This is a list of stocks that members asked us to do extra research on none of these are alerts/buy/sell recommendations.

Members overview #9

Author

jralex

Date

Jul 8, 2025

Company: Kratos Defense & Security Solutions

Quote: $KTOS

BT: We can’t confidently assign a baseline target at this level, largely due to our historical trades in the name. While that introduces some bias, the reality is we’d prefer to see shares fall back into the $20 range perhaps triggered by a secondary offering before considering re-entry, assuming defense demand remains intact.

ST: $60+ A breakout is possible if momentum behind the Golden Dome initiative materializes. This remains the key near-term swing catalyst.

Sharks Opinion:

For long-time Sharks members, KTOS is a name etched in early success. It was one of the first big wins we booked as a group accumulating shares near $4 and exiting north of $12. Since then, we’ve mostly let it run without us.

But what’s changed?

In truth not much. Kratos is still the same high-beta defense contractor focused on unmanned systems and tactical tech. What has changed is scale. Revenue is much higher, and so is the share price.

Yet in our view, the macro backdrop now heavily favors names like KTOS. The global defense environment is evolving quickly, with autonomous systems, counter-UAS, and precision targeting gaining priority.

We don’t expect a straight-line rally, but as long as defense budgets rise and unmanned platforms stay a strategic priority, Kratos should continue to grow into its multiple.

That said, patience is required here. At current levels, the risk/reward skews cautious. But if you get a pullback tied to dilution or macro jitters and defense demand holds we’d absolutely reconsider our position.

Description: Kratos Defense & Security Solutions, Inc., a technology company, provides technology, products, and system and software for the defense, national security, and commercial markets in the United States, other North America, the Asia Pacific, the Middle East, Europe, and Internationally.

Kratos Defense is beginning to reassert its edge in the unmanned systems space and early signs from Q1 suggest that narrative could gain momentum into 2026.

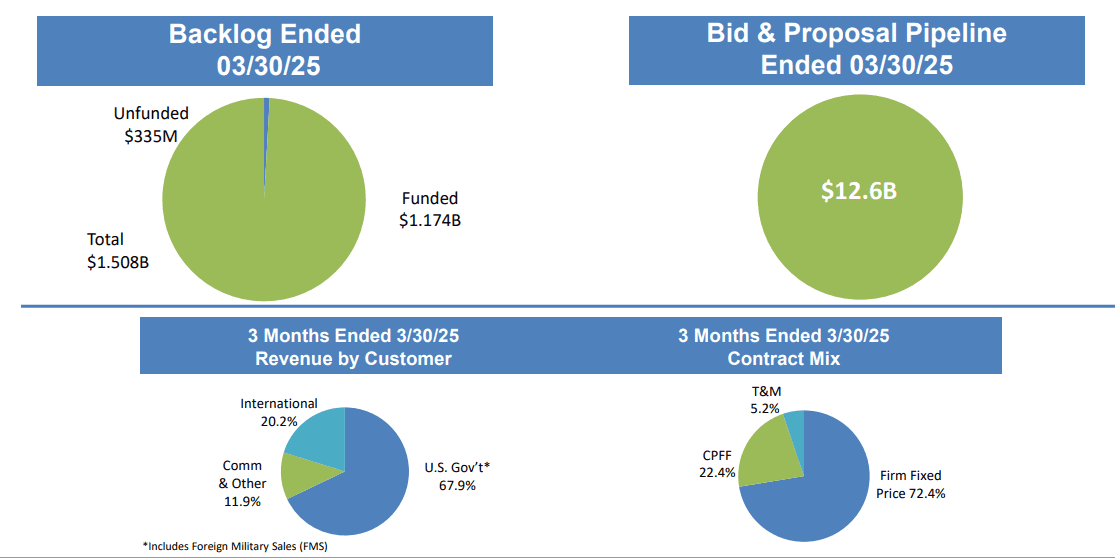

In the latest quarter, Kratos’ Unmanned Systems segment delivered $63.1 million in revenue, up 6.2% year-over-year excluding acquisitions. Just as importantly, the company reported 12-month bookings of $1.4 billion, boosting total backlog to $1.5 billion as of March 30 up from $1.445 billion at the end of 2024.

On the Q1 earnings call held May 7, CEO Eric DeMarco revealed a key development: Kratos has begun production of two next-gen hypersonic drones Aeronis and Dark Fury. The latter, Dark Fury, has already completed successful hypersonic test flights. DeMarco emphasized the platform’s “incredible speed, range, and precision” at an “extremely low cost point.”

What does this mean? Kratos is aiming to redefine the economics of hypersonic warfare.

According to the company, revenue from these hypersonic platforms will ramp later this year and accelerate into 2026, positioning Kratos as a strategic leader in a domain few players can compete in.

Why does this matter? Hypersonic drones are expected to offer significant tactical advantages, particularly in long-range precision strike capabilities and survivability. Their speed makes them extremely difficult to intercept potentially giving the U.S. military an edge in contested environments.

Kratos Defense (KTOS) isn’t your average military contractor.

This is a company engineering the future of warfare across land, air, sea, space—and even cyberspace—while remaining affordable and scalable enough to meet modern defense needs.

Kratos operates through four distinct but highly synergistic business segments:

🔹 Unmanned Systems: This is the heartbeat of the Kratos growth story. Kratos manufactures a suite of tactical unmanned aerial vehicles (UAVs), including the Valkyrie, Mako, and Gremlin all designed for combat applications. Supporting these systems are Kratos’ own ground control stations (GCS) and advanced jet turbine engines built in-house for both UAVs and cruise missiles.

🔹 Space Systems: Kratos is quietly becoming a key enabler of satellite and space communication infrastructure. From antenna systems to full ground stations, the company serves customers looking for turnkey solutions across telemetry, tracking, and command.

🔹 C5ISR Systems: In this segment, Kratos delivers a wide range of capabilities—from radar programs and combat systems to cyber-secure command-and-control platforms. Their systems support missile defense, directed energy weapons, and more.

🔹 Warfighter Readiness: This unit builds next-generation simulation systems, aircrew training centers, and provides ongoing sustainment and curriculum development services—critical for modern force preparedness.

The UAV Edge: Valkyrie + F-35 Integration is a Game-Changer

Last November, the U.S. Air Force validated one of Kratos’ most promising platforms: the XQ-58A Valkyrie. In coordinated tests, Valkyrie drones flew alongside manned F-35A fighter jets, operated either autonomously or by the F-35 pilot. This proved not just technical integration—but tactical flexibility.

“The Valkyrie’s low cost enhances the Air Force’s ability to execute more daring missions without endangering human pilots.”

Interesting Engineering

The implication? Kratos has cracked the code on cost-effective autonomy. These drones can operate independently, coordinate in real time with 5th-gen aircraft, and carry out dangerous or high-value missions. With operating ceilings above 45,000 feet, ranges over 3,000 miles, and air-to-air missile capability all without requiring a runway these are not toys. They're tools for modern warfare.

AI-enabled autonomous capabilities make Kratos' drones highly valuable in an era where unmanned operations are no longer optional.

The company has relentlessly driven down costs, improving margins and scaling potential.

From Valkyrie to space-ground infrastructure, KTOS is attacking from all sidesand remains a name we believe the market underappreciates.

Kratos is no longer just a speculative defense play. It’s now a mission-critical, multi-domain tech supplier and a serious contender in the future of combat autonomy.

Kratos Defense (KTOS) delivered a solid performance in Q1 2025, showing that its diversified defense platform continues to generate real momentum even as it invests heavily in next-gen technology.

By the numbers:

Revenue: $302.6M, up 7.4% YoY, entirely organic

Adjusted EPS: $0.12 vs. $0.11 last year

GAAP Net Income: $4.5M, up from $1.3M

Operating cash flow: -$29.2M, due to higher working capital from growth

Free cash flow: -$51.8M, reflecting $22.6M in capex tied to major R&D and production ramps

Segment breakdown:

Unmanned Systems (KUS): $63.1M in revenue (+6.2% YoY), largely on increased target drone volume. Operating loss widened slightly to $1.7M due to continued investment and scale-up.

KGS Segment: Up 7.8%, with standout growth in Defense Rocket Systems, Microwave Products, and C5ISR—up between 13.1% and 18.7%.

The big picture:

Yes, Kratos burned cash this quarter. But that burn was strategic tied directly to inventory build-up, production ramps, and investment in key R&D, especially in Space, Satellite, Unmanned Systems, and Microwave Electronics.

In our view, this is exactly what you want from a high-leverage, high-potential name in the defense space: investing ahead of contracts and growing into its backlog, which now sits at $1.5 billion.

Bottom line:

Kratos isn’t a cash cow yet. But it’s planting seeds in all the right places, and Q1 proves this team knows how to scale. A bet on KTOS is a bet on unmanned warfare and national defense priorities accelerating over the next 2–3 years. We think that bet is looking smarter by the quarter.

Forget Notre Dame. The real Golden Dome we’re watching could be the biggest U.S. defense initiative in decades potentially even rivaling Reagan’s original Star Wars program.

And with federal spending ballooning from $4.45T in 2019 to $7.03T in 2025 (+58%), and another $89.3T expected through 2035, the real question isn’t if new defense tech will get funded it’s who will win the contracts.

What is the Golden Dome?

Modeled loosely after Israel’s Iron Dome system, this is America’s answer to modern aerial threats but on steroids.

Where Iron Dome intercepts low-altitude projectiles with 85–90% success rates, the Golden Dome aims higher and faster, integrating hypersonic defense to intercept missiles and drones at speeds exceeding Mach 5.

That’s where Kratos Defense (KTOS) comes in.

Kratos: A Pure-Play Hypersonic Winner?

In January, Kratos received a Pentagon contract worth up to $1.45B to build out the MACH-TB 2.0 hypersonic testbed.

They’re also developing their own hypersonic drone tech, building on a portfolio that already includes the Valkyrie, one of the most advanced autonomous jet drones in the world.

While Lockheed and Raytheon will also benefit, Kratos’s $4B market cap makes it a far more concentrated and asymmetric play on the Golden Dome thesis.

This is exactly the kind of long-term, tech-levered catalyst that can rerate a name like KTOS in a hurry. Especially if geopolitical tensions keep pushing hypersonics and autonomous systems to the top of the Pentagon’s priority list.

Noble Capital Markets Maintains Outperform on Kratos Defense & Security, Raises Price Target to $44

JP Morgan Maintains Neutral on Kratos Defense & Security, Raises Price Target to $44

RBC Capital Maintains Outperform on Kratos Defense & Security, Raises Price Target to $38

Benchmark Maintains Buy on Kratos Defense & Security, Raises Price Target to $40

Truist Securities Maintains Buy on Kratos Defense & Security, Raises Price Target to $38

Company: Aduro Clean Technologies

Quote: $ADUR

BT: $2.50-$3.00 At the current trajectory, Aduro will likely run out of cash by year-end. That means one thing: a dilutive share offering is coming. For traders watching this name, we’d prefer to wait until after that flush when the hype fades and reality sets in for a lower-risk entry.

ST: $10 (bull case safe side), $3 IF the market turns sour

Sharks Opinion:

Let’s call it like it is: this is not a name we’ve tracked until recently, but after a quick dive, it checks a few classic cleantech boxes both the good and the ugly.

$60K in quarterly revenue

+250% since IPO

Promising tech, zero product-market fit (yet)

Sound familiar? We’ve seen this movie before with LICY, FREY, RUN—cleantech names with big ideas, bloated valuations, and underwhelming execution. Most got crushed once the market shifted from “vision” to “cash flow.”

But here’s the catch...

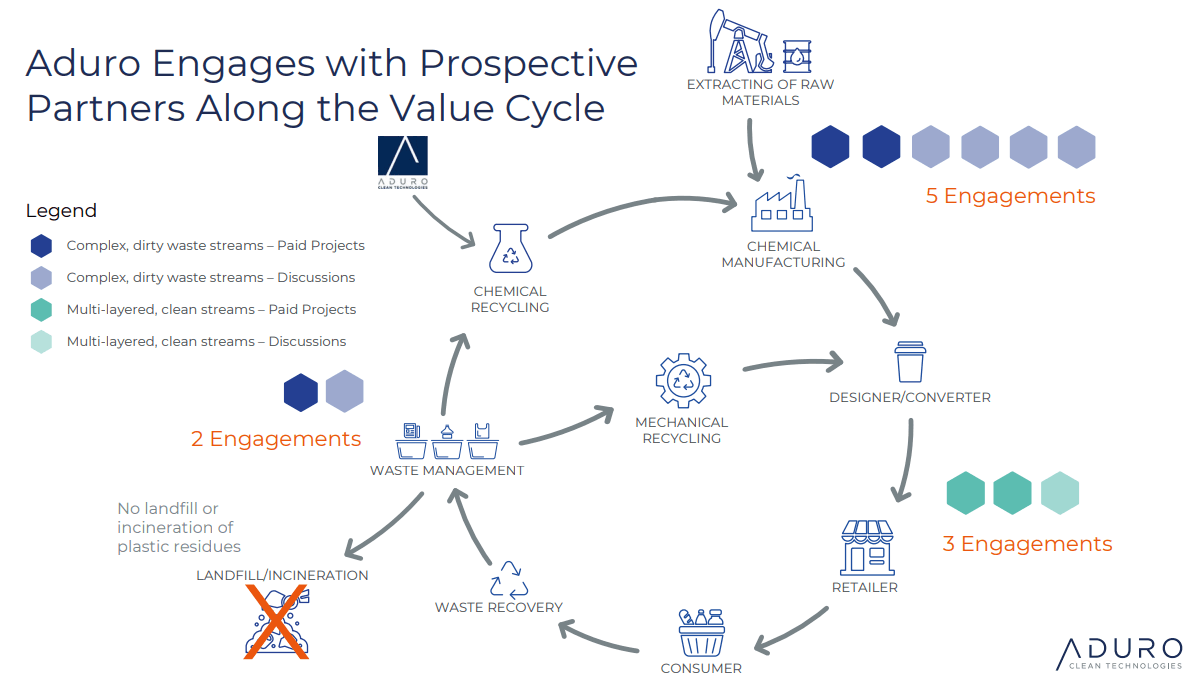

Aduro owns proprietary Hydrochemolytic™ Technology (HCT)—a method that could radically disrupt:

Advanced chemical recycling

Partial upgrading of heavy crude

Renewable fuel generation

That’s not just greenwashing. These are multi-billion dollar verticals, and unlike most tech startups, Aduro is already public, giving retail investors exposure before institutional capital dominates the cap table.

The Setup:

Short-Term? Extremely risky. Low float. Low liquidity. Any share offering will crush the price.

Mid-to-Long Term? Worth keeping on radar. If they survive dilution and deliver a real commercial partner or licensing deal, the stock could re-rate quickly.

Description: Aduro Clean Technologies Inc. develops water-based chemical recycling technologies. The company's platform converts end-of-life plastics and tire rubber to specialty chemicals and fuels; upgrades heavy crude oils; and transforms renewable oils into renewable fuels and specialty chemicals. Its water based chemical recycling platform features applications in hydrochemolytic plastics upcycling, hydrochemolytic renewables upgrading, and hydrochemolytic bitumen upgrading sectors.

Aduro’s HCT: The Cleantech Shortcut Industry Has Been Waiting For?

The Technology Pitch:

Forget pyrolysis Aduro’s Hydrochemolytic™ Technology (HCT) claims to do more with less.

Instead of relying on massive furnaces and clean, pre-sorted plastics, HCT uses superheated, pressurized water to break down complex chemical structures in plastic waste and heavy hydrocarbons. Think of it as a low-energy chemical pressure cooker that promises better margins and fewer headaches.

Why It Matters:

Let’s break it down by what really counts scalability, cost, and versatility:

✅ Feedstock Flexibility:

Unlike traditional pyrolysis that needs clean, uniform plastics, HCT doesn’t care if the plastic’s dirty, mixed, or low-grade. That’s a major logistical win.

✅ No External Hydrogen Needed:

Most recycling processes require costly hydrogen inputs. HCT makes its own from water, cutting costs and simplifying operations.

✅ Yield Efficiency:

Aduro claims 90–95% of the output is saleable product, compared to the 60–70% industry norm. That’s a massive jump in efficiency—exactly the kind of margin uplift industrial buyers want to see.

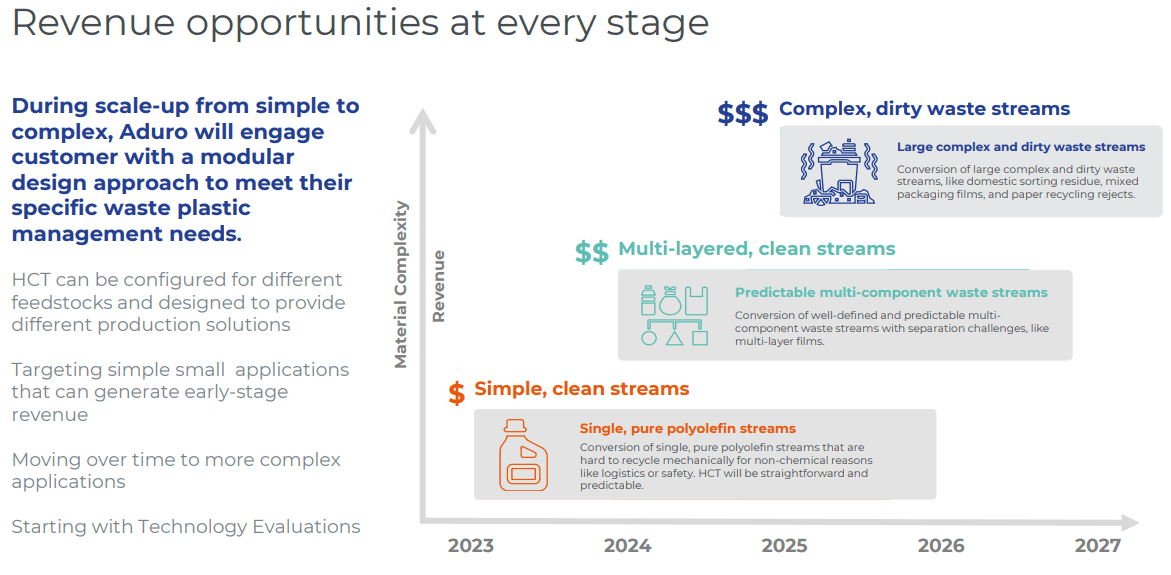

If HCT works as advertised at commercial scale, this tech could change the math for:

Advanced plastic recycling

Heavy oil upgrading

Renewable fuel production

This is not just a green story it’s about profit-per-ton economics. Aduro’s pitch is simple: do more with dirtier inputs, and generate higher-value outputs with fewer energy costs.

The Bottom Line:

Aduro’s tech hits all the right notes on paper: better margins, broader inputs, cheaper processing. But the million-dollar question (literally)? Can they scale?

If they pull it off, this isn’t just a green startup—it’s a potential acquisition target for the industrial giants scrambling to clean up their ESG and cost structures at the same time.

We're still not buyers yet, but now we know why this name deserves a spot on the watchlist.

Between advanced recycling, heavy oil upgrading, and renewable fuels, Aduro’s total addressable market crosses the $200 billion mark.

This isn’t some back-of-the-napkin number either governments are writing checks and corporations are rewriting supply chains to chase lower emissions and cleaner processes. Europe’s €100 billion cleantech initiative is just the tip of the spear. Recycled content mandates, carbon reduction targets, ESG investment flows it all adds up to one thing:

If Aduro’s tech works at scale, the tailwinds are already blowing.

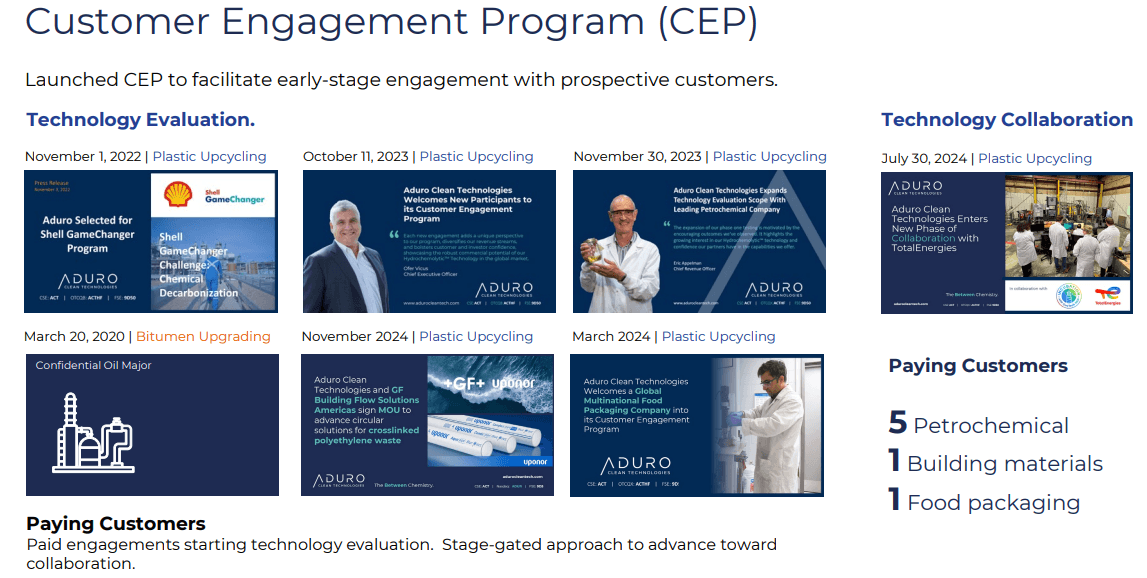

Early Validation:

✅ Shell GameChanger Program

Aduro’s inclusion is no small feat. This is where Shell vets disruptive energy technologies. Getting in means technical credibility.

✅ Customer Engagement Program (CEP)

Aduro isn’t pitching PowerPoints—they’re getting paid to test HCT with real feedstock from players like TotalEnergies. These aren’t looky-loos—they’re industry heavyweights paying upfront for proof-of-concept.

Why This Matters for Investors:

⏳ This isn’t a “wait-and-hope” cleantech play.

CEP brings in early revenue, builds relationships, and lowers burn—critical for a small-cap startup.

🚧 Real-world testing > theoretical results.

Aduro is actively proving the tech in field conditions, not just showing lab slides. That’s a key step toward unlocking pilot plant deals and industrial-scale rollouts.

💰 Once demonstration plants go live, all bets are off.

That’s the inflection point where institutional money and industrial buyers step in.

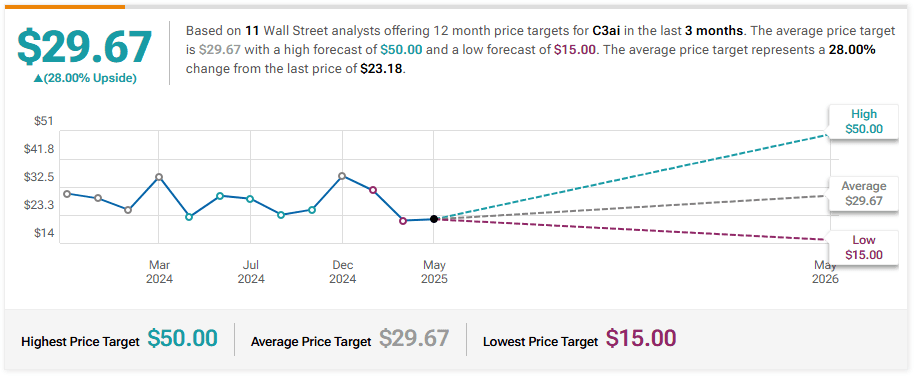

D. Boral Capital Maintains Buy on Aduro Clean Technologies, Lowers Price Target to $48

Company: Oscar Health, Inc.

Quote: $OSCR

Sharks Opinion:

Retail investors are circling Oscar Health like it’s the next HIMS—but let’s be clear: this is a very different animal.

🧴 HIMS sells health products direct to consumers.📄 Oscar sells health insurance. That’s a whole different set of margins, metrics, and risks.

Big Revenue, No Profits: Something Doesn’t Add Up

Oscar pulled in $9 billion in revenue last year. That’s not small-time. But despite the top line, profitability remains elusive.

That’s odd when you remember:

Insurance is usually a high-margin game.

U.S. regulations are looser than in most other countries.

Major players in the space are turning profits consistently.

So the question becomes: What’s broken in Oscar’s model?

Is it scale? Is it underwriting discipline? Is it tech bloat? That’s what smart investors should be digging into.

IPO to All-Time Lows… and Back Again

📉 IPO in March 2021 at $36 → Valued at $8B

📉 Crash to $2.05 in Dec 2022 → Market cap of $460M📈 Now trading near $18 → Market cap back up to $4.5B

That’s a 600%+ move off the bottom, but still less than half the IPO price.

Momentum traders see the trend. Value investors still see risk.

BT: Wouldn’t be a stock we buy but if we had to would be below $10

ST: N/A impossible to get a valuation on this name

Description: Oscar Health, Inc. operates as a healthcare technology company in the United States. The company offers health plans to individuals, families, employees, and small group markets. It also provides +Oscar platform that power others throughout the healthcare system; Campaign Builder platform, an engagement and recommendation platform for providers and payors; and reinsurance products.

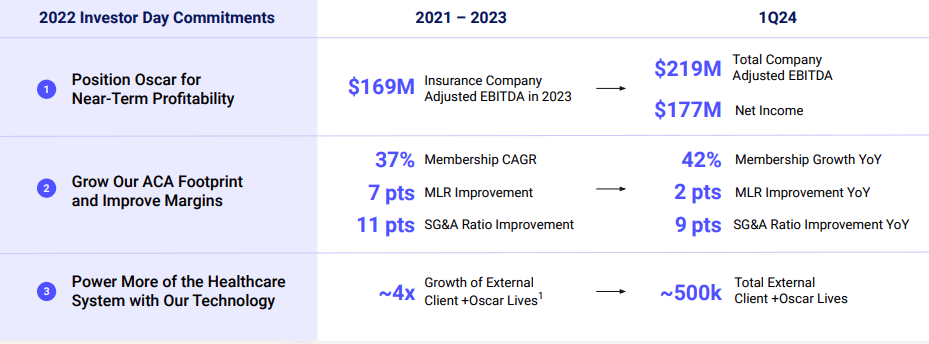

Oscar Health has largely relied on a single revenue stream—payments from the Affordable Care Act (ACA) program, predominantly from the federal government through the Centers for Medicare & Medicaid Services (CMS). The company ventured briefly into the reinsurance market but is wisely retreating from that complex and uncertain terrain.

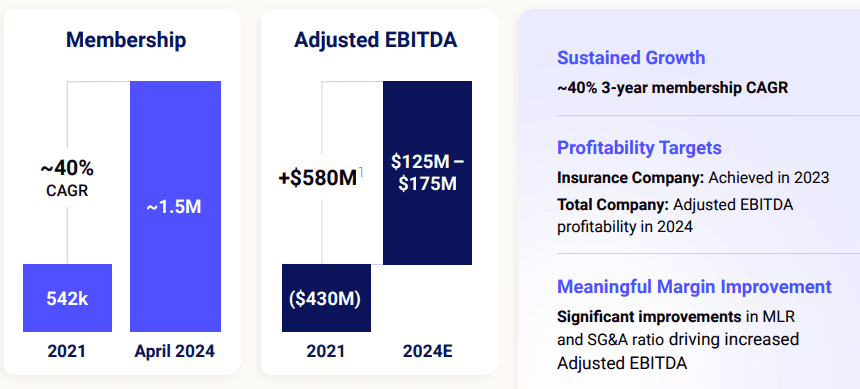

Following the 2025 open enrollment period, Oscar has emerged as one of the largest carriers of ACA plans. The individual market grew by 13% year-over-year, reaching a record 24 million individuals. Oscar’s growth, up 37%, outpaced the market by nearly three times. As of February 1, 2025, the company is serving 1.8 million members.

For the year ending December 31, 2024, Oscar reported:

Total Revenue of $9.2 billion, a robust 56.5% increase year-over-year

A Medical Loss Ratio of 81.7%, a slight increase of 10 basis points year-over-year

SG&A Expense Ratio of 19.1%, reflecting a 520 basis point improvement

Net income attributable to Oscar of $25.4 million, or $0.10 per diluted share, a $296.2 million improvement year-over-year

Adjusted EBITDA of $199.2 million, a marked improvement of $244.5 million year-over-year

The company’s adjusted EBITDA for 2024 was $199.2 million, up by $244.5 million from the prior year, while net income attributable to Oscar came in at $25.4 million, reflecting a $296.2 million year-over-year gain.

Oscar has now provided its outlook for 2025, introducing a new metric

Earnings from Operations. For 2025, the company projects:

Total Revenue of $11.2 billion to $11.3 billion

A Medical Loss Ratio of 80.7% to 81.7%

SG&A Expense Ratio of 17.6% to 18.1%

Earnings from Operations of $225 million to $275 million

Additionally, Oscar is welcoming healthcare veteran Janet Liang to the newly created role of President, Oscar Health Insurance, effective February 24, 2025. Liang, who previously served as Group President and COO at Kaiser Foundation Health Plan, will oversee all insurance functions, bringing operational expertise and a track record of growing markets to the role.

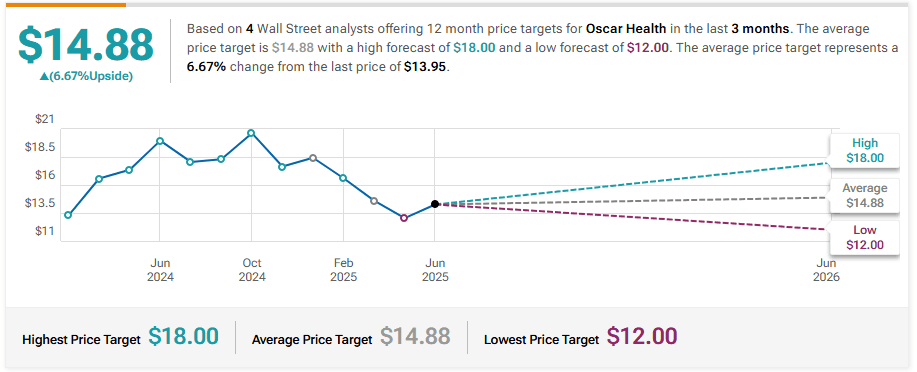

Piper Sandler Maintains Overweight on Oscar Health, Lowers Price Target to $18

Wells Fargo Downgrades Oscar Health to Equal-Weight, Lowers Price Target to $16

Jefferies Initiates Coverage On Oscar Health with Underperform Rating, Announces Price Target of $12

B of A Securities Downgrades Oscar Health to Underperform, Lowers Price Target to $13.5

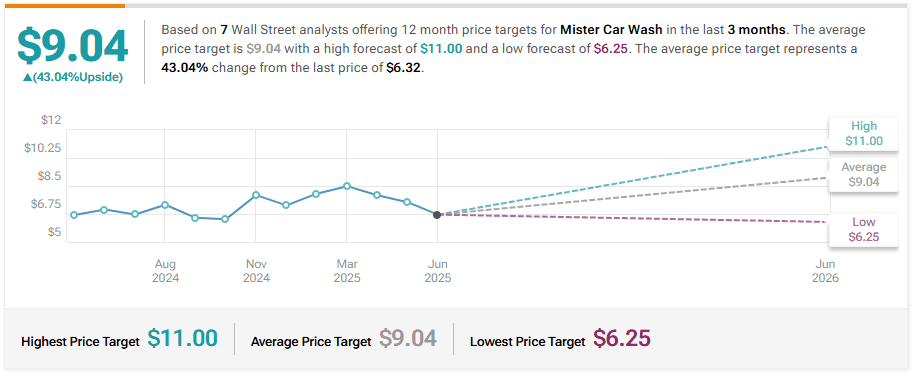

Company: Mister Car Wash, Inc

Quote: $MCW

BT: $4

ST: $8

Sharks Opinion:

Back in 2021, we were genuinely excited about Mister Car Wash. A clean, recurring-revenue business model, strong margins, and real estate backing—it looked like a perfect SPAC-era growth story.

But now? It feels like the company’s put the sponge down.

Where’s the Hustle?

Let’s start with the optics:

📉 No more earnings slides

📉 No narrative, no momentum, no vision

That’s never a good sign especially for a company trying to attract investor attention in a competitive market.

The Bigger Problem: Car Washes Aren’t a Speculative Play

Growth is flat.

Margins are thin.

CapEx requirements are heavy.

Consumer demand is discretionary.

In today’s market, speculative capital is chasing AI, biotech, and defense—not soap and suds.

Real Estate Angle? Not Enough

Yes, MCW owns a decent chunk of real estate. But here’s the issue:

📍 Real estate value ≠ stock price upside

📍 Investors are discounting those assets because they’re locked inside a low-margin business model.

You’re not buying REIT-like appreciation. You’re buying an underperforming operating business with some real estate, and that’s a very different investment case.

The car wash trade made sense in a zero-rate, story-driven market. But in today’s environment—where capital is scarce and narratives matter more than ever—MCW offers neither alpha nor upside.

Until the balance sheet changes or management wakes up, we’d stay far away from this one.

Description: Mister Car Wash, Inc., together with its subsidiaries, provides conveyorized car wash services in the United States. It offers express exterior and interior cleaning services. The company serves individual retail and corporate customers.

UBS Maintains Neutral on Mister Car Wash, Lowers Price Target to $8.25

Stephens & Co. Maintains Equal-Weight on Mister Car Wash, Lowers Price Target to $8.5

Raymond James Initiates Coverage On Mister Car Wash with Outperform Rating, Announces Price Target of $10

Morgan Stanley Maintains Equal-Weight on Mister Car Wash, Raises Price Target to $9

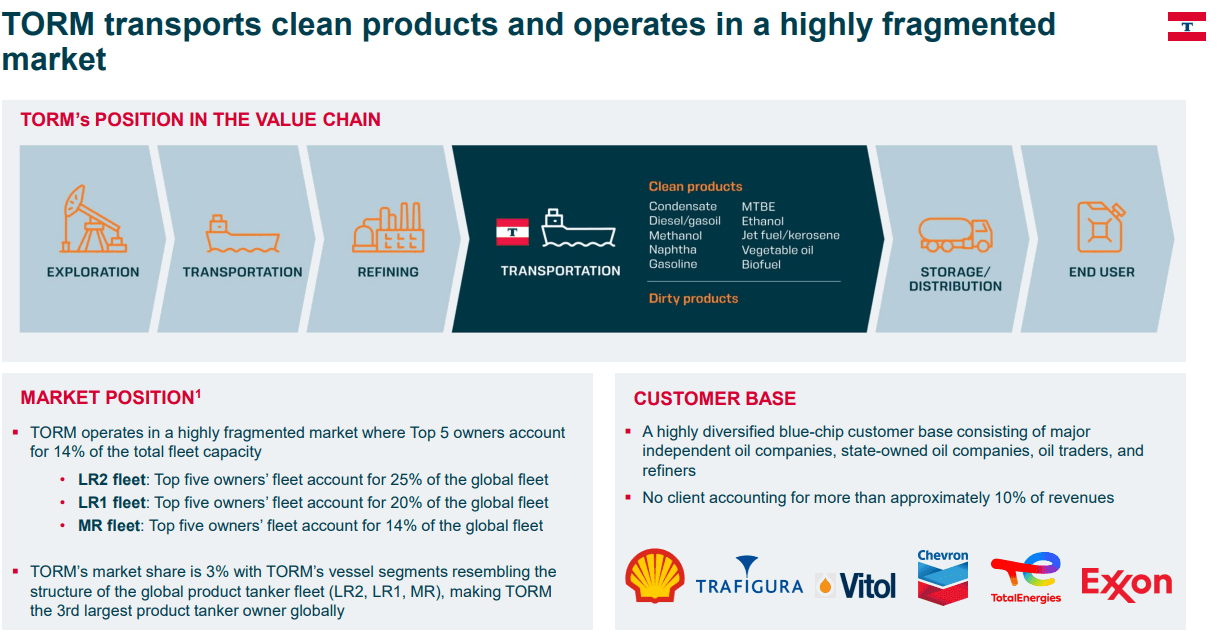

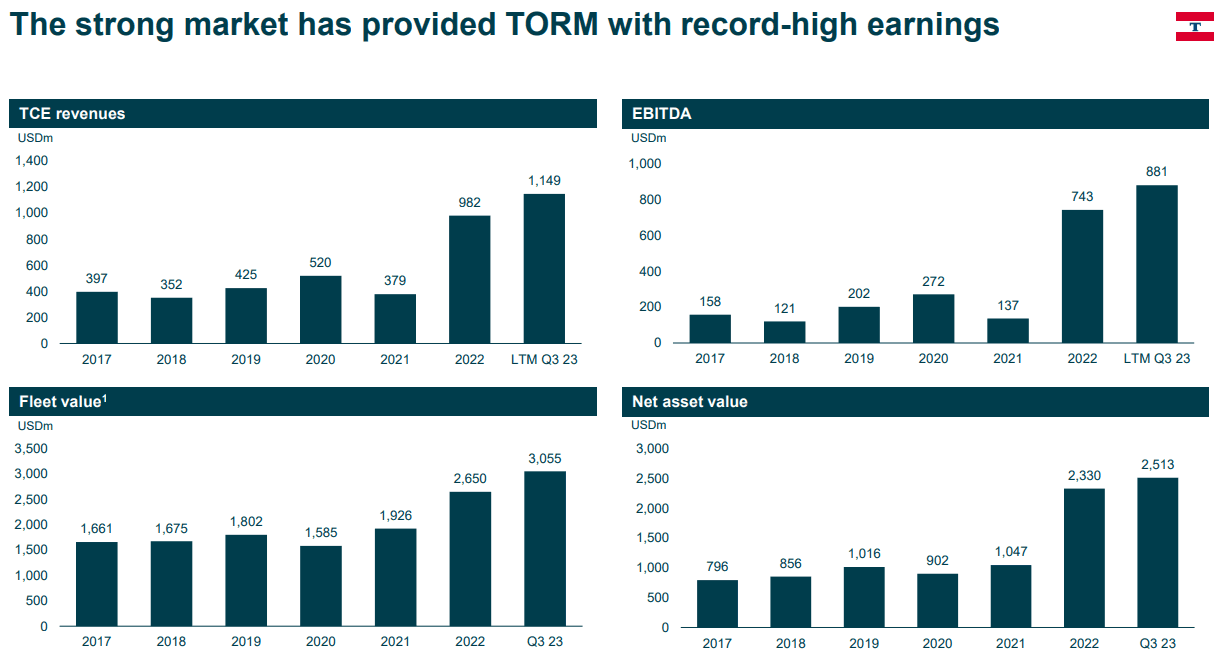

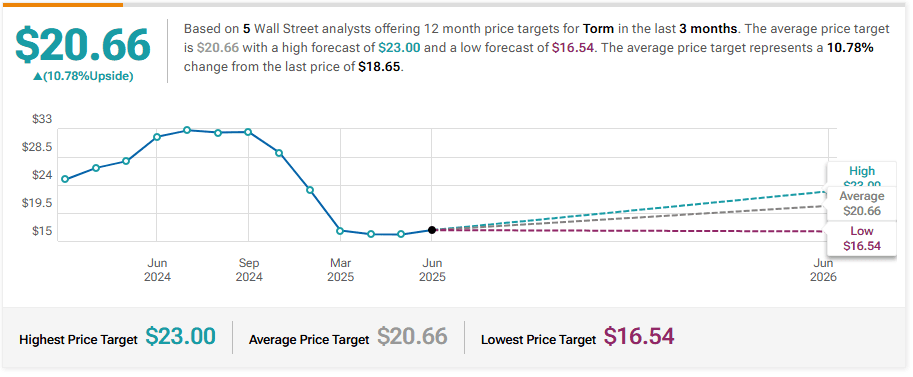

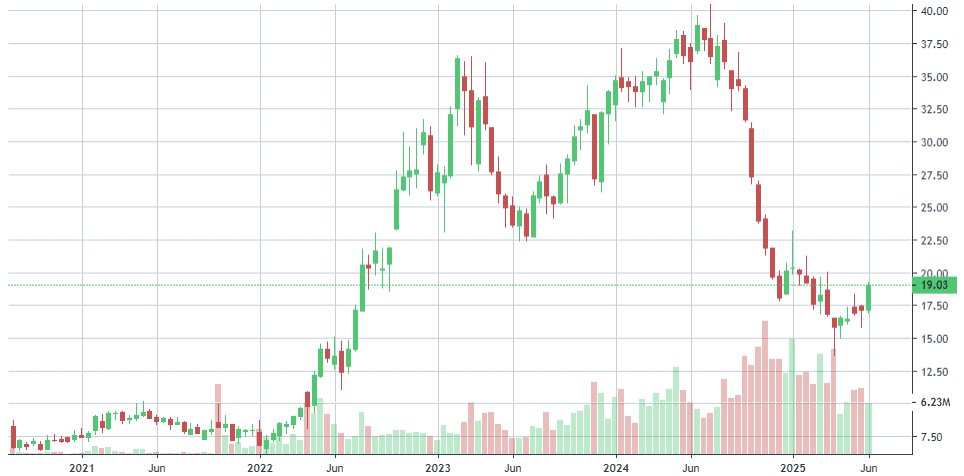

Company: TORM plc

Quote: $TRMD

BT: $20

ST: $28 (swing in the moment)

Sharks Opinion:

Torm plc (TRMD) looks like a value investor's dream at first glance. The company has a market cap just over $2 billion, pulls in more than $700 million in net revenue, trades at a price-to-earnings ratio of just 2.8, and pays out a jaw-dropping 20%+ dividend yield. On paper, the setup almost seems too good to be true. And maybe that's why it hasn't caught fire in the broader market—investors have been conditioned to assume something must be wrong.

But here's where it gets interesting: the "problem" with TRMD isn't specific to Torm. It's a reflection of the broader shipping cycle. TRMD operates in the refined product tanker space, transporting clean fuels like jet fuel and diesel rather than crude oil. These types of tankers live and die by spot rates, which can swing drastically based on global demand, geopolitical tensions, and shipping lane disruptions. When rates drop, profitability disappears quickly, and dividends often get slashed to zero. That fear is what’s likely being priced in here.

Over the past year, shipping rates tracked via the Baltic Clean Tanker Index saw a steep decline from August through November. This drawdown correlated closely with TRMD’s falling stock price, which then extended into December as tax-loss harvesting accelerated the selloff. The market's logic here is simple: lower spot rates mean lower earnings, and in a worst-case scenario, no dividend at all. In this kind of environment, even a company with strong fundamentals can look unattractive.

That said, we believe this logic is beginning to break down—and that’s exactly what makes TRMD an interesting setup. Tanker rates have started to rebound, particularly in light of growing geopolitical risk out of the Middle East, which could disrupt shipping lanes and tighten capacity across global routes. Add in increasing demand for refined fuels as air travel ramps back up and inventories stay tight, and you suddenly have the early signs of another upcycle. TRMD’s stock may be beaten down, but the underlying dynamics that once supported the rally are beginning to stir again.

To be clear, this isn’t a long-term dividend growth play. Shipping stocks are notoriously cyclical, and TRMD is no exception. If the current tailwinds reverse, profits will shrink and the dividend will go with it. But that’s not the angle we’re taking. This is a short-to-mid-term swing trade rooted in macro trends and capital flows. If shipping rates continue their rebound, this stock has room to run and traders who can stomach the volatility may find themselves rewarded handsomely.

In our view, it’s better to buy strength than hope for a bounce in weakness. TRMD looks like a textbook example of a stock bottoming with improving fundamentals just beneath the surface. The tanker trade might not be sexy, but it’s starting to look like one of the more asymmetric opportunities in the market right now.

Description: TORM plc, a shipping company, owns and operates a fleet of product tankers in the United Kingdom. It operates in two segments, Tanker and Marine Engineering. The Tanker segment transports refined oil products, such as gasoline, jet fuel, kerosene, naphtha, and gas oil, as well as dirty petroleum products, including fuel oil. The Marine Engineering segment engages in developing and producing advanced and green marine equipment. TORM plc was founded in 1889 and is based in London, the United Kingdom.

TORM's first-quarter 2025 results offer a clear snapshot of a company that’s still profitable, but no longer surfing the same wave of sky-high tanker rates it enjoyed just a year ago. Time charter equivalent (TCE) earnings came in at $214 million, down sharply from $330.7 million in Q1 of 2024. Adjusted EBITDA followed suit, dropping to $137.7 million from last year’s $267.2 million, while net profit landed at $62.9 million — a steep decline compared to $209.2 million a year earlier. That said, Q1 earnings were broadly in line with what the company posted in Q4 of 2024, suggesting we may be finding a floor in this part of the cycle.

The year-over-year drop is all about freight rates. TORM’s average TCE across its fleet was $26,807 per day, compared to a much higher $43,152 last year. While the headline numbers might seem bleak, they're important context: the fourth quarter had already seen a moderation in rates, and the fact that Q1 held steady shows resilience in a softer environment. Vessel utilization was still strong, with earning days rising to 8,061 from 7,697 the year before. Among vessel types, LR2s led the way with TCEs of $33,806, while LR1s and MRs came in at $24,947 and $24,675 respectively.

The freight environment, however, is dynamic and fraught with geopolitical risk. Much of the recent strength in tanker rates was driven by longer trade routes around the Cape of Good Hope due to Red Sea tensions. A potential reopening of the Red Sea would likely restore shorter routes between the Middle East and Europe, easing current bottlenecks and removing the need for clean petroleum products (CPP) to be carried by crude tankers over longer distances. At the same time, any easing of sanctions on Russia could lead to a return of sanctioned tonnage to the mainstream market and compress rates further. On the flip side, scrapping of older, underinsured, or poorly maintained vessels could provide a floor for supply and help balance the market.

For now, the trend is clearly softer return on invested capital dropped to 10.3%, down from 33.8% a year ago. Basic earnings per share came in at $0.64, off the prior year’s $2.34. While that drop might seem dramatic, it’s important to remember that last year was an outlier. The company is still generating healthy profits, maintaining a very reasonable payout, and is fundamentally in a much better position than many of its peers.

We view this as a cyclical reset, not a structural breakdown. If you're looking for a durable long-term play in the tanker space, TORM may not be as flashy at these freight levels, but its balance sheet is intact, the dividend is still flowing, and the downside appears fairly limited. If geopolitical volatility re-emerges — especially in the Middle East — don’t be surprised if rates snap back hard and TORM surges with them.

Evercore ISI Group Maintains Outperform on TORM, Lowers Price Target to $23

Jefferies Maintains Buy on TORM, Lowers Price Target to $32

Evercore ISI Group Maintains Outperform on TORM, Raises Price Target to $48

Have a question?

We’re just one click away. Let’s dive into your investment journey.