Shares of Wealthfront plummeted as much as 13% Thursday morning amid a broad market selloff and one day after the wealth management company reported mixed earnings results showing that hundreds of millions of dollars flowed out of customer accounts. The stock later pared its losses and ended the day down 6.2%

After earnings we initated a postion in wealthfront for several reasons this earnings overview will serve as a recap of the most recent quarter and a general overview of our long thesis and why we see upside in WLTH now.

Wealthfront was one of the pioneers in the robo-advisor space, helping define the automated wealth management model that many platforms now follow. Despite that early leadership, the stock has fallen nearly 50% since its IPO, which at first glance may seem perplexing but it is also where we begin to see opportunity emerge.

If WLTH struggles to regain traction in the public markets, there is a realistic scenario where the company could eventually be taken private. Importantly, this is still a highly valuable asset that could attract interest from multiple potential buyers.

A notable example occurred in 2022, when UBS reportedly attempted to acquire Wealthfront for $1.4 billion. Today, the company trades publicly at roughly $1.2 billion, meaning the entire business is currently valued below that prior takeover attempt.

That valuation gap begins to highlight the opportunity. And it’s not just traditional banks or fintech firms that could have interest. As artificial intelligence continues to reshape financial services from portfolio construction to automated financial planning platforms like Wealthfront could become increasingly attractive to technology companies looking to expand into the digital wealth ecosystem.

Part of the reason we exited FISV earlier this year was to create room for a potential position in Wealthfront. In our view, WLTH fits the automation and AIdriven financial services theme more directly and offers a more asymmetric setup if the company either executes operationally or becomes a strategic acquisition target.

This week we initiatied a starter position in WLTH (Wealthfront) as the setup checks all four of the key boxes we look for when entering a new trade.

First, the stock is trading near its 52-week lows, following the selloff that occurred after its recent IPO. Post-IPO weakness is a common pattern as early investors exit positions, but it can also create attractive entry points once the selling pressure begins to stabilize.

Second, we are seeing institutional footprints in the name, most notably through 13F filings showing involvement from Tiger Global, which helps validate that sophisticated capital is accumulating shares at these levels.

Third, the company maintains a strong balance sheet while trading at roughly 4.2× earnings, which appears inexpensive relative to both the FinTech sector and the company’s current revenue growth trajectory.

Finally, we received tape confirmation this morning, which was the last piece of the puzzle for us before stepping in. Seeing buyers begin to support the stock after a prolonged pullback adds confidence that downside momentum may be stabilizing.

Taken together post-IPO discount, institutional participation, strong fundamentals, and improving tape action WLTH presents a setup that fits well within the type of opportunities we look to initiate with a starter allocation before potentially scaling the position over time.

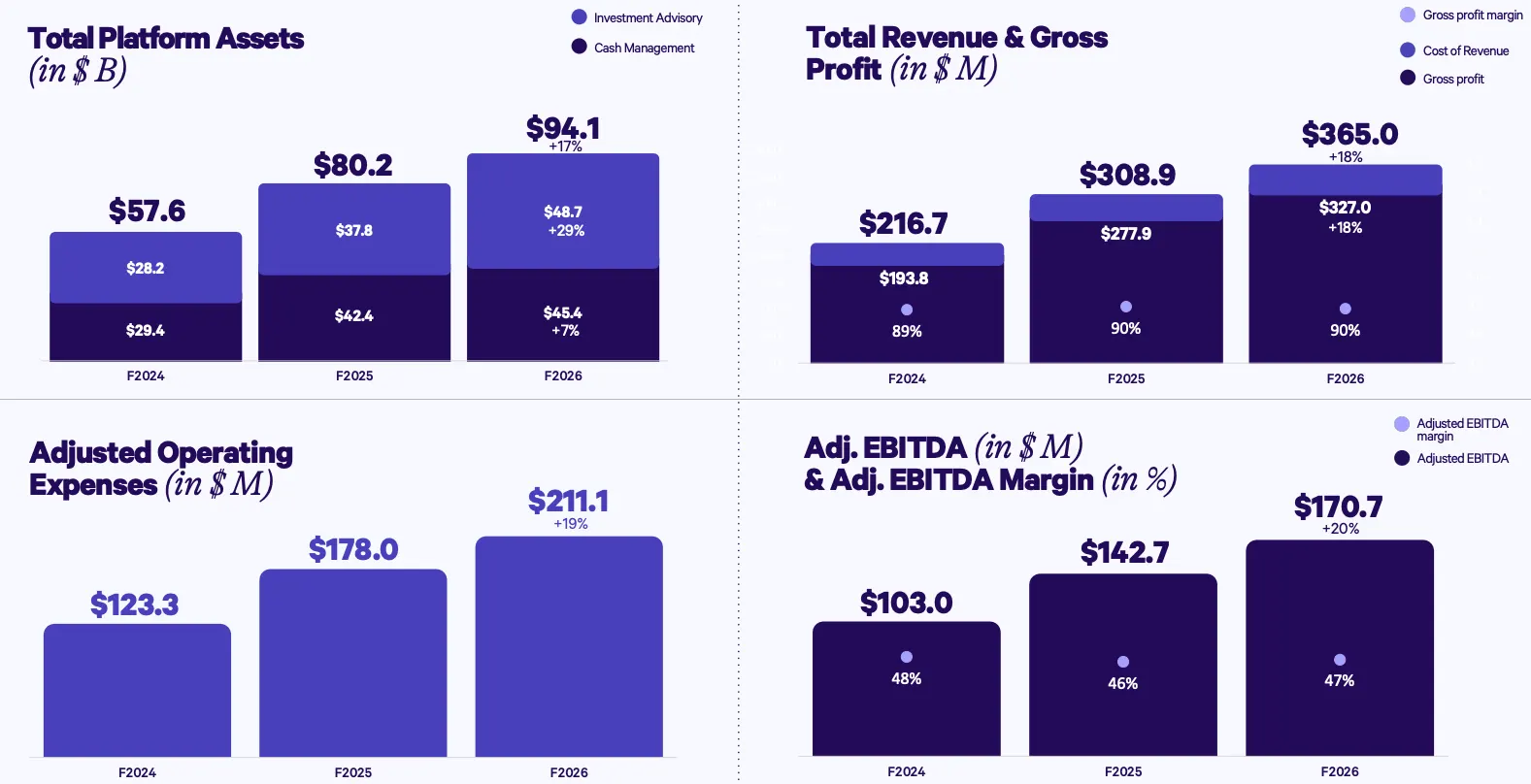

Wealthfront Corporation reported fourth-quarter revenue of $96.1 million, up 16% YoY, as the financial platform posted a GAAP loss of -$1.31 per share for the quarter ended January 31, 2026. The revenue figure surpassed the prior year’s $82.7 million for the same period.

The company reported a GAAP net loss of $134.8 million in the quarter, compared to net income of $32.1 million in the prior year period, primarily due to one-time IPO-related stock-based compensation expense of $239.0 million. Excluding these charges, adjusted EBITDA reached $44.2 million, up 22% YoY, with an adjusted EBITDA margin of 46%. For fiscal 2026, Wealthfront achieved record annual revenue of $365.0 million, up 18% YoY.

The company generated net cash from operating activities of $33.3 million in the quarter and $152.2 million for the full year. Wealthfront’s board authorized a $100 million share repurchase program in March. The company expects adjusted EBITDA margins to decline sequentially but remain above 40% for the first quarter of fiscal 2027.

F4Q26 Financial Highlights

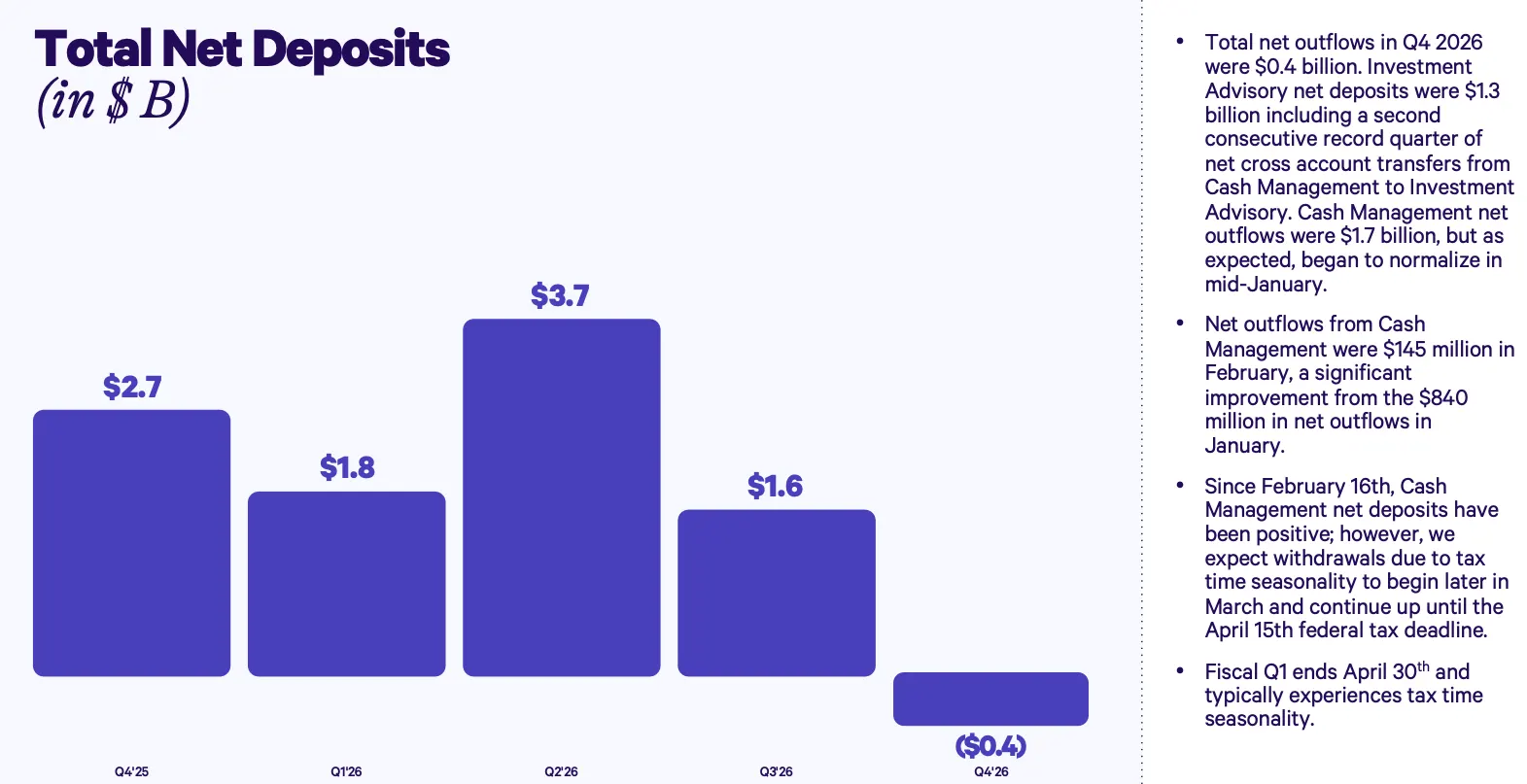

Quarterly total revenue of $96.1 million increased 16% year-over-year primarily driven by a 17% year-over-year increase in Total Platform Assets to $94.1 billion. This includes Investment Advisory Assets of $48.7 billion, which were up 29% year-over-year and Cash Management Assets of $45.4 billion, which were up 7% year-over-year. Change in Total Platform Assets included Total Net Deposits of $6.7 billion in the year and $(360) million in the quarter.

Funded Clients of 1.42 million grew 17% year-over-year. Funded Accounts of 1.84 million grew 16% year-over-year.

GAAP expenses of $310.7 million compared to $51.8 million in the prior year quarter, with the increase due primarily to higher stock-based compensation (SBC) expense primarily tied to one-time, IPO-related SBC expense of $239.0 million. Adjusted operating expenses of $57.1 million increased 15% year-overyear due to higher product development expense, partially offset by lower marketing expense.

GAAP diluted net income (loss) of $(134.8) million compared to $32.1 million in the prior year quarter with the decline due to higher GAAP expenses primarily tied to one-time, IPO-related SBC expense of $239.0 million. GAAP diluted net income margin was (140)%, compared to 39% in the prior year quarter with the decrease primarily driven by one-time, IPO-related SBC expense. GAAP diluted EPS was $(1.31) compared to $0.23 in the prior year quarter driven primarily by one-time, IPO-related SBC expense.

Adjusted EBITDA1 of $44.2 million grew 22% year-over-year. Adjusted EBITDA margin1 was 46%, compared to 44% for the prior year quarter. We expect Adjusted EBITDA margins to decline sequentially but remain above 40% for the fiscal first quarter 2027.

Net cash provided by operating activities was $33.3 million and Free cash flow1 was $33.0 million. Free cash flow conversion ratio1 was 75% for the three months ended January 31, 2026 and 88% in the twelve months ended January 31, 2026. F2026

Financial Highlights

Annual total revenue of $365.0 million increased 18% year-over-year. Annual GAAP expenses of $476.2 million compared to $187.4 million in the prior year with the increase due to higher SBC expense primarily tied to onetime, IPO-related SBC expense of $239.0 million. Annual adjusted operating expenses of $211.1 million increased 19% year-over-year due to higher product development and general & administrative expense, partially offset by lower marketing expense.

Annual GAAP diluted net income (loss) of $(43.2) million compared to $181.8 million in the prior year due to the one-time impact of IPO-related SBC expense of $239.0 million. Annual GAAP diluted net income margin was (12)%, compared to 59% in the prior year with the decrease primarily driven by the same factors.

Annual GAAP diluted EPS was $(0.76) down year-over-year compared to $1.31 in the prior year due primarily to the one-time impact of IPO-related SBC expense.

Annual adjusted EBITDA1 of $170.7 million grew 20% year-over-year. Annual adjusted EBITDA margin1 was 47%, compared to 46% for the twelve months ended January 31, 2025.

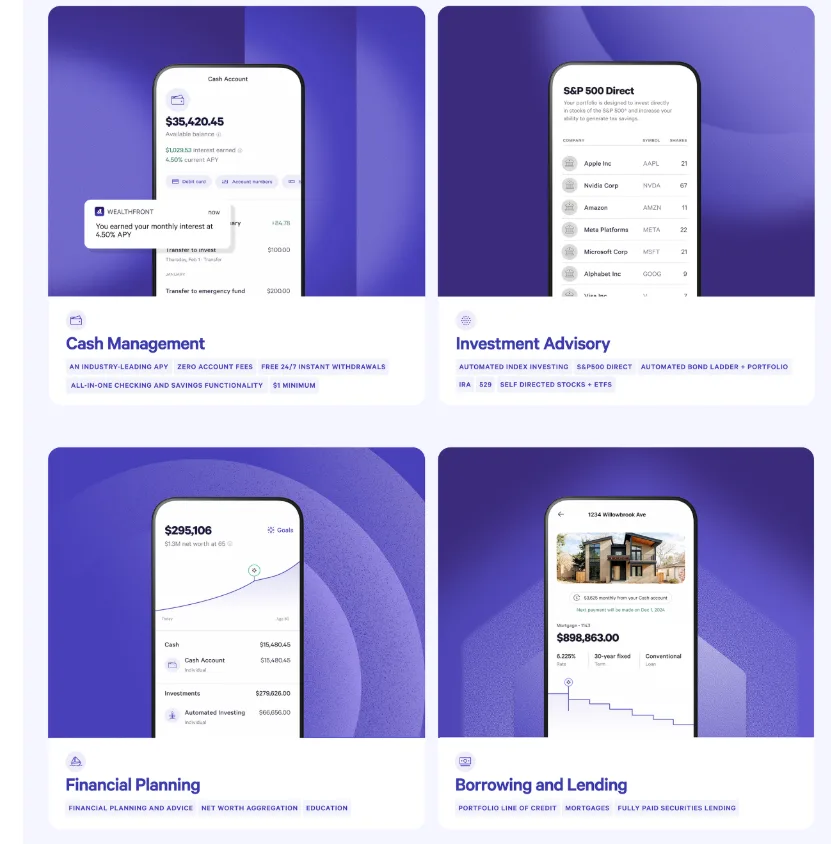

Wealthfront is a next-generation banking and investment management platform built to help individuals manage both their short-term finances and long-term investment goals through automated software-driven services.

At the core of the company’s philosophy is a simple concept: use software to automate investment management, pass the resulting cost savings back to customers, and continually reinvest into the platform to further improve automation and efficiency.

This model allows Wealthfront to provide financial planning, investing, and cash management services at significantly lower costs than traditional advisory firms.

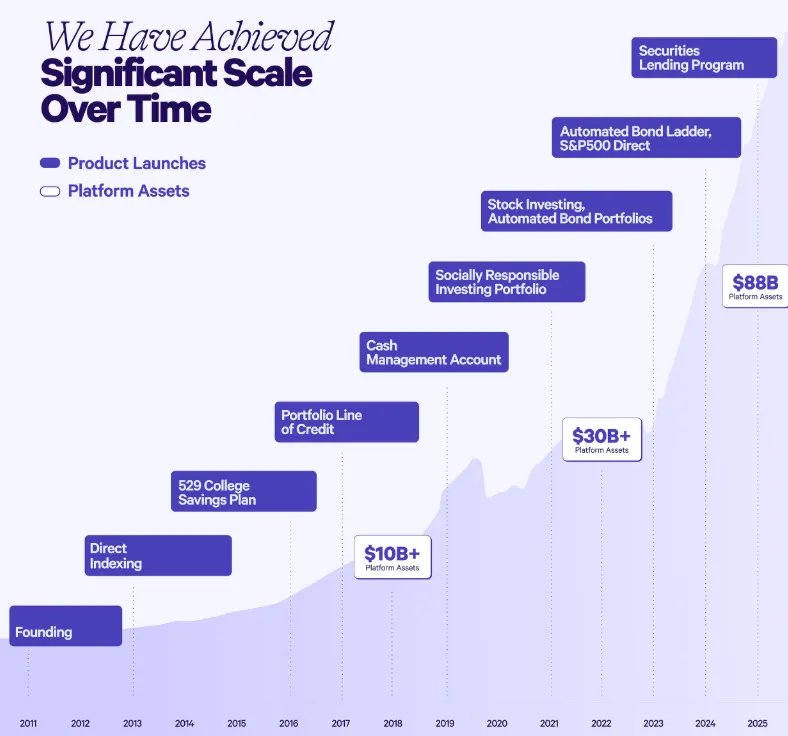

The company was founded in 2008 by Andy Rachleff, one of the original partners at Benchmark Capital. Initially launched under the name kaChing, the platform later pivoted and rebranded as Wealthfront in 2010 as the company refined its focus on automated investment management. Rachleff served two multi-year terms as CEO and now remains involved as Chairman of the Board.

Despite managing a substantial platform, Wealthfront operates with a relatively lean organization of roughly 400 full-time employees. The company currently oversees approximately $93 billion in platform assets across about 1.8 million customer accounts, with assets split roughly evenly between cash management accounts and investment portfolios.

Wealthfront’s typical customer is around 38 years old and generally prefers a fully digital experience rather than working with a traditional financial advisor or wealth manager. The platform initially gained popularity among younger technology professionals, particularly software engineers in Silicon Valley, who were early adopters of automated financial tools.

In fact, during the early growth phase, Wealthfront reportedly offered programs specifically designed to help employees at companies like Twitter and Facebook manage equity compensation following their IPOs.

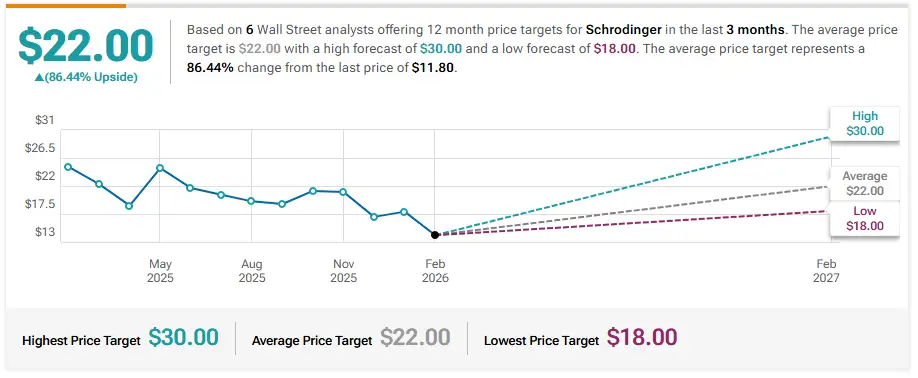

Goldman Sachs Maintains Neutral on Wealthfront, Lowers Price Target to $10.5

Citizens Maintains Market Outperform on Wealthfront, Lowers Price Target to $17

Keefe, Bruyette & Woods Maintains Outperform on Wealthfront, Lowers Price Target to $13.5

RBC Capital Maintains Outperform on Wealthfront, Lowers Price Target to $14

Wells Fargo Maintains Overweight on Wealthfront, Lowers Price Target to $12.5