After months of drought, the U.S. IPO market just caught fire and investors are finally taking notice.

Some of 2025’s most hyped names Circle, eToro, CoreWeave have exploded out of the gate, delivering strong aftermarket gains and reigniting confidence across the board.

Circle’s IPO in particular has been a standout, with one top analyst calling it “the return of the retail IPO frenzy.”

Here’s what the numbers say:

$25.36 billion raised YTD (as of June 11) that’s up 39% from 2024 and more than 2.5x higher than this time in 2023

IPO stocks were under pressure earlier this year, weighed down by trade volatility and macro noise but that’s shifting fast. The Renaissance IPO Index a proxy for post-IPO performance has clawed its way back and is now tracking nearly in line with the S&P 500.

That’s a clear signal.

Momentum is back, and with a loaded pipeline names like Klarna, Gemini, Cerebras this could be the start of a broader IPO cycle.

Especially in sectors like fintech, AI, and crypto infrastructure, where valuations are starting to justify public listings again.

For traders and early-growth investors, this is a window we haven’t seen in years: a reopening IPO market with high-demand names and a market finally ready to absorb them.

Be selective. But be ready.

Because when IPO windows open, they don’t stay that way for long.

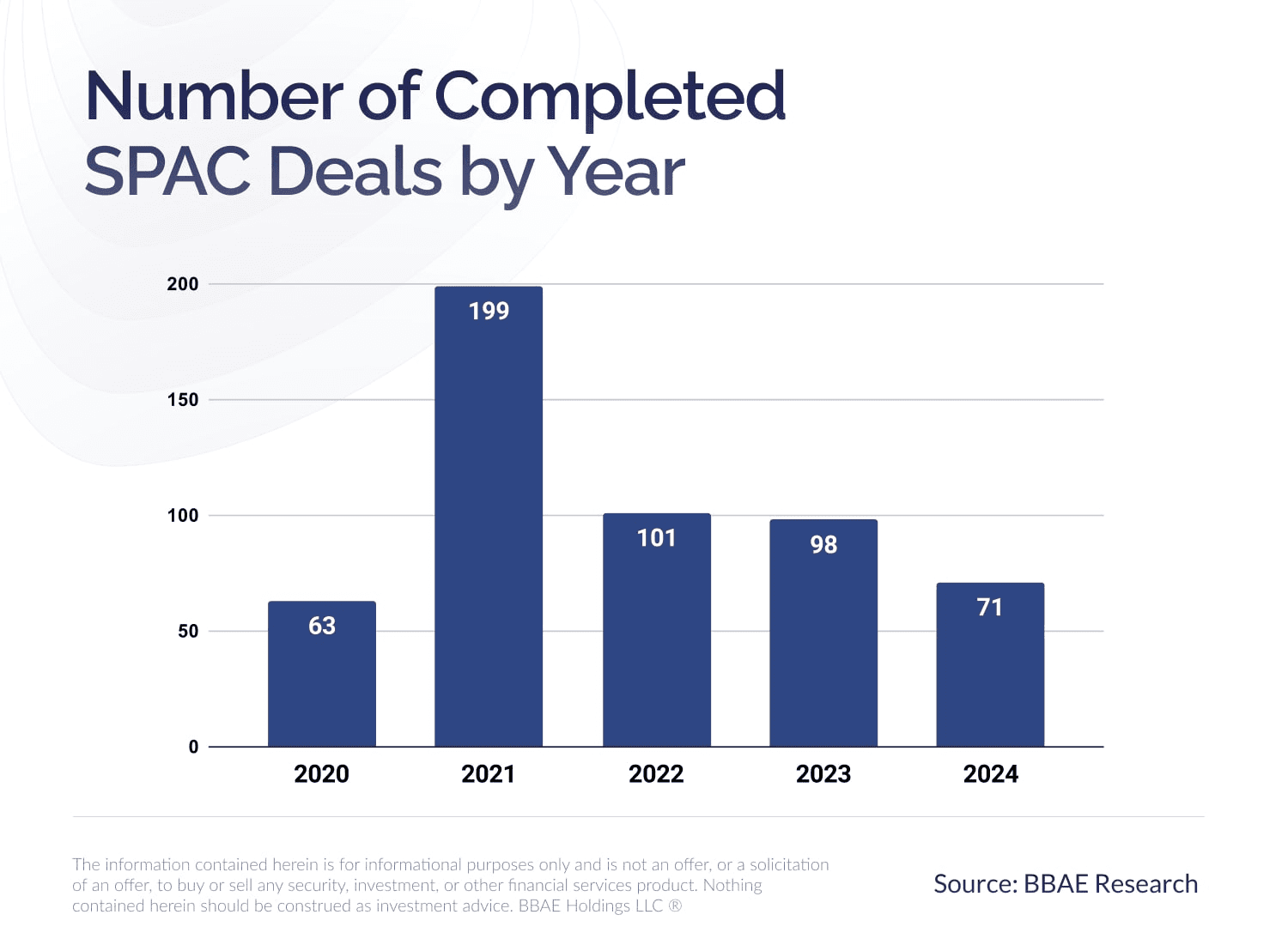

Remember when every startup and their cousin went public via SPAC?

That was 2021 peak bull market, peak hype.

From electric scooters to space tourism, it felt like any company with a pitch deck could hit the NASDAQ overnight.

But reality hit hard.

Most of those “next big thing” stories unraveled. Revenue missed. Promises evaporated. Retail investors got torched. SPACs became a dirty word.

Fast forward to 2025, and something unexpected is happening: SPACs are making a quiet comeback but this time, the tone is different.

Goldman Sachs, which swore off SPAC underwriting in 2022, is now back in the game, signaling that the space is maturing. The tourists have cleared out. What’s left are seasoned players SPAC sponsors with actual operating chops and reputations to protect.

What to watch:

Quality of sponsors: Are they operators or hype merchants?

Deal terms: Is there real alignment between backers and shareholders?

Post-merger execution: Can the company actually perform in public markets?

The SPAC vehicle itself was never the problem was the garbage shoved inside it.

Now, with markets stabilizing and investors more disciplined, SPACs might quietly return as a legit path to liquidity especially for companies in sectors like AI, defense tech, and digital infrastructure that don’t fit the traditional IPO mold.

Bottom line?

SPACs aren’t dead.

They’ve just grown up. And that might make them worth a second look if you know what you’re looking at.

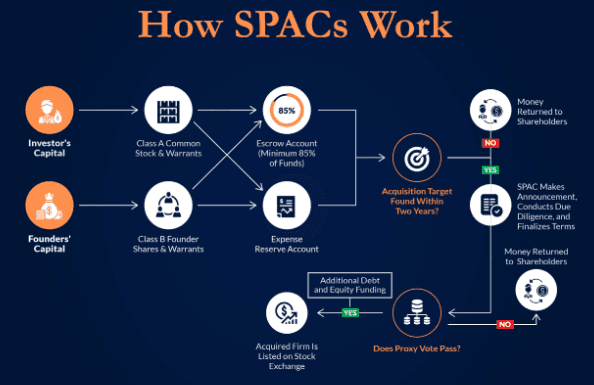

At the core, a (SPAC) Special Purpose Acquisition Company is just a blank-check shell that raises money from investors with one mission: buy a private company and take it public.

Here’s how it plays out:

Investors buy in at $10 a share. That’s the standard price. These early backers are basically betting the SPAC team can land a solid deal within a set time frame usually 18 to 24 months.

The SPAC sponsors (aka the dealmakers)? They toss in a nominal amount typically $25,000 but get a sweet deal: “founder shares” equal to 20% of the total equity post-merger.

That’s the real incentive here. If they close a deal, they win big.

While the search is on, the capital raised sits in a secure, interest-bearing trust account investors are protected if the deal doesn’t happen.

If a company is successfully acquired, the SPAC is “De-SPAC’d” and voilà, a brand-new public company hits the market, often overnight.

But here’s the catch:

If the SPAC fails to close a deal before time runs out, the trust dissolves, and investors get their cash back. The sponsors? They walk away with nothing.

Why it matters:

Understanding this structure is key. The incentives are built to favor speed and a successful close, but that doesn't always mean quality deals. That’s why so many SPACs in the last cycle crashed and burned post-merger bad businesses got rushed to market. We've learned to watch the sponsors, not just the story. Who’s running the show? What’s their track record? Because in the SPAC game, alignment matters and so does timing.

The IPO window is open again and we’ve got our eyes on nine companies we believe will go public before this cycle is over.

Whether it’s a traditional IPO, a direct listing, or even a SPAC merger, these names are on our radar for a reason.

Some of them you’ll recognize from past Stock Sharks writeups.

Others are new additions-growth plays or category disruptors that have quietly built serious momentum behind the scenes.

This list isn’t just about what’s trending. It’s about being prepared. When these names finally hit the market, you’ll already know the story, the fundamentals, and the upside case.

This is how smart money operates: anticipate the move, not react to it.

Stay tuned—we’ll be breaking down each company in more detail as their potential listing dates approach.