Q1 Trade Recap & Q2 Strategy Outlook We closed out Q1 with strong trading performance across the board, with the majority of our alerts and trade ideas landing in the green. Our strategy this year has leaned heavily into swing trading around key catalyst events, and that approach has served us well given the macroeconomic backdrop.

We continue to tread cautiously and deliberately as markets remain in a fragile and uncertain state. Key overhangs include:

Unresolved tariff tensions

Stubborn inflation, which could force the Fed to delay or reduce the scale of expected rate cuts

Growing fiscal concerns, reignited by the updated spending bill that has injected fresh volatility into both bond and equity markets

In short, while we’re seeing pockets of strength and opportunity, the broader environment lacks the clarity and momentum needed for sustained long exposure. This makes catalyst-based swing trading our preferred playbook for now.

Recent Trades: Strong Wins on XMTR & FUTU We executed successful trades in both Xometry (XMTR) and Futu Holdings (FUTU), each generating returns north of 25%. These setups were driven by clear event catalysts and disciplined risk management — exactly the kind of trades we’re prioritizing in this market.

New Earnings Swing Setup: $NCNO We’ve initiated a position in nCino ($NCNO) heading into its upcoming earnings report this week. The setup aligns with our framework: limited downside, asymmetric upside potential, and a clear fundamental or earnings-related catalyst on the horizon.

🔔 New Alert: $NCNO — swing setup into earnings 📊 All active trade ideas and setups can be found via the Watching Watchlist Overview at the link below.

These are stocks we have been long for some time and the current BT doesn’t represent other entry prices, The BT is updated weekly for new subscribers to jump in and know when to get out.

These stocks tend to have 6 Month-2 years holding period and is suggested for larger capital Allocations in your portfolio.

Please read the Overviews for full research and instructions on how to trade each name individually

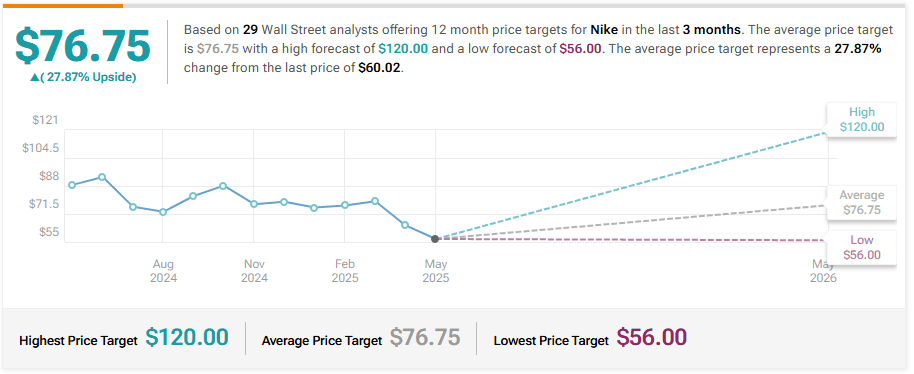

Company: NIKE, Inc.

Quote: $NKE

BT: $58.20

ST: $78

$110 (long term)

Sharks Opinion:

Nike has climbed roughly 9% since our entry, albeit on a slow grind higher. While the pace of the rebound has been underwhelming, our thesis remains intact heading into the upcoming earnings report, which we expect to be solid and potentially act as a catalyst for a re-rating.

That said, missing the Foot Locker + Dick’s Sporting Goods combo trade stings a bit. Foot Locker was just acquired at a 90% premium, which would have paired perfectly with the Nike position as a complementary retail rebound play. Sometimes that’s how it goes—we move on.

Valuation Still Compressed: Opportunity Remains Nike currently trades at a forward P/E of ~18–19x, far below its historical 5- to 10-year average of ~30x and nearing decade-low valuation levels. This kind of compression reflects a heavy dose of market pessimism, but it also sets the stage for upside if execution improves.

To put it in perspective:

Adidas, still mid-turnaround, trades at ~45x trailing earnings

On Holding (ONON), a premium challenger, trades at 50–55x

Deckers (HOKA) and Puma, more value-oriented names, trade at 15–17x

Nike’s brand strength, global scale, and margin profile remain superior. If earnings begin to stabilize, there’s a clear case for a multiple expansion back into the low- to mid-20s—creating room for significant upside from here.

Bottom Line While the missed Foot Locker trade was a rare oversight, Nike remains a high-conviction name with a favorable risk-reward profile. Valuation is washed out, sentiment is near lows, and the upcoming earnings event could finally provide the spark this stock needs to accelerate its recovery.

Description: NIKE, Inc., together with its subsidiaries, engages in the design, development, marketing, and sale of athletic footwear, apparel, equipment, accessories, and services worldwide. The company provides athletic and casual footwear, apparel, and accessories under the NIKE, Jumpman, Converse, Chuck Taylor, All Star, One Star, Star Chevron, and Jack Purcell trademarks. It also sells a line of performance equipment and accessories comprising bags, sport balls, socks, eyewear, timepieces, digital devices, bats, gloves, protective equipment, and other equipment for sports activities under the NIKE brand; and various plastic products to other manufacturers.

RBC Capital Maintains Sector Perform on Nike, Lowers Price Target to $65

Wells Fargo Maintains Equal-Weight on Nike, Raises Price Target to $60

Barclays Maintains Equal-Weight on Nike, Lowers Price Target to $60

Telsey Advisory Group Maintains Market Perform on Nike, Lowers Price Target to $70

JP Morgan Maintains Neutral on Nike, Lowers Price Target to $56

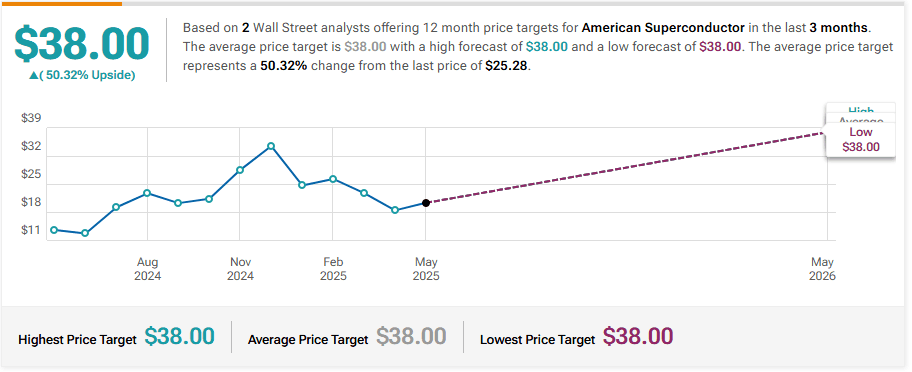

Company: American Superconductor

Quote: $AMSC

BT: $25.41

ST: $38 (short term)

Sharks Opinion:

AMSC posted a solid earnings print last week, and while the numbers weren’t extraordinary, the market reaction has been powerful—shares jumped 8% today, continuing a sharp rebound off the post-earnings dip.

We remain bullish on the name, but given AMSC’s volatile trading history, we’re beginning to prepare for profit-taking should this rally extend further. Locking in gains on strength is part of our playbook for names with this kind of risk profile.

Price Target Raised to $38 for 2025 The stock has now reclaimed its highest levels since early 2021, and we’re updating our 2025 price target to $38, based on:

Strong volume trends and technical momentum

Improving analyst sentiment

Supportive macro tailwinds in U.S. infrastructure, grid modernization, and clean tech

AMSC is increasingly being viewed as a pure-play beneficiary of the renewed push toward domestic energy resilience and next-gen transmission systems.

Still a Top Watch Into H2 We’re closely monitoring for signs of consolidation or overbought conditions, but at current levels, AMSC continues to rank among the more compelling U.S. energy-tech stories heading into the second half of 2025.

Execution risk remains, as always with small-cap tech, but the chart, narrative, and institutional interest are all aligned for now.

Description: American Superconductor Corporation, together with its subsidiaries, provides megawatt-scale power resiliency solutions worldwide. The company operates through Grid and Wind segments. The Grid segment offers products and services that enable electric utilities, industrial facilities, and renewable energy project developers to connect, transmit, and distribute power under the Gridtec Solutions brand. It provides transmission planning services, which identify power grid congestion, poor power quality, and other risks; grid interconnection solutions for wind farms and solar power plants, power quality systems, and transmission and distribution cable systems; D-VAR systems used for controlling power flow and voltage in the AC transmission system; actiVAR system, a fast-switching medium-voltage reactive compensation solution; armorVAR system installed for reactive compensation, power factor correction, loss reduction, utility bill savings, and mitigation of common power quality concerns related to power converter-based generation and load devices; and D-VAR volt var optimization (VVO) that serves the distribution power grid market.

Roth MKM analyst Justin Clare reiterated a Buy rating on American Superconductor today and set a price target of $38.00

Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Craig-Hallum Reiterates Buy on American Superconductor, Maintains $33 Price Target

Company: Schrödinger, Inc.

Quote: $SDGR

BT: $22.52

ST: $28

Sharks Opinion:

We’re officially downgrading Schrodinger ($SDGR) and looking to exit the position in the near term.

While our initial thesis on the company’s long-term potential remains intact, the stock has failed to gain meaningful traction, even in the face of positive catalysts.

Most notably, there's been a clear lack of follow-through volume—a red flag when trying to scale into the next leg higher.

Capital Rotation > Conviction Hold In this market, we’re prioritizing capital efficiency. SDGR has now stalled long enough that the opportunity cost is too high. We're choosing to redeploy funds into setups with stronger momentum or clearer catalysts on deck.

That said, we’re not abandoning the name entirely SDGR still has an interesting platform in computational drug discovery, and we’ll continue monitoring earnings and pipeline updates for a potential re-entry at lower levels.

Bottom Line Sometimes the timing just isn’t right. SDGR hasn’t worked for us yet, and we’re not forcing it. We're moving on for now—but keeping it on the radar.

Description: Schrödinger, Inc., together with its subsidiaries, develops physics-based computational platform that enables discovery of novel molecules for drug development and materials applications. The company operates in two segments, Software and Drug Discovery. The Software segment is focused on licensing its software to transform molecular discovery for life sciences and materials science industries. The Drug Discovery segment focuses on building a portfolio of preclinical and clinical programs, internally and through collaborations. The company serves biopharmaceutical and industrial companies, academic institutions, and government laboratories worldwide.

Keybanc Maintains Overweight on Schrodinger, Raises Price Target to $32

Piper Sandler Maintains Overweight on Schrodinger, Lowers Price Target to $45

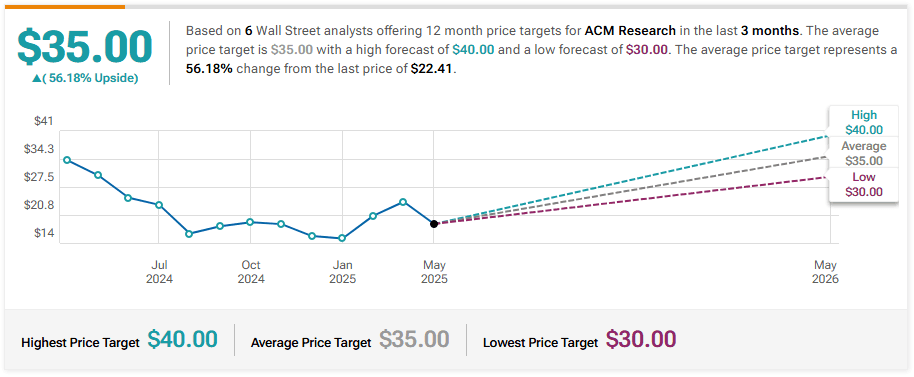

Company: ACM Research Inc

Quote: $ACMR

BT: $19.18

ST: $40

Sharks Opinion:

We’re pleased with our dip buy in ACMR a few weeks back—it’s already showing strength, and we continue to view it as a high-conviction long-term value play, especially if semiconductors regain momentum into the second half.

Valuation Gap Creates Strategic Asymmetry ACM Research stands out for one major reason: a stark valuation disconnect between its U.S. listing and its Chinese subsidiary.

ACM Research (Shanghai) — valued at ~$5.9B, trading at ~6x forward 2025 revenue

U.S.-listed parent (ACMR) — owns 82% of that entity, yet trades at just $1.54B market cap

This isn’t just a mispricing—it’s a legitimate arbitrage opportunity. With consolidated revenue on track to hit ~$1B this year, the underlying business fundamentals more than justify a re-rating, even under conservative assumptions.

What We’re Watching We’ll continue to monitor the China–U.S. regulatory backdrop, but the core thesis remains: ACMR gives exposure to one of the fastest-growing precision cleaning and process tool suppliers in China at a deep discount—and that valuation gap won’t stay open forever.

ACM Research, Inc., together with its subsidiaries, develops, manufactures, and sells single-wafer wet cleaning equipment for enhancing the manufacturing process and yield for integrated chips worldwide. It offers space alternated phase shift technology for flat and patterned wafer surfaces, which employs alternating phases of megasonic waves to deliver megasonic energy in a uniform manner on a microscopic level; timely energized bubble oscillation technology for patterned wafer surfaces at advanced process nodes, which provides cleaning for 2D and 3D patterned wafers; Tahoe technology for delivering cleaning performance using less sulfuric acid and hydrogen peroxide; and electro-chemical plating technology for advanced metal plating. The company markets and sells its products under the SAPS, TEBO, ULTRA C, ULTRA Fn, Ultra ECP, Ultra ECP map, and Ultra ECP ap trademarks through direct sales force and third-party representatives. ACM Research, Inc. was incorporated in 1998 and is headquartered in Fremont, California

JP Morgan Initiates Coverage On ACM Research with Overweight Rating, Announces Price Target of $36

Craig-Hallum Downgrades ACM Research to Hold, Lowers Price Target to $18

Needham Downgrades ACM Research to Hold, Maintains Price Target to $25

Company: Pony AI

Quote: $PONY

BT: $18.14

ST: $28 (short term)

Sharks Opinion:

Pony.ai has been one of the most volatile trades we’ve ever taken. After an explosive 35% move out of the gate, the stock round-tripped hard sliding below $10 before mounting an equally aggressive rebound.

Fast forward to today: shares are now up over 300% from the lows, and the position is firmly back in the green. It's a textbook example of just how violently sentiment can swing in the autonomous vehicle space.

Uber Deal: A Catalyst, Not a Conviction Builder The recent Uber partnership is a legitimate catalyst and could provide another leg higher, but it doesn’t change our overall posture. This remains a momentum trade, not a long-term hold.

Game Plan The plan is simple: we'll begin trimming the moment this gets close to our sell target. The stock has delivered, but the volatility is too extreme to justify holding through future drawdowns.

Description: Pony AI Inc., through its subsidiaries, engages in the autonomous mobility in the People’s Republic of China and the United States. The company provides robotruck services, such as transportation services to the logistics platforms. It also offers robotaxi services, including a suite of AV engineering solutions comprising AV software deployment and maintenance, vehicle integration and engineering, and road testing; and fare-charging robotaxi services. In addition, the company offers personally-owned vehicle intelligent solutions, including intelligent driving software solutions, proprietary vehicle domain controller products, and data analytics tools; vehicle integration services, software development, and licensing services; and vehicle-to-everything (V2X) products and services to enhance road safety. The company was incorporated in 2016 and is based in Guangzhou, the People’s Republic of China.

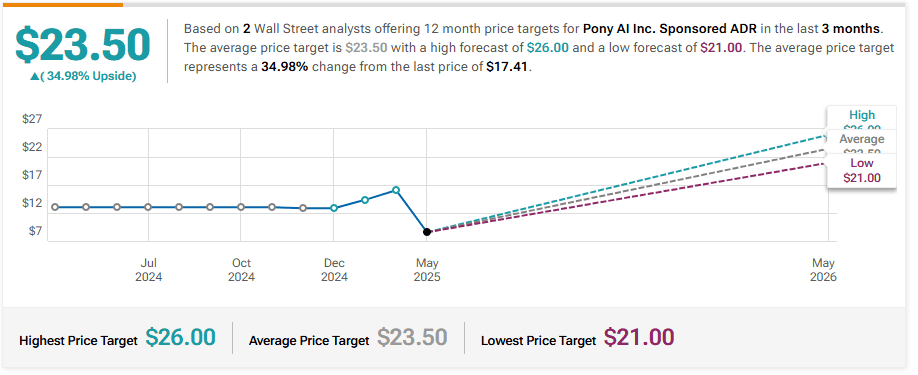

Deutsche Bank Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

B of A Securities Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $18

Goldman Sachs Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $19.6

Company: nCino, Inc

Quote: $NCNO

BT: $26.62

ST: $38

Sharks Opinion:

We’re re-initiating a position in nCino (NCNO) after this week’s earnings report triggered a clear surge in trading volume and drew multiple analyst upgrades. The stock is showing fresh momentum, and the setup closely resembles the same conditions we capitalized on during last year’s successful trade.

Why We Like It Here Volume confirms conviction — institutional interest appears to be stepping in.

Analyst sentiment is turning bullish, adding fuel to the move.

Historical analog — this mirrors the exact pattern we’ve seen lead to outsized gains before.

Trade Outlook We’re looking to ride this emerging trend with a swing timeframe in mind. If the pattern holds, NCNO could once again deliver a high-conviction win.

Description: nCino, Inc., a software-as-a-service company, provides cloud-based software applications to financial institutions in the United States and internationally. Its nCino Bank Operating System connects financial institution employees, clients and third parties on a single cloud-based platform which include client onboarding, deposit account opening, loan origination, end-to-end mortgage suite, and powerful ecosystem.

Morgan Stanley Maintains Equal-Weight on Ncino, Raises Price Target to $27

Needham Maintains Buy on Ncino, Raises Price Target to $33

Scotiabank Maintains Sector Perform on Ncino, Raises Price Target to $26

Company: BlackSky Technology

Quote: $BKSY

BT: $1.17

Sharks Opinion:

This stock had its chance earlier this year but since then has given back all its gains, Nothing we say at this point will change what it is.

ST: $18

Description: BlackSky Technology Inc. provides geospatial intelligence, imagery and related data analytic products and services, and mission systems that include the development, integration, and operations of satellite and ground systems to commercial and government customers worldwide. The company processes a range of observations from its constellation, as well as various space, internet-of-things, and terrestrial based sensors and data feeds. Its products are used in government defense and intelligence; commercial, construction, and industrial; and catastrophe, climate, and environment applications. The company was incorporated in 2014 and is headquartered in Herndon, Virginia.

Canaccord Genuity Initiates Coverage On BlackSky Technology with Buy Rating, Announces Price Target of $12

Benchmark Reiterates Buy on BlackSky Technology, Maintains $17 Price Target

HC Wainwright & Co. Reiterates Buy on BlackSky Technology, Maintains $20 Price Target

Oppenheimer Maintains Outperform on BlackSky Technology, Raises Price Target to $30

Company: Plurilock Security Inc

Quote: $PLUR (TSX.V), $PLCKF (OTC)

BT: $0.65

ST: $3-4

Sharks Opinion:

Our primary investment thesis for Plurilock hinges on two potential catalysts: a U.S. uplisting and its recently announced strategic partnership with cybersecurity heavyweight CrowdStrike.

A potential uplisting to the Nasdaq would significantly broaden Plurilock’s investor base and increase daily liquidity—benefits the company has not fully realized trading solely on the Canadian exchange. Encouragingly, the company took concrete steps toward this goal in its latest earnings update:

"In its efforts to explore a possible listing or other corporate activities in the U.S., the Company installed new auditors, MNP, to streamline the process of doing an audit under both Canadian (AASB) and U.S. standards (PCAOB)."

The second major development is Plurilock’s partnership with CrowdStrike, which not only strengthens its credibility in the cybersecurity ecosystem but also increases its visibility as a potential acquisition target. In a market where strategic consolidation is accelerating, Plurilock’s positioning becomes more compelling.

Looking ahead, the company expects growing demand for its cybersecurity solutions, driven by the escalating global threat landscape. With improving gross margins and a stated intent to pursue mergers and acquisitions over the next 12 to 24 months, Plurilock may be entering a phase of operational and strategic acceleration—one that, if accompanied by stronger investor recognition, could begin to unlock long-awaited shareholder value.

Description: Plurilock Security Inc. operates an identity-centric cybersecurity company in the United States, India, and Canada. The company operates in two divisions, Technology and Solutions. It offers Plurilock DEFEND, Plurilock DEFEND, an enterprise continuous authentication platform that confirms user identity or alerts security teams to detected compromises in real time; Plurilock AI DLP that helps in data loss prevention and cloud security; and Plurilock AI Cloud that provides access management, email data security, and compliance for cloud environments.

Have a question?

We’re just one click away. Let’s dive into your investment journey.