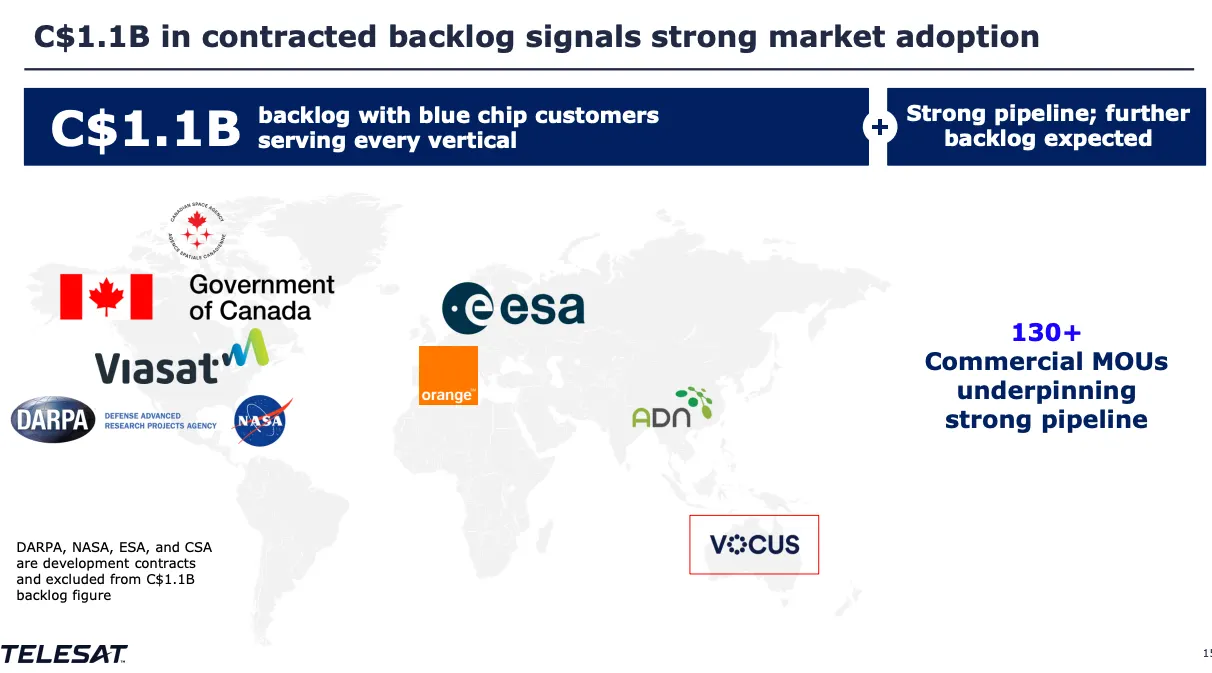

Backlog: Despite near-term revenue pressure, Telesat ended 2025 with ~$1.0 billion in LEO backlog and $800 million in GEO backlog, providing a solid runway for future growth as the LEO constellation ramps.

2026 Outlook:

For the legacy GEO unit, management expects revenue of $300–$320 million in 2026. The LEO segment will be the key driver of upside, but near-term earnings and margin pressure could create volatility before the ramp is fully realized.

Takeaway: Telesat is in transition balancing short-term margin pressure from legacy GEO declines with long-term optionality from Lightspeed LEO deployment and defense spectrum allocation.

The path forward is uneven, but this setup could present a tactical buying opportunity if the stock corrects ahead of the anticipated LEO ramp and broader sector re-rating.

Telesat’s 27% revenue decline in 2025 stemmed from structural shifts across its core service lines:

Broadcast / Direct-to-Home (DTH):

Still a foundational revenue source, this segment faced significant headwinds. Lower renewal rates and reduced capacity requirements from major North American providers drove roughly half of the year’s total revenue decline. Key clients include DISH Network and Bell Canada, with contracts like Nimiq-5 being renewed at materially lower rates a clear reflection of structural pricing pressure in the legacy GEO business.

Enterprise & Government Services:

Revenue slipped due to softer demand in rural broadband markets, particularly from international projects such as Indonesia’s rural broadband program. While this segment remains strategically important, the near-term impact of underutilized capacity and pricing pressure contributed to the overall decline.

Consulting & Other:

A smaller segment, including LEO-related consulting services, also experienced modest declines, reflecting the longer ramp timeline for Lightspeed adoption.

Key Customers & Market Segments:

Major Video Clients: DTH providers remain critical, but ongoing pricing pressure emphasizes the limitations of legacy GEO revenue.

Government & Military: This is where the growth thesis shifts. Telesat is actively targeting the sovereign defense market, recently securing a contract with the U.S. Department of War and allocating 25% of Lightspeed capacity to dedicated Military Ka-band spectrum positioning the company for highermargin, mission-critical applications.

Enterprise / ISPs: Includes telecom and internet providers leveraging satellite capacity for backhaul and rural connectivity. This segment provides stable utilization and a platform for future LEO adoption.

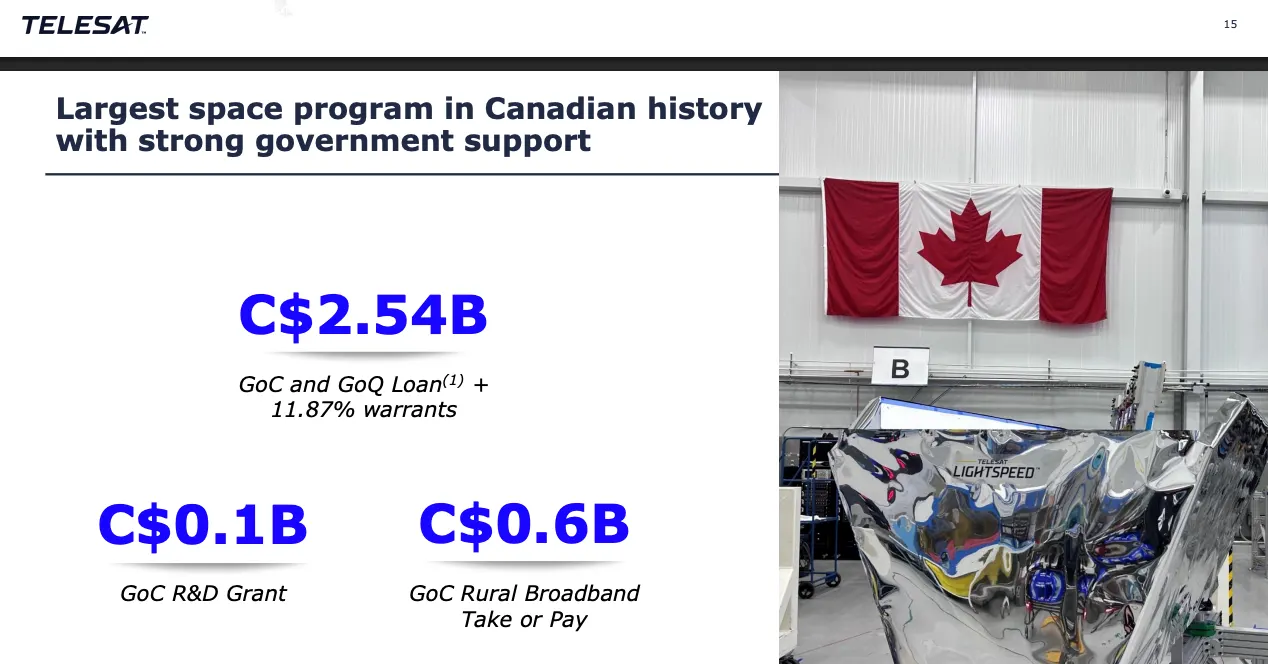

Telesat’s growth and LEO deployment are being heavily supported by major government funding packages, providing both capital and strategic validation for the Lightspeed program.

Government of Canada:

Loan: $2.14 billion repayable loan, managed through the Canada Development Investment Corporation (CDEV).

Terms: 15-year maturity with a floating rate of 4.75% above CORRA. Equity: The federal government received warrants for 10% of Telesat LEO Inc. common shares, aligning public support with long-term upside potential.

Government of Québec:

Loan: $400 million, structured with terms mirroring the federal agreement. Equity: Québec received warrants for 1.87% of the Lightspeed business, ensuring regional participation in the project’s upside.

Previous Commitments:

A 10-year, $600 million agreement from 2020 pre-purchased LEO capacity for subsidized broadband in rural and remote communities. This illustrates longterm demand visibility and government backing for both capacity and operational cash flow.

Takeaway: These government arrangements provide Telesat with capital security, strategic credibility, and a partially pre-funded revenue base, mitigating risk as Lightspeed ramps. The combination of loans, warrants, and long-term agreements positions the company for execution on both commercial and defense opportunities while smoothing near-term financial volatility.

As of December 31, 2025, Telesat has a healthy forward-looking revenue backlog that reflects both its legacy operations and growth initiatives:

GEO Backlog: $800 million, largely tied to long-term broadcast contracts. This provides a stable revenue base, even as the legacy GEO business faces structural pressures from declining DTH demand and pricing concessions.

LEO (Lightspeed) Backlog: $1.0 billion, representing pre-commitments for the upcoming Lightspeed constellation. This segment underpins Telesat’s growth trajectory and positions the company to capture both commercial and defensedriven demand as the constellation comes online.

Takeaway: The combination of GEO stability and LEO optionality gives Telesat a dual-layered revenue foundation. While legacy operations offer predictability, the Lightspeed backlog represents the upside potential that could drive rerating once the constellation begins deployment and monetization.

Company: Rocket Lab Corporation

Quote: $RKLB

BT: $38-$48

ST: $80 For Year end $100+ Post Space X IPO re rating and Neutron launch

Sharks Opinion:

Rocket Lab has long been a familiar name in the Sharks community we’ve tracked it through multiple earnings cycles post-exit.

he thesis mirrors what we’ve discussed for MDA and Telesat, but with a key difference: Rocket Lab is a launch provider, not a satellite operator. That makes it a direct play on space infrastructure and launch cadence, which remains critical as commercial and defense demand accelerates.

Primary Signals:

Won a $190M MACH-TB 2.0 hypersonic contract on March 18, highlighting defense and aerospace tailwinds.

Broader market catalysts include the SpaceX IPO in 2026, which could drive a sector-wide re-rating, and the recent PLTR + RKLB AI defense trade call by Benzinga, underscoring cross-sector AI/defense synergies.

Financial Snapshot:

Q4 2025 revenue: $180M (+36% YoY)

FY2025 revenue: $602M (+38% YoY)

Backlog: $1.85B (+73%)

Operational execution: 100% launch success rate in 2025

Next earnings: May 7, 2026

Near-Term Overhang:

The $1B ATM equity offering registered on March 16 caused a -9.1% move on March 18. While some see dilution risk (~1.4% of a $39B market cap), this is actually a healthy entry signal — management is opportunistically raising capital at elevated prices, which is a hallmark of disciplined growth companies.

Bull Case / Re-Rating Catalysts:

Neutron rocket Q4 2026 first launch a major rerating event. Silicon solar arrays for space data centers — opening new revenue streams.

$23.9M CHIPS award validating semiconductor/space infrastructure exposure. SpaceX IPO adjacency sector sentiment tailwind. Geopolitical + AI tailwinds the Iran conflict and defense AI spend amplify demand for launches.

Description: Rocket Lab Corp is engaged in space, building rockets, and spacecraft. It provides end-to-end mission services that provide frequent and reliable access to space for civil, defense, and commercial markets. It designs and manufactures the Electron and Neutron launch vehicles and Photon satellite platform. Rocket Lab's Electron launch vehicle has delivered multiple satellites to orbit for private and public sector organizations, enabling operations in national security, scientific research, space debris mitigation, Earth observation, climate monitoring, and communications. The business operates in two segments Launch Services and Space Systems. Geographically it serves Japan, and rest of the world and earns key revenue from the United States

Cantor Fitzgerald Reiterates Overweight on Rocket Lab, Maintains $85 Price Target

Clear Street Initiates Coverage On Rocket Lab with Buy Rating, Announces Price Target of $88

B of A Securities Maintains Buy on Rocket Lab, Raises Price Target to $120

Goldman Sachs Maintains Neutral on Rocket Lab, Raises Price Target to $69