Robot Stocks Overview 2025

Ten years ago, if someone told you that by 2025 artificial intelligence would be powering human-shaped robots, you might’ve thought we were finally living in a sci-fi dream. Now that it’s here, it turns out the real story isn’t just about fantasy it’s about a market on the verge of exponential growth.

The key difference today is that AI is finally useful in the real world. With the advancement of large language models and visual perception systems, robots now have a brain that justifies their battery life.

In other words, embodied AI the holy grail of robotics has left the lab and is starting to take its first commercial steps.

A Market on the Move

According to Bank of America, global humanoid robot sales are expected to hit 1 million units per year by 2030, with 3 billion robots projected to be in service by 2060. Importantly, the vast majority 65% are expected to operate in domestic environments, while 32% support services like logistics and hospitality, and only 3% remain in traditional industrial roles.

This represents a clear shift: robots are moving up the value chain, from factory automation toward general-purpose home and service applications.

The economic tailwinds are clear. Cost is dropping fast. Today’s unit costs average around $35,000, but that’s expected to fall to $17,000 by 2030 closely tracking the pricing of China’s Unitree G1 robot unveiled at CES 2025. This rapid decline in cost sets the stage for mass adoption, particularly in the home.

Leaders in the Field

The U.S. market is currently led by Boston Dynamics, Agility Robotics, and Tesla:

Boston Dynamics’ Atlas is already being tested by Hyundai for factory use.

Agility’s Digit is currently deployed at Amazon fulfillment centers.

Tesla’s Optimus, now in its third iteration, is being tested internally ahead of planned mass production in 2026.

Why This Matters Now

We’re approaching an inflection point. AI advances are intersecting with breakthroughs in miniaturization, component affordability, and a growing labor gap, especially in aging societies like Japan. These forces are accelerating demand for automation not just in businesses, but at the personal level.

From an investment perspective, this is an opportunity to build a basket of names exposed to this emerging trend companies that currently have understated forward estimates due to cyclical biases. The reality is that very few forecasts today are pricing in what happens when humanoid robots move from novelty to necessity.

Looking Ahead

Creating a humanoid robot that can truly serve as a general-purpose assistant is still about a decade away, requiring improvements in both AI models and mechanical hardware. But the path is clear. As costs fall and societal acceptance grows, this segment is likely to see one of the most dramatic transformations of the coming decade.

In short, the age of robots is no longer a question of if it's a question of when, and that when may be a lot sooner than most expect.

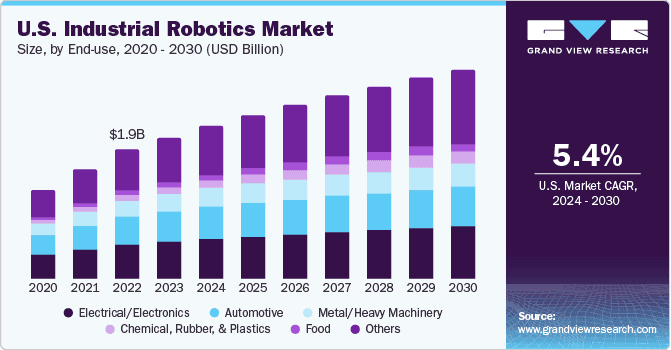

In 2024, the U.S. made up over 7% of the global industrial robotics market a sign that American manufacturing is quietly undergoing one of its most transformative shifts in decades. At the heart of this change is a growing reliance on advanced robotics, driven by demand for smarter, more flexible, and scalable production.

Much of this demand is coming from sectors like automotive, where the electric vehicle (EV) boom is reshaping how cars are built. High-volume EV production lines are now turning to automated robotic systems to meet scale, speed, and precision requirements. And that’s just the beginning.

Automation’s Next Chapter

The fusion of AI and machine learning with industrial robotics is ushering in a new era—one where machines are not just performing tasks, but learning and adapting in real-time. Add 5G connectivity to the mix, and suddenly robots are communicating with near-zero latency, enabling tighter coordination and vastly improved efficiency across entire production lines.

All of this is accelerating the shift toward smart manufacturing. Across sectors—electronics, metals, heavy machinery—factories are evolving from static, linear assembly lines into agile, intelligent ecosystems. Robots are now handling everything from assembly and welding to cleanroom precision tasks, keeping plants running at peak capacity.

Capital Is Flowing In

Investment continues to pour into this sector. The reasons are obvious: increased demand for electronics, cars, and infrastructure is putting pressure on manufacturers to scale up without sacrificing precision. Robotics especially industrial-grade platforms are proving to be the solution of choice.

And Yet… Why Humanoids?

All of this brings us back to the bigger picture humanoid robots. Not everyone in the space is going to like this, but here’s the reality: we’re not betting on a future where humanoids become perfectly autonomous AGI-powered butlers. That’s a long game and we don’t need to wait for it.

Instead, we’re focused on the bridge, not the destination. A large part of the value will be created long before general-purpose humanoids exist in every home. In fact, humanoid robots don’t have to be fully autonomous to provide utility, drive productivity, or generate meaningful revenue.

Like the industrial sector, it’s the intermediate applications in logistics, warehousing, basic domestic support that are already creating investable opportunities. We believe this is where the next wave of winners will emerge.

Because while AGI may be years away, ubiquitous humanoid assistance is already within reach.

Why Robotics Supply Chain Stocks Haven’t Re-Rated ...Yet

Despite major strides in embodied AI and growing mainstream buzz around humanoid robots, the robotics supply chain has yet to see a broad market re-rating. That’s not because of a lack of innovation. Instead, the drag comes from macro headwinds namely, the cyclical downturn in autos, the threat of fiscal tightening, and continued weakness in consumer electronics.

The Anatomy of a Robots And Its Risk Profile

Robots are not simple machines. They are built from a complex ecosystem of components: precision motors and actuators for movement, semiconductors and computing power to enable AI, and sensors to interpret the physical world around them. All of these rely on global trade flows and are vulnerable to supply chain disruptions and geopolitical risk.

This makes robotics exposure a macro-sensitive investment, not unlike semiconductors or industrial machinery.

The China Factor

Zooming out, there’s another dynamic that investors are watching closely: China controls 63% of the global humanoid robot supply chain, according to Morgan Stanley. That dominance is concentrated in “body” parts hardware components, actuators, sensors, and lithium-ion batteries. These aren’t optional pieces of the puzzle they’re essential.

That kind of concentration introduces both fragility and leverage. Trade tensions, export controls, or industrial policy changes can ripple through the entire robotics sector, especially as geopolitical rivalries sharpen.

What This Means for Investors

Until these external risks stabilize—or until markets begin to price in robotics as a core secular growth theme rather than a cyclical derivative many of the supply chain names will remain under-owned.

But the moment that shifts, re-ratings could be swift and substantial particularly for companies sitting at the crossroads of AI, automation, and next-gen manufacturing

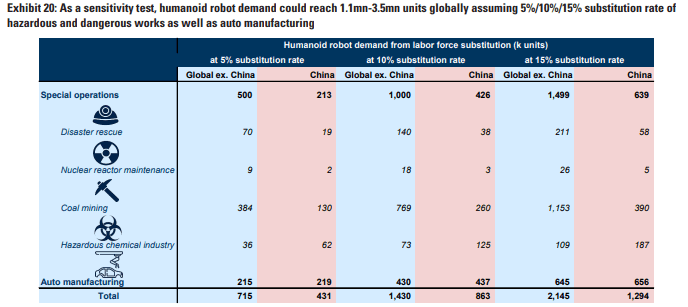

The Real Demand for Humanoids May Come From Jobs No One Wants to Do

When most people picture humanoid robots, they imagine them serving coffee or folding laundry at home but the real near-term demand lies elsewhere. Based on current technological capabilities, humanoids appear best suited for structured environments, particularly within manufacturing.

Think EV assembly lines, parts sorting, or repetitive industrial workflows. These are tasks that require precision but not creativity exactly the kind of work robots are beginning to excel at.

But the more intriguing opportunity lies in hazardous or high-risk jobs the kind of tasks that humans are either reluctant to do or shouldn't be doing in the first place. Mining operations, chemical exposure cleanup, disaster response, and certain military applications all come to mind.

Thanks to advances in AI, humanoids are becoming more adaptable to dynamic environments, making them uniquely suited for roles where safety, not speed or cost, is the top concern. It’s in these high-risk scenarios that customers are most likely to accept a premium price point for robots—because the alternative is exposing humans to danger.

Investment is ramping up to meet that demand. Across the U.S. and Asia, we’re seeing a surge in capital deployment into startups focused on humanoid robotics, while legacy companies are creating new robotics divisions to gain exposure to this trend. China, as always, is moving with intent providing early government support and leveraging its domestic supply chain advantages. The race is very much on.

Looking forward, the long-term projections are staggering. By 2050, analysts expect roughly 90% of humanoids around 930 million robots to be used for repetitive, simple, and structured work. That means most robots won’t be washing dishes in a suburban kitchen, but performing vital commercial and industrial tasks at scale.

China is expected to lead the world in deployment, with over 300 million humanoids in use by mid-century. The U.S. is forecasted to reach nearly 78 million, a notable upgrade from earlier estimates of 63 million.

This is the path to ubiquity not hype or sci-fi dreams, but filling the labor voids in places where humans either can’t or won’t go.

Humanoid robots have long sat at the intersection of aspiration and affordability. In 2024, a high-spec humanoid in a developed market cost around $200,000 a figure that has largely confined these machines to R&D labs, industrial pilots, and the PR videos of tech-forward automakers.

But now, the cost curve is starting to bend.

Downward Pressure on Price, Upward Pressure on Opportunity

According to Morgan Stanley Research, average humanoid costs are expected to fall to $150,000 by 2028 and as low as $50,000 by 2050 in high-income markets. In developing economies that can lean more heavily on China’s vertically integrated supply chain, that number could drop to $15,000.

This shift has massive implications for adoption. By 2050, 15 million U.S. households could own a humanoid robot roughly 10% of the country.

Penetration rates would vary by income, from just 3% of households earning $50K–$75K annually, to one-third of households making over $200K. China, with its affordability edge, could still see a higher unit count overall, but a much smaller per-capita penetration.

The Real Levers Behind the Price Decline

Traditional models have assumed a slow and linear cost decline but they may be too conservative. Historical data shows that robot prices dropped ~50% over the last decade without a hit to gross margins. The implication? Robotics companies have become proficient at driving cost efficiency without sacrificing profitability.

This time, a similar story is playing out.... only faster:

3D printing is reducing both the weight and material usage of key structural components, cutting costs up to 75%.

Advanced design optimization and shifts in manufacturing techniques (e.g., moving from electric discharge machining to cheaper mechanical machining for critical parts like T-screws) are accelerating the cost curve further.

The bill of materials (BOM) for high-spec humanoids has dropped from ~$250K in 2023 to around $150K today a 40% year-over-year decline, far steeper than previously modeled 15–20% annual reductions.

Hardware Bottlenecks And the Race to Solve Them

Despite the progress, scaling remains bottlenecked by key components particularly linear actuators, where companies like Tesla are using high-precision planetary roller screws. But production is still limited:

High-precision grinding machines needed to produce these screws come almost exclusively from Japan and Europe, and exports are increasingly restricted.

Domestic manufacturers lack technical know-how, making them reliant on foreign players for now.

Manufacturing throughput remains slow, with some components taking over an hour per unit to produce.

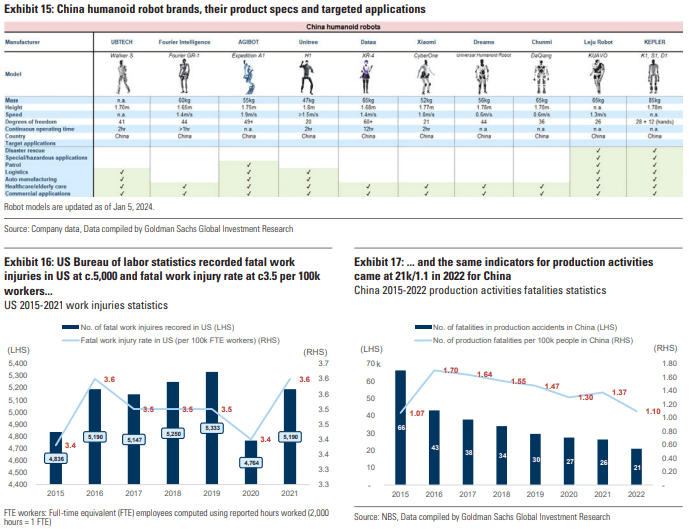

China’s Quiet Domination in Humanoid Robotics

While headlines in the West focus on AI models and autonomous vehicles, a different story is playing out across the Pacific: China is rapidly outpacing the U.S. in the development and deployment of AI-enabled robotics humanoids included.

Unlike the U.S. market, where humanoids are being engineered for industrial, service, and eventually domestic utility with increasingly advanced specs, China is leaning into simpler, more scalable applications notably entertainment and education. These verticals require lower technological complexity, but provide high-volume use cases that help build domestic momentum.

Why China’s Ecosystem Is Pulling Ahead

A few structural advantages are enabling China to take the lead:

Massive internal demand: China’s domestic market size allows for scale testing, iteration, and adoption that few countries can match.

Full-spectrum manufacturing control: The country has extended its global leadership in manufacturing to the robotics value chain. This includes everything from sensor production to actuator assembly.

Top-down policy alignment: National-level support for “embodied AI” is turning government attention and capital toward robotics. This is fostering deep tech clusters and accelerating startup formation.

As Sheng Zhong, Morgan Stanley’s Head of Industrials Research, recently put it:

“It is becoming apparent that national support for embodied AI may be far greater in China than in any other nation, driving continued innovation and capital formation. In our opinion, China's lead in AI-robotics may need to widen before rivals, including the U.S., pay closer attention.”

Closing the Precision Gap

Historically, Chinese robotics manufacturers have lagged behind Western peers in component precision and control fidelity particularly in areas like linear actuation, force sensing, and AI integration.

But that’s beginning to change.

Chinese supply-chain players are actively working to close the performance gap through:

New design architectures tailored for agility and lightweight motion;

Refined manufacturing processes to enable tighter tolerances and repeatability

Next-gen materials that reduce friction and wear

On-device AI algorithms that allow more adaptive and precise behavior in real time.

These efforts are not just incremental. They’re part of a broad national push to control the full stack of embodied AI from the silicon to the software.

The Value Chain Behind Humanoid Robots: Who Stands to Win

While the U.S. has some front-runners in humanoid design think Tesla, Apptronik, and Figure China remains strategically positioned to dominate when these machines transition from R&D novelties to mass-market tools.

There are some leading U.S. players in humanoid design and development at this stage, but China could catch up when humanoids reach downstream application and mass production, riding on its strong self-sufficient supply chain.

That statement carries weight and concern.

Because while the U.S. may lead in humanoid architecture, vision, and control algorithms, hardware is where the real battle lies and where the U.S. is at a structural disadvantage.

The Hardware Dependency Problem

Today, there are very few U.S.-based alternatives for many critical components used in humanoids:

High-precision planetary screws

Compact harmonic reducers

Lightweight but high-torque motors

Next-gen battery cells

Thermal and power management systems

Nearly every humanoid developer whether in North America, Europe, or Asia is reliant on Asia’s (and particularly China’s) manufacturing ecosystem to build, scale, and ship.

So while the Western players focus on intelligence and form, the foundational parts are still almost entirely made in China or its neighbors. This is not a short-term supply gap; it's a structural asymmetry.

Who’s in the Value Chain?

If you’ve made it this far, chances are you’re not just interested in the narrative you’re looking for exposure. Let’s talk about where the value actually lies:

1. Core Component Manufacturers

These are the companies building the essential parts—actuators, joints, batteries, screws, sensors—that power every humanoid:

Harmonic Drive Systems (Japan): High-precision motion control

Nabtesco (Japan): Compact reducers for robotic joints

Hengli Hydraulic (China): Precision roller screws

EVE Energy, CATL (China): Battery tech for mobile robotics

2. System Integrators

These firms assemble the brain and body, integrating AI with hardware:

Tesla (USA): Optimus Gen 2 testing in Gigafactories

Agility Robotics (USA): Digit deployed in Amazon warehouses

UBTECH, Fourier Intelligence (China): Educational and service humanoids

3. AI & Perception Layer

A critical layer where U.S. firms excel—language models, visual perception, spatial navigation:

NVIDIA: Omniverse for sim-to-real robotics training

Qualcomm: AI-on-the-edge processing chips

OpenAI, DeepMind, Boston Dynamics AI Institute

4. Enablers in the Background

These are the companies powering development through simulation, cloud robotics, and compute:

Unity / Unreal Engine: Simulation and training environments

Amazon Web Services (AWS): Cloud robotics infrastructure

TSMC, ASML: Semiconductor backbones enabling real-time inference

The Bottom Line

Humanoids aren't just about flashy demos or general-purpose AGI. They represent a multi-decade hardware-software convergence story and investors who understand the value chain, not just the headline, will be better positioned to benefit.

In the short term, the U.S. leads in software. But hardware wins markets, and China’s grip on the physical components of humanoids gives it the kind of leverage the West currently lacks.

The smarter play? Don’t pick a single robot. Pick the supply chain.

If you’re still with us by now, it seems like you’re interested in the companies that will benefit from this theme.

So let’s unravel the value chain behind robots.