A Message to the members from JR Sylvester

Purpose of This Report: This is a list of stocks that members asked us to research further. None of these are alerts, buy recommendations, or sell recommendations. The analysis below reflects our opinions and observations as of the date of publication and is subject to change without notice. Always conduct your own due diligence.

February Recap & Strategy Outlook

The months of February and March can best be described as a period of reflection and several “could/should” moments for investors opportunities where trimming profits or exiting weaker positions earlier may have been the right call. At the same time, the broader market dynamic has shifted meaningfully as the U.S./Iran conflict enters its tenth day.

We generally avoid political commentary in these overviews, but when events of this scale occur combined with oil prices moving above $112 at the time of writing it forces markets to begin repricing the economic outlook.

Markets experienced something of a perfect storm this week. Oil prices spiked following escalating tensions involving Iran, sparking renewed concerns around inflation.

At the same time, a weaker payrolls report added to worries about slowing U.S. economic growth. The combination created a stagflationary narrative that weighed on investor sentiment.

Given this backdrop, markets pulled back as investors reassessed the Federal Reserve’s ability and willingness to continue easing policy in such an environment.

The result was a broad risk-off move, with both equities and bonds experiencing selling pressure.

Despite the recent volatility, it’s worth noting that the S&P 500 remains roughly 17% higher over the past year and sits only about 3% below all-time highs.

When oil pushes above $100 per barrel, the entire economy effectively begins to reprice. Oil impacts far more than gasoline it is embedded across transportation, manufacturing, logistics, agriculture, and nearly every segment of the global supply chain. As energy costs rise, inflation tends to follow. That creates a domino effect across the economy. Higher inflation places the Federal Reserve in a difficult position, especially if the market had been expecting a continued rate-cutting cycle one of the primary drivers behind recent bullish sentiment. If inflation accelerates again, the Fed may be forced to pause or even reverse course, potentially shifting from cuts back toward tightening. Higher interest rates typically weaken consumer confidence and spending, which can slow overall economic activity. Additionally, a major refinery disruption during an already tight energy market can trigger a supply shock across the global oil system. When that happens, energy prices, inflation expectations, and monetary policy expectations all shift simultaneously effectively resetting the broader macroeconomic playing field.

Q1–Q2 Outlook

It is likely that volatility will remain elevated in the coming days and weeks as the situation in the Middle East continues to evolve. Geopolitical conflicts historically introduce uncertainty into financial markets. However, history also shows that the market impact of these events is often shorter-lived than many initially expect and can at times create opportunities for disciplined investors.

Looking through the near-term noise, we remain constructive on the broader outlook. Corporate profitability continues to expand across sectors, and fiscal stimulus measures including tax adjustments are gradually filtering through the U.S. and Canadian economies.

At the same time, the ongoing wave of investment in artificial intelligence infrastructure continues to act as a powerful structural tailwind.

There are also early indications that AI-related investment may begin contributing to measurable improvements in productivity growth something that could support economic expansion over the coming years.

Naturally, there remains a risk that a deeper or more prolonged geopolitical conflict could have a larger impact on global markets and economic activity. However, historically these types of shocks have tended to fade over time rather than permanently derail growth trends.

For long-term investors, remaining invested through periods of disruption has consistently proven to be the more effective strategy. While volatility may increase, it often creates opportunities rather than long-term damage to wellpositioned portfolios.

More broadly, the underlying fundamentals for global growth and corporate profitability remain healthy. Most economic indicators continue to point toward steady activity in both the U.S. and global economies. In our view, it would require a large and sustained spike in oil prices to meaningfully disrupt this trajectory.

Q1–Q2 Strategy

By reducing exposure in four positions while initiating only two new ones, we have intentionally created additional dry powder within the portfolio.

This provides flexibility to take advantage of market pullbacks and selectively add to high-conviction names particularly companies we are already actively covering.

Our focus remains on allocating capital toward areas where structural growth trends remain strongest.

Overweight

Technology (AI, robotics, automation)

M&A-driven mid-cap opportunities

Semiconductor infrastructure and AI compute supply chains

Underweight / Avoid

Overextended cyclical sectors facing margin pressure, policy risk, or stretched valuations

Volatility, sector rotations, and tactical opportunities are likely to define the year ahead. In this type of environment, disciplined positioning, timing, and selective capital allocation become more important than ever.

Longs:

These are stocks we have been long for some time and the current BT doesn’t represent other entry prices, The BT is updated weekly for new subscribers to jump in and know when to get out.

These stocks tend to have 6 Month-2 years holding period and is suggested for larger capital Allocations in your portfolio.

Please read the Overviews for full research and instructions on how to trade each name individually

Company: ATS Corporation

Quote: $ATS

BT: $29.72

ST: $48

Sharks Opinion:

ATS is a lower-volume mid-cap name, which means the stock can experience short-term volatility, particularly around earnings or macrodriven market swings.

However, that same lower liquidity can also limit extreme downside moves. Our preferred accumulation level remains around $25, where we believe the risk-reward becomes particularly attractive.

ATS’s most recent earnings call reinforced what we already view as the core strength of the company its positioning within the rapidly expanding industrial automation market. Management continues to emphasize innovation, operational discipline, and long-term execution.

While the company finished the year slightly below expectations, our long-term bullish thesis remains unchanged.

Importantly, ATS is not a single-line industrial company. We view it as a diversified automation platform spanning multiple end markets including life sciences, transportation, food & beverage, and energy. This diversification gives the company resilience while still allowing it to benefit from the structural growth in automation and robotics.

A major component of the ATS growth story has been its disciplined acquisition strategy. To date, the company has completed more than 23 acquisitions, deploying roughly $1.8 billion in capital to build a broad, AI-enabled automation ecosystem.

Key Tailwinds Supporting the Thesis

M&A valuation reset: Recent industry transactions have reinforced higher valuations for AI-driven automation assets. For example, SoftBank’s acquisition of ABB’s robotics business at 2.4× sales and 17.2× EBITDA establishes a meaningful valuation floor for high-quality automation platforms.

Structural manufacturing demand: ATS customers have collectively committed over $350 billion toward U.S. manufacturing investment, strengthening the multi-year automation and reshoring cycle that continues to drive demand for advanced manufacturing solutions. Why We Remain Overweight ATS

Direct exposure to AI-enabled industrial automation

Multi-year demand driven by reshoring and supply-chain localization

Potential valuation re-rating through M&A activity and strategic interest in robotics For these reasons, we continue to maintain our $48 price target for 2026.

Description: ATS Corporation, together with its subsidiaries, provides automation solutions worldwide. The company is involved in planning, designing, building, commissioning, and servicing automated manufacturing and assembly systems, including automation products and test solutions. It also offers pre-automation services comprising discovery and analysis, concept development, simulation, and total cost of ownership modelling; post-automation services, including training, process optimization, preventative maintenance, emergency and on-call support, spare parts, retooling, retrofits, and equipment relocation; and contract manufacturing services, as well as after sales and services.

JP Morgan Maintains Neutral on ATS, Raises Price Target to $35

RBC Capital Maintains Outperform on ATS, Lowers Price Target to C$48

Goldman Sachs Maintains Sell on ATS, Lowers Price Target to $30

Company: ACM Research, Inc

Quote: $ACMR

BT: $32.84

ST: $84 (Price Upgrade)

Sharks Opinion:

In hindsight, trimming some profits in ACMR around the $70 range would have been the prudent move and congratulations to those who took advantage of that opportunity. The stock had clearly gotten ahead of itself after a strong run, so the recent pullback should not come as a major surprise.

That said, the core thesis remains largely intact. If the stock revisits levels near our initial entry point, we would strongly consider adding to the position. While margins have slowed slightly, the change is not significant enough to alter the long-term investment narrative or warrant panic selling.

Since our entry, ACM Research (ACMR) has climbed approximately 57.3%, which already represents a strong return. However, the opportunity still appears compelling when looking deeper at the company’s underlying structure.

A key element of the thesis is ACMR’s 74.6% ownership stake in ACM Shanghai, which carries an estimated valuation of roughly $14.65 billion. Meanwhile, the U.S.-listed parent company currently trades at a market cap of only about $3.3 billion.

This creates a clear “China discount.” In practical terms, investors purchasing the U.S.-listed shares are effectively gaining exposure to the Shanghai business at a substantial discount, while receiving the parent company’s cash position, intellectual property, and global operations at a minimal implied valuation.

ACM Shanghai itself trades more like a highgrowth Chinese technology company, often commanding P/E multiples in the 40–50× range.

At several points over the past year, the market value of ACMR’s stake in Shanghai alone has actually exceeded the entire market capitalization of the U.S. parent. Looking forward, we maintain an updated price target of $84, with a more aggressive stretch scenario of $134 if the valuation gap begins to close.

However, given that ACMR remains far less widely followed than semiconductor leaders like NVIDIA or AMD, the higher-end scenario may take more time to materialize.

One potential catalyst that could help unlock this value is the next semiconductor capital expenditure cycle, which would likely increase demand for wafer cleaning and processing equipment a core segment where ACM Research operates.

Description: ACM Research Inc supplies advanced, innovative capital equipment developed for the world-wide semiconductor industry. Fabricators of advanced integrated circuits, or chips, can use its wet-cleaning and other frontend processing tools in numerous steps to improve product yield, even at increasingly advanced process nodes. It has designed these tools for use in fabricating foundry, logic and memory chips, including dynamic random-access memory, or DRAM, and 3D NAND-flash memory chips. The company also develops, manufactures and sells advanced packaging tools to wafer assembly and packaging customers.

Roth MKM analyst Sujeeva De Silva maintains $ACM Research with a buy rating, and adjusts the target price from $40 to $70.

Roth Capital Reiterates Buy, Raises $50 Price Target

JP Morgan Initiates Coverage with Overweight, Price Target $36

Craig Hallum Downgrades to Hold, Lowers Price Target to $18

Needham Downgrades to Hold, Maintains Price Target to $25

Company: American Superconductor

Quote: AMSC

BT: $31.84

ST: $64

Sharks Opinion:

The stock has moved a bit away from our initial entry following the recent market volatility, but we continue to see opportunity if shares pull back into the $22–$23 range, which would be an area we’d consider adding more exposure.

Fundamentally, the business continues to show solid progress. Over the past five years, AMSC has delivered consistent revenue growth, improving cash profitability, and expanding operating margins, indicating a business model that is becoming both more efficient and more durable.

While AMSC is not a semiconductor manufacturer, its advanced power electronics and superconductor technologies play a critical role in supporting semiconductor fabrication facilities.

This places the company squarely within the broader semiconductor infrastructure and supplychain investment theme, which continues to benefit from global chip demand and fab expansion.

We traded AMSC successfully last year but ultimately exited the position too early, missing the subsequent 100% rally that followed.

After peaking near $70, the stock has since retraced significantly to around $30, which has helped reset expectations and bring valuations back to more attractive levels.

Why We Like It

Supply-chain exposure: AMSC benefits directly from the global semiconductor capital expenditure cycle and continued expansion of fabrication facilities.

Improving fundamentals: Revenue growth and margin expansion indicate a strengthening operational foundation.

Risk/reward setup: The recent pullback provides a compelling opportunity for investors willing to tolerate near-term volatility in exchange for longerterm upside.

Following the strong earnings report and the recent price move, we are maintaining our $64 price target and will continue monitoring the position closely as semiconductor demand and infrastructure spending remain key drivers for the company’s growth trajectory.

Description: American Superconductor Corp generates the ideas, technologies, and solutions that meet the world's demand for smarter, cleaner, and energy. Through its Windtec Solutions, the company enables manufacturers to launch wind turbines quickly, effectively, and profitably. Through its Gridtec Solutions, the company provides engineering planning services and grid systems that optimize network reliability, efficiency, and performance. The company's segment includes Grid and Wind. It generates maximum revenue from the Grid segment.

Clear Street Reiterates Buy on American Superconductor, Maintains $52 Price Target

Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Roth MKM Reiterates Buy on American Superconductor, Maintains $29 Price Target

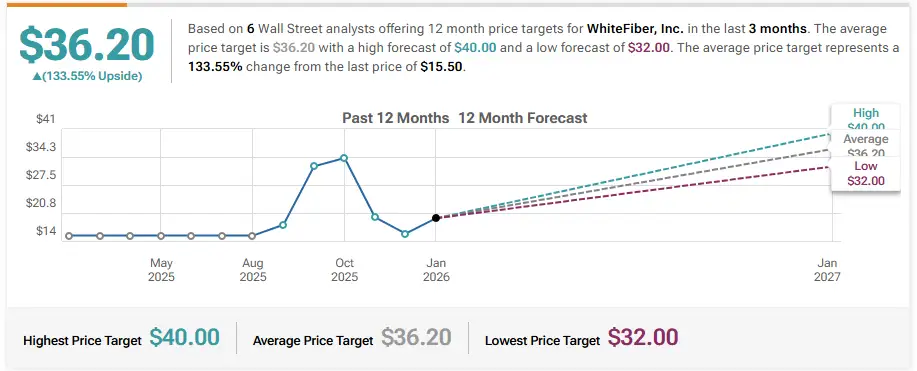

Company: WhiteFiber, Inc

Quote: $WYFI

BT: $16.70

ST: $32

Sharks Opinion:

WhiteFiber is a new name for us, uncovered through last month's 13F review process.

While we may be early especially with the stock selling off into year-end the AI infrastructure theme remains firmly intact.

At current levels, we think it could justify a starter position given the potential asymmetric upside.

The AI infrastructure thesis is straightforward: specialized compute capacity is scarce, demand is accelerating rapidly, and customers are willing to pay premium pricing for access.

WhiteFiber represents one of the few pure-play vehicles tied directly to this buildout. Instead of owning a small slice of a diversified cloud giant like Amazon or Microsoft, investors are gaining exposure to a focused operator that could control 200–300 MW of high-value data center capacity purpose-built for AI workloads.

There are risks. Bit Digital owns roughly 80% of WhiteFiber, meaning any sizable share sale could pressure the stock. That said, it also creates strategic alignment Bit Digital is incentivized to see WhiteFiber scale successfully.

The AI gold rush is underway. WhiteFiber is positioning itself to supply the pickaxes and shovels while also building the mines.

The real question is not whether AI infrastructure will be valuable. It’s whether WhiteFiber can execute quickly enough to secure meaningful share before the competitive window narrows.

Description: Whitefiber Inc is a provider of artificial intelligence infrastructure solutions. The company owns high-performance computing data centers and provide cloud-based HPC graphics processing units services, which it terms cloud services, for customers such as AI application and machine learning developers. Its Tier-3 data centers provide hosting and colocation services. Its cloud services support generative AI workstreams, especially training and inference. It has two reportable segments: cloud services and colocation services. The cloud services segment generates revenue from providing high performance computing services to support generative AI workstreams. Colocation services generate revenue by providing customers with physical space, power and cooling within the data center facility.

HC Wainwright & Co. Reiterates Buy on Whitefiber, Maintains $34 Price Target

B. Riley Securities Maintains Buy on Whitefiber, Lowers Price Target to $40

Compass Point Initiates Coverage On Whitefiber with Buy Rating, Announces Price Target of $32

Citizens Initiates Coverage On Whitefiber with Market Outperform Rating, Announces Price Target of $37

Roth Capital Maintains Buy on Whitefiber, Lowers Price Target to $37

Needham Maintains Buy on Whitefiber, Lowers Price Target to $38

Company: Chemours Company

Quote: $CC

BT: $19.62

ST: $32

Sharks Opinion:

Chemours has been somewhat off its footing since its latest earnings report, but we believe the broader setup for upside still remains intact once market conditions stabilize. If the stock continues to pull back, $15 remains our next target area to add exposure.

The recent selloff has coincided with a decline in Adjusted EBITDA, with full-year estimates now around $750 million, down significantly from the $1.4 billion generated in 2021. This reflects the prolonged downturn across Chemours’ two highly cyclical operating segments.

The cyclical nature of the business is clear, but so is the longer-term setup. Chemours has been on our radar since the beginning of the year and has quietly trended higher on steady, above-average volume, which often signals institutional accumulation rather than speculative trading. Notably, that relative strength held even during periods when the broader market experienced choppy conditions.

We believe this dynamic continues to position CC well as capital begins rotating away from crowded mega-cap names and into mid- and small-cap cyclical opportunities. The stock currently trades at a discount relative to both revenue and normalized earnings potential. At the same time, Chemours still benefits from its structure as a spin-off from a major conglomerate — a profile that historically can lead to valuation re-ratings once the underlying business cycle improves.

Strategy

With a high probability of fundamental recovery over the next two to three years, and meaningful upside leverage tied to normalized EBITDA levels, Chemours presents a compelling opportunity for aggressive, long-term investors.

That said, investors should remain aware of the inherent volatility tied to Chemours’ cyclical end markets and the swings in earnings power that can occur across economic cycles.

For these reasons, we are maintaining our $32 price target for the year while continuing to monitor the company’s operational recovery and broader market conditions.

Description: The Chemours Co is a provider of chemicals. It delivers customized solutions with a wide range of industrial and specialty chemicals products for various markets including coatings, plastics, refrigeration, air conditioning, etc. The company's operating segments include Titanium Technologies, Thermal & Specialized Solutions, and Advanced Performance Materials. It generates maximum revenue from the Titanium Technologies segment. The Titanium Technologies segment is a producer of TiO2 pigment, a premium white pigment used to deliver whiteness, brightness, opacity, durability, efficiency, and protection across a variety of applications. Geographically, the company derives a majority of its revenue from North America.

UBS Maintains Buy on Chemours, Raises Price Target to $23

BMO Capital Maintains Outperform on Chemours, Lowers Price Target to $19

JP Morgan Maintains Neutral on Chemours, Raises Price Target to $17

Morgan Stanley Maintains Equal-Weight on Chemours, Raises Price Target to $17

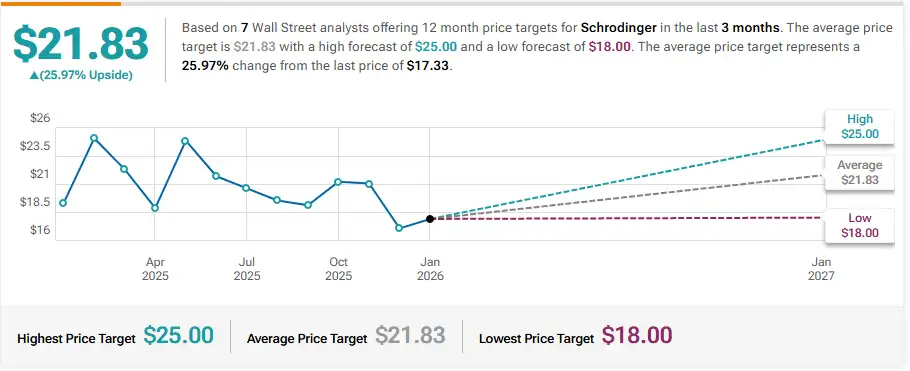

Company: Schrodinger, Inc

Quote: SDGR

BT: $16.54

ST: $28

Sharks Opinion:

Since our starter position was initiated, the stock has pulled back roughly 22%. At current levels, we believe the risk-reward profile has improved significantly, with meaningful value beginning to emerge.

From a valuation perspective, SDGR currently trades at approximately 3× 2026 consensus revenue, a level we view as disconnected from the long-term potential of its computational platform and its growing role within AI-driven drug discovery.

For investors looking to gain exposure to the AI theme within healthcare, without taking on the full binary risk associated with individual clinical trial outcomes, SDGR continues to represent a compelling way to express that thesis.

Looking ahead, the market’s focus will shift toward 2026 software ACV guidance and management’s longer-term goal of achieving positive adjusted EBITDA by the end of 2028.

While the company’s Q4 results offered reassurance that the business remains on track, it is also worth noting that expectations had already reset lower heading into the report, which helped stabilize sentiment.

For these reasons, we are maintaining our 2026 price objective of $28 while continuing to monitor the company’s progress in scaling its platform and expanding adoption across pharmaceutical and biotech partners.

Description: Schrodinger Inc is a healthcarebased software company. Its operating segments are Software and Drug discovery. Through the Software segment, the company is focused on selling software to transform drug discovery across the life sciences industry and customers in materials science industries. In the Drug discovery segment, it is engaged in generating revenue from a portfolio of preclinical and clinical programs, internally and through collaborations. It generates revenue from the sales of software solutions and from research funding and milestone payments from its drug discovery collaborations.

Keybanc Maintains Overweight on Schrodinger, Lowers Price Target to $25

UBS Initiates Coverage On Schrodinger with Neutral Rating, Announces Price Target of $18

B of A Securities Upgrades Schrodinger to Buy, Maintains Price Target to $24

Company: Pony AI Inc

Quote: $PONY

BT: $13.53

ST: $28

Sharks Opinion:

Pony jumped nicely following our initial re-entry, but the stock has since pulled back and flattened out amid the broader volatility in global markets.

Given the recent escalation surrounding the Iran conflict and the potential ripple effects it could have on global growth particularly for export-driven economies like China we are actively evaluating whether trimming some exposure may be the prudent move.

This remains a difficult call. On one hand, the longterm thesis around Pony.ai as a leader in autonomous mobility and robotaxi infrastructure remains intact. The company continues to scale its autonomous driving platform and robotaxi services, positioning itself within a rapidly evolving transportation technology market.

On the other hand, geopolitical developments and macro uncertainty can weigh disproportionately on China-linked technology names, regardless of underlying fundamentals.

For now, we are taking a tape-first approach. If momentum begins to deteriorate further, trimming could be warranted. However, if the stock stabilizes and buyers step back in, maintaining the position may still make sense given the longerterm growth narrative.

At this stage, the trade can realistically go either direction, and we will continue monitoring price action closely before making a final decision.

Description: Pony AI Inc is an artificial intelligence technology company that is principally engaged in the operation and development of autonomous vehicles. It operates fully driverless robotaxis through the PonyPilot mobile app in Beijing, Shanghai, Guangzhou, and Shenzhen. The company operates a fleet of robotaxis. The Group conducts its operations mainly in the People's Republic of China (PRC) and the United States of America (U.S.) through subsidiaries. Key revenue is generated from the People's Republic of China.

Citigroup Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $29

UBS Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

Deutsche Bank Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

B of A Securities Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $18